Europe Steel For Data Centers Construction Market

Market Size in USD Billion

CAGR :

%

USD

7.40 Billion

USD

15.03 Billion

2025

2033

USD

7.40 Billion

USD

15.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.40 Billion | |

| USD 15.03 Billion | |

| % | |

|

Europe Steel for Data Centers Construction Market Overview

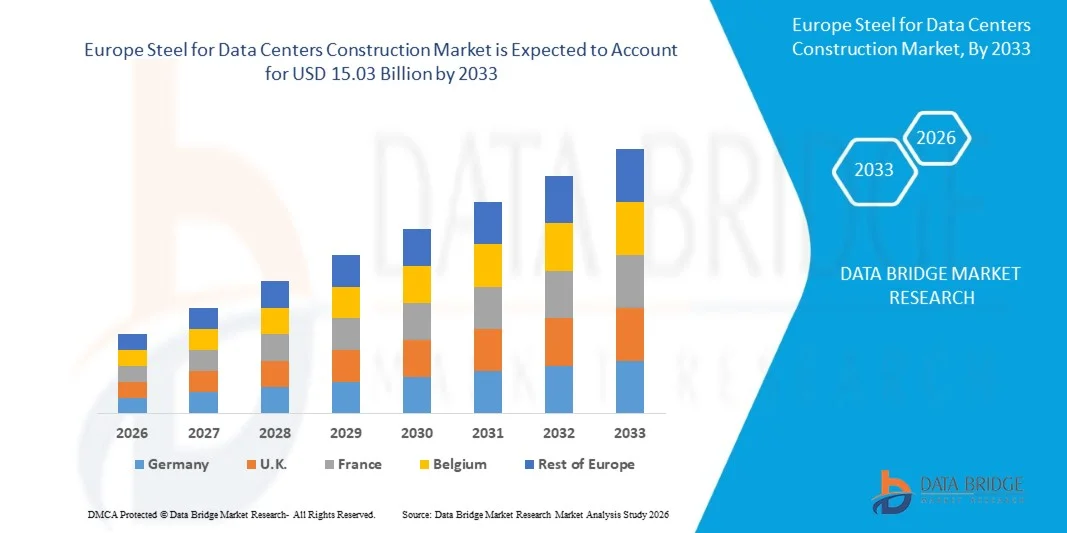

The Europe steel for data centers construction market size was valued at USD 7.40 Billion in 2026 and is projected to reach USD 15.03 Billion by 2033, growing at a CAGR of 9.1% from 2026 to 2033. The market is witnessing growth due to rising investments in hyperscale and colocation data center projects, increasing digitalization across industries, and expanding cloud computing infrastructure across Europe.

Furthermore, growing demand for sustainable and energy-efficient building materials, increasing adoption of modular data center construction, and stricter environmental regulations supporting low-carbon steel production are contributing to long-term market expansion.

Key Market Trends & Insights

- The Europe Steel for Data Centers Construction Market is experiencing strong growth, driven by rapid expansion of digital infrastructure, increasing deployment of cloud services, and rising investments in AI-ready and high-density data centers across the region.

- Germany dominated the driving simulators market with the largest revenue share of 17.70% in 2025, supported by its position as Europe's leading data center hub, particularly in the Frankfurt region.

- Growing construction of hyperscale data centers by cloud service providers and colocation operators is significantly increasing the demand for structural steel, fabricated steel components, and advanced steel solutions for cooling and power infrastructure.

- Rising emphasis on sustainable construction practices and carbon reduction targets is encouraging the adoption of recycled and green steel materials in data center development projects.

- Increasing adoption of modular and prefabricated construction techniques is accelerating the use of fabricated steel structures, enabling faster deployment, scalability, and improved construction efficiency.

