Europe Lung Cancer Screening Software Market

Market Size in USD Billion

CAGR :

%

USD

2.80 Billion

USD

11.72 Billion

2025

2033

USD

2.80 Billion

USD

11.72 Billion

2025

2033

| 2026 –2033 | |

| USD 2.80 Billion | |

| USD 11.72 Billion | |

| % | |

|

Europe Lung Cancer Screening Software Market Size

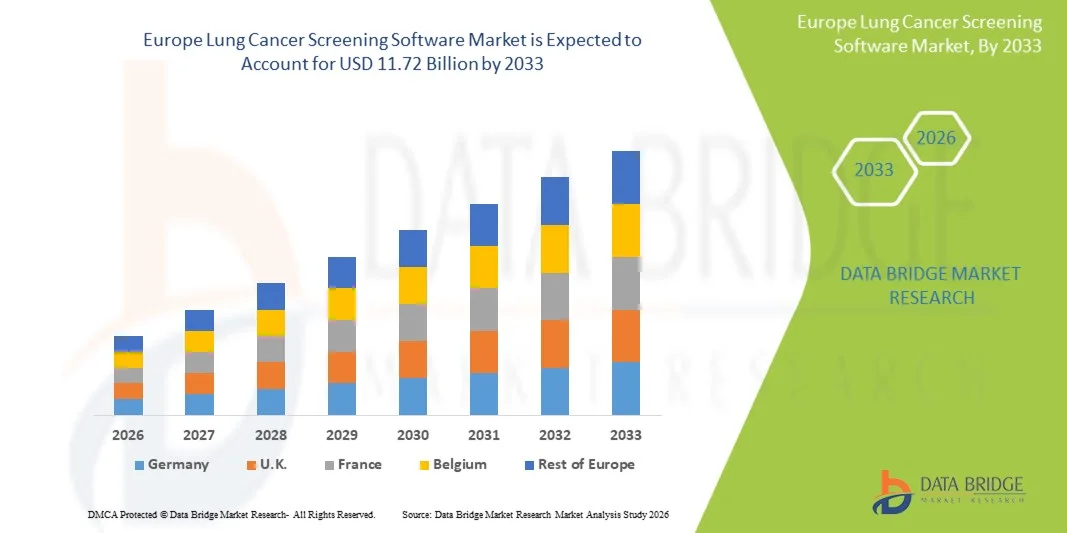

- The Europe lung cancer screening software market size was valued at USD 2.80 billion in 2025 and is expected to reach USD 11.72 billion by 2033, at a CAGR of 19.6% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within AI-powered imaging systems, low-dose CT screening programs, and digital diagnostic platforms, leading to improved early detection capabilities across healthcare systems in Europe

- Furthermore, rising prevalence of lung cancer, increasing government-led screening initiatives, and growing emphasis on early diagnosis and precision medicine are strengthening the adoption of advanced screening software solutions. These converging factors are accelerating the uptake of lung cancer screening technologies, thereby significantly boosting the industry's growth

Europe Lung Cancer Screening Software Market Analysis

- Europe lung cancer screening software solutions, including AI-powered imaging platforms, radiology workflow systems, and integrated diagnostic tools, are becoming essential components of modern oncology care due to their ability to enhance early detection accuracy, streamline clinical workflows, and support large-scale lung cancer screening programs across healthcare systems

- The escalating demand for lung cancer screening software is primarily driven by the rising incidence of lung cancer across Europe, increasing adoption of AI in medical imaging, and expanding government-led screening initiatives aimed at improving early diagnosis and reducing mortality rates

- Germany dominated the Europe lung cancer screening software market with the largest revenue share of 29.6% in 2025, supported by advanced digital healthcare infrastructure, strong adoption of AI-enabled radiology systems, and well-established lung cancer screening programs across major hospital networks

- France is expected to be the fastest growing country in the Europe lung cancer screening software market during the forecast period due to increasing government screening initiatives, rising investment in hospital digital transformation, and growing integration of AI-assisted radiology technologies

- Lung cancer screening radiology solution segment dominated the market with a share of 46.7% in 2025, driven by its critical role in CT image interpretation, high diagnostic accuracy, and strong reliance in clinical decision-making for early-stage lung cancer detection

Report Scope and Europe Lung Cancer Screening Software Market Segmentation

|

Attributes |

Europe Lung Cancer Screening Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Lung Cancer Screening Software Market Trends

