Europe Eclinical Solutions Market

Market Size in USD Billion

USD

2.85 Billion

USD

7.75 Billion

2024

2032

USD

2.85 Billion

USD

7.75 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.85 Billion | |

| USD 7.75 Billion | |

| % | |

|

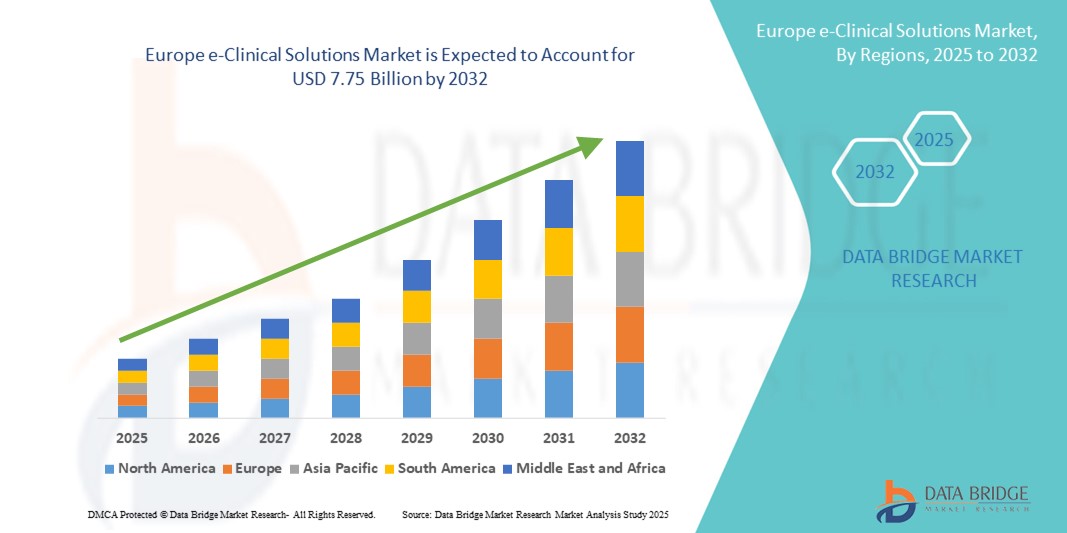

Europe e-Clinical Solutions Market Size

- The Europe e-clinical solutions market size was valued at USD 2.85 billion in 2024 and is expected to reach USD 7.75 billion by 2032, at a CAGR of 13.3% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital clinical trial technologies, rising volume of clinical trials, and stringent regulatory requirements driving efficient data management across pharmaceutical companies and Contract Research Organizations (CROs)

- Furthermore, technological advancements such as cloud computing, artificial intelligence, and decentralized trial models, combined with regulatory support such as the European Health Data Space (EHDS), are enhancing trial efficiency and data accessibility, thereby significantly boosting the adoption of e-Clinical solutions across Europe

Europe e-Clinical Solutions Market Analysis

- e-Clinical solutions, encompassing electronic data capture (EDC), clinical trial management systems (CTMS), and other digital platforms, are increasingly critical for streamlining clinical trials and ensuring regulatory compliance across Europe due to their efficiency, real-time data access, and integration capabilities with decentralized trial models

- The escalating demand for e-Clinical solutions is primarily driven by the rising number of clinical trials, increasing focus on patient-centric research, stringent regulatory requirements, and growing adoption of digital health technologies among pharmaceutical companies and Contract Research Organizations (CROs)

- Germany dominated the e-Clinical solutions market with the largest revenue share of 28.5% in 2024, characterized by a mature pharmaceutical industry, early adoption of digital solutions, and strong regulatory support, with leading companies deploying AI-driven and cloud-based trial management platforms

- France is expected to be the fastest-growing country during the forecast period due to expanding clinical trial activities, increasing healthcare investments, and higher participation in multinational research studies

- Clinical trial management systems (CTMS) segment dominated the Europe e-Clinical solutions market with a market share of 38.5% in 2024, driven by their ability to efficiently plan, track, and manage complex trials while ensuring compliance with evolving regulatory standards

Report Scope and Europe e-Clinical Solutions Market Segmentation

|

Attributes |

Europe e-Clinical Solutions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe e-Clinical Solutions Market Trends

Digital Transformation and AI-Driven Clinical Trials

- A significant and accelerating trend in the European e-Clinical solutions market is the increasing adoption of artificial intelligence (AI) and machine learning in clinical trial management, patient recruitment, and data analysis. These technologies are significantly improving trial efficiency, accuracy, and predictive insights

- For instance, platforms such as Medidata Rave and Oracle Health Sciences’ EDC integrate AI to identify patient eligibility, monitor protocol adherence, and flag anomalies in real time, reducing errors and accelerating trial timelines

