Europe Radiology Information Systems Ris Market

Market Size in USD Billion

CAGR :

%

USD

532.86 Billion

USD

971.76 Billion

2024

2032

USD

532.86 Billion

USD

971.76 Billion

2024

2032

| 2025 –2032 | |

| USD 532.86 Billion | |

| USD 971.76 Billion | |

| % | |

|

Europe Radiology Information Systems (RIS) Market Size

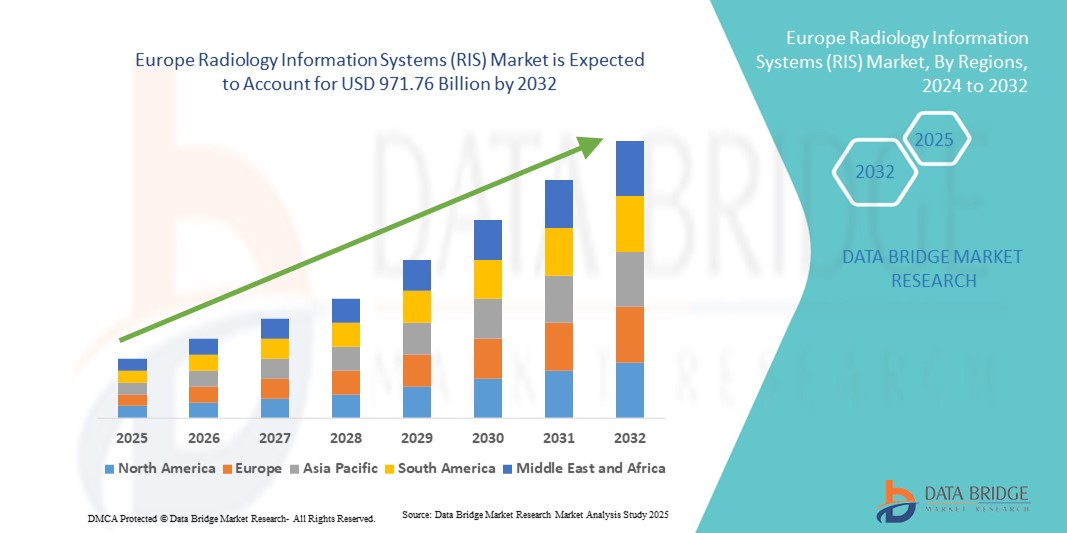

- The Europe radiology information systems (RIS) market size was valued at USD 532.86 billion in 2024 and is expected to reach USD 971.76 billion by 2032, at a CAGR of 7.80% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital healthcare solutions and technological advancements in medical imaging, driving higher integration of RIS with Picture Archiving and Communication Systems (PACS) and Electronic Health Records (EHR). This shift is enhancing workflow efficiency, accuracy, and data accessibility for radiologists and healthcare providers

- Furthermore, rising demand for secure, user-friendly, and interoperable platforms in hospitals and diagnostic centers is establishing RIS as an essential tool for managing imaging data, patient scheduling, and reporting. These converging factors are accelerating the uptake of RIS solutions, thereby significantly boosting the industry's growth

Europe Radiology Information Systems (RIS) Market Analysis

- Radiology Information Systems (RIS) are increasingly vital components of modern healthcare IT infrastructure, enabling efficient management of radiology workflows, scheduling, reporting, and seamless integration with PACS and electronic health records (EHR)

- The escalating demand for Radiology Information Systems (RIS) is primarily fueled by the rising adoption of digital healthcare technologies, growing need for efficient radiology workflow management, and increasing integration of RIS with PACS and electronic health records (EHR)

- The U.K. accounted for 32.5% of the global radiology information systems (RIS) market revenue in 2024. The country has experienced steady adoption of RIS solutions across NHS hospitals and private diagnostic centers, supported by nationwide digital transformation initiatives and increasing emphasis on integrated care systems. Government-led programs promoting electronic health records (EHR) integration, along with the rising implementation of AI-enabled imaging analytics, are enhancing workflow efficiency and diagnostic accuracy. Strong regulatory frameworks, centralized healthcare infrastructure under the NHS, and growing investments in health IT modernization continue to support the U.K.’s stable market position

