Global Aerospace Valves Market

Market Size in USD Billion

USD

3.12 Billion

USD

4.75 Billion

2025

2033

USD

3.12 Billion

USD

4.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.12 Billion | |

| USD 4.75 Billion | |

| % | |

|

What is the Global Aerospace Valves Market Size and Growth Rate?

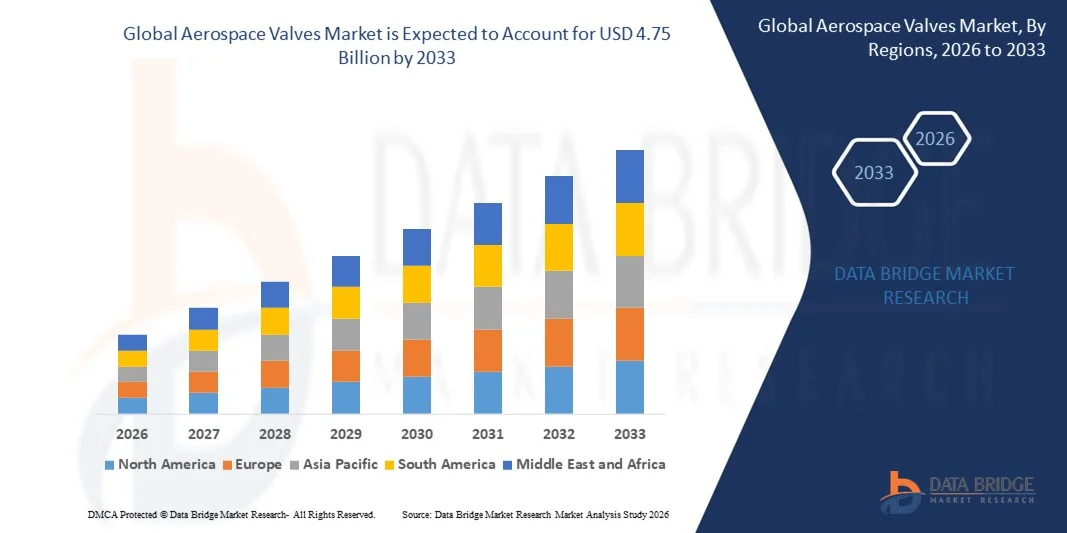

- The global aerospace valves market size was valued at USD 3.12 billion in 2025 and is expected to reach USD 4.75 billion by 2033, at a CAGR of5.40% during the forecast period

- Major factors that are expected to boost the growth of the aerospace valves market in the forecast period are the rise in the aircraft deliveries and the decrease in the replacement rotations of the aerospace valves

- Furthermore, the upsurge in the need for lightweight valves by most airlines and the increase in the passenger traffic are couple of factors that are propelling the growth of the aerospace valves market

What are the Major Takeaways of Aerospace Valves Market?

- The rise in the electrification of aircraft systems and the present backlogs regarding the aircraft deliveries are further anticipated to impede the growth of the aerospace valves market in the timeline period

- In addition, the initiation of lightweight valves will further provide potential opportunities for the growth of the aerospace valves market in the coming years. However, the advancing of the operational effectiveness of aerospace valves might further create obstructions for the growth of the aerospace valves market in the near future

- North America dominated the aerospace valves market with a 40.7% revenue share in 2025, driven by strong aircraft manufacturing presence, extensive defense spending, and continuous technological advancements across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 10.8% from 2026 to 2033, driven by rapid expansion of aircraft fleets, increasing defense budgets, and strong growth in domestic aircraft manufacturing across China, Japan, India, and South Korea

- The Aerospace Fuel System Valves segment dominated the market with a 29.8% share in 2025, driven by their critical role in regulating fuel flow, maintaining engine efficiency, and ensuring operational safety across commercial and military aircraft

Report Scope and Aerospace Valves Market Segmentation

|

Attributes |

Aerospace Valves Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Aerospace Valves Market?