- AI-driven analytics in e-Clinical solutions enable predictive modeling, risk-based monitoring, and real-time decision support. For instance, some Medidata and Veeva systems use AI to optimize site selection and forecast patient dropout rates, enhancing trial success rates. Furthermore, advanced cloud-based platforms allow seamless data sharing among study sites, sponsors, and regulators, ensuring faster and more compliant trial execution

- The integration of e-Clinical solutions with decentralized and hybrid trial models facilitates remote patient monitoring, electronic consent, and telemedicine-based follow-ups, creating a unified digital trial experience

- This trend towards intelligent, interconnected, and patient-centric clinical trials is reshaping expectations for trial management, with companies such as Veeva Systems and Oracle Health Sciences expanding AI-enabled offerings for improved operational efficiency and regulatory compliance

- The demand for AI-enhanced and fully integrated e-Clinical platforms is growing rapidly across Europe, driven by pharmaceutical firms, biotech companies, and Contract Research Organizations (CROs) seeking faster, more accurate, and compliant clinical trial operations

Europe e-Clinical Solutions Market Dynamics

Driver

Increasing Clinical Trials and Regulatory Pressure

- The rising number of clinical trials across Europe, coupled with stringent regulatory requirements such as the European Medicines Agency (EMA) guidelines and GDPR compliance, is a significant driver for the adoption of e-Clinical solutions

- For instance, in March 2025, the European Health Data Space (EHDS) initiative emphasized standardized electronic health data usage, prompting pharma companies to adopt integrated e-Clinical platforms for efficient trial management and regulatory reporting

- As organizations seek faster, safer, and more cost-effective trials, e-Clinical solutions provide features such as real-time monitoring, risk-based site management, and electronic source data verification, offering clear advantages over traditional manual processes

- Furthermore, the adoption of decentralized and hybrid trial models is making e-Clinical solutions essential for enabling remote patient monitoring, virtual visits, and real-time compliance tracking

- The combination of regulatory pressure, technological advances, and the need for operational efficiency is accelerating the uptake of cloud-based, AI-enabled, and fully integrated e-Clinical platforms across European pharmaceutical and biotech sectors

Restraint/Challenge

Data Privacy Concerns and High Implementation Costs

- Concerns surrounding patient data privacy, compliance with GDPR, and cybersecurity vulnerabilities in digital clinical trial platforms pose a significant challenge to broader market adoption. As e-Clinical solutions involve handling sensitive health data, companies must implement robust encryption, secure access protocols, and regular audits

- For instance, high-profile incidents of health data breaches in Europe have made some organizations hesitant to fully digitize trial management, particularly for multinational studies

- Addressing these data privacy and security concerns through advanced encryption, secure cloud storage, and staff training is crucial for building trust among sponsors and regulators. In addition, the relatively high initial cost of sophisticated e-Clinical platforms can be a barrier for small biotech firms and CROs with limited budgets

- While scalable cloud-based solutions are gradually lowering barriers, premium features such as AI-driven predictive analytics, integrated patient monitoring, or electronic patient-reported outcome (ePRO) tools often come with a higher price tag

- Overcoming these challenges through enhanced cybersecurity measures, compliance support, and cost-effective platform models will be vital for sustained growth in the European e-Clinical solutions market

Europe e-Clinical Solutions Market Scope

The market is segmented on the basis of product, delivery mode, clinical trial phase, organization size, user device, and end user.

- By Product

On the basis of product, the Europe e-Clinical solutions market is segmented into electronic data capture and clinical trial data management systems, clinical trial management systems (CTMS), clinical analytics platforms, care coordination medical records (CCMR), randomization and trial supply management, clinical data integration platforms, electronic clinical outcome assessment solutions, safety solutions, electronic trial master file systems, regulatory information management solutions, and others. The clinical trial management systems (CTMS) segment dominated the market with the largest revenue share of 38.5% in 2024, driven by its ability to efficiently plan, track, and manage complex trials while ensuring regulatory compliance. Pharmaceutical companies and CROs often prioritize CTMS for its comprehensive trial oversight, centralized data management, and integration with other e-Clinical systems. The segment also benefits from increasing adoption in large-scale multinational trials, where robust workflow automation and risk-based monitoring are critical.

The clinical analytics platforms segment is anticipated to witness the fastest CAGR of 17.5% from 2025 to 2032, fueled by growing demand for AI-driven insights, predictive analytics, and real-time decision support in clinical trials. The ability to analyze large datasets, identify trends, and optimize trial performance makes these platforms highly attractive for sponsors seeking improved operational efficiency and trial success rates. With the increasing complexity of clinical trials and the vast volume of data generated, clinical analytics solutions are becoming indispensable for improving trial outcomes and operational efficiency.

