Europe Teleradiology Market

Market Size in USD Million

CAGR :

%

USD

911.74 Million

USD

3,497.42 Million

2025

2033

USD

911.74 Million

USD

3,497.42 Million

2025

2033

| 2026 –2033 | |

| USD 911.74 Million | |

| USD 3,497.42 Million | |

| % | |

|

Europe Teleradiology Market Size

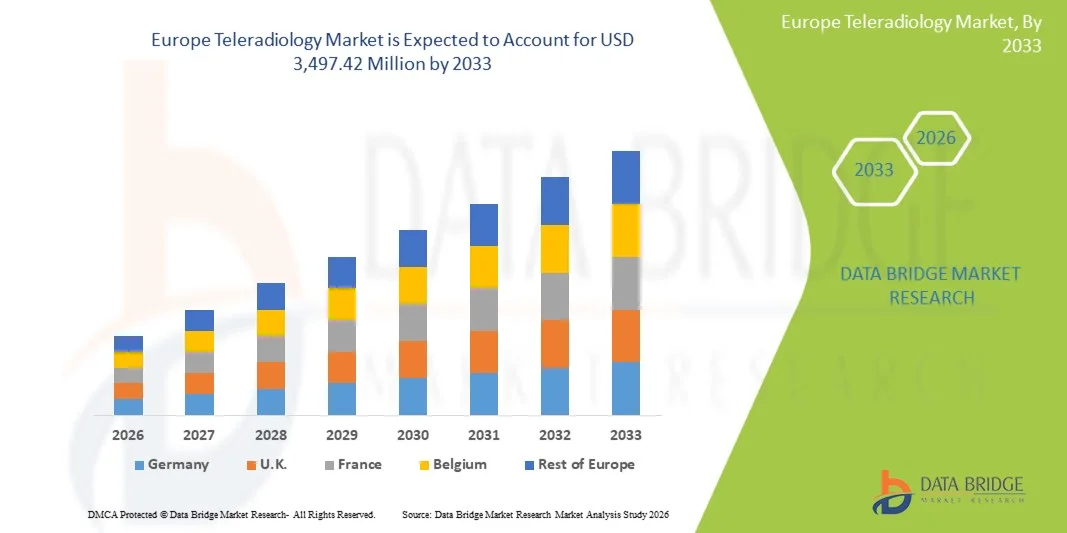

- The Europe teleradiology market size was valued at USD 911.74 million in 2025 and is expected to reach USD 3,497.42 million by 2033, at a CAGR of 18.3% during the forecast period

- The market growth is primarily driven by the rising demand for remote diagnostic imaging services, increasing shortage of radiologists across several European countries, and the growing adoption of digital healthcare infrastructure and AI-enabled imaging solutions

- Furthermore, increasing cross-border healthcare collaboration, expansion of hospital PACS (Picture Archiving and Communication Systems), and the need for faster, cost-effective diagnostic reporting are significantly accelerating the adoption of teleradiology services across Europe, thereby boosting overall market growth

Europe Teleradiology Market Analysis

- Teleradiology, enabling the remote transmission and interpretation of medical imaging such as X-rays, CT scans, and MRI scans, is becoming a critical component of Europe’s digital healthcare ecosystem due to improved diagnostic efficiency, enhanced specialist access, and streamlined workflow integration across hospitals and diagnostic centers

- The escalating demand for Europe teleradiology market is primarily driven by the shortage of radiologists in several European countries, increasing incidence of chronic and emergency conditions requiring advanced imaging, and rapid adoption of cloud-based imaging platforms and AI-assisted diagnostic tools

- Germany dominated the Europe teleradiology market with the largest revenue share of 28.6% in 2025, supported by advanced healthcare infrastructure, high hospital digitization, strong radiology networks, and early adoption of AI-enabled imaging solutions across major diagnostic centers and tertiary care hospitals

- The United Kingdom is expected to be the fastest growing country in the Europe teleradiology market during the forecast period, owing to rising NHS digital transformation initiatives, increasing demand for remote reporting services, and growing adoption of AI-based radiology workflow systems

