Europe Surgical Sutures Market

Market Size in USD Billion

CAGR :

%

USD

1.76 Billion

USD

2.66 Billion

2025

2033

USD

1.76 Billion

USD

2.66 Billion

2025

2033

| 2026 –2033 | |

| USD 1.76 Billion | |

| USD 2.66 Billion | |

| % | |

|

Europe Surgical Sutures Market Size

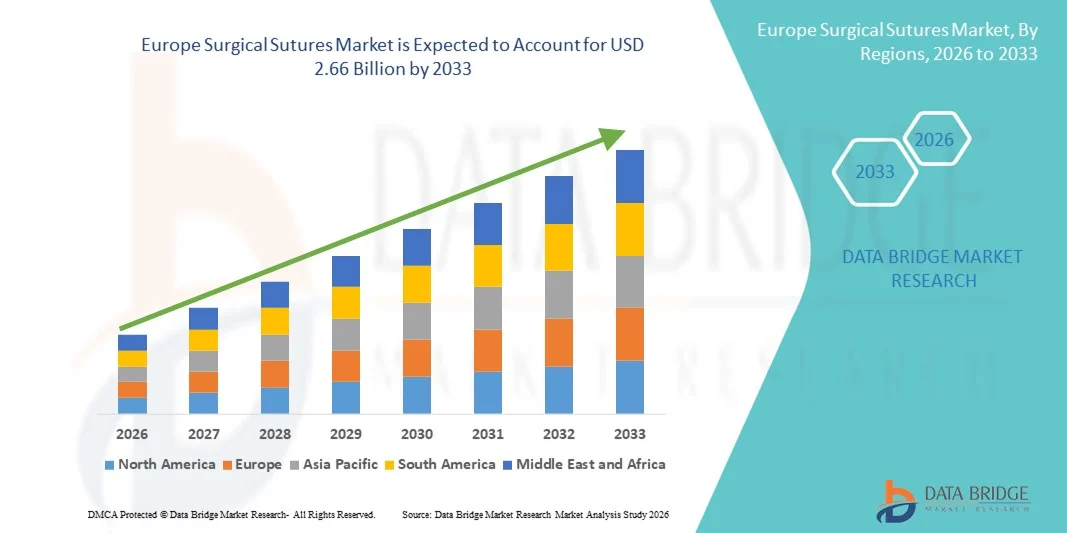

- The Europe surgical sutures market size was valued at USD 1.76 billion in 2025 and is expected to reach USD 2.66 billion by 2033, at a CAGR of5.30% during the forecast period

- The market growth is largely fueled by the increasing number of surgical procedures worldwide and continuous technological advancements in wound closure materials, leading to improved surgical outcomes in hospitals and healthcare facilities

- Furthermore, rising demand for effective wound management solutions, growing prevalence of chronic diseases, and increasing preference for minimally invasive surgeries are establishing surgical sutures as essential tools in modern surgical procedures. These converging factors are accelerating the uptake of Surgical Sutures solutions, thereby significantly boosting the industry's growth

Europe Surgical Sutures Market Analysis

- Surgical sutures, used for wound closure during surgical procedures, are increasingly vital components of modern healthcare systems in hospitals and surgical centers due to their effectiveness in promoting proper healing, minimizing infection risk, and supporting a wide range of surgical applications

- The escalating demand for surgical sutures is primarily fueled by the rising number of surgical procedures, increasing prevalence of chronic diseases, and growing adoption of advanced wound closure techniques in modern healthcare practices

- The U.K. dominated the surgical sutures market with the largest revenue share of 29.8% in 2025, characterized by a well-established healthcare system, high number of surgical procedures, and strong presence of leading medical device manufacturers and advanced surgical technologies

- Germany is expected to be the fastest growing region in the Surgical Sutures market during the forecast period, with a projected CAGR of 9.1%, due to increasing healthcare expenditure, rising surgical volumes, and growing adoption of advanced wound closure products across hospitals and surgical centers

- The suture threads segment dominated the largest market revenue share of 72.8% in 2025, driven by their extensive use across a wide range of surgical procedures including cardiovascular, orthopedic, gynecological, and general surgeries

Report Scope and Surgical Sutures Market Segmentation

|

Attributes |

Surgical Sutures Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Surgical Sutures Market Trends

Rising Adoption of Advanced and Biodegradable Sutures

- A significant and accelerating trend in the global Surgical Sutures market is the increasing adoption of advanced suture materials, particularly biodegradable and antimicrobial sutures, designed to improve wound healing outcomes and reduce the risk of post-surgical infections. Healthcare providers are increasingly preferring sutures that offer superior tensile strength, improved handling characteristics, and predictable absorption profiles, which enhance surgical efficiency and patient recovery