- By Delivery Mode

On the basis of delivery mode, the Europe e-Clinical solutions market is segmented into web-hosted (on-demand) solutions, licensed enterprise (on-premises) solutions, and cloud-based (SaaS) solutions. Cloud-Based (SaaS) Solutions held the largest market share of 42% in 2024 due to their scalability, lower upfront costs, remote accessibility, and seamless integration with decentralized trial operations. These solutions are particularly popular among CROs and mid-sized pharmaceutical companies seeking rapid deployment and flexible subscription models.

Web-Hosted (On-Demand) Solutions are expected to witness the fastest growth from 2025 to 2032, driven by the need for agile, cost-effective deployment, and the growing adoption of hybrid and decentralized clinical trial models across Europe. These solutions allow stakeholders including sponsors, investigators, and patients to access trial data securely from any location, improving trial efficiency and reducing operational delays

- By Clinical Trial Phase

On the basis of clinical trial phase, the Europe e-Clinical solutions market is segmented into phase i, phase ii, phase iii, and phase iv trials. Phase III trials dominated the market with a share of 40% in 2024, attributed to their larger scale, complex data management needs, and higher regulatory scrutiny. Efficient e-Clinical solutions are critical in Phase III trials to ensure real-time monitoring, data quality, and compliance with EMA regulations. e-Clinical solutions facilitate robust data quality assurance, compliance with EMA and local regulations, and streamlined reporting, all of which are essential for the successful execution of late-stage clinical trials.

Phase II trials are expected to grow at the fastest CAGR from 2025 to 2032, driven by the rising number of early-stage trials and the increasing adoption of digital platforms for patient recruitment, protocol adherence, and outcome analysis. These digital interventions reduce trial cycle times, improve accuracy, and allow sponsors to make quicker go/no-go decisions for drug development programs.

- By Organization Size

On the basis of organization size, the Europe e-Clinical solutions market is segmented into small & medium and large organizations. Large organizations dominated the market with a 55% share in 2024, benefiting from greater budgets for advanced e-Clinical platforms, extensive trial portfolios, and higher regulatory compliance requirements. These organizations have the capacity to invest in integrated, AI-enabled, cloud-based, and multi-functional platforms to ensure trial efficiency, maintain regulatory standards, and manage high-volume data.

Small & Medium organizations are anticipated to witness the fastest growth during the forecast period, fueled by cloud-based and SaaS solutions that reduce upfront costs and enable flexible deployment for smaller-scale trials. The rise of cloud-based and SaaS solutions has lowered the entry barriers for SMEs, allowing them to deploy e-Clinical platforms with minimal upfront investments, access advanced analytics tools, and conduct decentralized or hybrid trials efficiently.

- By User Device

On the basis of user device, the Europe e-Clinical solutions market is segmented into desktop, tablet, handheld PDA device, smartphone, and others. Desktop solutions held the largest market share of 45% in 2024, due to their reliability, full-feature access, and suitability for comprehensive trial management tasks performed at research sites and sponsor offices. Desktops remain essential for tasks such as protocol design, trial setup, regulatory reporting, and advanced analytics.

Smartphones and tablets are expected to witness the fastest growth from 2025 to 2032, driven by decentralized trial models, remote monitoring, ePRO data collection, and the need for real-time communication among patients, investigators, and sponsors. Mobile-enabled e-Clinical solutions improve patient engagement, adherence to trial protocols, and enable faster decision-making.

- By End User

On the basis of end user, the Europe e-Clinical solutions market is segmented into pharmaceutical and biopharmaceutical companies, contract research organizations (CROs), consulting service companies, medical device manufacturers, hospitals, and academic research institutes. Pharmaceutical and Biopharmaceutical Companies dominated the market with a 50% share in 2024, due to extensive clinical trial portfolios, regulatory obligations, and the need for robust, integrated e-Clinical platforms.

Contract research organizations (CROs) are expected to grow at the fastest CAGR from 2025 to 2032, driven by increasing outsourcing of clinical trial operations, demand for centralized trial management, and adoption of cloud-based and AI-enabled solutions to optimize trial efficiency and cost-effectiveness. CROs increasingly rely on e-Clinical solutions to manage trials for multiple sponsors simultaneously, optimize workflows, and ensure compliance with European regulatory standards.

Europe e-Clinical Solutions Market Regional Analysis

- Germany dominated the e-Clinical solutions market with the largest revenue share of 28.5% in 2024, characterized by a mature pharmaceutical industry, early adoption of digital solutions, and strong regulatory support, with leading companies deploying AI-driven and cloud-based trial management platforms

- Organizations in the country highly value the efficiency, real-time monitoring, and regulatory compliance offered by e-Clinical solutions, enabling faster and more accurate management of complex clinical trials across multiple sites

- This widespread adoption is further supported by advanced technological infrastructure, a high concentration of Contract Research Organizations (CROs), and growing investment in decentralized and hybrid clinical trials, establishing e-Clinical solutions as a preferred choice for pharmaceutical, biotech, and academic research institutions across Germany

The Germany e-Clinical Solutions Market Insight

Germany dominated the Europe e-Clinical solutions market with the largest revenue share of 28.5% in 2024, fueled by a strong pharmaceutical and biotech sector, advanced healthcare infrastructure, and early adoption of cloud-based and AI-driven e-Clinical platforms. German organizations highly value secure, privacy-compliant solutions and the integration of decentralized and hybrid trial models, supporting both Phase II and Phase III clinical trials. The emphasis on innovation and regulatory compliance continues to make Germany the key contributor to the European market.

