Europe Contrast Media Injectors Market

Market Size in USD Million

CAGR :

%

USD

925.81 Million

USD

1,555.38 Million

2025

2033

USD

925.81 Million

USD

1,555.38 Million

2025

2033

| 2026 –2033 | |

| USD 925.81 Million | |

| USD 1,555.38 Million | |

| % | |

|

Europe Contrast Media Injectors Market Size

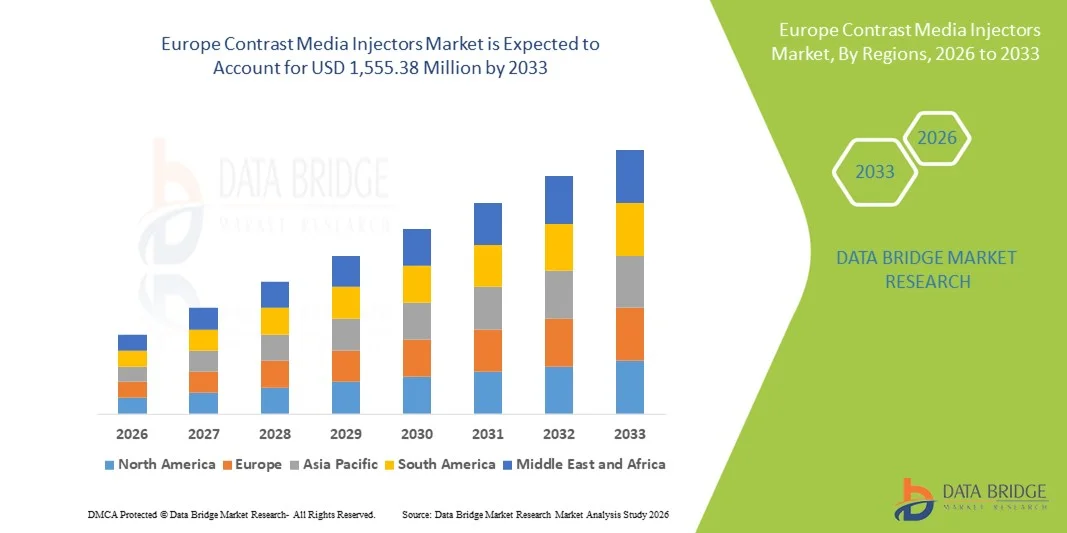

- The Europe contrast media injectors market size was valued at USD 925.81 million in 2025 and is expected to reach USD 1,555.38 million by 2033, at a CAGR of 6.70% during the forecast period

- The market growth is largely driven by the rising prevalence of chronic diseases such as cardiovascular disorders, cancer, and neurological conditions, leading to increased demand for diagnostic imaging procedures including CT, MRI, and angiography across European healthcare facilities

- Furthermore, ongoing technological advancements in dual-head and automated injector systems, growing adoption of minimally invasive diagnostic techniques, and expanding healthcare infrastructure across Western and Eastern Europe are strengthening product penetration, thereby significantly supporting the region’s market expansion

Europe Contrast Media Injectors Market Analysis

- Contrast media injectors, essential devices used in diagnostic imaging to deliver precise contrast agents during CT, MRI, and interventional procedures, are increasingly vital across hospitals and imaging centers in Europe due to rising demand for high‑quality diagnostics, growing chronic disease prevalence, and the shift toward minimally invasive procedures that require accurate and automated contrast delivery

- The escalating demand for contrast media injectors in Europe is primarily fueled by well‑established healthcare systems, stringent regulatory frameworks emphasizing safety and performance, increasing healthcare investments, and rising awareness of early disease detection through advanced imaging technologies, all of which drive adoption of both injector systems and consumables

- Germany dominated the Europe contrast media injectors market in 2025, with an estimated revenue share of 31.3%, supported by high procedural volumes, advanced imaging infrastructure, and a strong medical device manufacturing presence

- The United Kingdom is expected to be the fastest‑growing country in the Europe contrast media injectors market during the forecast period, owing to rapid adoption of modern imaging facilities, government initiatives to improve hospital efficiency, and increasing use of advanced injector types in both diagnostic and interventional procedures

- Dual-head injectors dominated the market in 2025 with a share of 44.9% driven by their ability to deliver precise and simultaneous injection of contrast agents and saline, reducing procedure time, minimizing human error, improving workflow efficiency, and supporting complex diagnostic and interventional imaging procedures in hospitals and diagnostic centers

Report Scope and Europe Contrast Media Injectors Market Segmentation

|

Attributes |

Europe Contrast Media Injectors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Contrast Media Injectors Market Trends