- The tele-diagnosis segment dominated the Europe teleradiology market with the largest revenue share of 61.3% in 2025, driven by its ability to support remote interpretation of imaging data, reduce turnaround time for diagnosis, and improve access to specialist radiologists across both urban and rural healthcare facilities

Report Scope and Europe Teleradiology Market Segmentation

|

Attributes |

Europe Teleradiology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Teleradiology Market Trends

“Expansion of AI-Enabled Remote Imaging and Cloud-Based Diagnostics”

- A significant and accelerating trend in the Europe teleradiology market is the growing integration of artificial intelligence (AI) and cloud-based imaging platforms to enhance remote diagnostic accuracy, speed, and workflow efficiency across hospitals and diagnostic centers

- For instance, AI-powered imaging systems are increasingly being integrated with PACS and RIS platforms across European healthcare networks, enabling radiologists to detect abnormalities faster and support automated image triaging for urgent cases

- AI integration in teleradiology enables features such as automated image enhancement, lesion detection support, and predictive analytics for radiology workflow prioritization, improving reporting accuracy and reducing turnaround time for critical diagnoses

- The seamless integration of teleradiology platforms with hospital information systems and electronic health records facilitates centralized access to imaging data, enabling cross-border consultations and real-time collaboration among specialist radiologists

- This trend towards intelligent, interoperable, and cloud-driven diagnostic ecosystems is fundamentally reshaping radiology workflows, with companies developing advanced remote reporting solutions and AI-assisted diagnostic tools for European healthcare providers

- The demand for AI-driven teleradiology services is growing rapidly across Europe as healthcare systems increasingly prioritize faster diagnosis, improved patient outcomes, and cost-efficient imaging workflows in both public and private healthcare sectors

- Furthermore, the rising collaboration between hospitals and third-party teleradiology service providers is expanding access to specialized expertise, especially in underserved regions and smaller healthcare facilities across Europe

Europe Teleradiology Market Dynamics

Driver

“Rising Demand Due to Radiologist Shortage and Digital Healthcare Expansion”

- The increasing shortage of radiologists across several European countries, coupled with the rapid expansion of digital healthcare infrastructure, is a major driver accelerating the demand for teleradiology services in hospitals and diagnostic centers

- For instance, in April 2025, several European healthcare networks expanded remote reporting collaborations to address imaging backlogs, enabling faster diagnosis through outsourced and cloud-based teleradiology platforms

- As healthcare providers face rising imaging volumes from chronic diseases and emergency cases, teleradiology offers efficient remote interpretation services, reducing workload pressure on in-house radiologists and improving diagnostic turnaround time

- Furthermore, the growing adoption of AI-enabled imaging tools and cloud-based PACS systems is making teleradiology an essential part of modern hospital workflows, enabling seamless data sharing and remote consultation capabilities

- The convenience of 24/7 remote diagnostic support, improved access to subspecialty radiologists, and faster reporting for critical cases are key factors propelling the adoption of teleradiology services across Europe

Restraint/Challenge

“Cybersecurity Risks and Data Privacy Compliance Hurdles”

- Concerns surrounding cybersecurity vulnerabilities and data privacy compliance pose a significant challenge to broader adoption of teleradiology services due to the sensitive nature of medical imaging data transmission across networks

- For instance, increasing reports of healthcare data breaches in digital imaging systems have raised concerns among hospitals and patients regarding unauthorized access to radiology databases and cloud-based platforms

- Addressing these cybersecurity challenges through advanced encryption, secure authentication protocols, and compliance with strict regulations such as GDPR is essential for ensuring trust and system reliability

- While major providers emphasize secure cloud architecture and encrypted data exchange, the high cost of implementing advanced cybersecurity infrastructure can be a barrier for smaller healthcare facilities and diagnostic centers

- Overcoming these challenges through stronger regulatory compliance, improved cybersecurity frameworks, and wider investment in secure digital health infrastructure will be critical for sustained market growth

- Furthermore, interoperability issues between legacy hospital systems and modern cloud-based teleradiology platforms can delay seamless data exchange, impacting operational efficiency and workflow integration

- In addition, resistance from healthcare professionals due to concerns over remote diagnostics accuracy and dependency on digital systems continues to slow down full-scale adoption in certain European healthcare settings

Europe Teleradiology Market Scope

The market is segmented on the basis of type, delivery mode, imaging technique, technology, procedure, application, site, age, mode of purchase, and end user.