Increasing Shift Toward Lightweight, Electrically Actuated, and Smart Aerospace Valves

- The aerospace valves market is witnessing strong adoption of lightweight, compact, and high-performance valve systems designed to support modern aircraft hydraulic, fuel, pneumatic, and environmental control systems

- Manufacturers are introducing electrically actuated and smart valves integrated with sensors and digital control units to enhance precision flow regulation, condition monitoring, and real-time performance diagnostics

- Growing demand for fuel-efficient aircraft, reduced emissions, and weight optimization is accelerating the replacement of traditional hydraulic systems with advanced electro-mechanical valve technologies

- For instance, companies such as Parker Hannifin, Honeywell International, Eaton, and Moog Inc. are expanding their aerospace valve portfolios with digitally controlled, lightweight, and high-durability solutions

- Increasing development of next-generation aircraft, UAVs, and electric propulsion platforms is driving the need for high-pressure, corrosion-resistant, and temperature-tolerant valve systems

- As aircraft architectures become more electric and digitally integrated, aerospace valves will remain critical for safe fluid control, system efficiency, and advanced flight operations

What are the Key Drivers of Aerospace Valves Market?

- Rising global aircraft production and fleet modernization programs are significantly increasing demand for advanced fuel control, hydraulic, and pneumatic valve systems

- For instance, in 2025, leading aerospace suppliers such as Crane Aerospace & Electronics and ITT Inc. expanded their high-performance valve offerings to support next-generation commercial and defense aircraft platforms

- Growing investments in military aviation, space exploration, and unmanned aerial systems are strengthening demand for high-reliability and precision-engineered valves

- Advancements in additive manufacturing, advanced alloys, and composite materials are improving durability, reducing weight, and enhancing resistance to extreme pressure and temperature conditions

- Increasing focus on aircraft safety standards, regulatory compliance, and predictive maintenance systems is driving integration of smart monitoring-enabled valve technologies

- Supported by sustained growth in global air travel, defense budgets, and aircraft electrification initiatives, the Aerospace Valves market is expected to witness steady long-term expansion

Which Factor is Challenging the Growth of the Aerospace Valves Market?

- High manufacturing and certification costs associated with aerospace-grade materials and stringent aviation regulatory approvals limit entry for small suppliers

- For instance, during 2024–2025, fluctuations in raw material prices such as titanium and specialty alloys, along with supply chain disruptions, increased production costs for several global valve manufacturers

- Complex integration requirements within modern aircraft hydraulic and fuel systems demand highly specialized engineering expertise and rigorous testing procedures

- Long product development cycles and strict compliance standards from aviation authorities extend time-to-market for new valve technologies

- Competition from integrated fluid control modules and alternative system architectures creates pricing pressure and technological challenges

- To address these constraints, companies are focusing on lightweight material innovation, digital monitoring capabilities, streamlined certification processes, and strategic OEM partnerships to strengthen global adoption of advanced aerospace valve systems

How is the Aerospace Valves Market Segmented?

The market is segmented on the basis of valves type, material, mechanism, aviation, and end-user.

- By Valves

On the basis of valves, the Aerospace Valves market is segmented into Aerospace Water and Waste System Valves, Aerospace Lubrication Systems Valves, Aerospace Pneumatic System Valves, Aerospace Ice and Rain System Valves, Aerospace Air Conditioning System Valves, Aerospace Hydraulic System Valves, and Aerospace Fuel System Valves. The Aerospace Fuel System Valves segment dominated the market with a 29.8% share in 2025, driven by their critical role in regulating fuel flow, maintaining engine efficiency, and ensuring operational safety across commercial and military aircraft. Increasing aircraft production and engine modernization programs continue to strengthen demand.

The Aerospace Hydraulic System Valves segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising electrification of aircraft systems, expansion of flight control technologies, and growing demand for high-pressure, lightweight hydraulic components.

- By Material

On the basis of material, the market is segmented into Titanium, Aluminium, Corrosion Resistant Steel, and Others. The Titanium segment dominated the market with a 37.6% share in 2025, owing to its superior strength-to-weight ratio, high corrosion resistance, and ability to withstand extreme temperatures and pressures in aerospace environments. Titanium valves are widely preferred in critical aircraft systems where durability and weight optimization are essential.

