Europe Point Of Care Diagnostics Market

Market Size in USD Billion

USD

9.64 Billion

USD

20.99 Billion

2025

2033

USD

9.64 Billion

USD

20.99 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.64 Billion | |

| USD 20.99 Billion | |

| % | |

|

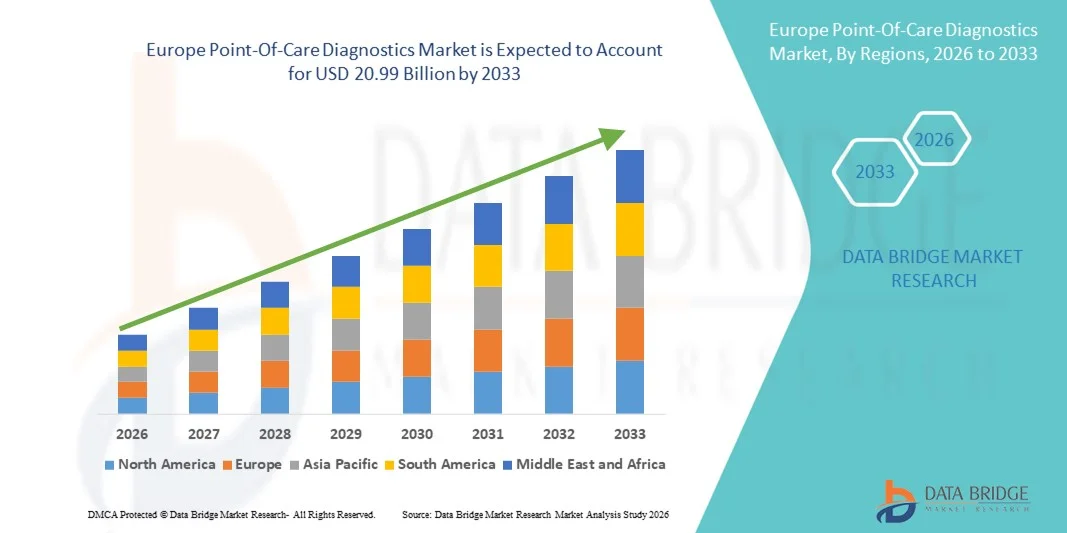

Europe Point-Of-Care Diagnostics Market Size

- The Europe Point-Of-Care Diagnostics market size was valued at USD 9.64 billion in 2025 and is expected to reach USD 20.99 billion by 2033, at a CAGR of 10.22% during the forecast period

- The market growth is largely fueled by the increasing demand for rapid and accurate diagnostic solutions, along with continuous technological advancements in portable and user-friendly testing devices, leading to greater decentralization of healthcare services across hospitals, clinics, and homecare settings

- Furthermore, rising prevalence of infectious and chronic diseases, growing preference for immediate clinical decision-making, and increasing adoption of cost-effective and easy-to-use diagnostic solutions are establishing point-of-care diagnostics as a critical component of modern healthcare delivery. These converging factors are accelerating the uptake of Point-Of-Care Diagnostics solutions, thereby significantly boosting the industry's growth

Europe Point-Of-Care Diagnostics Market Analysis

- Point-of-care diagnostics, offering rapid and on-site testing solutions across hospitals, clinics, emergency care units, and homecare settings, are increasingly vital components of modern healthcare systems due to their ability to deliver immediate results, improve clinical decision-making, and enhance patient outcome

- The escalating demand for point-of-care diagnostics is primarily fueled by the rising prevalence of infectious and chronic diseases, increasing need for decentralized healthcare services, and growing preference for fast, accurate, and cost-effective diagnostic solutions

- U.K. dominated the Point-Of-Care Diagnostics market with the largest revenue share of 37.6% in 2025, characterized by advanced healthcare infrastructure, strong regulatory framework, and high adoption of rapid diagnostic technologies, with the U.K. accounting for the majority share within the region, driven by widespread use of rapid testing kits, molecular diagnostics, and portable immunoassay systems across hospitals and primary care centers

- Germany is expected to be the fastest-growing country in the Point-Of-Care Diagnostics market during the forecast period, expanding at a CAGR of 9.4% from 2026 to 2033, due to increasing investments in diagnostic innovation, rising geriatric population, growing burden of chronic diseases, and rapid integration of digital health technologies in clinical workflows