- By Type

On the basis of type, the Europe teleradiology market is segmented into hardware, systems, software, telecom, and networking services. The software segment dominated the market with the largest revenue share of 38.5% in 2025, driven by the rapid adoption of AI-enabled diagnostic platforms, cloud-based PACS integration, and advanced radiology workflow management solutions. Healthcare providers increasingly rely on software solutions for image storage, transmission, and remote reporting, improving efficiency and reducing diagnostic turnaround time. The growing shift toward digital healthcare infrastructure and interoperability between hospital systems further strengthens software dominance in the market. In addition, continuous upgrades in imaging analytics and AI-assisted diagnosis tools are accelerating demand for advanced teleradiology software solutions.

The telecom and networking services segment is expected to witness the fastest growth rate of 19.8% from 2026 to 2033, fueled by rising demand for high-speed data transmission and secure connectivity for large medical imaging files. Increasing reliance on 5G networks, fiber-optic communication, and secure cloud networks enables faster and more reliable image transfer between healthcare facilities. The expansion of cross-border teleradiology services within Europe also boosts demand for robust telecom infrastructure. Furthermore, growing investments in secure data encryption and real-time connectivity solutions are supporting the rapid expansion of this segment.

- By Delivery Mode

On the basis of delivery mode, the Europe teleradiology market is segmented into web-based delivery mode, cloud-based delivery mode, and on-premise delivery mode. The cloud-based delivery mode dominated the market with the largest revenue share of 52.1% in 2025, driven by its scalability, cost efficiency, and ability to support remote access to imaging data from multiple locations. Hospitals and diagnostic centers increasingly prefer cloud platforms for centralized data storage and seamless collaboration among radiologists. The integration of AI tools and real-time reporting capabilities further enhances cloud adoption. In addition, compliance with European data security regulations has improved trust in cloud-based healthcare systems.

The web-based delivery mode is expected to witness the fastest growth rate of 18.6% from 2026 to 2033, supported by its ease of deployment and minimal infrastructure requirements. Web-based systems allow healthcare providers to access imaging data through browsers without complex installations, making them highly suitable for small and mid-sized facilities. Increasing demand for flexible remote diagnostic solutions and growing adoption of telehealth platforms are accelerating segment growth. Furthermore, continuous improvements in browser security and bandwidth efficiency are enhancing system reliability and usability.

- By Imaging Technique

On the basis of imaging technique, the Europe teleradiology market is segmented into small matrix size and large matrix size. The large matrix size segment dominated the market with the largest revenue share of 64.3% in 2025, driven by its ability to deliver high-resolution imaging essential for complex diagnostic applications such as oncology, neurology, and cardiology. Large matrix imaging enables clearer visualization of fine anatomical structures, improving diagnostic accuracy in remote reporting workflows. The increasing adoption of advanced CT and MRI systems across European hospitals further strengthens this segment. In addition, growing reliance on AI-based image analysis tools is enhancing the utilization of high-resolution imaging formats.

The small matrix size segment is expected to witness the fastest growth rate of 17.9% from 2026 to 2033, supported by its lower data storage requirements and faster transmission speeds. It is widely used in basic diagnostic procedures and emergency screening cases where rapid reporting is critical. Smaller healthcare facilities and rural hospitals prefer this format due to lower infrastructure requirements. Furthermore, advancements in image compression technologies are improving diagnostic usability even with smaller matrix outputs.

