Global Abdominal Aortic Aneurysm Market

Market Size in USD Billion

CAGR :

%

USD

4.74 Billion

USD

9.38 Billion

2024

2032

USD

4.74 Billion

USD

9.38 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.74 Billion | |

| USD 9.38 Billion | |

| % | |

|

Abdominal Aortic Aneurysm Market Size

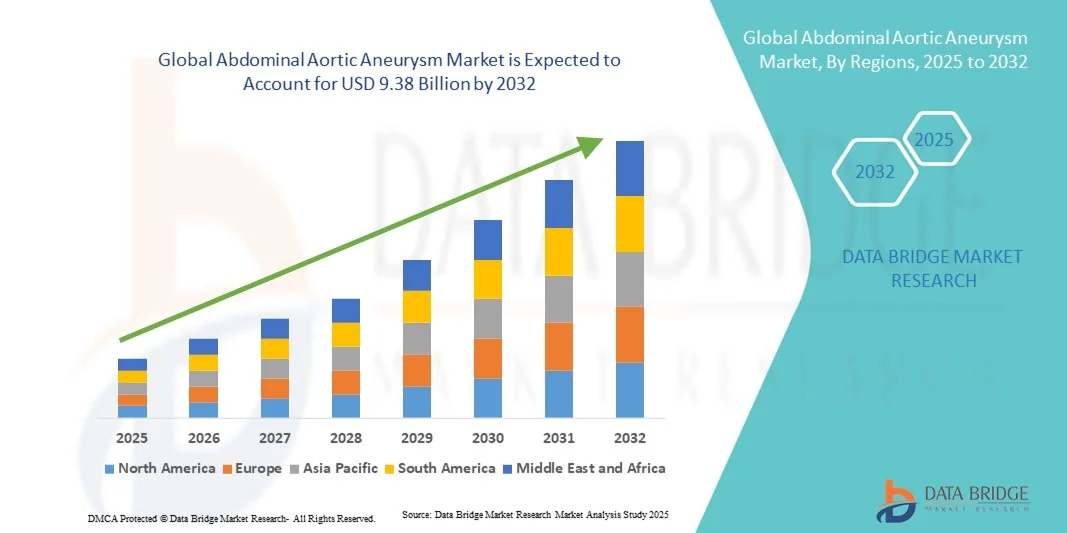

- The global abdominal aortic aneurysm market size was valued at USD 4.74 billion in 2024 and is expected to reach USD 9.38 billion by 2032, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of AAA, advancements in diagnostic and treatment technologies, and a growing aging population, leading to greater demand for minimally invasive and surgical interventions

- Furthermore, rising awareness about abdominal aortic aneurysm, coupled with improved healthcare infrastructure and early detection programs, is establishing advanced abdominal aortic aneurysm repair and monitoring solutions as the preferred choice for healthcare providers. These converging factors are accelerating the adoption of AAA treatment options, thereby significantly boosting the industry's growth

Abdominal Aortic Aneurysm Market Analysis

- Abdominal aortic aneurysms (AAA) are characterized by the abnormal dilation of the abdominal aorta, posing serious health risks. The global Abdominal Aortic Aneurysms market includes diagnostic and treatment solutions, with a growing emphasis on minimally invasive procedures and advanced surgical devices for effective patient management

- The escalating demand for abdominal aortic aneurysms treatments is primarily fueled by the increasing prevalence of abdominal aortic aneurysms, the rising geriatric population, advancements in surgical techniques, and greater awareness about early detection and intervention

- North America dominated the abdominal aortic aneurysms market with the largest revenue share of 40.06% in 2024, driven by advanced healthcare infrastructure, high adoption of endovascular repair procedures, and the presence of key market players focused on innovative treatment solutions

- Asia-Pacific is expected to be the fastest-growing region in the abdominal aortic aneurysms market during the forecast period, due to increasing healthcare investments, a growing aging population, and rising adoption of advanced medical technologies

- Endovascular Repair segment dominated the abdominal aortic aneurysms market in 2024 with a market share of 62.5% driven by its minimally invasive nature, reduced post-operative complications, shorter hospital stays, faster recovery times, and lower overall risk compared to open abdominal surgery

Report Scope and Abdominal Aortic Aneurysm Market Segmentation

|

Attributes |

Abdominal Aortic Aneurysm Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Abdominal Aortic Aneurysm Market Trends

Minimally Invasive and Image-Guided Intervention

- A significant and accelerating trend in the global abdominal aortic aneurysms market is the increasing adoption of minimally invasive procedures such as Endovascular Aneurysm Repair (EVAR) combined with image-guided navigation, which enhances procedural precision and patient safety

- For instance, the Medtronic Endurant II Stent Graft System allows physicians to perform EVAR with real-time imaging guidance, improving procedural accuracy and reducing recovery time.