- Germany is expected to be the fastest-growing country in the European Radiology Information Systems (RIS) market during the forecast period, with a projected CAGR higher than the regional average. Growth is driven by increasing digitalization of hospitals, government-backed healthcare IT funding programs, and rising demand for interoperable imaging informatics systems. Germany’s well-established healthcare infrastructure, strong presence of medical technology companies, and expanding adoption of AI-integrated RIS platforms across university hospitals and diagnostic imaging centers are accelerating market expansion. Additionally, regulatory support for health data exchange and hospital modernization initiatives are creating significant opportunities for RIS vendors across the country

- The Integrated segment dominated the market with the largest revenue share of 65.4% in 2024, driven by its ability to combine seamlessly with Picture Archiving and Communication Systems (PACS), Electronic Health Records (EHR), and other hospital information systems

Report Scope and Radiology Information Systems (RIS) Market Segmentation

|

Attributes |

Radiology Information Systems (RIS) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Radiology Information Systems (RIS) Market Trends

Enhanced Efficiency Through AI and Cloud-Based Integration

- A significant and accelerating trend in the Europe radiology information systems (RIS) market is the growing integration of artificial intelligence (AI) and cloud-based platforms into radiology workflows. These technologies are transforming diagnostic imaging by improving speed, accuracy, and accessibility

- For instance, AI-enabled RIS solutions are increasingly being used to automatically detect anomalies in imaging scans, assist radiologists in prioritizing urgent cases, and reduce diagnostic errors. Such advancements help clinicians manage the rising volume of imaging data more effectively

- Cloud-based RIS platforms also facilitate real-time collaboration between radiologists, hospitals, and specialists located in different geographies. This has proven especially valuable in rural or underserved regions where access to radiology experts is limited

- Vendors are investing in AI-driven analytics and natural language processing (NLP) to automate reporting, streamline administrative tasks, and improve interoperability with electronic health records (EHR)

- The trend is also marked by growing partnerships between RIS providers and cloud service companies such as Microsoft Azure, AWS, and Google Cloud, enabling scalable and secure infrastructure for radiology data management

- As hospitals move toward value-based care models, RIS solutions that combine AI with cloud capabilities are reshaping expectations by offering faster diagnosis, operational efficiency, and improved patient outcomes

Europe Radiology Information Systems (RIS) Market Dynamics

Driver

Growing Need for Streamlined Imaging Workflows and Rising Diagnostic Imaging Volumes

- The increasing global burden of chronic diseases such as cancer, cardiovascular conditions, and neurological disorders has led to a surge in diagnostic imaging procedures. This rising demand is a major driver for the adoption of Radiology Information Systems (RIS)

- For instance, in February 2023, GE HealthCare announced advancements in its Edison Digital Health Platform, emphasizing improved interoperability and integration with RIS to support faster diagnosis and reporting in high-volume radiology departments

- Hospitals and imaging centers are adopting RIS to reduce turnaround times, improve scheduling efficiency, and ensure seamless communication between radiologists, referring physicians, and patients

- The ability of RIS to provide features such as digital workflow management, appointment scheduling, automated reporting, billing integration, and performance analytics makes them indispensable for modern healthcare facilities

- In addition, government initiatives promoting healthcare digitization—such as the U.S. HITECH Act and similar programs in Europe and Asia-Pacific—are further driving RIS adoption by incentivizing the integration of advanced health IT systems

- As imaging volumes continue to rise worldwide, the demand for efficient RIS solutions that optimize both clinical and administrative workflows will remain a strong driver of market growth

Restraint/Challenge

High Implementation Costs and Interoperability Issues

- Despite its benefits, the high cost of implementing and maintaining radiology information systems (RIS) remains a significant barrier for smaller hospitals, diagnostic centers, and healthcare facilities in developing regions. Licensing fees, hardware requirements, IT infrastructure upgrades, and training expenses often strain budgets

- For instance, smaller community hospitals in emerging markets have struggled to adopt RIS due to limited financial resources, relying instead on manual processes or basic imaging management systems

- Interoperability challenges also present a major hurdle. Many healthcare facilities operate with legacy systems or non-standardized IT infrastructure, making seamless integration between RIS, PACS (Picture Archiving and Communication Systems), and EHR platforms difficult

- Data privacy and compliance with healthcare regulations such as HIPAA in the U.S. and GDPR in Europe further complicate RIS implementation, as providers must ensure secure handling and storage of sensitive patient information

- In addition, the shortage of skilled IT professionals trained in healthcare informatics slows down adoption and maintenance of RIS platforms in some regions

- Addressing these challenges requires vendors to develop cost-effective, interoperable, and user-friendly RIS solutions. Increased cloud adoption and subscription-based models are helping mitigate some of these issues, but high upfront costs and integration barriers remain key restraints to widespread adoption

Europe Radiology Information Systems (RIS) Market Scope

The market is segmented on the basis of type, component, deployment mode, and end user.