Automation and Digital Integration Enhancing Diagnostic Precision

- A significant and accelerating trend in the Europe contrast media injectors market is the integration of automation and digital platforms with injector systems, enhancing workflow efficiency, dosing accuracy, and patient safety across diagnostic and interventional procedures

- For instance, dual-head injectors equipped with automated software can deliver precise volumes of contrast and saline simultaneously, reducing procedure time and minimizing human error in high-volume radiology departments

- Digital integration allows injectors to interface with hospital PACS (Picture Archiving and Communication Systems) and radiology information systems, enabling centralized monitoring, dose tracking, and real-time alerts for abnormal injection parameters

- The seamless connectivity of injector systems with hospital digital infrastructure facilitates standardized protocols and improved compliance with safety regulations, streamlining operations across multiple imaging modalities

- This trend towards automation, connectivity, and precision is reshaping expectations for imaging equipment, with companies such as MEDRAD developing injector systems that offer programmable protocols, real-time monitoring, and compatibility with advanced imaging software

- The demand for injector systems that combine automation and digital integration is growing rapidly across hospitals, diagnostic centers, and ambulatory surgery centers, as healthcare providers increasingly prioritize efficiency, accuracy, and patient safety

- Adoption of AI-assisted injectors capable of analyzing historical injection data to optimize contrast flow and timing is emerging as a trend to further improve diagnostic outcomes and patient safety

Europe Contrast Media Injectors Market Dynamics

Driver

Increasing Demand Due to Rising Imaging Procedures and Healthcare Investments

- The rising volume of diagnostic imaging procedures across Europe, coupled with growing investments in healthcare infrastructure, is a significant driver for the heightened demand for contrast media injectors

- For instance, in March 2025, Bracco Imaging announced expansion of its automated injector portfolio to European hospitals, aiming to support high-volume CT and interventional imaging workflows efficiently

- As chronic disease prevalence rises, hospitals and diagnostic centers increasingly require precise and reliable contrast delivery for accurate imaging, driving adoption of dual-head and syringeless injector systems

- Furthermore, government initiatives to modernize hospitals and implement standardized imaging protocols are making automated and digitally integrated injectors essential for clinical efficiency and patient safety

- Features such as programmable injection protocols, real-time monitoring, and dose tracking provide healthcare providers with enhanced control, accuracy, and workflow optimization, propelling injector system adoption

- Increasing preference for minimally invasive procedures in interventional cardiology and radiology is boosting demand for high-precision injector systems

- Strategic partnerships between injector manufacturers and imaging equipment providers are expanding the availability and adoption of advanced injector solutions across European hospitals and diagnostic centers

Restraint/Challenge

Operational Complexity and High Capital Investment

- The relatively high initial cost of advanced injector systems, including dual-head and digitally integrated platforms, can limit adoption among budget-conscious hospitals and smaller diagnostic centers

- For instance, the integration of injector systems with hospital IT infrastructure may require specialized training for radiology staff, increasing operational complexity and short-term implementation costs

- Operational downtime due to system maintenance or software updates can disrupt high-volume imaging schedules, posing a challenge for healthcare providers relying on injector reliability

- While cost reductions are occurring, the perceived premium for automated and digitally integrated injectors may hinder rapid adoption in certain European markets with constrained healthcare budgets

- Overcoming these challenges through staff training, scalable deployment options, and cost-effective injector solutions will be vital for sustained growth across hospitals, diagnostic centers, and ambulatory surgery centers

- Regulatory compliance and the need for periodic validation of injector performance can slow adoption, especially in smaller imaging centers with limited technical resources

- Limited awareness of advanced injector features among healthcare professionals can reduce the perceived value, requiring educational initiatives and demonstration programs by manufacturers

Europe Contrast Media Injectors Market Scope

The market is segmented on the basis of product, type, application, and end use.

- By Product

On the basis of product, the Europe contrast media injectors market is segmented into injector systems and consumables. The injector systems segment dominated the market in 2025 with the largest revenue share of 67%, driven by hospitals and diagnostic centers prioritizing precise, reliable, and automated contrast delivery for CT, MRI, and interventional procedures. Injector systems are preferred due to their ability to standardize injection protocols, reduce human error, and integrate with hospital PACS and radiology information systems. Healthcare providers increasingly adopt dual-head and programmable systems to manage high procedural volumes efficiently. The segment also benefits from frequent upgrades and replacement cycles, as institutions invest in digital and automated imaging technologies. Furthermore, advanced injector systems with real-time monitoring enhance patient safety and workflow productivity, supporting their strong market presence.