- The prescription-based testing segment dominated the largest market revenue share of 57.2% in 2025, driven by strong hospital and physician reliance on clinically validated diagnostic tests

Report Scope and Point-Of-Care Diagnostics Market Segmentation

|

Attributes |

Point-Of-Care Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Point-Of-Care Diagnostics Market Trends

Enhanced Technological Advancements and Rapid Testing Integration

- A significant and accelerating trend in the Europe Point-Of-Care Diagnostics market is the growing adoption of rapid, portable, and decentralized diagnostic testing solutions across hospitals, clinics, pharmacies, and home-care settings. This shift is transforming traditional laboratory-dependent testing models by enabling faster clinical decision-making and improving patient management efficiency

- For instance, Abbott’s rapid antigen and molecular point-of-care platforms have been widely deployed across European hospitals and community healthcare centers, allowing physicians to obtain diagnostic results within minutes and initiate timely treatment interventions

- The increasing integration of compact molecular diagnostic systems, handheld analyzers, and multiplex testing platforms is enabling clinicians to detect multiple biomarkers simultaneously at the patient’s bedside, significantly reducing turnaround time compared to centralized laboratory testing

- Decentralized diagnostic solutions are also improving healthcare accessibility in rural and remote areas of Europe, where laboratory infrastructure may be limited, thereby strengthening early disease detection and preventive healthcare strategies

- This transition toward faster, patient-centric testing solutions is reshaping clinical workflows across emergency departments, outpatient clinics, and primary care settings, leading manufacturers to develop more accurate, user-friendly, and compact diagnostic devices

- The demand for rapid and accurate point-of-care diagnostic solutions is expanding steadily across hospitals, ambulatory care centers, and home healthcare environments, as healthcare providers prioritize efficiency, early diagnosis, and improved patient outcomes

Europe Point-Of-Care Diagnostics Market Dynamics

Driver

Rising Prevalence of Infectious and Chronic Diseases

- The increasing burden of infectious diseases, cardiovascular disorders, diabetes, and respiratory conditions across Europe is a major driver accelerating demand for point-of-care diagnostics. Rapid testing enables early detection and timely intervention, which is critical for effective disease management

- For instance, during seasonal influenza outbreaks across Germany and France, hospitals expanded the use of rapid molecular point-of-care testing systems to quickly identify viral infections and reduce patient wait times in emergency departments

- The aging population across European countries is also contributing to rising diagnostic needs, as elderly individuals require frequent monitoring for chronic diseases such as diabetes and cardiovascular conditions

- Government initiatives promoting early disease detection, preventive healthcare, and decentralized testing models are encouraging hospitals and primary care centers to adopt advanced point-of-care diagnostic systems

- In addition, the growing emphasis on reducing hospital admissions and improving outpatient care efficiency is further driving the integration of point-of-care testing devices in routine clinical practice

Restraint/Challenge

High Equipment Costs and Regulatory Complexities

- Despite strong growth potential, high initial costs of advanced point-of-care diagnostic devices and consumables remain a significant barrier, particularly for smaller clinics and resource-constrained healthcare facilities

- For instance, the installation and maintenance of molecular point-of-care analyzers in smaller regional hospitals in Southern Europe can require substantial investment, limiting widespread adoption

- Stringent regulatory requirements under European medical device regulations also increase compliance costs and lengthen product approval timelines for manufacturers

- Furthermore, concerns regarding test accuracy, quality control, and the need for trained healthcare professionals to operate certain advanced systems can restrict deployment in non-hospital settings

- Overcoming these challenges through cost-effective device development, streamlined regulatory pathways, reimbursement support, and improved training programs will be critical for sustained growth of the Europe Point-Of-Care Diagnostics market

Europe Point-Of-Care Diagnostics Market Scope

The market is segmented on the basis of product, platform, prescription, and end user.

