Global Active Protection System Market

Market Size in USD Billion

CAGR :

%

USD

4.95 Billion

USD

7.35 Billion

2025

2033

USD

4.95 Billion

USD

7.35 Billion

2025

2033

| 2026 –2033 | |

| USD 4.95 Billion | |

| USD 7.35 Billion | |

| % | |

|

Active Protection System Market Size

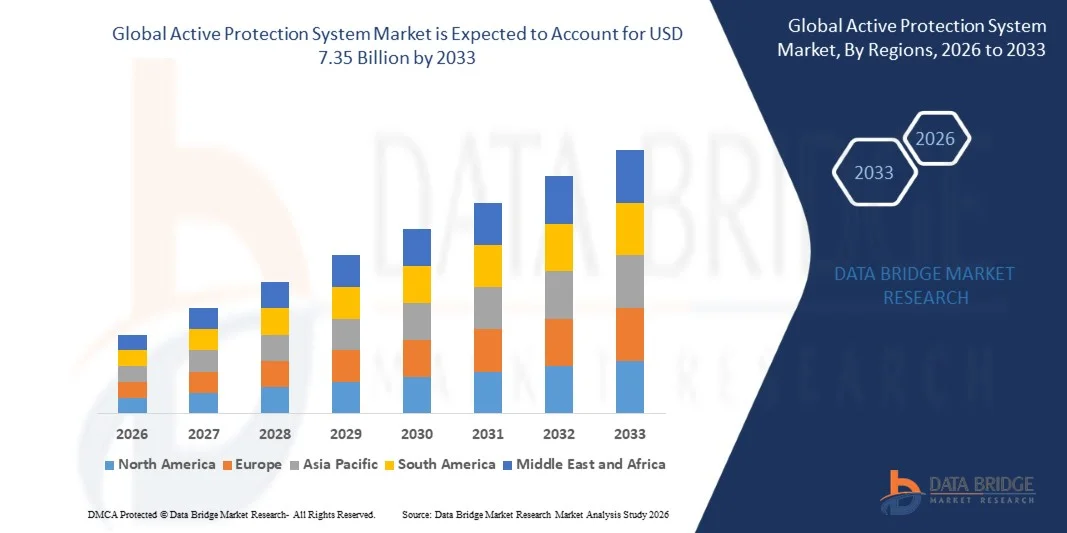

- The global active protection system market size was valued at USD 4.95 billion in 2025 and is expected to reach USD 7.35 billion by 2033, at a CAGR of 5.05% during the forecast period

- The market growth is largely fuelled by rising defense modernization programs, increasing demand for armored vehicles with advanced threat mitigation capabilities, and the growing need to protect military assets from guided missiles and RPG attacks

- Adoption of advanced sensor technologies, radar-based threat detection systems, and integration with vehicle-mounted countermeasure systems is further driving market expansion

Active Protection System Market Analysis

- The market is witnessing continuous technological innovations, including laser-based interceptors, modular APS designs, and networked protection solutions for real-time threat response

- Key players are focusing on strategic partnerships, defense contracts, and R&D investments to enhance system accuracy, reduce response times, and expand adoption across both armored vehicles and critical military infrastructure

- North America dominated the active protection system (APS) market with the largest revenue share of 38.2% in 2025, driven by growing defense modernization programs, increased procurement of armored vehicles, and rising investments in advanced threat mitigation technologies

- Asia-Pacific region is expected to witness the highest growth rate in the global active protection system market, driven by expanding defense budgets, rapid modernization of armored fleets, increasing regional security concerns, and rising adoption of both hard-kill and soft-kill APS technologies across countries such as China, India, and Japan

- The Land-based segment held the largest market revenue share in 2025, driven by the widespread deployment of APS on tanks, armored personnel carriers, and mobile command vehicles. Land-based APS enhances vehicle survivability against guided missiles and RPG attacks, offering real-time threat detection and interception capabilities, which makes it a preferred choice for modern militaries

Report Scope and Active Protection System Market Segmentation

|

Attributes |

Active Protection System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Rheinmetall AG (Germany) • Artis, LLC (U.S.) |

|

Market Opportunities |

• Rising Adoption Of Advanced Sensor-Based Protection Systems |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Active Protection System Market Trends