- In 2025, the Structural Steel segment dominates the Europe Steel for Data Centers Construction Market with 34.51% share, accounting for the largest market share due to its extensive use in data center frameworks, load-bearing structures, equipment support systems, and large-scale hyperscale construction projects. Increasing investments in durable, scalable, and energy-efficient data center facilities are further strengthening segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 7.40 Billion

- Expected Market Value (2033): USD 15.03 Billion

- Forecast CAGR (2026–2033): 9.1%

- Leading Country in 2025: Germany

- Fastest Growing Country: Germany

Report Scope and Europe Steel for Data Centers Construction Market Segmentation

|

Attributes |

Steel for Data Centers Construction Key Market Insights |

|

Segments Covered |

· By SteelType: Structural Steel, Carbon Steel, Galvanized Steel, Stainless Steel, Alloy Steel and Recycled / Green Steel · By Product Form: Long Steel Products, Flat Steel Products, Fabricated Steel Components and Tubular Steel Products · By Data Center Application: Structural Framework, Cooling Infrastructure, Power & Electrical Infrastructure, Server & IT Infrastructure, Flooring Systems, Mechanical & Support Systems, Security & Protection Systems and Others · By Data Center Type: Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers and Edge Data Centers · By Construction Type: Conventional Construction and Modular / Prefabricated Construction · By End-User: Cloud & Hyperscale Providers, Colocation Providers, Telecom Operators, Government & Defense, BFSI & Enterprise IT and Others · By Distribution Channel: Direct and Indirect |

|

Countries Covered |

· Germany · U.K. · Netherlands · France · Sweden · Denmark · Italy · Spain · Norway · Switzerland · Turkey · Finland · Belgium · Russia · Rest of Europe |

|

Key Market Players |

· ArcelorMittal (Luxembourg) · thyssenkrupp Steel (Germany) · voestalpine Stahl GmbH (Austria) · Nippon Steel Corporation (Japan) · POSCO Holdings (South Korea) · Acerinox (Spain) · Outokumpu (Finland) · Baowu Steel Group (China) · HBIS Group (China) · Tata Steel (India) · Van Leeuwen (Netherlands) · Hyundai Steel (South Korea) · JFE Steel Corporation (Japan) · JSW Steel (India) |

|

Market Opportunities |

· Expansion of Edge Data Centers in Emerging Urban Areas · Rising Demand for Corrosion-Resistant Steel in Coastal Data Center Projects |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Europe Steel for Data Centers Construction Market Trends

Trend: Growth in Motorsports & Professional Training

Europe is witnessing a significant increase in hyperscale and AI-focused data center construction, driving robust demand for structural steel, reinforcement bars, steel sections, and prefabricated steel components. Major cloud providers, colocation operators, and technology companies are expanding capacity across key markets such as Germany, United Kingdom, Ireland, and Spain. Steel is increasingly preferred due to its strength, speed of construction, design flexibility, and compatibility with modular data center designs. The growing adoption of prefabricated steel structures is helping developers reduce construction timelines while supporting the rapid deployment requirements of AI and cloud computing facilities. Several hyperscale projects announced across Frankfurt, London, Dublin, and Madrid during 2024–2025 have incorporated modular steel-intensive construction methods to accelerate project delivery and improve sustainability performance.

Europe Steel for Data Centers Construction Market Dynamics

Key Market Driver: Rapid Expansion of Hyperscale and Cloud Data Centers

The accelerating demand for cloud computing, artificial intelligence workloads, edge computing, and digital transformation initiatives is driving large-scale data center construction across Europe. Data center facilities require substantial quantities of structural steel for building frames, server halls, equipment support structures, roofing systems, and utility infrastructure. Major investments by hyperscale operators and colocation providers are increasing steel consumption throughout the construction phase. For example, Microsoft, Amazon Web Services (AWS), and Google Cloud continue to expand their European data center footprints, creating sustained demand for steel-intensive construction materials and supporting infrastructure.

In June 2025, Amazon Web Services (AWS) announced through its official newsroom plans to invest AU$20 billion between 2025 and 2029 to expand, operate, and maintain its data center infrastructure across Australia, including major cloud and AI capacity expansions in Sydney and Melbourne, increasing construction activities associated with steel-intensive server facilities, cooling infrastructure, and power support systems

Key Restraint/Challenge: Volatility in Steel Prices and Rising Construction Costs

A significant challenge facing the Europe steel for data centers construction market is the volatility of steel prices and broader construction cost inflation. Fluctuations in energy prices, raw material costs, labor expenses, and supply chain disruptions can significantly impact project budgets and timelines. Data center developers often face uncertainty in procurement planning due to changing steel prices, while stringent European environmental regulations may further increase compliance and production costs for steel manufacturers. The ongoing transition toward low-carbon steel production also requires substantial investment from steel producers, potentially increasing short-term material costs for construction projects.