- By Product

On the basis of product, the Point-Of-Care Diagnostics market is segmented into glucose monitoring products, cardio metabolic, infectious disease, coagulation, pregnancy and fertility, tumor or cancer marker, urinalysis, cholesterol, haematology, drugs-of-abuse, fecal occult, and others. The glucose monitoring products segment dominated the largest market revenue share of 34.8% in 2025, driven by the rising global prevalence of diabetes and increasing demand for continuous glucose monitoring (CGM) systems. Growing awareness regarding self-monitoring of blood glucose significantly supports segment growth. Technological advancements such as wearable CGM devices enhance patient compliance. Increasing geriatric population and sedentary lifestyles contribute to higher diabetes incidence. Favorable reimbursement policies in developed markets strengthen adoption. Expansion of home-based diagnostic solutions accelerates penetration. Integration with smartphone applications enables real-time tracking and remote physician monitoring. Strong distribution networks and OTC availability further boost sales. Government initiatives promoting diabetes screening programs add momentum. High testing frequency among diabetic patients ensures recurring demand. Continuous innovation in minimally invasive devices supports sustained dominance.

The infectious disease segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2033, fueled by increasing demand for rapid diagnostic tests for COVID-19, influenza, HIV, and other communicable diseases. Rising awareness about early disease detection accelerates adoption. Technological advancements in rapid antigen and molecular testing platforms improve accuracy and turnaround time. Growing healthcare investments in emerging markets enhance accessibility. Expansion of decentralized testing facilities strengthens uptake. Government initiatives supporting epidemic preparedness drive growth. Increasing use of point-of-care molecular diagnostics supports higher precision. Integration with digital health systems improves disease surveillance. Rising international travel and urbanization increase infection risks, supporting demand. Continuous R&D in portable testing kits enhances usability. Expansion of screening programs in outpatient and community settings accelerates adoption. Favorable regulatory approvals further boost CAGR performance.

- By Platform

On the basis of platform, the market is segmented into lateral flow assays (immunochromatography tests), dipsticks, microfluidics, molecular diagnostics, and immunoassays. The lateral flow assays segment dominated the largest market revenue share of 39.5% in 2025, owing to their cost-effectiveness, rapid results, and ease of use in decentralized settings. These assays are widely utilized for pregnancy testing, infectious diseases, and cardiac marker detection. Minimal training requirements enhance adoption in homecare and outpatient settings. Strong demand for rapid antigen tests supports revenue generation. Wide product availability across retail pharmacies strengthens distribution. Portability and short turnaround time increase clinical efficiency. Technological improvements enhance sensitivity and specificity. Government-backed mass screening programs accelerate usage. Compatibility with OTC distribution channels supports sales. Low manufacturing costs enable large-scale production. Growing demand in rural and remote areas reinforces segment leadership.

The molecular diagnostics segment is anticipated to register the fastest CAGR of 15.6% from 2026 to 2033, driven by increasing need for high-sensitivity pathogen detection and genetic testing. Rising adoption of point-of-care PCR systems fuels growth. Technological advancements in microfluidics and nucleic acid amplification improve speed and precision. Growing focus on personalized medicine supports molecular-based testing. Expansion of portable molecular platforms enhances decentralized care. Increasing funding for advanced diagnostic research accelerates innovation. Integration with digital data systems improves clinical decision-making. Rising prevalence of complex infectious diseases boosts demand. Hospitals and critical care centers increasingly adopt molecular PoC devices. Regulatory approvals for rapid PCR kits support market expansion. Continuous innovation reduces device size and cost, improving accessibility.

- By Prescription

On the basis of prescription, the market is segmented into prescription-based testing and OTC testing The prescription-based testing segment dominated the largest market revenue share of 57.2% in 2025, driven by strong hospital and physician reliance on clinically validated diagnostic tests. Regulatory compliance and higher accuracy standards support segment dominance. Hospitals prefer prescription-based tests for critical disease management. Insurance reimbursement policies favor clinically supervised diagnostics. Increasing chronic disease burden boosts physician-directed testing volumes. Integration with electronic health records enhances workflow efficiency. Expanding diagnostic laboratory networks strengthen demand. Continuous technological upgrades improve reliability and accuracy. Growing adoption in emergency and ICU settings sustains revenue growth. Government healthcare funding further supports prescription-based diagnostics.

