Global Achondroplasia Market

Market Size in USD Billion

CAGR :

%

USD

68.73 Billion

USD

828.33 Billion

2025

2033

USD

68.73 Billion

USD

828.33 Billion

2025

2033

| 2026 –2033 | |

| USD 68.73 Billion | |

| USD 828.33 Billion | |

| % | |

|

Achondroplasia Market Size

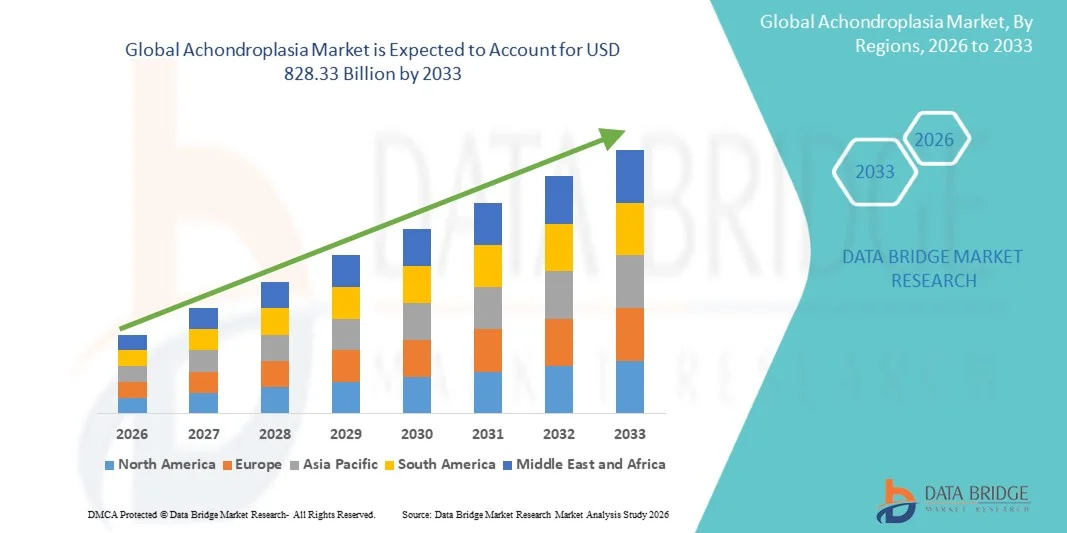

- The global achondroplasia market size was valued at USD 68.73 billion in 2025 and is expected to reach USD 828.33 billion by 2033, at a CAGR of 36.50% during the forecast period

- The market growth is largely fueled by the increasing awareness of rare genetic disorders, advancements in molecular diagnostics, and the growing adoption of targeted biologics and growth-modulating therapies, leading to improved disease management and patient outcomes in both pediatric and specialty healthcare settings

- Furthermore, rising demand for effective disease-modifying treatments, expanding research in gene therapy and monoclonal antibodies, and increasing healthcare support for rare disease management are establishing Achondroplasia solutions as an important focus area in modern therapeutic development. These converging factors are accelerating the uptake of Achondroplasia solutions, thereby significantly boosting the industry's growth

Achondroplasia Market Analysis

- Achondroplasia treatment solutions, including growth hormone–related therapies, C-type natriuretic peptide (CNP) analogs, genetic therapies, and supportive orthopedic and symptomatic management, are increasingly vital components of rare disease care due to their role in improving growth outcomes, managing skeletal abnormalities, and enhancing quality of life in pediatric and adult patients

- The escalating demand for Achondroplasia treatments is primarily fueled by growing awareness of rare genetic disorders, increasing diagnosis rates through advanced genetic screening, and rising adoption of targeted biologics and novel disease-modifying therapies aimed at addressing the underlying FGFR3 mutation

- North America dominated the achondroplasia market with the largest revenue share of approximately 43.6% in 2025, characterized by strong rare disease research funding, early regulatory approvals for novel therapies, advanced healthcare infrastructure, and the presence of leading biotechnology companies, with the U.S. accounting for significant uptake of newly approved targeted treatments

- Asia-Pacific is expected to be the fastest growing region in the achondroplasia market during the forecast period due to improving genetic testing capabilities, rising healthcare expenditure, increasing awareness of rare diseases, and expanding access to specialized treatment centers across China, India, Japan, and South Korea

- The parenteral segment held the largest market revenue share of 68.3% in 2025, driven by the widespread use of injectable growth hormone therapies used in pediatric treatment protocols

Report Scope and Achondroplasia Market Segmentation

|

Attributes |

Achondroplasia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Achondroplasia Market Trends