“AI-Driven Imaging and Integrated Diagnostic Platforms”

- A significant and accelerating trend in the Europe lung cancer screening software market is the deepening integration of artificial intelligence (AI) with radiology imaging systems and cloud-based diagnostic platforms, significantly improving early detection accuracy and clinical workflow efficiency

- For instance, AI-powered solutions such as lung nodule detection and risk stratification tools are being increasingly integrated into low-dose CT screening programs across leading European hospital networks, enabling faster and more precise diagnosis

- AI integration in lung cancer screening software enables capabilities such as automated lesion detection, predictive risk scoring, and continuous learning from imaging datasets, improving diagnostic consistency and reducing radiologist workload

- The seamless integration of screening software with hospital information systems (HIS), radiology information systems (RIS), and picture archiving and communication systems (PACS) is enabling unified access to patient imaging data and streamlined clinical decision-making

- This trend towards more intelligent, data-driven, and interoperable screening ecosystems is fundamentally reshaping oncology diagnostics, with companies developing advanced AI modules capable of improving early-stage lung cancer detection accuracy

- The demand for integrated lung cancer screening software platforms is growing rapidly across Europe as healthcare providers increasingly prioritize precision diagnostics, early intervention, and large-scale population screening programs

- Furthermore, increasing collaboration between AI developers and healthcare institutions is accelerating the validation and clinical adoption of advanced screening algorithms across European healthcare systems

Europe Lung Cancer Screening Software Market Dynamics

Driver

“Rising Burden of Lung Cancer and Expansion of Screening Programs”

- The increasing prevalence of lung cancer across Europe, coupled with the expansion of national and EU-supported screening initiatives, is a significant driver for the rising demand for lung cancer screening software solutions

- For instance, in April 2025, several European healthcare systems expanded pilot low-dose CT screening programs to improve early detection rates, increasing reliance on advanced software-based diagnostic support tools

- As healthcare providers focus more on early-stage detection and mortality reduction, lung cancer screening software offers critical capabilities such as automated image analysis, risk assessment, and clinical decision support

- Furthermore, the growing adoption of AI-powered radiology tools and digital health transformation initiatives is making screening software an integral part of modern oncology workflows across hospitals and diagnostic centers

- The increasing need for efficient population-scale screening, faster reporting times, and improved diagnostic accuracy is strongly driving the adoption of advanced lung cancer screening software across Europe

- In addition, rising investments from public health agencies and private healthcare providers in preventive oncology programs are further strengthening software deployment across screening networks

Restraint/Challenge

“High Implementation Costs and Data Privacy Compliance Barriers”

- Concerns surrounding high deployment costs and strict regulatory requirements for patient data protection pose a significant challenge to broader adoption of lung cancer screening software in Europe

- For instance, compliance with stringent frameworks such as GDPR requires advanced data security, anonymization, and storage protocols, increasing operational complexity for software providers and healthcare institutions

- Addressing these regulatory challenges through secure cloud architectures, encrypted data exchange, and compliance-focused software design is essential for building trust among healthcare providers and patients

- In addition, the high cost of integrating AI-based screening platforms with existing hospital IT infrastructure can be a barrier for smaller healthcare facilities and developing healthcare systems within Europe

- While adoption is increasing, budget constraints and long procurement cycles can still limit rapid deployment of advanced screening software solutions, particularly in public healthcare settings

- Furthermore, interoperability issues between legacy hospital systems and modern AI-based screening platforms continue to slow down seamless digital transformation across certain healthcare networks

Europe Lung Cancer Screening Software Market Scope

The market is segmented on the basis of mode of delivery, product, type, application, platform, purchase mode, end user, and distribution channel.

- By Mode of Delivery

On the basis of mode of delivery, the Europe lung cancer screening software market is segmented into cloud-based solutions, on-premise solutions, and web-based solutions. The cloud-based solutions segment dominated the market with the largest revenue share of 48.6% in 2025, driven by increasing reliance on scalable healthcare IT infrastructure and easy remote access to imaging and patient data across hospitals and diagnostic centers. Cloud deployment enables seamless integration with AI-based diagnostic tools, faster updates, and centralized data management, making it highly suitable for large-scale screening programs. In addition, reduced infrastructure costs and improved interoperability with hospital systems such as PACS and RIS further strengthen its dominance. Healthcare providers across Europe prefer cloud models for real-time collaboration and efficient handling of large imaging datasets generated from low-dose CT screening.