The expansion of low-emission steel manufacturing initiatives across Europe, including investments by SSAB and ArcelorMittal in green steel technologies, demonstrates the industry's commitment to sustainability but also highlights the significant capital expenditure requirements that may contribute to higher steel procurement costs during the transition period.

As reported by Infrastructure Australia – 2025 Infrastructure Market Capacity Report in November 2025, fabricated steel imports in Australia during 2024 were nearly 50% higher than the annual average recorded between 2016 and 2021, while imported products were often priced 15% to 50% below locally fabricated steel, creating significant pricing volatility and procurement uncertainty for steel-intensive infrastructure sectors such as hyperscale data center construction.

In February 2026, BlueScope Steel ASX Release announced through its official financial results that softer domestic and export steel pricing, combined with cost escalation pressures, continued affecting operational performance across Australia, highlighting ongoing volatility in steel pricing and raw material costs impacting major construction and infrastructure projects.

Key Market Opportunity: Growing Adoption of Green Data Centers and Low-Carbon Steel

The increasing focus on sustainable data center development presents a substantial opportunity for the market. European governments, investors, and data center operators are prioritizing carbon reduction targets, energy efficiency, and environmentally responsible construction practices. This trend is driving demand for recycled steel, low-carbon steel, and environmentally certified construction materials. Steel manufacturers that offer low-emission products are well positioned to benefit from the growing number of green data center projects being developed across Europe.

The emergence of low-carbon steel production technologies, coupled with sustainability initiatives from major data center operators, is creating new opportunities for premium steel products. As developers pursue green building certifications and net-zero targets, demand is expected to increase for steel solutions that support lifecycle carbon reduction, circular economy objectives, and sustainable construction practices across Europe's expanding data center ecosystem.

Europe Steel for Data Centers Construction Market Scope

The Europe steel for data centers construction market is segmented into seven notable segments based on steel type, product form, data center application, data center type, construction type, end-user and distribution channel.

- By Steel Type

On the basis of steel type, the Europe Steel for Data Centers Construction Market is segmented into Structural Steel, Carbon Steel, Galvanized Steel, Stainless Steel, Alloy Steel, and Recycled / Green Steel. In 2026, the Structural Steel segment is expected to dominate the market with a 34.75% market share, driven by increasing hyperscale and colocation data center construction activities, high load-bearing requirements, and extensive use in structural frameworks and support infrastructure. The segment is further supported by growing investments in large-scale digital infrastructure projects and demand for durable, scalable, and cost-efficient construction materials.

In 2026, the Galvanized Steel segment is expected to witness the highest growth rate of 10.1% in the Europe Steel for Data Centers Construction Market, driven by rising demand for corrosion-resistant materials, increasing deployment in cooling and electrical infrastructure, and growing focus on long-term durability and energy-efficient data center facilities. Expanding adoption of sustainable and low-maintenance construction materials is also supporting segment growth.

- By Product Form

On the basis of product form, the Europe Steel for Data Centers Construction Market is segmented into Long Steel Products, Flat Steel Products, Fabricated Steel Components, and Tubular Steel Products. In 2026, the Long Steel Products segment is expected to dominate the market with a 41.81% market share, driven by its extensive application in structural beams, reinforcement systems, columns, and framework construction for hyperscale and enterprise data centers. Strong growth in large-scale infrastructure development and expansion of modular construction projects are further supporting segment demand.

In 2026, the Fabricated Steel Components segment is expected to witness the highest growth rate of 10.0% in the Europe Steel for Data Centers Construction Market, driven by increasing adoption of modular and prefabricated data center construction techniques, rising need for faster deployment timelines, and growing demand for customized steel assemblies for cooling, power, and server infrastructure.

- By Data Center Application

On the basis of data center application, the Europe Steel for Data Centers Construction Market is segmented into Structural Framework, Cooling Infrastructure, Power & Electrical Infrastructure, Server & IT Infrastructure, Flooring Systems, Mechanical & Support Systems, Security & Protection Systems, and Others. In 2026, the Structural Framework segment is expected to dominate the market with a 33.57% market share, driven by rising construction of hyperscale and colocation data centers requiring robust structural support systems, heavy-load capacity, and scalable building designs. Increasing investments in AI-ready and high-density facilities are further strengthening demand for structural steel applications.