- By Technology

On the basis of technology, the market is segmented into advanced graphics processing, volume rendering, multiplanar reconstructions, and image compression. The volume rendering segment dominated the market with the largest revenue share of 35.7% in 2025, driven by its ability to create detailed 3D visualizations of anatomical structures, significantly improving diagnostic interpretation in complex cases. It is widely used in oncology and cardiovascular imaging for enhanced treatment planning. Integration of volume rendering with AI tools further improves precision and diagnostic efficiency. In addition, increasing adoption of advanced imaging workstations in European hospitals supports segment dominance.

The image compression segment is expected to witness the fastest growth rate of 20.4% from 2026 to 2033, fueled by the rising need for efficient transmission of large imaging files over cloud-based and remote platforms. Compression technologies reduce bandwidth usage while maintaining diagnostic quality, making them essential for cross-border teleradiology services. Increasing demand for real-time remote diagnostics is accelerating adoption. Furthermore, advancements in lossless compression techniques are improving image integrity and reliability.

- By Procedure

On the basis of procedure, the market is segmented into tele-consultation, tele-diagnosis, and tele-monitoring. The tele-diagnosis segment dominated the market with the largest revenue share of 61.3% in 2025, driven by its central role in remote interpretation of medical imaging and rapid diagnostic decision-making. Hospitals across Europe increasingly rely on tele-diagnosis to manage high imaging volumes and reduce radiologist workload. The growing integration of AI-based diagnostic support tools enhances accuracy and efficiency. In addition, rising demand for emergency imaging interpretation further strengthens segment leadership.

The tele-monitoring segment is expected to witness the fastest growth rate of 18.7% from 2026 to 2033, supported by increasing use of remote patient monitoring in chronic disease management and post-treatment imaging follow-ups. Healthcare providers are adopting continuous monitoring systems for oncology and neurological patients. Integration with wearable and connected health devices is further enhancing segment growth. Moreover, increasing focus on preventive healthcare is driving long-term adoption.

- By Application

On the basis of application, the market is segmented into cardiology, neurology, oncology, musculoskeletal, gastroenterology, pelvic and abdominal, gynecology, urology, mammography, dental, and others. The oncology segment dominated the market with the largest revenue share of 27.9% in 2025, driven by rising cancer prevalence across Europe and high dependency on imaging for diagnosis, staging, and treatment monitoring. Advanced imaging techniques such as CT, MRI, and PET scans are widely used in oncology workflows. Increasing adoption of AI-powered tumor detection tools further strengthens this segment. In addition, growing demand for early cancer detection supports sustained dominance.

The neurology segment is expected to witness the fastest growth rate of 19.2% from 2026 to 2033, fueled by rising incidence of neurological disorders such as stroke, Alzheimer’s, and epilepsy. Increasing use of MRI-based brain imaging and real-time remote diagnostics is accelerating segment expansion. The shortage of specialized neurologists in several European regions further boosts reliance on teleradiology. Furthermore, advancements in neuroimaging analytics are improving diagnostic accuracy and speed.

- By Site

On the basis of site, the Europe teleradiology market is segmented into in-house, offshore, and onshore. The in-house segment dominated the market with the largest revenue share of 49.6% in 2025, driven by hospitals and diagnostic centers preferring direct control over imaging data, faster communication between radiologists and clinicians, and improved compliance with strict European data privacy regulations. In-house deployment ensures better integration with hospital PACS systems and reduces dependency on external service providers. The increasing need for real-time emergency diagnostics further strengthens this segment. In addition, large tertiary care hospitals across Europe continue to invest heavily in internal radiology infrastructure.

The offshore segment is expected to witness the fastest growth rate of 21.3% from 2026 to 2033, fueled by rising demand for cost-effective radiology reporting services and shortage of specialist radiologists in several European countries. Offshore teleradiology providers offer round-the-clock reporting services, improving turnaround time for hospitals. Increasing adoption of cross-border healthcare collaborations within Europe is also supporting segment expansion. Furthermore, advancements in secure cloud-based imaging transmission are enabling safe offshore diagnostics.