“Enhanced Therapeutic Advancements Through Gene-Targeted Therapies and Precision Medicine”

- A significant and accelerating trend in the global Achondroplasia market is the growing focus on gene-targeted therapies, molecular pathway modulation, and precision medicine approaches aimed at addressing the underlying FGFR3 gene mutation responsible for the condition. These advancements are improving disease management beyond symptomatic care

- Targeted therapies that regulate abnormal FGFR3 signaling are increasingly being developed to promote more normal bone growth in pediatric patients

- For instance, vosoritide (a C-type natriuretic peptide analog) has shown clinical efficacy in improving growth velocity in children with achondroplasia by counteracting overactive FGFR3 signaling pathways

- The expansion of clinical research in gene therapy and RNA-based interventions is also gaining momentum, with pharmaceutical companies exploring long-term disease-modifying solutions rather than supportive treatments alone

- Another important trend is the increasing use of early genetic screening and newborn diagnostic programs, which enable earlier intervention and improved growth outcomes through timely initiation of therapy

- In addition, patient registries and real-world evidence databases are being developed globally to better understand disease progression, treatment response, and long-term safety outcomes in achondroplasia patients

- This shift toward targeted, disease-modifying, and genetically informed therapies is fundamentally reshaping expectations in rare skeletal disorder management

Achondroplasia Market Dynamics

Driver

“Rising Awareness, Early Diagnosis, and Expanding Rare Disease Research Initiatives”

- The increasing awareness of rare genetic disorders and improved diagnostic capabilities is a major driver for the Achondroplasia market, leading to earlier detection and more timely therapeutic intervention in affected children

- Growing government and institutional support for rare disease research is further accelerating market expansion

- For instance, programs in the U.S., Europe, and Japan are actively funding orphan drug development and encouraging clinical trials focused on skeletal dysplasia disorders

- Rising collaboration between biotechnology firms, academic institutions, and patient advocacy groups is also supporting faster development of novel treatment options

- Furthermore, improved access to pediatric endocrinology and genetic counseling services is enhancing disease identification and long-term management

- The increasing availability of orphan drug incentives, including fast-track approvals and market exclusivity, is encouraging pharmaceutical companies to invest in achondroplasia therapies

Restraint/Challenge

“High Treatment Costs, Limited Patient Population, and Long-Term Therapy Dependence”

- One of the major challenges restraining the Achondroplasia market is the high cost of novel targeted therapies, which can significantly limit access in low- and middle-income regions

- The relatively small patient population associated with this rare genetic disorder also restricts large-scale clinical trials and reduces overall market size, making therapy development economically challenging for manufacturers

- For instance, long-term use of specialized growth-modulating treatments such as vosoritide requires continuous administration during growth years, increasing cumulative treatment burden and cost for families and healthcare systems

- In addition, limited awareness in some regions may lead to delayed diagnosis, reducing the effectiveness of early therapeutic intervention

- Overcoming these barriers through improved reimbursement policies, expanded rare disease funding, and development of cost-effective long-term therapies will be essential for sustained market growth

Achondroplasia Market Scope

The market is segmented on the basis of treatment, route of administration, end-users, and distribution channel.

• By Treatment

On the basis of treatment, the Achondroplasia market is segmented into growth hormone therapy, surgery, supportive therapy, and others. The growth hormone therapy segment dominated the largest market revenue share of 41.8% in 2025, driven by its increasing clinical use to promote linear growth in children with achondroplasia. Recombinant human growth hormone therapies are widely prescribed to improve height outcomes and skeletal development when initiated early in pediatric patients. Rising awareness among parents and pediatric endocrinologists regarding early intervention has significantly contributed to segment growth. Favorable reimbursement policies in developed regions further support adoption. Increasing diagnosis rates due to genetic screening and neonatal testing are expanding patient eligibility. Hospitals and specialty endocrine clinics are the primary centers for therapy initiation. Continuous clinical monitoring improves treatment adherence and outcomes. Pharmaceutical advancements in hormone formulations have enhanced efficacy and safety profiles. Growing focus on improving quality of life in affected children is also driving demand. Expanding healthcare access in emerging economies supports broader adoption. These factors collectively ensure dominance in 2025.

The supportive therapy segment is anticipated to witness the fastest growth rate of 10.6% from 2026 to 2033, driven by increasing demand for multidisciplinary management approaches. Supportive care includes physiotherapy, orthopedic support, psychological counseling, and nutritional management. These therapies play a crucial role in improving mobility, posture, and overall quality of life. Rising awareness of holistic care models is encouraging wider adoption. Parents and caregivers increasingly seek non-invasive long-term management solutions. Growing integration of rehabilitation services in pediatric care centers supports segment expansion. Schools and social support programs are also contributing to improved patient outcomes. Advancements in assistive devices and ergonomic support tools further strengthen demand. Increasing focus on developmental support during early childhood is accelerating uptake. Government and NGO-led awareness initiatives are expanding access in developing regions. These factors position supportive therapy as the fastest-growing segment.