The on-premise solutions segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by increasing concerns over data privacy, cybersecurity risks, and strict regulatory compliance such as GDPR. Hospitals and government institutions prefer on-premise deployment for full control over sensitive patient data and better customization of software systems. It also ensures higher security for medical imaging records and reduces dependency on external cloud infrastructure. Furthermore, large healthcare organizations investing in internal IT modernization are increasingly adopting on-premise solutions for long-term operational stability and compliance assurance.

- By Product

On the basis of product, the market is segmented into lung cancer screening radiology solution, lung cancer screening patient management software, nodule management software, data collection and reporting, patient coordination and workflow, lung nodule computer-aided detection, pathology and cancer staging, statistical audit reporting, screening PACS, and practice management and audit log tracking. The lung cancer screening radiology solution segment dominated the market with a revenue share of 46.7% in 2025, due to its critical role in CT image interpretation and early lung nodule detection across screening programs. It is widely adopted in hospitals because it integrates AI-assisted imaging analysis with radiologist workflows, improving diagnostic accuracy and reducing interpretation time. Strong dependence on radiology workflows for early cancer detection and increasing implementation of structured reporting systems further support segment dominance. Growing integration with PACS and RIS systems also enhances operational efficiency in clinical environments.

The lung nodule computer-aided detection segment is expected to witness the fastest growth rate of 20.4% from 2026 to 2033, driven by rapid advancements in AI algorithms and increasing demand for automated diagnostic support tools. These systems assist radiologists in detecting small and complex nodules that may be missed in manual analysis. Rising clinical validation of AI-based CAD tools and increasing pressure on healthcare systems to improve early detection rates are accelerating adoption. In addition, growing investment in machine learning-based imaging solutions across European healthcare systems is further boosting segment expansion.

- By Type

On the basis of type, the market is segmented into computer-assisted screening and traditional screening. The computer-assisted screening segment dominated the market with the largest revenue share of 72.3% in 2025, driven by widespread adoption of AI-enabled imaging tools and increasing implementation of structured lung cancer screening programs across Europe. These systems provide higher diagnostic accuracy, faster image interpretation, and improved consistency in detecting early-stage lung abnormalities. Healthcare providers increasingly prefer computer-assisted methods due to reduced radiologist workload and enhanced efficiency in handling large screening volumes. Government initiatives promoting digital healthcare transformation further support segment dominance.

The traditional screening segment is expected to witness the fastest growth rate of 16.7% from 2026 to 2033, mainly due to its continued use in smaller hospitals and diagnostic centers with limited access to advanced AI infrastructure. Many healthcare facilities still rely on conventional radiology workflows due to budget constraints and lack of technical expertise. However, gradual modernization of healthcare systems and hybrid adoption of digital tools are contributing to steady growth. Traditional screening remains relevant in regions where full-scale AI integration is still under development.

- By Application

On the basis of application, the market is segmented into non-small cell lung cancer (NSCLC) and small cell lung cancer (SCLC). The NSCLC segment dominated the market with the largest revenue share of 81.5% in 2025, driven by its high prevalence across Europe and strong focus of screening programs on early detection of non-small cell lung cancer cases. NSCLC cases form the majority of lung cancer diagnoses, leading to higher utilization of screening software for nodule detection, staging, and patient monitoring. Increasing adoption of AI tools for early-stage NSCLC detection further strengthens segment leadership. In addition, improved survival rates with early diagnosis encourage continued investment in NSCLC screening technologies.

The SCLC segment is expected to witness the fastest growth rate of 17.8% from 2026 to 2033, driven by rising awareness of aggressive cancer types requiring rapid diagnosis and treatment planning. Although less common, SCLC progresses quickly, increasing the need for advanced imaging and automated detection tools. AI-based screening systems are increasingly being optimized for early identification of small and fast-growing lesions. Expanding clinical research and improved imaging sensitivity are also supporting segment growth.