- By Age

On the basis of age, the Europe teleradiology market is segmented into pediatric, geriatric, and adults. The geriatric segment dominated the market with the largest revenue share of 44.8% in 2025, driven by the rapidly aging population in Europe and higher prevalence of chronic diseases requiring frequent imaging such as cardiovascular disorders, cancer, and musculoskeletal conditions. Elderly patients undergo more diagnostic imaging procedures, increasing reliance on teleradiology services. The growing demand for early disease detection and continuous monitoring further strengthens this segment. In addition, healthcare systems across Europe are prioritizing elderly care, boosting imaging volumes.

The pediatric segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, supported by increasing awareness of early diagnosis of congenital and developmental disorders. Advancements in low-dose imaging techniques are encouraging more frequent pediatric imaging procedures. Rising adoption of telemedicine in pediatric care, especially in rural and underserved regions, is further accelerating growth. Moreover, improved AI-based imaging tools are enhancing diagnostic accuracy in children.

- By Mode of Purchase

On the basis of mode of purchase, the market is segmented into group purchase and individual purchase. The group purchase segment dominated the market with the largest revenue share of 62.4% in 2025, driven by hospital networks, diagnostic chains, and public healthcare systems opting for bulk procurement of teleradiology solutions to reduce costs and ensure standardized imaging infrastructure. Group purchasing agreements enable better pricing, centralized management, and seamless integration across multiple facilities. Increasing collaboration among hospital groups across Europe further strengthens this segment. In addition, large healthcare organizations prefer unified systems for improved workflow efficiency.

The individual purchase segment is expected to witness the fastest growth rate of 17.6% from 2026 to 2033, fueled by rising adoption among small clinics, independent diagnostic centers, and private practitioners. Lower-cost cloud-based solutions and subscription-based models are making teleradiology more accessible. Increasing demand for flexible and scalable imaging solutions is also driving adoption. Furthermore, growing digitalization of small healthcare facilities is accelerating segment expansion.

- By End User

On the basis of end user, the Europe teleradiology market is segmented into hospitals, ambulatory surgical centers, private physician offices, diagnostic imaging centers, and others. The hospitals segment dominated the market with the largest revenue share of 46.7% in 2025, driven by high patient inflow, extensive imaging requirements, and strong integration of advanced radiology systems within hospital networks. Hospitals rely heavily on teleradiology for emergency diagnostics, inpatient care, and specialist consultations. Increasing adoption of AI-enabled imaging platforms further strengthens this segment. In addition, government investments in hospital digitalization across Europe support continued dominance.

The diagnostic imaging centers segment is expected to witness the fastest growth rate of 20.2% from 2026 to 2033, fueled by increasing demand for standalone imaging services and rising outsourcing of radiology workloads from hospitals. These centers benefit from cost efficiency and high patient throughput. Expansion of private diagnostic chains across Europe is further accelerating growth. Moreover, advancements in cloud-based reporting systems are enabling faster turnaround times and improved service delivery.

Europe Teleradiology Market Regional Analysis

- Germany dominated the Europe teleradiology market with the largest revenue share of 28.6% in 2025, supported by advanced healthcare infrastructure, high hospital digitization, strong radiology networks, and early adoption of AI-enabled imaging solutions across major diagnostic centers and tertiary care hospitals

- Healthcare providers in the country highly value the faster diagnostic turnaround, improved specialist access, and seamless integration of AI-powered imaging platforms with hospital PACS and RIS systems, enhancing overall clinical workflow efficiency

- This widespread adoption is further supported by a high imaging volume burden, strong presence of leading healthcare IT providers, and growing preference for cloud-based and cross-border teleradiology solutions within Germany’s well-established hospital network

The Germany Teleradiology Market Insight

The Germany teleradiology market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by its highly developed healthcare infrastructure and increasing adoption of advanced imaging technologies. Rising demand for faster diagnostic turnaround and growing integration of AI-enabled PACS systems are supporting market growth. Furthermore, Germany’s strong focus on healthcare digitization, strict data security regulations, and hospital automation initiatives is accelerating the adoption of secure, cloud-based teleradiology solutions across both public and private healthcare facilities.

