Europe Vital Signs Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

2.86 Billion

USD

4.58 Billion

2025

2033

USD

2.86 Billion

USD

4.58 Billion

2025

2033

| 2026 –2033 | |

| USD 2.86 Billion | |

| USD 4.58 Billion | |

| % | |

|

Europe Vital Signs Monitoring Market Size

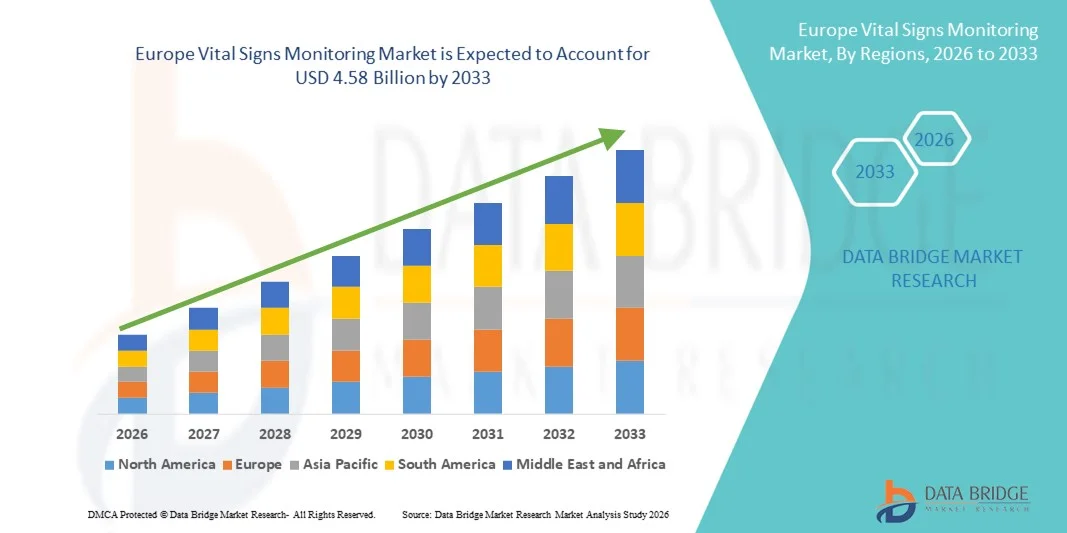

- The Europe vital signs monitoring market size was valued at USD 2.86 billion in 2025 and is expected to reach USD 4.58 billion by 2033, at a CAGR of 6.07% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases, increasing patient awareness, and the integration of advanced monitoring technologies such as wearable and remote monitoring devices in healthcare settings

- Furthermore, growing demand for real-time, non-invasive, and connected patient monitoring solutions in hospitals, clinics, and home healthcare is driving the adoption of vital signs monitoring systems. These factors are accelerating the uptake of advanced monitoring solutions, thereby significantly boosting the industry's growth

Europe Vital Signs Monitoring Market Analysis

- Vital signs monitoring systems, encompassing devices that track parameters such as temperature, blood pressure, and oxygen saturation, are becoming essential components of modern healthcare infrastructure in hospitals, clinics, and home care due to their ability to provide continuous, real-time patient data and integration with digital health platforms

- The rising demand for vital signs monitoring is primarily driven by increasing prevalence of chronic diseases, an aging population, and growing adoption of connected and portable monitoring technologies

- Germany dominated the Europe vital signs monitoring market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high adoption of connected health technologies, and a strong presence of leading medical device manufacturers, with substantial deployment of vital signs monitoring solutions in hospitals and clinics

- Poland is expected to be the fastest-growing country in the Europe vital signs monitoring market during the forecast period due to ongoing healthcare modernization initiatives, rising awareness about continuous patient monitoring, and expansion of home healthcare services

- Temperature monitoring devices dominated the Europe vital signs monitoring market with a market share of 41.7% in 2025, driven by their ease of use, non-invasive design, and critical role in early detection and continuous tracking of patient health conditions

Report Scope and Europe Vital Signs Monitoring Market Segmentation

|

Attributes |

Europe Vital Signs Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Vital Signs Monitoring Market Trends

Rise of Connected and AI-Enabled Monitoring Devices

- A significant and accelerating trend in the Europe vital signs monitoring market is the integration of AI and connected health technologies in devices such as wearable monitors, wireless blood pressure cuffs, and pulse oximeters, enhancing continuous patient monitoring and real-time data analysis