The consumables segment is expected to witness the fastest growth from 2026 to 2033, driven by the rising use of disposable syringes, contrast media lines, and connectors in hospitals and ambulatory surgery centers. Increasing concerns regarding cross-contamination and infection control are accelerating the adoption of single-use consumables. Consumables also experience steady demand due to recurring needs in high-volume imaging procedures. Their cost-effectiveness and compatibility with multiple injector systems further encourage uptake. The rising preference for outpatient and ambulatory imaging procedures, which rely heavily on disposable consumables, also contributes to segment growth.

- By Type

On the basis of type, the market is segmented into single-head injectors, dual-head injectors, and syringeless injectors. The dual-head injectors segment dominated the market in 2025 with a share of 44.9%, driven by their ability to deliver simultaneous contrast and saline injections accurately, reducing procedure time and enhancing operational efficiency in high-volume imaging centers. Dual-head injectors are highly valued in hospitals and diagnostic centers for interventional cardiology and radiology, where precise dosing is critical. Their compatibility with automation and digital monitoring systems allows seamless integration with hospital imaging workflows. In addition, dual-head injectors minimize errors associated with manual injections, improving patient safety. Their growing adoption is further supported by government and institutional investments in advanced imaging technologies, establishing them as the dominant injector type in Europe.

The syringeless injectors segment is expected to witness the fastest growth during 2026–2033 due to increasing adoption in outpatient diagnostic centers and ambulatory surgery centers, where compact, easy-to-use systems are preferred. Syringeless injectors reduce procedural setup time and allow faster patient throughput, making them ideal for smaller facilities. They also minimize maintenance requirements and reduce operational costs compared to traditional systems. Rising awareness of infection control and environmental sustainability benefits from reduced waste handling also drives growth. In addition, their integration with digital dose-tracking systems ensures accuracy and compliance, increasing their popularity in emerging clinical settings.

- By Application

On the basis of application, the Europe contrast media injectors market is segmented into radiology, interventional cardiology, and interventional radiology. The radiology segment dominated the market in 2025 with a share of 55%, driven by high procedural volumes in hospitals and diagnostic centers performing CT and MRI scans. Radiology departments prioritize accuracy, workflow efficiency, and patient safety, which are facilitated by automated dual-head injector systems. The segment benefits from recurring demand due to routine imaging for chronic disease monitoring and preventive diagnostics. Integration with PACS and radiology information systems enhances operational efficiency. In addition, radiology departments are early adopters of AI-assisted injectors that optimize injection timing and dosage, strengthening the segment’s dominance.

The interventional cardiology segment is expected to witness the fastest growth during 2026–2033 due to increasing minimally invasive procedures and rising prevalence of cardiovascular diseases across Europe. Injector systems in this segment must deliver precise contrast volumes in real-time, enhancing imaging accuracy during catheter-based interventions. Growing investments in specialized cath labs and high patient throughput are boosting adoption. Compact dual-head and syringeless injectors are increasingly preferred for interventional cardiology procedures, especially in outpatient and ambulatory settings. Awareness of radiation dose reduction and workflow optimization also drives growth in this segment.

- By End Use

On the basis of end use, the market is segmented into hospitals, diagnostic centers, and ambulatory surgery centers (ASCs). The hospitals segment dominated the market in 2025 with a share of 61%, driven by their high procedural volumes, extensive diagnostic imaging infrastructure, and the need for reliable, automated, and digitally integrated injector systems. Hospitals invest in dual-head and AI-assisted injectors to standardize imaging protocols, improve patient safety, and enhance workflow efficiency. Advanced injector systems also support interventional cardiology and radiology applications within hospital settings, further solidifying their dominance. The segment benefits from recurring demand and frequent upgrades as hospitals modernize imaging departments.

The ambulatory surgery centers (ASCs) segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising trend of outpatient minimally invasive procedures and increasing preference for same-day imaging diagnostics. ASCs favor compact, easy-to-use, and cost-effective injector systems that reduce setup time and operational complexity. Syringeless and dual-head injectors are particularly suitable for these facilities, allowing efficient patient throughput. Growing patient demand for convenience and quick procedures, coupled with infection control requirements, is accelerating adoption in ASCs. In addition, integration with digital monitoring platforms enhances accuracy and compliance in outpatient settings, driving rapid growth.