- By Type

On the basis of type, the Europe Radiology Information Systems (RIS) market is segmented into Integrated and Standalone. The Integrated segment dominated the market with the largest revenue share of 65.4% in 2024, driven by its ability to combine seamlessly with Picture Archiving and Communication Systems (PACS), Electronic Health Records (EHR), and other hospital information systems. Healthcare providers increasingly prefer integrated RIS platforms as they offer improved workflow management, automated reporting, and reduced duplication of records. Integrated systems also facilitate faster diagnosis by centralizing patient imaging histories and enabling easy access for both radiologists and referring physicians. In addition, government incentives for promoting digitization in healthcare and interoperability standards in the U.S. have further propelled the dominance of integrated RIS solutions. Large hospitals and diagnostic centers rely heavily on integrated RIS to manage high imaging volumes, further cementing this segment’s leadership.

The Standalone segment is expected to witness the fastest CAGR of 10.8% from 2025 to 2032, owing to its adoption among smaller clinics, office-based physicians, and specialty imaging centers that require cost-effective and easy-to-deploy solutions. Standalone RIS offers flexibility for facilities that do not yet have fully digitized infrastructure, making it an attractive entry-level option for medical practices transitioning from manual processes. In addition, many vendors are launching modular standalone RIS platforms that can later integrate with EHRs and PACS, offering scalability for growing practices. The affordability, simplified training requirements, and reduced IT maintenance needs of standalone RIS solutions contribute to their faster adoption in underserved and rural healthcare markets.

- By Component

On the basis of component, the Europe RIS market is segmented into Services, Software, and Hardware. The Software segment dominated the market with the largest revenue share of 52.7% in 2024, as RIS software forms the core of diagnostic imaging management. Advanced RIS software provides functionalities such as patient scheduling, result reporting, billing, and analytics, which significantly improve operational efficiency. Many hospitals are investing in AI-powered RIS software capable of enhancing diagnostic accuracy, automating administrative tasks, and integrating seamlessly with telemedicine platforms. Furthermore, the software segment benefits from regular upgrades and cloud-based subscription models, which allow providers to access the latest functionalities without large upfront costs. This adaptability and continuous innovation ensure software’s leading role within the RIS ecosystem.

The Services segment is projected to grow at the fastest CAGR of 11.4% from 2025 to 2032, driven by the rising demand for consulting, training, integration, and maintenance services across healthcare facilities. As RIS solutions become increasingly complex, providers rely on vendor-led or third-party services to ensure smooth implementation and system optimization. In particular, cloud migration services and cybersecurity support are gaining traction, as healthcare facilities seek secure, compliant, and efficient operations. Service contracts also include 24/7 technical support and workflow customization, making them critical for sustaining system performance. This growing dependence on professional services for RIS deployment and management is expected to fuel strong long-term growth in this segment.

- By Deployment Mode

On the basis of deployment mode, the market is segmented into Web-Based, On-Premise, and Cloud-Based. The Web-Based segment held the largest revenue share of 47.9% in 2024, supported by its wide-scale adoption among hospitals and imaging centers seeking cost-effective yet scalable deployment solutions. Web-based RIS enables providers to access patient data securely through internet browsers without the need for extensive IT infrastructure investments. These solutions are popular in Europe due to their affordability and faster deployment timelines compared to on-premise alternatives. In addition, web-based systems allow regular vendor updates and integration with third-party applications, making them a practical choice for medium-sized healthcare institutions. The balance of cost-efficiency, accessibility, and scalability positions web-based RIS as the dominant deployment mode in 2024.