- Image-guided interventions enable tailored treatment planning based on patient-specific anatomy and aneurysm morphology, improving outcomes and reducing perioperative complications.

- The integration of advanced imaging modalities such as 3D CT angiography and intraoperative fluoroscopy with EVAR devices allows surgeons to visualize vascular structures and deploy stent grafts with greater precision. Increased use of hybrid operating rooms combining imaging and surgical capabilities is enhancing the efficiency and safety of AAA procedures globally

- Innovations in robotic-assisted vascular surgery are emerging, allowing for higher precision in stent graft deployment and reduced human error during procedures. This trend towards minimally invasive, image-driven AAA repair is reshaping clinical practice and patient expectations, driving the development of more sophisticated stent grafts and procedural devices

- The demand for advanced, image-guided, and minimally invasive AAA interventions is rising globally, as clinicians seek safer, faster, and more effective treatment options for high-risk patients

Abdominal Aortic Aneurysm Market Dynamics

Driver

Increasing Prevalence of AAA and Aging Population

- The rising prevalence of abdominal aortic aneurysms, particularly among the aging population, is a key driver for the global abdominal aortic aneurysm market. For instance, the Society for Vascular Surgery reported a growing incidence of AAA among adults over 65, prompting higher demand for early detection and intervention

- Increasing awareness of cardiovascular health and abdominal aortic aneurysm screening programs is encouraging timely diagnosis and intervention, boosting treatment adoption rates

- Technological advancements in minimally invasive repair techniques and stent graft systems are making abdominal aortic aneurysm treatment more accessible and safer, driving market growth

- The rising incidence of comorbidities such as hypertension and atherosclerosis in elderly populations further emphasizes the need for timely AAA management, fueling market expansion

- Government initiatives and insurance reimbursement policies promoting early AAA screening and treatment are expanding patient access and stimulating market demand

- Growing collaboration between device manufacturers and healthcare providers to develop innovative AAA solutions is fostering adoption of advanced therapies and boosting market growth

Restraint/Challenge

High Procedure Costs and Limited Access in Emerging Regions

- The high cost of abdominal aortic aneurysm repair procedures, including EVAR and associated devices, poses a significant challenge to market growth in price-sensitive regions

- For instance, in some developing countries, limited reimbursement policies and high procedural expenses restrict patient access to advanced AAA treatments

- Unequal healthcare infrastructure and a shortage of trained vascular surgeons in certain regions hinder widespread adoption of minimally invasive AAA interventions

- While technological advancements improve outcomes, high device costs such as stent grafts and imaging systems limit affordability and adoption in low-resource settings

- Complex regulatory approval processes for medical devices in multiple regions can delay product launches and restrict market expansion

- Limited awareness among patients in rural and underserved areas about AAA risks and treatment options slows adoption of advanced procedures

- Addressing these challenges through cost-effective device development, expanded screening programs, and healthcare infrastructure improvements is crucial for sustained growth of the AAA market

Abdominal Aortic Aneurysm Market Scope

The market is segmented on the basis of treatment, product, site, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the abdominal aortic aneurysms market is segmented into open abdominal surgery and endovascular repair (EVAR). The Endovascular Repair segment dominated the market with the largest revenue share of 62.5% in 2024, driven by its minimally invasive nature, shorter hospital stays, and lower post-operative complications compared to open surgery. Patients and physicians prefer EVAR for its reduced recovery time and lower perioperative risk, especially among high-risk and elderly populations. Hospitals increasingly adopt EVAR due to efficiency gains and cost savings associated with shorter ICU stays. Technological advancements in stent graft systems and imaging guidance further enhance procedural accuracy, making EVAR the treatment of choice in many developed regions. The segment also benefits from increasing patient awareness and physician preference for advanced, less invasive treatments. Rising investments in hybrid operating rooms further consolidate the dominance of EVAR procedures.