In 2026, the Cooling Infrastructure segment is expected to witness the highest growth rate of 10.1% in the Europe Steel for Data Centers Construction Market, driven by growing deployment of advanced cooling systems, liquid cooling technologies, and energy-efficient HVAC infrastructure required to manage increasing heat loads in modern data centers.

- By Data Center Type

On the basis of data center type, the Europe Steel for Data Centers Construction Market is segmented into Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, and Edge Data Centers. In 2026, the Hyperscale Data Centers segment is expected to dominate the market with a 48.70% market share, driven by increasing cloud adoption, expansion of AI and big data workloads, and rising investments by global technology companies in large-scale digital infrastructure across Europe. The segment is also benefiting from growing demand for scalable and energy-efficient facilities.

In 2026, the Edge Data Centers segment is expected to witness the highest growth rate of 9.7% in the Europe Steel for Data Centers Construction Market, driven by rapid expansion of 5G networks, increasing edge computing adoption, and rising demand for low-latency data processing infrastructure across urban and industrial environments.

- By Construction Type

On the basis of construction type, the Europe Steel for Data Centers Construction Market is segmented into Conventional Construction and Modular / Prefabricated Construction. In 2026, the Conventional Construction segment is expected to dominate the market with a 71.35% market share, driven by widespread adoption in large-scale hyperscale facilities, greater design flexibility, and strong investments in permanent data center infrastructure across key European markets.

In 2026, the Modular / Prefabricated Construction segment is expected to witness the highest growth rate of 9.5% in the Europe Steel for Data Centers Construction Market, driven by increasing demand for rapid deployment, scalability, reduced construction timelines, and cost-efficient infrastructure solutions. Rising adoption of prefabricated steel structures and containerized data center modules is further supporting market expansion.

- By End-User

On the basis of end-user, the Europe Steel for Data Centers Construction Market is segmented into Cloud & Hyperscale Providers, Colocation Providers, Telecom Operators, Government & Defense, BFSI & Enterprise IT, and Others. In 2026, the Cloud & Hyperscale Providers segment is expected to dominate the market with a 46.79% market share, driven by growing cloud computing demand, increasing investments in AI infrastructure, and expansion of hyperscale facilities by global technology companies across Europe. The segment is further supported by rising digital transformation initiatives and increasing data traffic volumes.

In 2026, the Cloud & Hyperscale Providers segment is also expected to witness the highest growth rate of 9.4% in the Europe Steel for Data Centers Construction Market, driven by continuous expansion of cloud regions, increasing demand for high-performance computing infrastructure, and rising investments in sustainable and energy-efficient data center construction projects.

- By Distribution Channel

On the basis of distribution channel, the Europe Steel for Data Centers Construction Market is segmented into Direct and Indirect. In 2026, the Direct segment is expected to dominate the market with a 74.66% market share, driven by strong procurement relationships between steel manufacturers, construction contractors, and large-scale data center developers. Direct sourcing enables better customization, cost optimization, quality assurance, and supply chain efficiency for major infrastructure projects.

In 2026, the Indirect segment is expected to witness the highest growth rate of 9.7% in the Europe Steel for Data Centers Construction Market, driven by expanding regional distributor networks, increasing participation of specialized steel suppliers, and growing demand from small and medium-sized data center construction projects across emerging European markets.

Europe Steel for Data Centers Construction Market Regional Analysis

The region benefits from the presence of major data center hubs, advanced construction capabilities, and stringent sustainability regulations encouraging the use of high-performance and low-carbon steel materials. Growing investments in hyperscale, colocation, and edge data centers across key markets such as Germany, the U.K., Ireland, the Netherlands, and Spain continue to drive demand for structural steel, reinforcement steel, and prefabricated steel components. Furthermore, the increasing adoption of modular construction techniques and green building standards is strengthening Europe’s position as a leading market for steel-intensive data center construction projects.