The Aluminium segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing emphasis on lightweight aircraft structures, cost efficiency, and improved fuel economy in next-generation aircraft programs.

- By Mechanism

On the basis of mechanism, the Aerospace Valves market is segmented into Ball and Plug Valves, Flapper-Nozzle Valves, Pilot Valves, Poppet Valves, and Others. The Ball and Plug Valves segment dominated the market with a 32.4% share in 2025, supported by their simple design, reliable sealing capability, and suitability for high-pressure aerospace fluid control systems. Their durability and low maintenance requirements make them widely adopted across fuel and hydraulic applications.

The Poppet Valves segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing demand for precise flow control, rapid response mechanisms, and enhanced performance in modern aircraft systems.

- By Aviation

On the basis of aviation, the market is segmented into Business and General Aviation, Military Aviation, and Commercial Aviation. The Commercial Aviation segment dominated the market with a 45.1% share in 2025, driven by expanding global passenger traffic, aircraft fleet expansion, and rising MRO activities. Commercial aircraft require a large volume of advanced valve systems to support fuel, hydraulic, and environmental control operations.

The Military Aviation segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by rising defense budgets, next-generation fighter jet programs, UAV development, and modernization of military aircraft fleets.

- By End-User

On the basis of end-user, the Aerospace Valves market is segmented into Original Equipment Manufacturer (OEM) and Aftermarket. The OEM segment dominated the market with a 58.3% share in 2025, driven by increasing new aircraft deliveries, integration of advanced valve technologies, and long-term supply contracts with aircraft manufacturers.

The Aftermarket segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by growing global aircraft fleets, rising maintenance cycles, replacement demand, and strict regulatory compliance requirements for aviation safety and performance.

Which Region Holds the Largest Share of the Aerospace Valves Market?

- North America dominated the aerospace valves market with a 40.7% revenue share in 2025, driven by strong aircraft manufacturing presence, extensive defense spending, and continuous technological advancements across the U.S. and Canada. High production of commercial aircraft, military jets, UAVs, and space systems continues to fuel demand for advanced fuel, hydraulic, pneumatic, and environmental control valves across OEM and MRO facilities

- Leading aerospace manufacturers and component suppliers in North America are introducing lightweight, corrosion-resistant, and electronically actuated valve systems, strengthening the region’s technological leadership. Continuous investment in next-generation aircraft programs, space exploration missions, and aircraft electrification initiatives supports long-term market expansion

- Strong regulatory frameworks, high R&D expenditure, and the presence of major aircraft OEMs further reinforce regional market dominance

U.S. Aerospace Valves Market Insight

The U.S. is the largest contributor within North America, supported by the presence of major aircraft manufacturers, defense contractors, and advanced aerospace component suppliers. Increasing production of next-generation commercial aircraft, fighter jets, rotorcraft, and space launch vehicles drives sustained demand for high-performance valve systems. Rising investments in electric aircraft, unmanned aerial systems, and space programs further accelerate adoption of lightweight and smart valve technologies. Strong MRO infrastructure and long-term defense modernization initiatives continue to strengthen market growth across the country.

Canada Aerospace Valves Market Insight

Canada contributes significantly to regional growth due to its strong aerospace manufacturing clusters and participation in global aircraft supply chains. Increasing production of regional jets, business aircraft, and aircraft components supports steady demand for hydraulic and fuel system valves. Government-backed aerospace innovation programs and rising focus on sustainable aviation technologies further enhance adoption of advanced valve systems across commercial and defense applications.

Asia-Pacific Aerospace Valves Market

Asia-Pacific is projected to register the fastest CAGR of 10.8% from 2026 to 2033, driven by rapid expansion of aircraft fleets, increasing defense budgets, and strong growth in domestic aircraft manufacturing across China, Japan, India, and South Korea. Rising air passenger traffic and infrastructure development are accelerating procurement of new commercial aircraft. Growing investments in indigenous fighter jet programs, UAV development, and space exploration further stimulate demand for high-performance aerospace valve systems across the region.