- For instance, the Biobeat wearable monitors provide continuous, cloud-connected vital signs tracking, allowing healthcare providers to remotely monitor multiple patients simultaneously. Similarly, TempTraq smart temperature patches enable non-invasive, continuous body temperature monitoring with mobile app integration

- AI integration in vital signs monitoring enables predictive analytics for early detection of patient deterioration and personalized health alerts, improving clinical decision-making. For instance, EarlySense systems analyze patient data trends to alert clinicians of abnormal vital signs before critical events occur

- The seamless integration of monitoring devices with hospital information systems and mobile health platforms facilitates centralized patient data management, enabling clinicians to view, track, and analyze vital signs across multiple patients through a single interface

- This trend towards intelligent, connected, and predictive monitoring solutions is reshaping healthcare expectations in Europe, with companies such as iHealth and Withings developing AI-enabled devices capable of remote monitoring, automated alerts, and seamless integration with telehealth platforms

- The demand for connected and AI-powered vital signs monitoring devices is growing rapidly across hospitals, clinics, and home healthcare, as providers increasingly prioritize proactive patient care, efficiency, and real-time data accessibility

- Growing partnerships between device manufacturers and telemedicine providers are expanding the availability of remote monitoring solutions, allowing clinicians to manage larger patient populations effectively and improve care outcomes

Europe Vital Signs Monitoring Market Dynamics

Driver

Increasing Chronic Disease Burden and Remote Monitoring Adoption

- The rising prevalence of chronic diseases such as hypertension, cardiovascular disorders, and respiratory illnesses, combined with the increasing adoption of remote patient monitoring, is a key driver for the Europe vital signs monitoring market

- For instance, in March 2025, Philips launched expanded remote monitoring programs across Germany and France, integrating connected blood pressure monitors and pulse oximeters into telehealth platforms to improve patient management

- As patient populations age and healthcare systems focus on preventive care, vital signs monitoring devices provide critical tools for early detection, continuous tracking, and timely intervention, reducing hospital readmissions

- Furthermore, the growing demand for home healthcare solutions and telemedicine services is driving adoption of portable, connected devices capable of transmitting real-time data to clinicians for remote evaluation and decision-making

- Ease of use, non-invasive operation, and integration with digital health platforms are making these devices increasingly popular in hospitals, physician offices, and home care settings, boosting market expansion across Europe

- Rising government initiatives and funding for digital health adoption are supporting the deployment of connected vital signs monitoring devices in public healthcare facilities, particularly in countries such as Germany, France, and the U.K.

- Increasing awareness among patients and caregivers regarding the benefits of continuous monitoring is driving demand for wearable and home-use devices, expanding the market beyond traditional hospital settings

Restraint/Challenge

High Costs and Data Privacy Concerns

- The relatively high cost of advanced vital signs monitoring devices compared to conventional equipment poses a challenge, particularly for smaller healthcare facilities and price-sensitive patients in some European countries

- For instance, premium AI-enabled wearable monitors with cloud connectivity can cost several times more than traditional monitoring equipment, limiting adoption despite their clinical advantages

- Data privacy and cybersecurity concerns regarding connected health devices also pose significant challenges, as sensitive patient information is transmitted and stored digitally, raising regulatory and trust issues

- Addressing these concerns requires robust encryption protocols, compliance with GDPR and other regional data protection regulations, and regular software updates to prevent unauthorized access

- While gradual cost reductions and increasing awareness of remote monitoring benefits are helping, perceived high costs and concerns over data security continue to restrain widespread adoption, particularly in home healthcare and smaller clinics

- Limited interoperability between different device brands and healthcare IT systems can hinder seamless integration, complicating data management for hospitals and telehealth providers

- Resistance to adopting new technology among some healthcare professionals, due to training requirements and workflow adjustments, may slow the uptake of advanced monitoring solutions despite their clinical advantages

Europe Vital Signs Monitoring Market Scope

The market is segmented on the basis of product type and end use.