- For instance, Ethicon (Johnson & Johnson) introduced its antibacterial coated sutures such as Vicryl Plus, which are designed to inhibit bacterial colonization around the wound site and reduce surgical site infections. Similarly, Medtronic offers advanced absorbable sutures that support consistent wound closure and minimize the need for suture removal, improving patient comfort and clinical outcomes

- Advancements in suture technology have enabled manufacturers to develop materials that maintain strength during the critical healing phase while gradually degrading once tissue healing is complete. These innovations help surgeons achieve reliable wound closure while minimizing complications associated with traditional non-absorbable sutures

- In addition, there is growing demand for specialty sutures used in minimally invasive and robotic-assisted surgeries, where precision, flexibility, and durability are essential. Surgeons increasingly rely on high-performance sutures that allow better knot security and tissue compatibility during delicate procedures

- The continuous focus on innovation and improved surgical outcomes is encouraging companies to invest heavily in research and development to introduce sutures with enhanced performance characteristics. Manufacturers are also developing antimicrobial and barbed sutures that help reduce operating time and improve wound stability

- As surgical procedures continue to rise globally due to increasing chronic diseases, trauma cases, and aging populations, the demand for technologically advanced surgical sutures is expected to grow steadily across hospitals, ambulatory surgical centers, and specialty clinics

Europe Surgical Sutures Market Dynamics

Driver

Increasing Number of Surgical Procedures

- The growing number of surgical procedures globally, driven by rising prevalence of chronic diseases, trauma injuries, and expanding access to healthcare services, is a major factor fueling the demand for surgical sutures. As surgeries become more common across various medical specialties, the need for reliable wound closure solutions continues to increase

- For instance, according to global health estimates, millions of surgical procedures are performed annually worldwide, including cardiovascular surgeries, orthopedic procedures, and cesarean sections. Companies such as B. Braun and Smith & Nephew have expanded their surgical suture portfolios to meet this rising demand, offering a wide range of absorbable and non-absorbable sutures used across multiple surgical disciplines

- The increasing prevalence of conditions such as cardiovascular diseases, cancer, and orthopedic disorders often requires surgical intervention, which directly contributes to higher consumption of sutures in operating rooms worldwide

- Furthermore, the growing geriatric population is more susceptible to chronic diseases and surgical treatments, further accelerating the need for effective wound closure solutions. Older patients frequently undergo procedures such as joint replacements, cardiovascular surgeries, and general surgeries that rely heavily on surgical sutures

- In addition, expanding healthcare infrastructure in emerging economies and improved access to surgical care are increasing the number of surgeries performed in hospitals and ambulatory surgical centers. This expansion is further strengthening the global demand for surgical sutures across diverse healthcare settings

Restraint/Challenge

Risk of Surgical Site Infections and Availability of Alternative Wound Closure Methods

- One of the major challenges affecting the global Surgical Sutures market is the risk of surgical site infections (SSIs) associated with improper wound closure or contamination during surgical procedures. These complications can delay healing, increase healthcare costs, and negatively impact patient outcomes

- For instance, healthcare organizations and hospitals worldwide continuously implement strict infection prevention protocols after reports indicating that surgical site infections remain among the most common healthcare-associated infections. Such concerns have encouraged the adoption of alternative wound closure technologies such as surgical staplers, tissue adhesives, and adhesive strips in certain procedures

- Alternative wound closure methods can sometimes provide faster closure, reduced operating time, and minimal tissue trauma compared to traditional suturing techniques, making them attractive options in specific surgical applications

- In addition, the availability of advanced wound closure technologies, including absorbable staples and bioadhesive glues, is gradually increasing competition for conventional sutures in certain procedures such as cosmetic surgeries and minimally invasive operations

- Moreover, the cost pressures faced by healthcare systems and hospitals in several regions may also influence purchasing decisions, particularly when alternative closure solutions offer shorter procedure times and improved efficiency

- Addressing these challenges through improved infection-resistant suture materials, enhanced sterilization standards, and continuous innovation in suture technology will be crucial for sustaining the long-term growth of the global surgical sutures market

Europe Surgical Sutures Market Scope

The market is segmented on the basis of product, type, application, and end-user.