“Rising Demand for Enhanced Vehicle Survivability and Threat Mitigation”

• The growing focus on armored vehicle safety and real-time threat neutralization is significantly shaping the active protection system (APS) market, as defense forces increasingly prefer systems that can detect, intercept, and neutralize incoming threats such as RPGs and anti-tank missiles. APS adoption is gaining traction due to its ability to enhance vehicle survivability without compromising mobility or operational readiness. This trend strengthens deployment across military ground vehicles, encouraging manufacturers to innovate with advanced sensors, interceptors, and modular solutions to meet evolving defense needs

• Increasing awareness around battlefield safety, force protection, and operational efficiency has accelerated the demand for active protection systems in armored vehicles, tanks, and mobile command units. Defense organizations globally are seeking systems that can integrate with existing platforms while providing rapid response to threats, prompting manufacturers to invest in R&D for high-accuracy sensors and countermeasure technologies

• Modern warfare and defense modernization trends are influencing procurement decisions, with military agencies emphasizing advanced radar detection, modular APS designs, and integration with vehicle systems. These factors are helping defense forces enhance survivability, build operational resilience, and strengthen strategic capabilities while driving adoption across global defense markets

• For instance, in 2025, Rheinmetall in Germany and Raytheon Technologies in the U.S. expanded their APS offerings for armored vehicles by integrating laser-based interceptors and networked threat detection systems. These deployments were introduced in response to increasing battlefield threats and modernization programs, with installations across both combat and support vehicles. The systems were also marketed as enabling higher mission success rates and reducing vehicle losses, enhancing defense operational efficiency

• While demand for APS is growing, sustained market expansion depends on continuous technological innovation, cost optimization, and maintaining rapid response capabilities under diverse battlefield conditions. Manufacturers are also focusing on improving modularity, interoperability, and developing next-generation solutions that balance accuracy, speed, and reliability for broader military adoption

Active Protection System Market Dynamics

Driver

“Growing Emphasis on Vehicle Survivability and Threat Response”

• Rising defense modernization programs and increasing investments in armored vehicles are major drivers for the active protection system market. Militaries are increasingly integrating APS to enhance battlefield survivability, protect high-value assets, and improve mission effectiveness

• Expanding applications in tanks, armored personnel carriers, and mobile command vehicles are influencing market growth. APS enhances real-time threat detection, interception capabilities, and situational awareness, enabling defense forces to meet modern combat and security requirements

• Defense organizations are actively promoting APS adoption through procurement contracts, modernization initiatives, and integration with advanced radar and countermeasure systems. These efforts are supported by geopolitical tensions and the growing need for operational efficiency, encouraging collaborations between defense contractors and system integrators

• For instance, in 2023, Lockheed Martin in the U.S. and MBDA in Europe reported increased incorporation of APS in main battle tanks and armored vehicles. This expansion followed rising demand for vehicle survivability against guided missiles and RPG threats, driving repeat contracts and system upgrades. Both companies also highlighted integration with radar-based sensors and interceptors to strengthen operational effectiveness

• Although rising defense modernization programs support growth, wider adoption depends on cost optimization, technology scalability, and integration capabilities. Investment in R&D, advanced sensor development, and efficient production processes will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Cost and Complex Integration Requirements”

• The relatively high cost of active protection systems compared to conventional defense solutions remains a key challenge, limiting adoption among budget-constrained defense forces. High R&D expenses, advanced sensor technology, and interceptor development contribute to elevated system pricing

• Integration complexities remain significant, particularly for retrofitting APS onto existing vehicles, which can require extensive vehicle modifications, software updates, and personnel training. These factors restrict adoption in older fleets or smaller defense budgets

• Supply chain and production challenges also impact market growth, as APS components require high-precision manufacturing and adherence to strict military standards. Logistical complexities and system testing requirements increase operational timelines and deployment costs

• For instance, in 2024, defense organizations in Southeast Asia reported slower uptake of APS due to high procurement costs, integration challenges, and limited technical expertise. Installation and calibration requirements for armored vehicles also delayed deployment, affecting operational readiness

• Overcoming these challenges will require cost-efficient production, modular designs, and enhanced integration support for defense clients. Collaboration with system integrators, defense contractors, and research institutions can help unlock the long-term growth potential of the global active protection system market. In addition, developing scalable, interoperable solutions and strengthening maintenance and support networks will be essential for widespread adoption

Active Protection System Market Scope

The market is segmented on the basis of platform, type, and end-user.