U.K. Driving Simulators Market Insight

The U.K. steel for data centers construction market is experiencing strong growth, driven by increasing investments in hyperscale and colocation data centers, particularly in the London metropolitan region and emerging regional hubs. Rising demand for cloud services, artificial intelligence infrastructure, and digital transformation initiatives is accelerating new data center developments, thereby increasing the consumption of structural steel and prefabricated construction materials. Additionally, growing emphasis on sustainable building practices and energy-efficient data center designs is supporting demand for low-carbon steel products. The expansion of data center capacity by global technology companies and colocation providers continues to position the U.K. as one of Europe's most significant markets for data center-related steel consumption.

Germany Driving Simulators Market Insight

The Germany steel for data centers construction market is expanding steadily due to the country's position as Europe’s largest data center market, led by the Frankfurt metropolitan area, one of the world's most important digital infrastructure hubs. Strong demand from cloud service providers, hyperscale operators, and enterprise data center developers is generating substantial requirements for structural steel frameworks, steel reinforcement products, and modular construction solutions. Germany’s advanced industrial base, focus on sustainable construction, and investments in renewable-energy-powered data centers are further supporting market growth. Additionally, increasing deployment of AI-ready facilities and edge computing infrastructure is creating new opportunities for steel manufacturers supplying specialized materials for next-generation data center project.

Europe Steel for Data Centers Construction Market Share

The Europe Steel for Data Centers Construction Market is primarily led by well-established companies, including:

- ArcelorMittal (Luxembourg)

- thyssenkrupp Steel (Germany)

- voestalpine Stahl GmbH (Austria)

- Nippon Steel Corporation (Japan)

- POSCO Holdings (South Korea)

- Acerinox (Spain)

- Outokumpu (Finland)

- Baowu Steel Group (China)

- HBIS Group (China)

- Tata Steel (India)

- Van Leeuwen (Netherlands)

- Hyundai Steel (South Korea)

- JFE Steel Corporation (Japan)

- JSW Steel (India)

Latest Developments in Europe Steel for Data Centers Construction Market

- In April 2026, ArcelorMittal has entered into a partnership with Stockland, through its Steligence platform and JSteel, to supply engineered low-carbon steel solutions for Stockland’s construction projects in Australia. The collaboration focuses on using ArcelorMittal’s XCarb recycled and renewable steel to reduce embodied carbon in large-scale logistics and infrastructure developments. This deal strengthens ArcelorMittal’s position in the low-carbon construction steel market and expands the adoption of its XCarb brand in large international infrastructure projects.

- In May 2026, Thyssenkrupp Steel Europe has raised the valuation of its steel division to around €3 billion, after negotiations to sell the business to India’s Jindal Steel collapsed. The decision reflects restructuring progress, including workforce reduction plans, exit from joint ventures, and stronger EU protection measures against cheap steel imports. This valuation increase strengthens Thyssenkrupp Steel Europe’s strategic position for future investment.

- In September 2025, Vallourec SA has secured a major offshore supply contract with Petrobras worth up to $1 billion. The agreement covers the supply of oil country tubular goods (OCTG), including carbon and stainless-steel pipes along with associated services for offshore operations from 2026 to 2029. This deal strengthens Vallourec’s long-term revenue pipeline and reinforces its position as a leading global supplier of high-value offshore energy tubular solutions.

- In April 2026, Nippon Steel Corporation has obtained new SuMPO EPD certifications for its stainless hot extruded steel shapes, including Stainless Steel (SUS304), under the SuMPO Environmental Labeling Program. The certification strengthens the environmental transparency of its product category, which already holds multiple EPD certifications, and supports customer demand for carbon neutrality and verified low-impact materials. This enhances Nippon Steel’s credibility in sustainable steel products.

- In December 2025, Acerinox has launched EcoACX® ultra-low-carbon stainless steel, its most sustainable product range to date, produced using more than 90% recycled material and renewable electricity, achieving around a 50% reduction in carbon emissions compared with conventional stainless steel. The company has also introduced “Blueline” low-emission stainless steel chimney and duct systems in partnership with Jeremias, designed for construction applications and built using EcoACX® steel to significantly reduce embodied carbon in building infrastructure. These product launches strengthen Acerinox’s position in premium low-carbon stainless steel markets in Europe.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Europe Steel For Data Centers Construction Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Steel For Data Centers Construction Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Steel For Data Centers Construction Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.