- By Product Type

On the basis of product type, the Europe vital signs monitoring market is segmented into temperature monitoring devices, blood pressure monitors, and pulse oximeters. The temperature monitoring devices segment dominated the market with the largest market revenue share of 41.7% in 2025, driven by their critical role in early detection of fever and infection, particularly in hospitals and home healthcare settings. Hospitals and clinics prefer temperature monitoring devices due to their non-invasive design, ease of use, and ability to continuously track patient conditions, reducing the risk of undetected clinical deterioration. The increasing integration of connected and wearable temperature sensors with mobile apps and hospital information systems further strengthens their adoption. Rising awareness of infection control, particularly in emergency care centers and physician offices, is also fueling demand. In addition, advancements in infrared and wearable technologies are enhancing accuracy and patient comfort, boosting preference among healthcare providers. Overall, temperature monitoring devices are viewed as essential first-line tools for patient monitoring in Europe.

The blood pressure monitors segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the rising prevalence of hypertension and cardiovascular disorders across Europe. The growing adoption of home healthcare and remote patient monitoring programs is fueling demand, as patients increasingly prefer self-monitoring of blood pressure. Blood pressure monitors integrated with IoT and mobile applications allow real-time transmission of data to clinicians, facilitating timely intervention and personalized care. Hospitals and ambulatory centers are also increasingly deploying automated blood pressure monitoring systems for continuous patient assessment. Furthermore, government health initiatives promoting preventive care and chronic disease management support the expansion of this segment. The combination of ease of use, clinical accuracy, and compatibility with telehealth solutions positions blood pressure monitors as the fastest-growing product type in the European market.

- By End Use

On the basis of end use, the Europe vital signs monitoring market is segmented into hospitals, physician’s offices, home healthcare, ambulatory centers, emergency care centers, and others. The hospitals segment dominated the market with the largest market revenue share in 2025, as hospitals require advanced vital signs monitoring solutions to manage high patient volumes and provide critical care. Hospitals invest in connected monitoring systems capable of tracking multiple patients simultaneously, ensuring timely detection of physiological changes. Integration with electronic health records allows seamless documentation and data-driven decision-making. Hospitals also benefit from AI-enabled predictive analytics that can alert clinicians to deteriorating conditions before they become critical. The increasing prevalence of chronic and acute diseases, alongside government funding for modern healthcare infrastructure, reinforces hospital adoption. Continuous training and support for clinical staff further drive the use of sophisticated monitoring devices in hospital settings.

The home healthcare segment is expected to witness the fastest growth during the forecast period due to increasing demand for remote patient monitoring and telehealth services. Patients and caregivers prefer home-use devices such as wearable temperature sensors, pulse oximeters, and blood pressure monitors to track vital signs conveniently and safely without frequent hospital visits. The rising adoption of connected devices enables real-time transmission of patient data to physicians, supporting proactive care and early intervention. In addition, the aging European population and increasing prevalence of chronic diseases are fueling demand for home monitoring solutions. Technological advancements improving device accuracy, usability, and affordability further accelerate growth. Moreover, insurance and government programs supporting home healthcare solutions contribute to expanding this segment rapidly.

Europe Vital Signs Monitoring Market Regional Analysis

- Germany dominated the Europe vital signs monitoring market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high adoption of connected health technologies, and a strong presence of leading medical device manufacturers, with substantial deployment of vital signs monitoring solutions in hospitals and clinics

- Healthcare providers in the region highly value the accuracy, real-time monitoring capabilities, and seamless integration of vital signs monitoring devices with hospital information systems and telehealth platforms

- This widespread adoption is further supported by a technologically skilled healthcare workforce, growing prevalence of chronic diseases, and increasing focus on preventive care, establishing vital signs monitoring systems as essential tools in hospitals, clinics, and home healthcare settings across Germany

The Germany Vital Signs Monitoring Market Insight

The Germany vital signs monitoring market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, high technological adoption, and strong government support for digital health programs. Hospitals and clinics in Germany increasingly invest in AI-enabled and connected monitoring devices to provide continuous patient care and real-time alerts. Germany’s focus on innovation and quality healthcare promotes the deployment of wearable and multi-parameter monitoring systems, particularly in hospitals and home healthcare settings. Integration with electronic health records and telehealth platforms is becoming increasingly prevalent, ensuring efficient patient data management and proactive clinical interventions. The rising prevalence of chronic diseases, coupled with an aging population, reinforces the need for reliable and accurate monitoring solutions