- By Platform

On the basis of platform, the market is segmented into standalone and integrated systems. The integrated platform segment dominated the market with a revenue share of 63.9% in 2025, driven by strong demand for interoperability with hospital systems such as PACS, RIS, and electronic health records (EHR). Integrated systems allow seamless data exchange across departments, improving workflow efficiency and diagnostic coordination. Healthcare providers prefer integrated platforms for unified patient data access and centralized imaging management. The growing adoption of enterprise imaging solutions across European hospitals further strengthens segment dominance.

The standalone platform segment is expected to witness the fastest growth rate of 18.2% from 2026 to 2033, driven by increasing adoption in small clinics and diagnostic centers that require cost-effective and easy-to-deploy solutions. These platforms offer flexibility, lower implementation complexity, and faster deployment compared to integrated systems. Standalone solutions are particularly attractive for pilot screening programs and private diagnostic facilities. Rising demand for subscription-based and modular software models is further supporting segment expansion.

- By Purchase Mode

On the basis of purchase mode, the market is segmented into institutional and individual. The institutional segment dominated the market with the largest revenue share of 88.4% in 2025, driven by large-scale procurement by hospitals, government healthcare systems, and oncology centers implementing national screening programs. Institutional buyers prefer comprehensive, scalable, and compliant software solutions capable of handling population-level screening data. Strong public healthcare funding across Europe further strengthens institutional adoption. Long-term contracts and bundled service agreements also contribute to this segment’s dominance.

The individual segment is expected to witness the fastest growth rate of 19.1% from 2026 to 2033, driven by increasing adoption among private practitioners and small diagnostic clinics. Rising awareness of AI-based screening tools and growing availability of subscription-based models are encouraging individual adoption. Telemedicine expansion and digital diagnostic platforms are further supporting this segment’s growth. Furthermore, digital transformation of healthcare systems is accelerating institutional adoption.

- By End User

On the basis of end user, the market is segmented into oncology centers, hospitals, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share of 57.8% in 2025, driven by high patient volumes, advanced imaging infrastructure, and strong integration of AI-based screening systems within radiology departments. Hospitals act as primary centers for lung cancer diagnosis and screening programs, making them the largest adopters of screening software. Availability of multidisciplinary care teams and structured diagnostic workflows further strengthens hospital dominance.

The oncology centers segment is expected to witness the fastest growth rate of 20.6% from 2026 to 2033, driven by increasing specialization in cancer care and rising demand for precision oncology solutions. These centers are increasingly adopting advanced AI-based screening software for early detection and treatment planning. Growing investment in cancer-specific healthcare infrastructure and improved diagnostic accuracy tools are also supporting segment growth. Moreover, collaboration between oncology centers and AI vendors is accelerating adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market with the largest revenue share of 74.2% in 2025, driven by bulk procurement by government healthcare systems and public hospitals across Europe. Direct purchasing enables better pricing control, customized solutions, and long-term service agreements with software providers. National screening programs often rely on direct vendor contracts to ensure standardization and compliance.

The third-party distributors segment is expected to witness the fastest growth rate of 17.4% from 2026 to 2033, driven by increasing demand from smaller hospitals and diagnostic centers. Distributors help in local deployment, training, and technical support, making software adoption easier in fragmented healthcare settings. Expanding market penetration in emerging healthcare facilities is further accelerating this segment’s growth. Moreover, expansion of public-private partnerships is strengthening direct distribution channels.

Europe Lung Cancer Screening Software Market Regional Analysis

- Germany dominated the Europe lung cancer screening software market with the largest revenue share of 29.6% in 2025, supported by advanced digital healthcare infrastructure, strong adoption of AI-enabled radiology systems, and well-established lung cancer screening programs across major hospital networks

- Healthcare providers in the country are increasingly implementing lung cancer screening software to improve early detection accuracy, reduce diagnostic delays, and enhance workflow efficiency across radiology departments

- This widespread adoption is further supported by high healthcare expenditure, rapid integration of cloud-based diagnostic platforms, and strong collaboration between hospitals and medical imaging technology providers, establishing Germany as the key regional leader in Europe

The Germany Lung Cancer Screening Software Market Insight

The Germany lung cancer screening software market accounted for the largest revenue share in Europe in 2025, attributed to its advanced healthcare infrastructure, early adoption of AI-enabled diagnostic imaging, and strong implementation of structured lung cancer screening programs. Hospitals across Germany are increasingly deploying intelligent radiology software to improve early-stage detection and reduce diagnostic turnaround time. Strong investment in healthcare digitalization and precision medicine is further supporting market leadership. In addition, collaboration between hospitals and medical imaging technology providers is accelerating software integration across clinical workflows.