The OTC testing segment is expected to witness the fastest CAGR of 16.1% from 2026 to 2033, fueled by rising consumer preference for self-testing and home-based healthcare solutions. Increasing awareness regarding preventive health screening drives adoption. Expansion of retail pharmacy networks supports product availability. Technological innovation improves ease of use and accuracy. Smartphone integration enhances result interpretation. Rising demand for privacy and convenience boosts uptake. Growth in e-commerce platforms accelerates distribution. Government initiatives encouraging self-care strengthen adoption. Affordable pricing and compact design improve accessibility. Expansion of telehealth services complements OTC testing growth. Continuous product approvals further drive segment expansion.

- By End User

On the basis of end user, the market is segmented into clinical laboratories, outpatient healthcare and ambulatory care settings, hospitals or critical care centers, home care, research laboratories, and others. The hospitals or critical care centers segment dominated the largest market revenue share of 41.6% in 2025, due to high patient inflow and demand for rapid diagnostic decision-making. Availability of advanced PoC devices supports immediate treatment initiation. Rising emergency admissions increase testing volumes. Integration with hospital information systems enhances workflow. Skilled healthcare professionals ensure proper utilization. Reimbursement coverage supports procurement. Expansion of tertiary care centers strengthens segment growth. Continuous investments in critical care infrastructure drive demand. Growing burden of chronic and infectious diseases sustains usage. Regulatory approvals support hospital adoption.

The home care segment is projected to witness the fastest CAGR of 15.3% from 2026 to 2033, driven by rising preference for decentralized and patient-centric healthcare. Increasing adoption of portable glucose and infectious disease testing kits supports expansion. Aging population and chronic disease prevalence fuel demand. Telemedicine integration enables remote monitoring. Government initiatives promoting home healthcare accelerate growth. Technological advancements improve device portability and user-friendliness. Expanding health awareness campaigns strengthen adoption. Insurance support for home-based testing enhances affordability. Growing availability through online platforms increases accessibility. Continuous innovation in wearable and connected devices sustains strong CAGR growth.

Europe Point-Of-Care Diagnostics Market Regional Analysis

- The Europe point-of-care diagnostics market is projected to expand at a substantial CAGR throughout the forecast period, driven by the rising demand for rapid diagnostic solutions, increasing prevalence of infectious and chronic diseases, and strong regulatory support for advanced medical technologies

- Growing emphasis on decentralized healthcare delivery and early disease detection is accelerating the adoption of portable and rapid diagnostic devices across hospitals, clinics, and community healthcare settings

- The region is witnessing significant expansion in molecular diagnostics, rapid antigen testing, blood glucose monitoring systems, and portable immunoassay platforms, which are increasingly being integrated into routine clinical workflows

U.K. Point-Of-Care Diagnostics Market Insight

The U.K. point-of-care diagnostics market dominated the Point-Of-Care Diagnostics market with the largest revenue share of 37.6% in 2025, supported by its advanced healthcare infrastructure, strong regulatory framework, and high adoption of rapid diagnostic technologies. The country accounts for the majority share within the European region, driven by widespread use of rapid testing kits, molecular diagnostic platforms, and portable immunoassay systems across hospitals, emergency departments, and primary care centers. The increasing burden of chronic diseases such as diabetes and cardiovascular disorders, along with seasonal infectious disease outbreaks, has strengthened the demand for near-patient testing solutions. Additionally, NHS initiatives promoting early diagnosis and faster clinical decision-making are encouraging broader deployment of point-of-care systems. Strong reimbursement structures and investments in healthcare digitization further reinforce the U.K.’s leading position in the regional market.

Germany Point-Of-Care Diagnostics Market Insight

Germany point-of-care diagnostics market is expected to be the fastest-growing country in the Point-Of-Care Diagnostics market during the forecast period, expanding at a CAGR of 9.4% from 2026 to 2033. Growth is driven by increasing investments in diagnostic innovation, a rapidly rising geriatric population, growing prevalence of chronic diseases, and expanding integration of digital health technologies into clinical practice. The country’s well-established hospital infrastructure and strong medical device manufacturing base support the rapid adoption of advanced diagnostic solutions, including molecular point-of-care platforms and compact hematology analyzers. Furthermore, Germany’s focus on healthcare modernization, precision medicine, and digital patient record systems is facilitating seamless integration of rapid diagnostic technologies into routine clinical workflows, positioning the country as the fastest-growing market within Europe.