Open Abdominal Surgery is expected to witness the fastest growth rate of 7.8% CAGR from 2025 to 2032, mainly in emerging markets where advanced EVAR devices may be less accessible. Open surgery remains critical for complex aneurysms unsuitable for EVAR, and growing surgical expertise in hospitals is expanding its adoption. Increased training programs and awareness campaigns in developing regions are supporting broader utilization of open surgical interventions. Open surgery also continues to be preferred for pararenal and thoracoabdominal aneurysms where minimally invasive options are limited. The segment benefits from established procedural protocols and physician experience. Rising demand in regions with limited EVAR infrastructure will continue to drive growth.

- By Product

On the basis of product, the market is segmented into stent graft, synthetic stent graft, catheter, guidewire, vascular closure devices, balloon inflation devices, and others. The Stent Graft segment dominated the market with the largest share of 45% in 2024, owing to its crucial role in EVAR procedures. Stent grafts are widely preferred for their minimally invasive deployment, reliability in excluding aneurysm sacs, and compatibility with imaging technologies for precise placement. Manufacturers are continuously innovating stent graft designs to improve flexibility, radial strength, and anatomical adaptability. The segment is supported by increasing awareness among clinicians and patients about the advantages of stent graft interventions. Ongoing R&D and regulatory approvals in major markets further drive demand. Growing adoption of next-generation stent grafts with fenestrated or branched designs is expanding the procedural applicability for complex aneurysms.

Synthetic Stent Grafts are anticipated to witness the fastest growth from 2025 to 2032, fueled by advances in biomaterials that reduce thrombosis risk, enhance durability, and offer better long-term outcomes. Rising adoption in both developed and emerging markets, along with physician preference for newer generation grafts, contributes to their accelerated growth. Improved material properties, such as enhanced biocompatibility, reduce complications and reinterventions. Increasing regulatory approvals and clinician training programs further support the segment’s expansion.

- By Site

On the basis of aneurysm site, the market is segmented into Infrarenal AAA and Pararenal AAA. The Infrarenal AAA segment dominated the market with a revenue share of 70% in 2024, as it is the most common type of AAA and is easier to treat using EVAR or open surgical procedures. Infrarenal aneurysms are often detected through routine imaging, allowing timely intervention and better clinical outcomes. Standardized stent grafts and procedural guidelines make treatment more predictable and widely available in major healthcare centers. Physician familiarity and favorable post-procedural results further reinforce dominance. Availability of less complex procedural techniques for infrarenal AAA also supports high adoption. Health insurance and reimbursement policies in developed regions favor infrarenal repair, boosting market revenue.

Pararenal AAA is expected to witness the fastest growth from 2025 to 2032 due to technological advancements in fenestrated and branched stent grafts, allowing minimally invasive repair of complex anatomies. Increasing detection of pararenal aneurysms through advanced imaging and rising surgeon expertise support rapid adoption globally. Growing awareness among physicians and patients about early intervention benefits further fuels adoption. New training programs for complex EVAR procedures increase procedural confidence. Expansion in emerging markets also contributes to segment growth.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, ambulatory surgical centers, and others. The Hospitals segment dominated the market with a revenue share of 65% in 2024, driven by the availability of advanced infrastructure, trained vascular surgeons, and access to high-end imaging and stent graft devices. Hospitals can perform both EVAR and open abdominal surgeries, making them the preferred treatment centers for AAA patients. Growing hospital investments in hybrid operating rooms further support the dominance of this segment. Hospitals also benefit from reimbursement coverage and centralized patient care, which improves treatment adoption. Access to advanced devices and multidisciplinary care teams reinforces hospital dominance. Hospitals are also centers for clinical trials and R&D collaborations, enhancing technology adoption.