• By Route of Administration

On the basis of route of administration, the Achondroplasia market is segmented into oral and parenteral. The parenteral segment held the largest market revenue share of 68.3% in 2025, driven by the widespread use of injectable growth hormone therapies used in pediatric treatment protocols. Parenteral administration ensures higher bioavailability and precise dosing, which is critical in long-term growth management. Most approved biologic therapies for achondroplasia are delivered via subcutaneous injections. Healthcare professionals prefer injectable routes for consistent therapeutic outcomes. Hospital and specialty clinic supervision further supports adherence and safety. Rising availability of user-friendly injection devices has improved patient compliance. Regular monitoring and dose adjustments are easier with parenteral therapies. Strong clinical guidelines recommend injectable treatment in eligible patients. Insurance coverage for biologics further supports adoption. Increasing use in early childhood treatment enhances long-term effectiveness. These factors collectively ensure segment dominance.

The oral segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by growing research into orally available therapeutic agents and small-molecule drugs. Oral formulations offer higher convenience and improved patient compliance compared to injections. Pharmaceutical companies are investing in novel oral compounds targeting bone growth pathways. Increasing preference for non-invasive treatment options is supporting future demand. Pediatric patients and caregivers favor oral dosing for ease of administration. Expanding clinical trials for oral modulators of FGFR3 signaling are encouraging innovation. Improved drug delivery technologies are enhancing bioavailability of oral agents. Rising homecare treatment trends also support adoption. Regulatory approvals of new oral therapies may further accelerate growth. Awareness of long-term treatment adherence benefits is increasing globally. These factors drive the fastest growth in the oral segment.

• By End-Users

On the basis of end-users, the Achondroplasia market is segmented into hospitals, homecare, speciality centres, and others. The hospitals segment accounted for the largest market revenue share of 52.9% in 2025, driven by their role as primary diagnostic and treatment centers for genetic and skeletal disorders. Hospitals provide multidisciplinary care involving pediatricians, endocrinologists, geneticists, and orthopedic specialists. Early diagnosis and initiation of growth hormone therapy are commonly conducted in hospital settings. Availability of advanced diagnostic imaging and genetic testing supports accurate assessment. Strong infrastructure for long-term monitoring enhances treatment effectiveness. Hospitals also manage complications such as spinal issues and orthopedic deformities. High patient inflow and referral-based care systems support segment leadership. Government-funded hospital programs improve access in many regions. Reimbursement frameworks favor hospital-based treatment initiation. Clinical trial activities are also concentrated in hospitals. These factors ensure strong dominance in 2025.

The speciality centres segment is anticipated to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by increasing demand for highly specialized genetic and endocrine care. These centres offer focused treatment pathways for rare skeletal disorders like achondroplasia. Availability of expert multidisciplinary teams improves treatment precision and outcomes. Rising awareness of rare disease management is increasing referrals to specialty centres. Advanced growth monitoring systems and personalized treatment plans support adoption. Families prefer specialized centres for better long-term developmental care. Expansion of rare disease networks is improving accessibility globally. Collaboration with research institutes enhances treatment innovation. Increasing investment in pediatric specialty infrastructure supports growth. Digital health integration improves patient follow-up and monitoring. These factors position speciality centres as the fastest-growing end-user segment.

• By Distribution Channel

On the basis of distribution channel, the Achondroplasia market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 55.6% in 2025, driven by centralized dispensing of injectable growth hormone therapies and specialty medications. Hospital pharmacies ensure controlled storage and accurate dosing of biologic treatments. Most initial prescriptions are filled directly within hospital settings. Integration with pediatric endocrinology departments improves medication adherence. Strong procurement systems support continuous drug availability. Monitoring of treatment response is often coordinated through hospital pharmacy services. Insurance reimbursement structures frequently favor institutional dispensing. High dependency on specialist prescriptions supports hospital pharmacy dominance. Government healthcare programs further strengthen access. Emergency and follow-up care coordination also contributes to demand. These factors collectively sustain leadership in 2025.