Europe Point-Of-Care Diagnostics Market Share

The Point-Of-Care Diagnostics industry is primarily led by well-established companies, including:

- Roche Diagnostics (Switzerland)

- Abbott (U.S.)

- Siemens Healthineers (Germany)

- Danaher Corporation (U.S.)

- BD. (U.S.)

- BioMérieux (France)

- QuidelOrtho Corporation (U.S.)

- Thermo Fisher Scientific (U.S.)

- Sysmex Corporation (Japan)

- TSD Biosensor (South Korea)

- Arkray (Japan)

- Chembio Diagnostics (U.S.)

- EKF Diagnostics (U.K.)

- Hologic (U.S.)

- Biomerica (U.S.)

Latest Developments in Europe Point-Of-Care Diagnostics Market

- In March 2021, MatMaCorp launched MYRTA, a handheld real-time PCR point-of-care device capable of performing molecular diagnostics outside traditional labs — enabling rapid pathogen detection directly at patient sites, which was especially useful during ongoing infectious disease responses

- In April 2021, researchers at the Indian Institute of Technology Kharagpur announced the release of a nucleic acid-based point-of-care diagnostic device for COVID-19 detection, designed to provide fast, on-site testing in areas without stable laboratory infrastructure

- In January 2023, Cipla Limited introduced Cippoint, a multi-parameter point-of-care testing device capable of assessing a wide range of health conditions including infections, cardiac markers, metabolic and thyroid functions — expanding the scope of POC testing beyond single disease targets

- In February 2023, bioMérieux received U.S. FDA approval for the BIOFIRE SPOTFIRE Respiratory Panel, a portable POC respiratory pathogen test that delivers rapid identification of multiple viruses and bacteria — enhancing rapid infectious disease diagnosis in clinical settings

- In March 2023, BioLytical Laboratories Inc. obtained Health Canada authorization for its INSTI Multiplex HIV-1/2 Syphilis rapid test, enabling simultaneous, point-of-care screening for two major sexually transmitted— improving screening efficiency in resource-limited environments

- In June 2023, Sysmex Corporation launched an innovative point-of-care antimicrobial susceptibility testing (AST) system in Europe that uses microfluidics to rapidly assess pathogen resistance profiles — an important step toward decentralized antibiotic stewardship diagnostics

- In October 2023, EKF Diagnostics opened a state-of-the-art point-of-care manufacturing facility in the U.S., increasing production capacity for POC diagnostic reagents and devices to meet growing demand across North American markets

- In April 2024, the World Health Organization (WHO) prequalified Cepheid’s Xpert HIV-1 Qual XC POC test, which detects HIV-1 total nucleic acid from dried blood spots and whole blood — expanding global confidence and uptake of decentralized HIV diagnostics

- In May 2024, **the U.S. FDA approved an HPV self-testing kit from F. Hoffmann-La Roche Ltd., enabling women to perform at-home HPV screening — a major step in expanding early cervical cancer detection through accessible point-of-care testing

- In June 2024, bioMérieux received special 510(k) clearance and CLIA waiver for its BIOFIRE SPOTFIRE Respiratory/Sore Throat Panel Mini device, supporting rapid, high-sensitivity POC testing for respiratory and bacterial infections in decentralized settings

- In January 2024, QIAGEN launched new QIAstat-Dx syndromic testing panels in India, providing multiplex point-of-care diagnostics capable of detecting a broad range of infectious disease pathogens within about an hour — significantly enhancing rapid diagnostic capacity in high-demand health systems

- In April 2025, Molbio Diagnostics launched India’s first indigenously developed HPV point-of-care test kit for cervical cancer screening on its Truenat PCR platform, demonstrating local innovation in POC molecular diagnostics validated by top clinical bodies

- In August 2025, Sonic Incytes Medical Corp received FDA 510(k) clearance for Velacur ONE, an AI-guided point-of-care ultrasound elastography device designed for chronic liver disease management — expanding the POC diagnostics category into imaging-assisted assessment tools

- In June 2025, Amazon India launched at-home diagnostics services across six major cities, offering point-of-care health testing services directly to consumers without a clinic visit, reflecting the growing integration of POC diagnostics into consumer health platforms

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.