• By Platform

On the basis of platform, the active protection system (APS) market is segmented into Airborne, Land-based, and Naval. The Land-based segment held the largest market revenue share in 2025, driven by the widespread deployment of APS on tanks, armored personnel carriers, and mobile command vehicles. Land-based APS enhances vehicle survivability against guided missiles and RPG attacks, offering real-time threat detection and interception capabilities, which makes it a preferred choice for modern militaries.

The Airborne segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by the increasing need for threat mitigation systems on helicopters and unmanned aerial vehicles (UAVs). Airborne APS provides protection against missiles and ground-based threats while maintaining operational mobility and speed. Its adoption is rising due to advancements in lightweight interceptors, radar sensors, and integration with aircraft avionics systems.

• By Type

On the basis of type, the market is segmented into Hard Kill System and Soft Kill System. The Hard Kill System segment held the largest revenue share in 2025 due to its ability to physically intercept and neutralize incoming projectiles, ensuring high protection levels for armored vehicles. These systems are increasingly adopted in main battle tanks and combat vehicles to enhance battlefield survivability.

The Soft Kill System segment is expected to witness the fastest growth from 2026 to 2033, driven by rising demand for electronic countermeasures, jamming technologies, and decoy-based solutions. Soft kill APS is particularly preferred for stealth operations and scenarios where non-kinetic threat mitigation is required, offering cost-effective and scalable protection options.

• By End-User

On the basis of end-user, the market is segmented into Defence and Homeland Security. The Defence segment held the largest market share in 2025, fueled by extensive modernization programs, rising geopolitical tensions, and increased investments in armored vehicle fleets across global military forces. Defence organizations prioritize APS to protect critical assets and personnel in high-threat environments.

The Homeland Security segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising security concerns, border protection requirements, and increasing adoption of APS on mobile security platforms. The growing need to safeguard critical infrastructure, government facilities, and strategic transport units is boosting APS deployment among homeland security agencies worldwide.

Active Protection System Market Regional Analysis

• North America dominated the active protection system (APS) market with the largest revenue share of 38.2% in 2025, driven by growing defense modernization programs, increased procurement of armored vehicles, and rising investments in advanced threat mitigation technologies

• Defense organizations in the region highly value real-time threat detection, rapid interception capabilities, and integration with existing vehicle systems, enhancing survivability and operational efficiency

• This widespread adoption is further supported by high defense budgets, advanced military infrastructure, and increasing geopolitical tensions, establishing APS as a critical solution for protecting personnel and high-value assets

U.S. Active Protection System Market Insight

The U.S. APS market captured the largest revenue share in North America in 2025, fueled by extensive armored vehicle fleets and ongoing defense modernization programs. The increasing emphasis on survivability against guided missiles and RPG attacks is driving adoption across main battle tanks, armored personnel carriers, and mobile command units. The U.S. military’s focus on integrating advanced radar sensors, hard-kill and soft-kill systems, and networked countermeasures further propels the market. Moreover, ongoing R&D and defense contracts support continuous innovation, strengthening the U.S. APS market.

Europe Active Protection System Market Insight

The Europe APS market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing defense spending, modernization of armored fleets, and stringent military safety requirements. European militaries are emphasizing vehicle survivability, modular APS solutions, and integration with advanced sensor and radar technologies. Rising geopolitical tensions and investments in autonomous and connected platforms are fostering adoption. Countries across the region are equipping tanks and combat vehicles with APS to enhance mission effectiveness and operational readiness.

U.K. Active Protection System Market Insight

The U.K. APS market is expected to witness strong growth from 2026 to 2033, driven by the modernization of armored units and the need for advanced threat mitigation capabilities. Heightened security concerns and the desire to protect military personnel and assets are prompting adoption of both hard-kill and soft-kill systems. The country’s robust defense infrastructure, emphasis on R&D, and collaboration with global defense contractors are expected to sustain market expansion.