The online pharmacy segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by increasing digital healthcare adoption and convenience in medication access. Patients requiring long-term therapy prefer doorstep delivery services. Telemedicine integration is expanding prescription fulfillment through digital platforms. Growing smartphone penetration is increasing accessibility across regions. Subscription-based refill systems improve treatment adherence. Price transparency and discounts attract caregivers and patients. Rural and remote areas benefit from improved drug availability. Logistics improvements support safe delivery of temperature-sensitive medications. Rising awareness of e-pharmacy services is boosting adoption. Regulatory advancements are improving trust in online channels. These factors make online pharmacy the fastest-growing distribution channel.

Achondroplasia Market Regional Analysis

- North America dominated the achondroplasia market with the largest revenue share of approximately 43.6% in 2025, driven by strong rare disease research funding, advanced healthcare infrastructure, and early regulatory approvals for novel targeted therapies. The presence of leading biotechnology and rare disease-focused pharmaceutical companies significantly supports market expansion. Increasing diagnosis rates through improved genetic testing and newborn screening programs are enhancing early identification of patients

- Strong reimbursement frameworks and insurance coverage improve access to high-cost orphan drugs and biologic therapies. Rising awareness among physicians regarding growth disorders and genetic conditions further strengthens treatment adoption. Continuous clinical research in growth hormone pathways and FGFR3-targeted therapies is accelerating innovation

- Patient advocacy groups and government initiatives supporting rare disease management are also contributing to market growth. The U.S. Food and Drug Administration’s supportive orphan drug policies further encourage new product approvals. North America is expected to maintain its dominant position throughout the forecast period

U.S. Achondroplasia Market Insight

The U.S. achondroplasia market captured the largest revenue share in 2025 within North America, driven by significant uptake of newly approved targeted therapies and strong clinical research activity. The country has a well-established rare disease care ecosystem with specialized treatment centers and expert pediatric endocrinologists. Increasing adoption of precision medicine and FGFR3 inhibitor therapies is improving patient outcomes. Strong insurance coverage and reimbursement policies support access to expensive orphan drugs. Growing participation in clinical trials is accelerating drug development and innovation. Rising awareness among healthcare providers and parents is improving early diagnosis rates. Patient support programs and advocacy organizations are further strengthening treatment access. Continuous advancements in genetic testing technologies are enabling faster identification of cases. The U.S. remains the primary contributor to regional market growth.

Europe Achondroplasia Market Insight

The Europe achondroplasia market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of rare genetic disorders and strong healthcare support systems. Rising availability of genetic testing and improved diagnostic infrastructure are enhancing early detection rates across the region. Governments across Germany, France, the U.K., and Nordic countries are increasing funding for rare disease research and orphan drug development. Strong regulatory frameworks support the approval of innovative therapies for rare conditions. Growing collaboration between academic institutions and biotechnology companies is accelerating clinical advancements. Patient registries and rare disease networks are improving disease monitoring and treatment planning. Expanding access to specialized pediatric care centers is further supporting market growth. Increasing participation in global clinical trials enhances treatment availability. Europe continues to strengthen its rare disease management ecosystem.

U.K. Achondroplasia Market Insight

The U.K. achondroplasia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong NHS support for rare disease diagnosis and treatment. Increasing availability of genetic screening programs is improving early detection of achondroplasia cases. The country has a well-developed rare disease strategy that promotes research and treatment access. Rising adoption of novel biologic therapies is supporting improved patient outcomes. Strong collaboration between academic institutions and biotech firms is accelerating drug development. Patient advocacy groups are playing an important role in awareness and support. Expanding clinical trial participation is further strengthening innovation. Government funding for orphan diseases continues to enhance healthcare infrastructure. The U.K. remains a key contributor to the European rare disease market.

Germany Achondroplasia Market Insight

The Germany achondroplasia market is expected to expand at a considerable CAGR during the forecast period, supported by advanced healthcare infrastructure and strong research capabilities. Germany has a high level of expertise in genetic testing and pediatric rare disease management. Increasing use of molecular diagnostics is improving early identification of achondroplasia cases. Strong pharmaceutical R&D ecosystem supports development of novel targeted therapies. Government funding for rare disease programs enhances patient access to advanced treatments. Growing collaboration between hospitals and biotech companies is driving clinical innovation. Expansion of specialized treatment centers improves care delivery. Rising awareness among healthcare professionals supports early diagnosis and intervention. Germany remains one of the leading European markets for rare disease therapeutics.