- By Product

On the basis of product, the America Surgical Sutures market is segmented into suture threads and automated suturing devices. The suture threads segment dominated the largest market revenue share of 72.8% in 2025, driven by their extensive use across a wide range of surgical procedures including cardiovascular, orthopedic, gynecological, and general surgeries. Suture threads remain the most widely used wound closure method due to their cost-effectiveness, reliability, and ease of use. Hospitals and surgical centers rely heavily on traditional suturing techniques for both routine and complex surgeries. The increasing number of surgical procedures across Europe significantly contributes to the strong demand for suture threads. Continuous advancements in absorbable and non-absorbable suture materials also enhance clinical outcomes and patient safety. In addition, the availability of different suture sizes, materials, and needle combinations supports their widespread application. Surgeons often prefer suture threads because they provide precise wound closure and reduce the risk of complications. Growing healthcare infrastructure and rising surgical volumes further strengthen this segment. Product innovations such as antibacterial coated sutures also contribute to segment expansion. The increasing aging population undergoing surgical procedures continues to drive demand. As a result, suture threads remain the dominant product segment in the surgical sutures market.

The automated suturing devices segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by the growing adoption of advanced surgical technologies and minimally invasive procedures. Automated suturing devices enable faster and more efficient wound closure, improving surgical precision and reducing operation time. Surgeons increasingly prefer automated devices in laparoscopic and robotic surgeries where manual suturing can be challenging. The demand for minimally invasive procedures is rising rapidly due to shorter hospital stays and faster patient recovery. Technological advancements in automated suturing tools are improving usability and clinical outcomes. Hospitals and ambulatory surgical centers are increasingly investing in advanced surgical devices to enhance efficiency. In addition, automated suturing devices reduce surgeon fatigue during long and complex surgeries. Increasing healthcare spending and technological integration in surgical practices further support market growth. Medical device manufacturers are introducing innovative automated suturing systems with enhanced ergonomics and safety features. Training programs for surgeons are also encouraging adoption. As surgical procedures continue to increase across North America, the automated suturing devices segment is expected to grow rapidly.

- By Type

On the basis of type, the market is segmented into multifilament sutures and monofilament sutures. The monofilament sutures segment held the largest market revenue share of 58.4% in 2025, driven by their superior infection resistance and reduced tissue trauma compared to multifilament sutures. Monofilament sutures consist of a single strand of material, which minimizes bacterial colonization and reduces the risk of surgical site infections. These sutures are widely used in cardiovascular, ophthalmic, and plastic surgeries where precision and minimal tissue reaction are critical. Surgeons often prefer monofilament sutures because they glide smoothly through tissues, reducing friction during wound closure. The increasing focus on infection prevention and patient safety also supports the widespread use of monofilament sutures. Hospitals and surgical centers increasingly adopt these sutures in delicate surgical procedures. Technological advancements in polymer materials have further improved the strength and flexibility of monofilament sutures. In addition, the rising number of minimally invasive surgeries contributes to segment growth. Healthcare providers emphasize high-quality sutures to improve surgical outcomes and reduce complications. The availability of absorbable monofilament sutures further expands their applications. As surgical procedures continue to rise across North America, monofilament sutures maintain their dominance in the market.

The multifilament sutures segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, fueled by their strong knot security and flexibility, which make them suitable for various surgical procedures. Multifilament sutures are composed of multiple braided strands that provide excellent handling characteristics for surgeons. These sutures are commonly used in orthopedic, general, and gynecological surgeries where secure wound closure is essential. Surgeons often prefer multifilament sutures in procedures requiring strong tissue approximation. The braided structure enhances knot strength and stability, reducing the risk of suture slippage. Increasing surgical volumes and expanding healthcare infrastructure contribute to growing demand. Advances in coating technologies have improved the smoothness and antibacterial properties of multifilament sutures. In addition, manufacturers are introducing innovative products to reduce infection risks. The increasing adoption of advanced suturing materials further supports market growth. Training programs and surgical education initiatives are also improving surgeon familiarity with multifilament sutures. Growing healthcare investments and rising surgical procedures in Europe continue to drive this segment. As a result, multifilament sutures are expected to experience steady growth during the forecast period.

- By Application

On the basis of application, the market is segmented into cardiovascular surgery, general surgery, gynaecological surgery, orthopaedic surgeries, ophthalmic surgery, cosmetic and plastic surgery, and other applications. The general surgery segment accounted for the largest market revenue share of 36.9% in 2025, driven by the high volume of general surgical procedures performed across hospitals and healthcare facilities. Surgical sutures are widely used in procedures such as appendectomies, hernia repairs, gastrointestinal surgeries, and abdominal surgeries. The rising prevalence of chronic diseases requiring surgical interventions significantly contributes to segment growth. Hospitals and surgical centers rely on sutures as essential tools for wound closure and tissue repair. Increasing healthcare accessibility and improved surgical infrastructure across Europe further support demand. Surgeons prefer advanced suture materials that enhance healing and minimize infection risks. Technological advancements in suturing techniques and materials also contribute to improved clinical outcomes. In addition, the aging population undergoing surgical treatments increases the need for sutures. Government healthcare spending and insurance coverage for surgeries also boost procedure volumes. Continuous product innovation by medical device companies further strengthens market growth. As surgical procedures continue to increase, the general surgery segment remains the dominant application in the surgical sutures market.