United Kingdom Teleradiology Market Insight

The United Kingdom teleradiology market is expected to expand at a considerable CAGR during the forecast period, driven by NHS-led digital transformation initiatives and increasing demand for rapid diagnostic reporting services. The shortage of radiologists and rising imaging backlogs are encouraging hospitals to adopt remote reporting solutions. In addition, strong adoption of AI-based imaging tools and cloud platforms is improving workflow efficiency, reducing reporting delays, and enabling faster access to specialist radiology expertise across urban and rural healthcare settings in the country.

France Teleradiology Market Insight

The France teleradiology market is witnessing steady growth due to increasing digitalization of healthcare services and rising demand for efficient diagnostic imaging solutions. Growing adoption of cloud-based radiology platforms and AI-assisted diagnostic tools is improving clinical workflow efficiency and accuracy in reporting. Furthermore, government initiatives supporting e-health transformation, along with increasing collaboration between public hospitals and private diagnostic centers, are strengthening the integration of teleradiology into the national healthcare system.

Italy Teleradiology Market Insight

The Italy teleradiology market is growing steadily, supported by rising demand for remote diagnostic services and increasing pressure on healthcare systems to improve efficiency amid rising patient volumes. The shortage of radiology specialists and growing dependence on advanced imaging modalities are encouraging wider adoption of teleradiology platforms. In addition, expansion of hospital digital infrastructure and increasing use of AI-powered imaging solutions are enhancing diagnostic accuracy and reducing turnaround time for critical cases across healthcare facilities.

Europe Teleradiology Market Share

The Europe Teleradiology industry is primarily led by well-established companies, including:

- Everlight Radiology (U.K.)

- 4ways Healthcare Limited (U.K.)

- Agfa-Gevaert NV (Belgium)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- FUJIFILM Europe GmbH (Germany)

- GE Healthcare (U.K.)

- Sectra AB (Sweden)

- Carestream Health Europe (U.K.)

- RamSoft Inc. (U.K.)

- Telemedicine Clinic (Spain)

- Teleradiology Solutions (U.K.)

- Radiology Reporting Online (U.K.)

- Ambra Health (U.K.)

- ONRAD Europe (U.K.)

- StatRad Europe (U.K.)

- Doctor NET (France)

- Medica Group PLC (U.K.)

- InHealth Group (U.K.)

- Alliance Medical Group (U.K.)

What are the Recent Developments in Europe Teleradiology Market?

- In November 2024, Philips Healthcare (Koninklijke Philips N.V.) announced expanded deployment of its cloud-based enterprise imaging and teleradiology solutions across multiple European hospital networks to enhance remote diagnostics and cross-site radiology reporting efficiency. The initiative supports improved interoperability between hospitals and centralized radiology services

- In October 2024, the European Society of Radiology (ESR) highlighted the growing expansion of AI-assisted teleradiology workflows across European hospitals during its annual conference, emphasizing the increasing use of remote reporting systems to address radiologist shortages and improve diagnostic turnaround times across cross-border healthcare networks

- In May 2024, Aidoc, a leading AI-based medical imaging company, expanded its AI-powered radiology solutions deployment across hospitals in Germany and Austria to support teleradiology workflows and improve emergency diagnostic turnaround times. The integration focused on stroke, pulmonary embolism, and trauma imaging, strengthening AI-assisted remote radiology interpretation across European healthcare systems

- In June 2023, the UK National Health Service (NHS) expanded its use of remote radiology reporting networks, increasing collaboration with external teleradiology providers to reduce imaging backlogs and improve emergency diagnostic response times across multiple NHS Trust hospitals

- In March 2022, the European Commission supported digital health infrastructure expansion under its EU4Health programme, accelerating adoption of interoperable imaging systems and cross-border teleradiology services to strengthen healthcare resilience across EU member states

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.