France e-Clinical Solutions Market Insight

France is expected to be the fastest-growing country in the Europe e-Clinical solutions market during the forecast period, driven by increasing clinical trial activities, supportive regulatory initiatives, and higher adoption of AI-enabled trial management and analytics platforms. French pharmaceutical companies and CROs are increasingly leveraging e-Clinical solutions to optimize patient recruitment, protocol adherence, and real-time reporting. The growing focus on digitalization and data-driven decision-making is propelling rapid market expansion in France.

U.K. e-Clinical Solutions Market Insight

The U.K. e-Clinical solutions market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the adoption of decentralized trials, robust life sciences ecosystem, and compliance with MHRA and EMA regulations. Pharmaceutical companies and CROs in the U.K. increasingly leverage AI, real-time analytics, and remote monitoring to optimize trial efficiency and reduce operational costs.

Italy e-Clinical Solutions Market Insight

The Italy e-Clinical solutions market is poised to grow steadily during the forecast period, driven by expanding clinical trial activities, increased investment in digital health technologies, and participation in multinational studies. Cloud-based platforms, EDC, and clinical analytics solutions are enhancing operational efficiency for pharmaceutical companies, CROs, and academic research institutes.

Spain e-Clinical Solutions Market Insight

The Spain e-Clinical solutions market is experiencing growth due to increasing adoption of integrated trial management platforms, AI-enabled analytics, and regulatory emphasis on patient data security. The focus on efficient clinical operations and cross-border collaboration within the EU is supporting market demand, particularly in Phase II and Phase III trials.

Europe e-Clinical Solutions Market Share

The Europe e-Clinical Solutions industry is primarily led by well-established companies, including:

- eClinical Solutions LLC (U.S.)

- Oracle Corporation (U.S.)

- Anju Software, Inc. (U.S.)

- Castor EDC (Netherlands)

- Signant Health (U.S.)

- Dassault Systèmes SE (France)

- Medidata Solutions, Inc. (U.S.)

- Parexel International (MA) Corporation (U.S.)

- IQVIA (U.S.)

- Veeva Systems (U.S.)

- RealTime Software Solutions, LLC (U.S.)

- Bioclinica (U.S.)

- CRF Health (U.S.)

- eClinicalWorks (U.S.)

- Maxisit (Germany)

- Clario (U.S.)

- Fountayn (U.S.)

- ICON plc (Ireland)

- Medrio (U.S.)

What are the Recent Developments in Europe e-Clinical Solutions Market?

- In April 2025, Veeva Systems announced the upcoming release of its new Veeva SiteVault CTMS, a clinical trial management system specifically designed for research sites. The initial release is planned for August 2025. This development is significant as it provides research sites with a dedicated, integrated system to manage trials, streamlining site-specific workflows and improving collaboration with sponsors

- In December 2024, eClinical Solutions announced a new collaboration with Snowflake, an AI Data Cloud company. The partnership establishes a bidirectional integration between eClinical's elluminate Clinical Data Cloud and the Snowflake platform. This collaboration is designed to streamline data exchange for life sciences organizations, helping them manage and analyze the growing volume of complex clinical trial data more efficiently. This partnership highlights the increasing focus on creating seamless data ecosystems across different platforms

- In September 2024, eClinical Solutions, a leading provider of digital clinical software and services, announced a majority investment from GI Partners, a private investment firm. This strategic move is intended to accelerate the company’s growth and enhance its AI-powered data products and biometric services. This investment highlights a broader industry trend where private equity firms are investing heavily in e-clinical technology companies to capitalize on the growing demand for data-driven, efficient clinical trials

- In June 2024, Medidata, a Dassault Systèmes company, announced the launch of its Clinical Data Studio. This new AI-powered software platform is designed to streamline clinical trial data management. By leveraging AI and automation, the studio centralizes trial data from various sources, helping to cut review cycles by up to 80% and improve data quality. This launch is a significant step in the industry's shift toward using AI to modernize and accelerate data-related processes in clinical trials

- In February 2021, eClinical Solutions introduced the elluminate CTMS, a cloud-based platform designed to accelerate drug development by streamlining clinical trial processes. The system offers real-time data access, advanced analytics, and enhanced collaboration among clinical teams

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.