Asia-Pacific Achondroplasia Market Insight

The Asia-Pacific achondroplasia market is poised to grow at the fastest CAGR due to improving genetic testing capabilities, rising healthcare expenditure, and increasing awareness of rare diseases. Expanding access to advanced diagnostic tools is enabling earlier detection of genetic disorders. Governments across China, India, Japan, and South Korea are increasing investments in rare disease research and treatment infrastructure. Growing availability of specialized treatment centers is improving patient access to care. Rising participation in global clinical trials is accelerating drug development in the region. Increasing healthcare insurance penetration is improving affordability of rare disease therapies. Expanding biotechnology sectors and domestic pharmaceutical manufacturing are supporting innovation. Awareness campaigns by patient organizations are improving disease recognition. Asia-Pacific is expected to remain the fastest growing regional market during the forecast period.

Japan Achondroplasia Market Insight

The Japan achondroplasia market is gaining momentum due to advanced healthcare infrastructure and strong focus on genetic research. High adoption of precision medicine and molecular diagnostics supports early detection of rare disorders. Increasing availability of pediatric endocrinology specialists is improving treatment outcomes. Government support for rare disease programs is strengthening healthcare delivery. Rising participation in clinical trials is accelerating access to innovative therapies. Strong pharmaceutical R&D capabilities further support market growth. Patient advocacy initiatives are increasing awareness and support systems. Japan’s aging and health-conscious population contributes to strong healthcare engagement. Continuous innovation in biotechnology is expected to support long-term market expansion.

China Achondroplasia Market Insight

The China achondroplasia market accounted for the largest market revenue share in Asia Pacific in 2025, driven by expanding healthcare infrastructure and growing awareness of genetic disorders. Increasing adoption of advanced genetic testing technologies is improving diagnosis rates. Government investments in rare disease management and healthcare modernization are supporting market growth. Rising participation in clinical trials and global drug development programs is enhancing treatment availability. Expansion of specialized pediatric hospitals is improving access to care. Increasing healthcare spending and insurance coverage are supporting affordability. Domestic biotechnology growth is accelerating innovation in rare disease therapeutics. Awareness campaigns are improving recognition of genetic conditions. China is expected to remain a key growth driver in the Asia-Pacific region.

Achondroplasia Market Share

The Achondroplasia industry is primarily led by well-established companies, including:

- BioMarin Pharmaceutical Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Ascendis Pharma A/S (Denmark)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- Amgen Inc. (U.S.)

- Ipsen S.A. (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Eli Lilly and Company (U.S.)

- Horizon Therapeutics plc (Ireland)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- BridgeBio Pharma, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Bristol Myers Squibb (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Kyowa Kirin Co., Ltd. (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Viatris Inc. (U.S.)

Latest Developments in Global Achondroplasia Market

- In August 2021, the European Commission approved VOXZOGO® (vosoritide), developed by BioMarin Pharmaceutical, for the treatment of achondroplasia in children with open growth plates. This marked the first disease-modifying therapy targeting the underlying FGFR3 pathway in achondroplasia, introducing a precision medicine approach for improving linear growth in affected children

- In November 2021, the U.S. Food and Drug Administration (FDA) approved VOXZOGO® (vosoritide) for pediatric patients aged 5 years and older with achondroplasia and open epiphyses. This approval established the first FDA-authorized pharmacological therapy for improving growth in the most common form of dwarfism, significantly transforming the treatment landscape

- In 2021 (clinical development milestone), BioMarin Pharmaceutical reported continued advancement of vosoritide (VOXZOGO) through global clinical adoption programs, with increasing use across multiple countries following its regulatory approvals. The therapy demonstrated improved annualized growth velocity and became the first widely adopted targeted treatment for achondroplasia, reinforcing FGFR3 inhibition as a validated therapeutic strategy

- In September 2024, BridgeBio Pharma reported positive Phase 3 PROPEL3 trial results for infigratinib, an oral FGFR inhibitor for achondroplasia. The therapy demonstrated approximately 2.1 cm/year improvement in growth rate versus placebo, positioning it as a potential best-in-class oral alternative to existing injectable therapies and intensifying competition in the growth disorder treatment market

- In November 2025, clinical pipeline analyses highlighted the expanding achondroplasia treatment landscape with emerging therapies such as infigratinib (oral FGFR inhibitor), TransCon CNP (Ascendis), and other investigational agents competing alongside VOXZOGO. The market evolution is increasingly driven by differentiation in convenience (oral vs injectable), efficacy improvements, and earlier treatment initiation in pediatric patients

- In February 2026 (late-stage 2025 development impact), BridgeBio announced that updated Phase 3 data for infigratinib showed statistically significant improvements in growth rate and body proportionality, outperforming existing injectable standards such as vosoritide in cross-trial comparisons. The results strengthened expectations that the therapy could become the first oral treatment for achondroplasia pending regulatory approval

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.