The cosmetic and plastic surgery segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by the increasing demand for aesthetic procedures and reconstructive surgeries. Cosmetic surgeries such as facelifts, rhinoplasty, and breast augmentation require high-precision sutures to ensure minimal scarring and optimal healing. The growing influence of social media and increasing consumer awareness about aesthetic procedures contribute significantly to demand. Surgeons prefer advanced sutures that provide better cosmetic outcomes and reduce visible scars. Technological innovations in absorbable and fine sutures have enhanced their effectiveness in plastic surgeries. The rise in medical tourism and availability of specialized cosmetic clinics further boost segment growth. Increasing disposable incomes and changing beauty standards encourage more individuals to opt for aesthetic procedures. In addition, reconstructive surgeries following trauma or medical conditions also require specialized suturing techniques. Hospitals and specialty clinics are investing in advanced surgical materials to improve patient satisfaction. Growing acceptance of cosmetic procedures among both men and women also supports market expansion. As aesthetic medicine continues to grow, the cosmetic and plastic surgery segment is expected to experience the fastest growth.

- By End-User

On the basis of end-user, the market is segmented into hospitals, ambulatory surgical centres (ASC), clinics, and physician offices. The hospitals segment dominated the largest market revenue share of 61.7% in 2025, driven by the high number of surgical procedures performed in hospital settings. Hospitals possess advanced surgical infrastructure and specialized medical professionals capable of handling complex surgical cases. The availability of operating rooms, sterilization facilities, and post-operative care units makes hospitals the primary location for surgeries. In addition, hospitals perform a wide range of procedures including cardiovascular, orthopedic, and general surgeries that require suturing. Government healthcare funding and insurance coverage further support hospital surgical volumes. Large hospitals often adopt advanced suturing technologies and materials to improve clinical outcomes. The presence of multidisciplinary surgical teams also supports complex procedures. Increasing hospital admissions for chronic diseases contributes to the demand for surgical sutures. Medical training institutions within hospitals further enhance the use of advanced suturing techniques. Continuous investment in healthcare infrastructure strengthens hospital dominance. As surgical volumes continue to increase, hospitals remain the largest end-user segment.

The ambulatory surgical centres (ASC) segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, driven by the growing shift toward outpatient surgical procedures. ASCs offer cost-effective and efficient alternatives to hospital-based surgeries. Patients increasingly prefer ASCs due to shorter waiting times, reduced costs, and faster recovery periods. Minimally invasive surgical techniques have further enabled many procedures to be performed in outpatient settings. ASCs are rapidly expanding across Europe to meet increasing surgical demand. These centers require reliable suturing products to support efficient wound closure during procedures. Healthcare providers are increasingly investing in ASCs to reduce the burden on hospitals. Advances in surgical technologies and anesthesia techniques also support outpatient surgeries. Government policies encouraging cost-effective healthcare delivery contribute to ASC growth. In addition, improved healthcare infrastructure and rising patient awareness support the expansion of ambulatory care facilities. As outpatient surgical procedures continue to increase, ASCs are expected to experience the fastest growth in the surgical sutures market.

Europe Surgical Sutures Market Regional Analysis

- Europe dominated the surgical sutures market with the largest revenue share in 2025, supported by the region’s highly developed healthcare infrastructure, increasing surgical procedure volumes, and the strong presence of leading medical device manufacturers that continuously introduce advanced wound closure products. The region benefits from well-established hospital networks, highly skilled surgical professionals, and widespread access to modern medical technologies, which collectively contribute to the extensive use of surgical sutures across a wide range of procedures including cardiovascular, orthopedic, and general surgeries

- Healthcare providers in the region highly value the reliability, precision, and effectiveness offered by modern surgical sutures in ensuring secure wound closure and optimal healing outcomes. The availability of technologically advanced sutures such as absorbable sutures, antimicrobial-coated sutures, and specialty sutures supports improved patient recovery and reduces the risk of post-operative complications. These products are widely used across hospitals, ambulatory surgical centers, and specialty clinics to enhance surgical efficiency and patient safety