The Cloud-Based segment is expected to witness the fastest CAGR of 13.2% from 2025 to 2032, fueled by the growing shift toward digital healthcare ecosystems and demand for remote accessibility. Cloud-based RIS offers real-time collaboration between radiologists across different geographies, facilitating tele-radiology and improving diagnostic turnaround times. The ability to scale storage capacity dynamically, reduce IT infrastructure costs, and ensure business continuity through disaster recovery solutions further strengthens adoption. With leading companies such as GE HealthCare, Philips, and Siemens Healthineers investing heavily in cloud-enabled platforms, adoption is accelerating rapidly across Europe. Increasing concerns about data security are being addressed through HIPAA-compliant cloud architectures, boosting trust among healthcare providers and driving rapid growth in this segment.

- By End User

On the basis of end user, the Europe RIS market is segmented into Hospitals, Office-Based Physicians, and Emergency Healthcare Service Providers. The Hospitals segment dominated with the largest market share of 71.6% in 2024, due to their ability to invest in advanced RIS platforms that manage high imaging volumes. Large hospital networks benefit from RIS systems by streamlining workflow, reducing diagnostic turnaround times, and ensuring efficient communication across multiple departments. Integration with PACS and EHR within hospitals allows for seamless patient record management, enhancing both clinical and administrative efficiency. In addition, hospitals are at the forefront of adopting AI and advanced analytics within RIS platforms to optimize radiologist workloads and improve patient outcomes. With expanding imaging facilities and demand for centralized solutions, hospitals continue to lead the end-user segment.

The Office-Based Physicians segment is anticipated to grow at the fastest CAGR of 12.6% from 2025 to 2032, driven by the rising adoption of RIS in smaller practices and outpatient imaging centers. These facilities are increasingly offering specialized diagnostic services and require efficient systems to manage patient data, scheduling, and reporting. Affordable and modular RIS platforms tailored for small and medium practices are fueling adoption in this segment. The flexibility of standalone and cloud-based RIS solutions further makes them attractive to office-based physicians who often lack large IT teams. In addition, the shift toward decentralized healthcare and outpatient care models in Europe is encouraging more physicians to adopt RIS solutions, driving rapid growth in this segment.

Europe Radiology Information Systems (RIS) Market Regional Analysis

- Europe dominated the radiology information systems (RIS) market with the largest revenue share of 49% in 2024, driven by advanced healthcare infrastructure, high healthcare IT spending, and the strong presence of leading imaging informatics providers across the region

- The market has witnessed significant adoption of RIS solutions across public hospitals, university medical centers, and private diagnostic imaging facilities, supported by government-backed digital transformation initiatives and the growing demand for streamlined radiology workflows

- Increasing integration of RIS with electronic health records (EHRs) and Picture Archiving and Communication Systems (PACS), along with the adoption of AI-enabled imaging analytics, is enhancing diagnostic accuracy, data interoperability, and operational efficiency. High patient awareness regarding digital healthcare services, robust IT ecosystems, and regulatory emphasis on data standardization further reinforce the region’s sustained market leadership

U.K. Radiology Information Systems (RIS) Market Insight

The U.K. radiology information systems (RIS) market accounted for 32.5% of the global radiology information systems (RIS) market revenue in 2024, reflecting its strong position within the European landscape. The country has experienced steady adoption of RIS platforms across NHS hospitals and private diagnostic centers, supported by nationwide digital transformation initiatives and the increasing focus on integrated care systems. Government-led programs promoting electronic health record (EHR) integration and digital hospital infrastructure, combined with the growing implementation of AI-enabled imaging analytics, are significantly improving workflow management and diagnostic precision. The centralized healthcare structure under the NHS, well-defined regulatory frameworks, and continuous investments in health IT modernization are maintaining the U.K.’s stable and mature RIS market growth trajectory.

Germany Radiology Information Systems (RIS) Market Insight

Germany radiology information systems (RIS) market is projected to be the fastest-growing country in the European radiology information systems (RIS) market during the forecast period, with a CAGR exceeding the regional average. Market growth is driven by accelerating hospital digitalization, government-supported healthcare IT funding programs, and rising demand for interoperable imaging informatics solutions. Germany’s well-established healthcare infrastructure, strong presence of medical technology companies, and expanding deployment of AI-integrated RIS platforms across university hospitals and diagnostic imaging centers are accelerating adoption. Additionally, regulatory support for health data exchange, hospital modernization initiatives, and increasing emphasis on integrated digital imaging ecosystems are creating substantial growth opportunities for RIS vendors across the country.