Ambulatory Surgical Centers are expected to witness the fastest growth from 2025 to 2032 due to rising preference for outpatient EVAR procedures, shorter stays, and cost-effectiveness. Expansion of these centers in developed and emerging markets is enhancing access to minimally invasive AAA interventions. Increasing patient preference for outpatient care drives growth. Improved procedural safety allows more AAA interventions in ASC settings. Favorable insurance policies supporting outpatient treatment further stimulate adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. The Direct Tender segment dominated the market with a share of 52% in 2024, as hospitals and large healthcare providers prefer direct procurement from manufacturers for stent grafts, catheters, and other high-value devices. Direct tenders ensure timely supply, bulk purchase benefits, and adherence to strict quality standards required for surgical interventions. Established relationships between manufacturers and healthcare providers facilitate strategic contracts and long-term partnerships. Direct procurement also reduces supply chain risks and ensures availability of critical devices for high-volume hospitals. Large-scale tenders help negotiate pricing advantages, supporting market dominance. High reliability and traceability of direct supply chains drive institutional preference.

Online Pharmacy and E-commerce channels are expected to witness the fastest growth from 2025 to 2032 , driven by increasing digitalization of medical device distribution, easier access to consumables such as catheters and guidewires, and growing adoption of telemedicine-supported post-operative care solutions. Expansion of online distribution platforms is improving access in remote and underserved regions. Digital channels also provide real-time tracking, inventory management, and faster delivery. Ease of ordering and subscription-based procurement models enhance convenience. Integration with hospital supply systems further boosts adoption.

Abdominal Aortic Aneurysm Market Regional Analysis

- North America dominated the abdominal aortic aneurysms market with the largest revenue share of 40.06% in 2024, driven by advanced healthcare infrastructure, high adoption of endovascular repair procedures, and the presence of key market players focused on innovative treatment solutions

- Patients and healthcare providers in the region highly value the availability of minimally invasive EVAR procedures, advanced imaging technologies, and specialized vascular surgery expertise, which improve patient outcomes and reduce recovery times

- This widespread adoption is further supported by high healthcare expenditure, robust insurance coverage, and growing awareness of abdominal aortic aneurysms screening and treatment options, establishing North America as the leading market for abdominal aortic aneurysm interventions in both hospital and outpatient settings

U.S. Abdominal Aortic Aneurysm Market Insight

The U.S. abdominal aortic aneurysms market captured the largest revenue share of 81% in 2024 within North America, fueled by the widespread availability of advanced EVAR devices and high adoption of minimally invasive procedures. Patients increasingly prioritize early detection and intervention through regular screening programs. The growing prevalence of AAA among the aging population, combined with robust healthcare infrastructure and reimbursement support, further propels the market. Moreover, the increasing integration of advanced imaging technologies and hybrid operating rooms is significantly contributing to the market’s expansion. Strong presence of key device manufacturers and ongoing clinical research also support growth.

Europe Abdominal Aortic Aneurysms Market Insight

The Europe abdominal aortic aneurysms market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent cardiovascular healthcare regulations and rising awareness about AAA screening and treatment. The increase in urbanization, coupled with rising adoption of minimally invasive surgical procedures, is fostering the market. European healthcare providers and patients are also drawn to EVAR for its safety and reduced recovery time. The region is experiencing significant growth across hospitals, outpatient centers, and surgical facilities, with AAA interventions being incorporated into both new treatment protocols and updated clinical guidelines.

U.K. Abdominal Aortic Aneurysms Market Insight

The U.K. abdominal aortic aneurysms market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of aneurysm-related risks and a growing focus on minimally invasive treatment options. In addition, the rising aging population and prevalence of cardiovascular conditions are encouraging timely AAA management. The U.K.’s well-developed healthcare infrastructure and adoption of advanced endovascular repair devices are expected to continue stimulating market growth. Insurance coverage for AAA screening and interventions further supports adoption.

Germany Abdominal Aortic Aneurysms Market Insight

The Germany abdominal aortic aneurysms market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cardiovascular health and demand for technologically advanced interventions. Germany’s well-developed healthcare system, combined with high physician expertise and hospital infrastructure, promotes the adoption of both EVAR and open abdominal surgery procedures. Integration of advanced imaging modalities and hybrid surgical rooms is becoming increasingly prevalent, with strong patient preference for less invasive, safe, and efficient treatment options. Regulatory support for advanced devices also encourages market adoption.