United Kingdom Lung Cancer Screening Software Market Insight

The United Kingdom lung cancer screening software market is anticipated to grow at a significant CAGR during the forecast period, driven by expansion of national lung cancer screening programs and increasing use of AI in radiology diagnostics. Healthcare providers are adopting advanced screening platforms to enhance early detection accuracy and improve patient outcomes. Rising investment in digital health transformation and cloud-based diagnostic systems is further supporting market growth. In addition, strong focus on preventive healthcare and early intervention strategies is accelerating adoption across hospitals and diagnostic centers.

France Lung Cancer Screening Software Market Insight

The France lung cancer screening software market is expected to expand at a substantial CAGR during the forecast period, driven by increasing government-led screening initiatives and pilot programs focused on early lung cancer detection. Hospitals are increasingly adopting AI-powered imaging tools to improve radiology efficiency and diagnostic precision. Rising investment in healthcare modernization and digital imaging infrastructure is further strengthening market growth. In addition, growing awareness of lung cancer risks is encouraging wider adoption of advanced screening software solutions.

Italy Lung Cancer Screening Software Market Insight

The Italy lung cancer screening software market is witnessing steady growth due to increasing focus on early cancer detection and gradual adoption of AI-based radiology systems. Healthcare institutions are integrating advanced screening software to improve diagnostic workflows and reduce reporting delays. Government support for healthcare digitalization and rising investment in hospital infrastructure are further contributing to market expansion. In addition, growing awareness of preventive oncology is encouraging adoption across public and private healthcare facilities.

Europe Lung Cancer Screening Software Market Share

The Europe Lung Cancer Screening Software industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Fujifilm Holdings Corporation (Japan)

- Agfa-Gevaert N.V. (Belgium)

- Carestream Health, Inc. (U.S.)

- TeraRecon, Inc. (U.S.)

- Riverain Technologies LLC (U.S.)

- Median Technologies (France)

- Esaote S.p.A. (Italy)

- Visage Imaging GmbH (Germany)

- MeVis Medical Solutions AG (Germany)

- Riverain Technologies LLC (U.S.)

- Coreline Soft Co., Ltd. (South Korea)

- Lunit Inc. (South Korea)

- AZmed SAS (France)

- Thirona B.V. (Netherlands)

- Aidoc Medical Ltd. (Israel)

- Zebra Medical Vision Ltd. (Israel)

What are the Recent Developments in Europe Lung Cancer Screening Software Market?

- In January 2026, NHS England announced a major AI-enabled lung cancer screening expansion trial aimed at improving early detection using artificial intelligence tools for CT scan analysis and robotic biopsy support. The initiative focuses on identifying small pulmonary nodules earlier and increasing diagnostic accuracy across national screening programs. It is expected to significantly enhance early-stage lung cancer detection rates in the U.K. healthcare system

- In November 2025, Median Technologies showcased its AI-powered lung cancer screening software eyonis® LCS at the RSNA 2025 Annual Meeting, highlighting advancements in AI-driven early detection and diagnostic efficiency. The software is designed to analyze low-dose CT scans and support radiologists in identifying malignant lung nodules at earlier stages

- In November 2025, a peer-reviewed study introduced a new AI system outperforming radiologists in lung nodule detection and cancer risk assessment on low-dose CT scans. The model showed improved accuracy in identifying early-stage cancers and reducing false positives, supporting its potential integration into European screening programs. The findings reinforce rapid innovation in AI-assisted radiology across Europe

- In June 2025, researchers published advancements in AI-based lung cancer screening models demonstrating improved accuracy in CT-based nodule detection and risk prediction. The study highlighted transformer-based AI systems capable of analyzing full lung CT scans for early malignancy detection with higher sensitivity than traditional approaches. This reflects growing European adoption of advanced deep learning tools in screening workflows

- In March 2025, researchers from the University of Liverpool reported that AI-assisted lung cancer screening systems can reduce radiologist workload by up to 79% by accurately ruling out negative low-dose CT scans. The study, published in the European Journal of Cancer, demonstrates how AI integration significantly improves efficiency in lung cancer screening workflows while maintaining diagnostic accuracy

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.