Europe Contrast Media Injectors Market Regional Analysis

- Germany dominated the Europe contrast media injectors market in 2025, with an estimated revenue share of 31.3%, supported by high procedural volumes, advanced imaging infrastructure, and a strong medical device manufacturing presence

- Healthcare providers in the region highly value precision, workflow efficiency, and patient safety offered by modern injector systems, along with seamless integration with hospital PACS and radiology information systems

- This widespread adoption is further supported by robust public healthcare investment, advanced interventional radiology and cardiology programs, and increasing awareness of the benefits of automated and digitally integrated injector solutions, establishing Europe as a key market for both hospitals and diagnostic centers

The Germany Contrast Media Injectors Market Insight

The Germany contrast media injectors market dominated Europe in 2025, capturing the largest revenue share of 31.3%, fueled by advanced hospital infrastructure, high imaging volumes, and strong adoption of automated and dual-head injector systems. Germany’s emphasis on innovation, digital integration, and patient safety promotes adoption in both public and private healthcare facilities. Hospitals and diagnostic centers favor injector systems with real-time monitoring and programmable protocols to standardize contrast delivery. Increasing interventional procedures in cardiology and radiology, coupled with frequent upgrades of imaging departments, support sustained market growth.

France Contrast Media Injectors Market Insight

The France contrast media injectors market accounted for 26% of Europe’s revenue in 2025, driven by modernization of hospital imaging facilities, growing outpatient diagnostic centers, and adoption of dual-head and syringeless injectors. French healthcare providers are investing in automated systems to improve procedural efficiency and enhance patient safety. The demand is further supported by government initiatives encouraging digitalization and standardization of diagnostic protocols. Both radiology and interventional procedures are seeing increased adoption of precision injector systems.

United Kingdom Contrast Media Injectors Market Insight

The United Kingdom contrast media injectors market is expected to grow at a noteworthy CAGR during the forecast period, driven by expansion of hospital networks, rising interventional procedures, and growing outpatient and ambulatory surgery center adoption. Increasing cardiovascular disease prevalence and emphasis on workflow optimization are promoting automated injector adoption. The UK’s strong healthcare infrastructure, integration of injectors with hospital IT systems, and preference for dual-head and AI-assisted injectors are supporting sustained growth. The country is also emerging as the fastest-growing injector market in Europe due to government programs improving hospital efficiency and imaging accuracy.

Italy Contrast Media Injectors Market Insight

The Italy contrast media injectors market is gaining traction due to rising imaging volumes, particularly in interventional radiology and cardiology procedures. Investments in hospital modernization, digitalization of radiology departments, and adoption of dual-head and syringeless injector systems are key growth factors. Italian healthcare providers increasingly prefer automated systems to optimize contrast dosing, improve safety, and reduce procedure time. Regional initiatives promoting outpatient diagnostic centers and ambulatory surgery facilities further support market expansion.

Europe Contrast Media Injectors Market Share

The Europe Contrast Media Injectors industry is primarily led by well-established companies, including:

- ulrich medical (Germany)

- MEDTRON AG (Germany)

- Guerbet AG (France)

- GE HealthCare (U.S.)

- Nemoto Kyorindo Co., Ltd. (Japan)

- Mallinckrodt Pharmaceuticals (U.S.)

- Medtron AG (Germany)

- Lantheus Holdings, Inc. (U.S.)

- AngioDynamics, Inc. (U.S.)

- APOLLO RT Co. Ltd (U.S.)

- Magnus Health (U.S.)

- TAEJOON PHARM (South Korea)

- Spago Nanomedical AB (Sweden)

- MedWrench, LLC (U.S.)

- Anaecon India Health Care Pvt. Ltd. (India)

- Shenzhen Anke High-Tech Co., Ltd. (China)

- Bayer AG (Germany)

- Bracco Imaging S.p.A (Italy)

- ACIST Medical Systems (U.S.)

What are the Recent Developments in Europe Contrast Media Injectors Market?

- In April 2025, University College London Hospitals (UCLH) added ulrich medical injector pumps to improve contrast administration, reporting that the new pumps streamlined workflow by reducing consumable use, allowing a single saline bag to last a full day, and enhancing safety with adjustable injection modes for dynamic studies in MRI imaging

- In March 2025, at the European Congress of Radiology (ECR 2025), Bracco Imaging showcased innovations in contrast media and sustainability, highlighting developments to improve contrast efficiency, reduce environmental impact, and enhance patient safety, reaffirming its leadership in advanced imaging technologies

- In September 2024, syringe‑free contrast media injectors gained more users across Europe, with ulrich medical reporting above‑average sales growth in contrast media injectors for CT and MRI, especially in France where flexible tubing systems were well received for improved efficiency and higher patient throughput

- In July 2024, Ulrich Medical announced extraordinary growth in Europe’s contrast media injector segment, driven by strong adoption of CT motion SPICY and MRI Max 3 injectors that support efficient workflows and multi‑patient use, helping the company increase its European market share

- In May 2023, ulrich medical’s CT motion Spicy contrast media injector received enhanced functionality introductions, including increased pressure and flow performance and digital interfaces to simplify workflow and enable automated injection protocols demonstrated at major European radiology forums

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.