Germany Active Protection System Market Insight

The Germany APS market is expected to witness significant growth from 2026 to 2033, fueled by rising awareness of digital defense technologies and demand for technologically advanced, eco-conscious solutions. Germany’s well-developed defense industry, focus on innovation, and investment in armored vehicle upgrades promote APS adoption. Integration with vehicle-mounted sensors and automated threat response systems is increasingly prevalent, with a strong preference for high-precision, reliable protection solutions aligning with national defense priorities.

Asia-Pacific Active Protection System Market Insight

The Asia-Pacific APS market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing defense modernization programs, rising military budgets, and procurement of armored and tactical vehicles in countries such as China, India, and Japan. The region’s focus on border security, force protection, and modernization of mobile defense platforms is boosting APS deployment. In addition, growing domestic defense manufacturing capabilities and local production of APS components are improving affordability and accessibility, enabling wider adoption across military forces.

Japan Active Protection System Market Insight

The Japan APS market is expected to witness strong growth from 2026 to 2033 due to the country’s emphasis on high-tech defense solutions, modernization of armored units, and enhanced focus on homeland and border security. Adoption is driven by integration with advanced sensor technologies, UAV threat monitoring, and vehicle-mounted interception systems. The country’s proactive approach toward upgrading main battle tanks and armored vehicles supports the APS market, particularly for protecting strategic and high-value assets.

China Active Protection System Market Insight

The China APS market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid modernization of its armored fleets, rising defense expenditure, and high adoption of advanced threat detection and mitigation systems. China is equipping main battle tanks, infantry fighting vehicles, and mobile defense units with both hard-kill and soft-kill APS to enhance survivability. The country’s focus on self-reliance in defense technologies, development of domestic APS manufacturers, and integration with modern combat platforms are key factors propelling market growth.

Active Protection System Market Share

The Active Protection System industry is primarily led by well-established companies, including:

• Rheinmetall AG (Germany)

• Saab AB (Sweden)

• Raytheon Company (U.S.)

• Israel Military Industries (Israel)

• Rafael Advanced Defense Systems Ltd. (Israel)

• Artis, LLC (U.S.)

• Airbus Group (Netherlands)

• KBM (Russia)

• Aselsan A.S. (Turkey)

• Safran (France)

• Lockheed Martin Corporation (U.S.)

• BAE Systems plc (U.K.)

• Northrop Grumman Corporation (U.S.)

• Thales Group (France)

• General Dynamics Corporation (U.S.)

Latest Developments in Global Active Protection System Market

- In November 2025, Rafael Advanced Defense Systems (Israel) announced a collaboration with a leading technology firm to develop next-generation electronic warfare and active protection systems. The initiative aims to enhance countermeasure capabilities against emerging threats, improve operational effectiveness, and strengthen the company’s position in the global defense market. This development is expected to drive innovation in integrated electronic warfare solutions and expand adoption across multiple defense platforms

- In October 2025, Northrop Grumman (U.S.) unveiled a new active protection system for armored vehicles, incorporating AI and machine learning technologies. This launch enhances survivability, accelerates threat response times, and reinforces the company’s leadership in advanced vehicle protection solutions. The system addresses the growing demand for intelligent defense measures and supports modernization programs in militaries worldwide

- In September 2025, Thales Group (France) secured a major contract with a European nation for the supply of advanced active protection systems. The deal strengthens Thales’ presence in the European defense market, boosts revenue, and reinforces its reputation as a trusted supplier of high-performance threat mitigation systems. The contract also demonstrates the rising importance of APS in modern armored vehicle fleets.

- In March 2025, Saab AB (Sweden), in partnership with Ukrainian defense firm Radionix, signed a Memorandum of Understanding to collaborate on sensors and defense electronics. The partnership aims to develop and maintain advanced sensor systems for enhanced threat detection and armored vehicle protection, improving Ukraine’s defense capabilities and supporting regional security initiatives

- In February 2025, HENSOLDT AG (Germany) secured a EUR 17.6 million (USD 18.4 million) contract from the German Federal Office of Bundeswehr Equipment, Information Technology, and In-Service Support (BAAINBw) to develop an optical detection system demonstrator, Odaeon. Utilizing Jammer Head 2 technology within its Multifunctional Self-Protection System (MUSS), the demonstrator is expected to improve situational awareness, threat detection, and countermeasure efficiency, reinforcing HENSOLDT’s technological leadership in vehicle protection systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.