Asia-Pacific Abdominal Aortic Aneurysms Market Insight

The Asia-Pacific abdominal aortic aneurysms market is poised to grow at the fastest CAGR of 24% during 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's growing inclination toward minimally invasive interventions, supported by government healthcare initiatives, is driving adoption of EVAR and stent grafts. Furthermore, expansion of trained vascular specialists and advanced imaging facilities is improving accessibility. Increasing awareness of AAA screening and early intervention, along with affordability of devices in select markets, is also contributing to growth.

Japan Abdominal Aortic Aneurysms Market Insight

The Japan abdominal aortic aneurysms market is gaining momentum due to the country’s high healthcare standards, aging population, and demand for minimally invasive procedures. The Japanese market places a significant emphasis on patient safety and clinical outcomes, and the adoption of EVAR and stent graft interventions is driven by advanced hospital infrastructure. Integration of imaging technologies with treatment procedures is fueling growth. Moreover, Japan's aging population is such asly to spur demand for safer, quicker, and less invasive AAA treatment options in both hospitals and outpatient centers.

India Abdominal Aortic Aneurysms Market Insight

The India abdominal aortic aneurysms market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding aging population, rapid urbanization, and increasing awareness about AAA management. India is witnessing rising adoption of minimally invasive EVAR procedures and stent graft technologies in hospitals and specialty surgical centers. Government healthcare initiatives, expanding insurance coverage, and increasing availability of affordable devices are key factors propelling market growth. The presence of domestic manufacturers and growing access to advanced imaging further support market expansion.

Abdominal Aortic Aneurysm Market Share

The Abdominal Aortic Aneurysm industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Cook (U.S.)

- MicroPort Scientific Corporation (China)

- W. L. Gore & Associates, Inc. (U.S.)

- Terumo Corporation (Japan)

- Endologix LLC (U.S.)

- Cardinal Health, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Cardiatis S.A. (Belgium)

- JOTEC GmbH (Germany)

- Lombard Medical, Inc. (U.S.)

- LifeTech Scientific Corporation (China)

- Getinge AB (Sweden)

- Arsenal Medical (U.S.)

- Artivion, Inc. (U.S.)

- Endospan Ltd. (Israel)

- Bentley InnoMed GmbH (Germany)

- Taurus Vascular (Netherlands)

- InspireMD Inc. (Israel)

What are the Recent Developments in Global Abdominal Aortic Aneurysm Market?

- In October 2025, Shape Memory Medical Inc. announced that it had reached 50% enrollment in its ongoing AAA-SHAPE Pivotal Trial (NCT06029660). The trial evaluates the IMPEDE-FX RapidFill device for managing abdominal aortic aneurysm (AAA) sac during endovascular aneurysm repair (EVAR). This pivotal study aims to assess the device's effectiveness in preventing aneurysm sac expansion and reducing the need for reintervention

- In September 2025, Bentley InnoMed GmbH announced that the U.S. Food and Drug Administration (FDA) granted Breakthrough Device designation to its BeFlared fenestrated endovascular aneurysm repair (FEVAR) bridging stent graft system. This designation aims to expedite the development and review of devices that offer significant advantages over existing treatments. The BeFlared device is designed to simplify the deployment process in complex aortic aneurysm repairs

- In April 2025, Penn State Health Milton S. Hershey Medical Center became the first hospital in central Pennsylvania to perform a groundbreaking, minimally invasive surgery for complex aortic aneurysms. The procedure involved the use of a custom-made stent graft with branches to fit around the aneurysm, allowing blood to flow through the graft and bypass the aneurysm, effectively neutralizing it. This approach avoids open surgery, shortens recovery time, and expands options for high-risk patients

- In January 2024, Nectero Medical announced the initiation of a Phase II/III clinical trial for its Nectero EAST® System, aimed at treating small- to medium-sized abdominal aortic aneurysms. The randomized trial seeks to evaluate the safety and efficacy of the EAST® System in patients with infrarenal AAA. This study represents a significant step forward in developing less invasive treatment options for AAA patients

- In December 2022, Endologix announced that it had received FDA approval for a premarket approval (PMA) supplement for its AFX2 Endovascular AAA System. The AFX2 system integrates anatomical fixation with an advanced delivery system, facilitating the treatment of patients with abdominal aortic aneurysms. This approval marks a significant advancement in endovascular repair technology, offering physicians a new option for treating AAA patients

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.