China Aerospace Valves Market Insight

China is the largest contributor within Asia-Pacific, supported by expanding commercial aircraft programs, strong defense modernization efforts, and increasing investments in space exploration. Development of indigenous aircraft platforms and engine technologies is driving demand for advanced fuel and hydraulic valve systems. Government-backed manufacturing initiatives and strong domestic supply chains further strengthen market expansion.

Japan Aerospace Valves Market Insight

Japan demonstrates steady growth supported by advanced aerospace engineering capabilities and strong participation in global aircraft programs. Increasing focus on high-precision manufacturing, lightweight materials, and safety compliance drives demand for premium aerospace valve technologies. Ongoing defense upgrades and participation in next-generation fighter programs further reinforce market growth.

India Aerospace Valves Market Insight

India is emerging as a high-growth market due to rising defense procurement, indigenous aircraft development programs, and expanding MRO infrastructure. Government initiatives promoting domestic aerospace manufacturing and growing participation in global supply chains are accelerating demand for advanced aerospace valves across military and commercial segments.

South Korea Aerospace Valves Market Insight

South Korea contributes significantly due to increasing development of indigenous fighter aircraft, UAV systems, and space launch programs. Growing defense budgets and expansion of aerospace manufacturing capabilities are driving demand for precision-engineered valve systems. Technological innovation and collaboration with global aerospace companies continue to support long-term regional growth.

Which are the Top Companies in Aerospace Valves Market?

The aerospace valves industry is primarily led by well-established companies, including:

- Parker Hannifin Corp. (U.S.)

- Eaton (Ireland)

- Honeywell International Inc. (U.S.)

- Zodiac Aerospace (France)

- Woodward, Inc. (U.S.)

- AeroControlex (U.S.)

- Crane Aerospace & Electronics (U.S.)

- Moog Inc. (U.S.)

- Liebherr (Switzerland)

- ITT Inc. (U.S.)

- Porvair Filtration Group (U.K.)

- Crissair, Inc. (U.S.)

- CIRCOR International, Inc. (U.S.)

- Dynex/Rivett Inc. (U.S.)

- Meggitt PLC (U.K.)

- LAKSHMI TECHNOLOGY AND ENGINEERING INDUSTRIES (India)

- Valcor Engineering Corporation (U.S.)

- United Technologies Corporation (U.S.)

- Triumph Group, Inc. (U.S.)

- Sitec Aerospace GmbH (Germany)

What are the Recent Developments in Global Aerospace Valves Market?

- In January 2025, Aerolloy Technologies commissioned its first Vacuum Arc Remelting furnace to domestically manufacture aerospace-grade titanium alloys, strengthening local production of lightweight, high-performance materials for aircraft engines and gas turbines while reducing dependence on imports and enhancing supply chain resilience in the aerospace components market, thereby reinforcing long-term material self-sufficiency and industry growth

- In November 2024, a newly developed servo-driven lightweight latch valve was successfully tested under simulated rocket flight conditions, introducing a compact and weight-efficient alternative to conventional motor-based systems while delivering improved reliability across fluctuating temperature and pressure environments, ultimately advancing propulsion efficiency and precision fluid control for next-generation aerospace applications

- In June 2024, Honeywell International introduced an additively manufactured bleed-pressure regulating valve designed for trainer aircraft, showcasing the growing adoption of digital production technologies and advanced materials to achieve lightweight, complex, and durable aerospace components while reducing production timelines, thereby accelerating modernization of aerospace manufacturing processes

- In November 2022, Triumph Group secured a contract from Lockheed Martin to produce brake valve assemblies for the F-16 Fighting Falcon aircraft, committing to deliver production hardware and operational support, thus strengthening its position in military aircraft component manufacturing and long-term defense supply programs

- In August 2022, Marsh Brothers Aviation entered into a four-year agreement with Aviation Fabricators to supply customized aircraft seat actuator valves after resolving supply chain challenges, supporting maintenance, repair, and overhaul operations for private and commercial aircraft seating systems while reinforcing reliability and continuity within the aerospace aftermarket supply chain

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.