Europe Radiology Information Systems (RIS) Market Share

The Radiology Information Systems (RIS) industry is primarily led by well-established companies, including:

- Siemens Medical Solutions USA, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- General Electric Company (U.S.)

- Carestream Health, Inc. (U.S.)

- FUJIFILM Holdings America Corporation (Japan)

- Konica Minolta, Inc. (Japan)

- Epic Systems Corporation (U.S.)

- Oracle Health (U.S.)

- INFINITT Healthcare Co., Ltd. (South Korea)

- Novarad Corporation (U.S.)

- PaxeraHealth Corp. (U.S.)

- Sectra AB (Sweden)

- Pro Medicus Limited (Australia)

- MedInformatix, Inc. (U.S.)

- eRAD, Inc. (U.S.)

- Agfa-Gevaert Group (Belgium)

Latest Developments in Europe Radiology Information Systems (RIS) Market

- In February 2021, Sectra AB, a Sweden-based medical imaging IT company, announced a multi-year contract with Integrated Diagnostic Holdings (IDH) to deploy its enterprise imaging solution, including RIS capabilities, across multiple countries. The agreement expanded Sectra’s footprint in emerging markets and strengthened its position in cloud-enabled radiology workflow management. This development highlighted the growing demand for scalable and interoperable RIS platforms supporting cross-border diagnostic networks

- In January 2023, Pro Medicus Limited, through its U.S. subsidiary Visage Imaging, Inc., secured an 8-year contract valued at approximately USD 12 million with Samaritan Health Services in Oregon, U.S. The contract involved the implementation of Visage’s RIS/PACS platform to enhance imaging workflows, reporting efficiency, and enterprise-wide interoperability. This agreement reinforced Pro Medicus’ expanding presence in the North American RIS market and reflected rising hospital investments in advanced imaging IT systems

- In January 2024, Siemens Healthineers announced the expansion of its cloud-based imaging IT portfolio, integrating advanced RIS functionalities within its enterprise digital health ecosystem. The enhanced platform supports real-time data access, multi-site radiology collaboration, and improved system interoperability. This development underscores Siemens Healthineers’ strategic focus on cloud transformation and AI-enabled radiology workflow optimization

- In March 2024, GE HealthCare introduced advancements to its Centricity™ RIS platform, focusing on AI integration, automation, and improved data analytics capabilities. The upgraded system enables streamlined scheduling, faster report turnaround times, and enhanced interoperability with electronic health records (EHR) and PACS systems. This launch reflects GE HealthCare’s continued investment in intelligent imaging informatics solutions to improve radiology department productivity

- In November 2024, FUJIFILM Healthcare expanded its Synapse enterprise imaging portfolio with enhancements supporting RIS interoperability and telehealth-enabled imaging workflows. The update focused on improving accessibility for remote diagnostics and strengthening integration between imaging, reporting, and hospital information systems. This move aligns with the increasing global shift toward cloud-based and tele-radiology solutions

- In June 2024, Konica Minolta Healthcare Americas and Apollo Enterprise Imaging announced a collaboration with Amazon Web Services (AWS) to integrate the Exa Platform and arcc using AWS HealthImaging (AHI). This cloud-based integration aims to enhance enterprise-wide clinical workflows and provide a comprehensive imaging solution for healthcare providers

- In November 2024, Konica Minolta Healthcare Americas launched Exa Enterprise, an enterprise imaging solution with an integrated PACS/RIS core powered by Amazon Web Services (AWS). Leveraging AWS HealthImaging, Exa Enterprise offers a scalable, web-based platform with enhanced cybersecurity measures and fast data access, aiming to boost efficiency across imaging specialties

- In April 2025, Konica Minolta Healthcare Americas announced updates to its Exa Enterprise Imaging platform, incorporating enhanced visualization tools and improved API-based interoperability to streamline RIS and PACS integration. The upgraded platform supports multi-site imaging networks and enterprise-wide workflow standardization. This development demonstrates the company’s commitment to advancing vendor-neutral, scalable radiology IT infrastructure

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.