U.K. Vital Signs Monitoring Market Insight

The U.K. vital signs monitoring market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing trend of telehealth adoption and the need for enhanced patient monitoring in both hospitals and home healthcare. Growing awareness regarding chronic diseases and preventive care is encouraging healthcare providers to deploy connected monitoring solutions. The U.K.’s strong healthcare infrastructure, combined with high technological adoption among clinicians and patients, is fostering the integration of wearable and remote monitoring devices. Hospitals, physician offices, and home care services are increasingly incorporating devices such as blood pressure monitors, pulse oximeters, and temperature monitoring systems. Moreover, government initiatives supporting digital health and remote patient management are expected to further stimulate market growth

France Vital Signs Monitoring Market Insight

The France vital signs monitoring market is poised to grow steadily during the forecast period, driven by the country’s investment in digital health infrastructure and the increasing prevalence of chronic and lifestyle-related diseases. French hospitals and clinics are adopting advanced monitoring devices to improve patient care efficiency, enable early diagnosis, and reduce hospital readmissions. The integration of monitoring systems with mobile health applications and electronic health records allows for seamless data sharing among healthcare providers. Home healthcare and ambulatory care centers are also expanding their use of connected devices, supporting remote patient management and telemedicine services. Moreover, government initiatives promoting preventive care and chronic disease management reinforce the adoption of vital signs monitoring solutions

Poland Vital Signs Monitoring Market Insight

The Poland vital signs monitoring market is expected to witness the fastest growth in Europe during the forecast period, driven by ongoing healthcare modernization initiatives and increasing adoption of connected and remote monitoring solutions. Hospitals, clinics, and home healthcare providers in Poland are increasingly investing in devices such as blood pressure monitors, pulse oximeters, and temperature monitoring systems to improve patient care and enable real-time tracking of vital signs. The growing prevalence of chronic diseases, coupled with rising patient awareness and demand for preventive care, is accelerating adoption. Integration with telehealth platforms and mobile health applications allows clinicians to monitor patients remotely, improving efficiency and early detection of health deterioration. Government support for digital health infrastructure and initiatives promoting home healthcare further boost market growth

Europe Vital Signs Monitoring Market Share

The Europe Vital Signs Monitoring industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- GE HealthCare (U.S.)

- NIHON KOHDEN Corporation (Japan)

- OMRON Healthcare Co., Ltd. (Japan)

- Masimo Corporation (U.S.)

- Nonin Medical Inc. (U.S.)

- Contec Medical Systems Co., Ltd. (China)

- A&D Company, Limited (Japan)

- SunTech Medical, Inc. (U.S.)

- Smiths Group plc (U.K.)

- Schiller AG (Switzerland)

- Drägerwerk AG & Co. KGaA (Germany)

- Radiometer (Denmark)

- Spacelabs Healthcare (U.S.)

- Abbott (U.S.)

- Baxter (U.S.)

- Mindray Medical International Ltd. (China)

- Siemens Healthineers AG (Germany)

- ICU Medical, Inc. (U.S.)

What are the Recent Developments in Europe Vital Signs Monitoring Market?

- In September 2025, Royal Philips and Masimo announced an expanded innovation partnership aimed at advancing next‑generation patient monitoring technologies across Europe through integrated monitoring platforms and wearable solutions, enhancing interoperability and clinician support

- In May 2025, the European Commission approved the market authorization for the Finnish Oura Ring a smart health wearable that monitors key vital signs such as body temperature, heart rate variability, and sleep stages, marking the first CE‑certified wearable of its kind in the EU and broadening the vital signs monitoring landscape beyond traditional clinical devices

- In May 2025, Medtronic expanded its acute care and monitoring portfolio in Europe by entering a distribution agreement with Corsano Health to bring Corsano’s advanced multi‑sensor wearable vital signs monitoring solution capable of measuring heart rate, breathing rate, SpO₂, cuffless blood pressure, and ECG to hospitals and hospital‑at‑home care settings across Western Europe

- In April 2025, Masimo Corporation raised USD 200 million in a major funding round led by Sequoia Capital to bolster the development and global expansion of its non‑invasive vital signs monitoring technologies, highlighting increased investment interest and innovation momentum in Europe and globally

- In May 2024, Philips rolled out its wearable ePatch and AI analytics platform across 14 Spanish hospitals to monitor heart patients, enabling extended ambulatory cardiac monitoring and faster arrhythmia detection, reducing emergency room pressure and length of stay

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.