- This widespread adoption is further supported by increasing healthcare spending, strong reimbursement frameworks, and continuous advancements in surgical techniques. In addition, the increasing prevalence of chronic diseases, a growing aging population requiring surgical interventions, and ongoing investments in healthcare innovation continue to strengthen the demand for surgical sutures across Europe

U.K. Surgical Sutures Market Insight

The U.K. surgical sutures market dominated the Surgical Sutures market with the largest revenue share of 29.8% in 2025, characterized by a well-established healthcare system, high surgical procedure volumes, and the strong presence of leading medical device manufacturers and advanced surgical technologies. Hospitals and surgical centers across the country perform a significant number of procedures annually, including cardiovascular surgeries, orthopedic operations, and minimally invasive procedures that require reliable wound closure solutions. Furthermore, continuous product innovations such as antibacterial sutures, barbed sutures, and absorbable materials are enhancing surgical efficiency and patient outcomes. The growing focus on patient safety, infection prevention, and improved surgical outcomes is further supporting the adoption of advanced surgical sutures across hospitals and ambulatory surgical centers throughout the U.K.

Germany Surgical Sutures Market Insight

The Germany surgical sutures market is expected to be the fastest growing country in the Surgical Sutures market during the forecast period, with a projected CAGR of 9.1%. This growth is driven by increasing healthcare expenditure, rising surgical procedure volumes, and the growing adoption of advanced wound closure products across hospitals and surgical centers. Germany has one of the largest healthcare systems in Europe, supported by continuous investments in hospital infrastructure and surgical technologies. Additionally, the increasing prevalence of chronic diseases such as cardiovascular disorders, cancer, and orthopedic conditions is contributing to the rising demand for surgical procedures. Healthcare providers are also increasingly adopting advanced absorbable and antimicrobial sutures to enhance surgical outcomes and reduce infection risks, which is expected to further drive the growth of the surgical sutures market in Germany during the forecast period.

Europe Surgical Sutures Market Share

The Surgical Sutures industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Medtronic (Ireland)

- B. Braun S.E. (Germany)

- Smith & Nephew (U.K.)

- Boston Scientific (U.S.)

- Teleflex Incorporated (U.S.)

- Stryker Corporation (U.S.)

- Conmed Corporation (U.S.)

- Apollo Endosurgery (U.S.)

- DemeTECH Corporation (U.S.)

- Sutures India Pvt. Ltd. (India)

- Healthium Medtech (India)

- Internacional Farmacéutica S.A. de C.V. (Mexico)

- Peters Surgical (France)

- Mani Inc. (Japan)

- Dolphin Sutures (India)

- Lotus Surgicals (India)

- Riverpoint Medical (U.S.)

- W. L. Gore & Associates (U.S.)

- Zimmer Biomet (U.S.)

Latest Developments in Europe Surgical Sutures Market

- In February 2021, Corza Medical, a global provider of surgical solutions, announced the acquisition of Surgical Specialties Corporation, a company known for its surgical sutures and ophthalmic knives portfolio. The acquisition strengthened Corza Medical’s position in the global wound closure market by expanding its surgical sutures product offerings and distribution network across multiple regions

- In August 2023, Healthium Medtech launched TRUMAS™, a specialized range of surgical sutures designed for minimal access surgery, aimed at improving suturing efficiency in laparoscopic and minimally invasive procedures. The new product line was developed to address challenges associated with limited access surgical environments and enhance surgical precision and patient outcomes

- In September 2023, Genesis MedTech received regulatory approval from China’s National Medical Products Administration (NMPA) for its antibacterial sutures, designed to reduce surgical site infections and improve postoperative healing. The launch expanded the availability of advanced infection-resistant sutures in the Asia-Pacific region

- In May 2023, researchers at the Massachusetts Institute of Technology (MIT) developed smart sutures capable of detecting inflammation and delivering therapeutic drugs directly to wounds, representing a breakthrough in next-generation wound closure technology and enabling real-time monitoring of surgical healing processes

- In June 2023, Samyang Holdings Corp., a global manufacturer of biodegradable suture materials, completed the construction of a US$21.9 million surgical material production facility in Hungary, aimed at expanding manufacturing capacity and strengthening its presence in the European medical device market

- In March 2024, private equity firms including Mankind Pharma and ChrysCapital submitted bids to acquire Healthium Medtech, a major global surgical sutures manufacturer previously owned by Apax Partners. The strategic interest highlighted the increasing consolidation and investment activity in the global wound closure and surgical sutures industry

- In April 2024, Samyang Holdings inaugurated a new USD 22 million surgical suture manufacturing facility in Hungary, significantly expanding production capacity and enabling the company to strengthen supply of biodegradable suture materials across European healthcare markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.