Global Agricultural Drones Market

Market Size in USD Billion

CAGR :

%

USD

8.30 Billion

USD

10.68 Billion

2025

2033

USD

8.30 Billion

USD

10.68 Billion

2025

2033

| 2026 –2033 | |

| USD 8.30 Billion | |

| USD 10.68 Billion | |

| % | |

|

Agricultural Drones Market Size

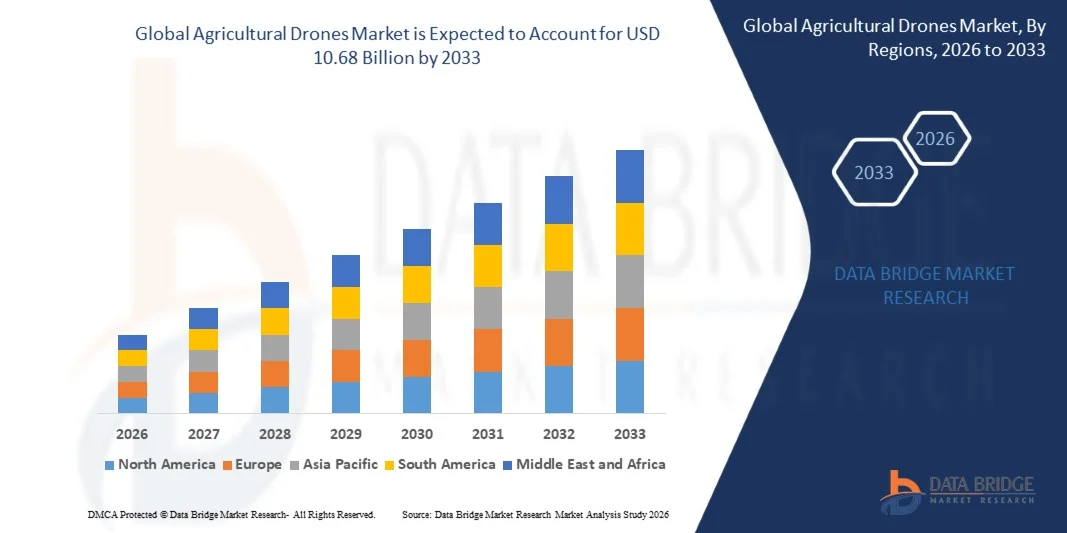

- The global agricultural drones market size was valued at USD 8.30 billion in 2025 and is expected to reach USD 10.68 billion by 2033, at a CAGR of 3.20% during the forecast period

- The market growth is largely fuelled by the increasing adoption of precision agriculture technologies that help farmers improve crop monitoring, irrigation management, and yield optimization

- Rising demand for efficient crop spraying, field mapping, and real-time farm data collection is further accelerating the adoption of agricultural drones across large-scale farming operations

Agricultural Drones Market Analysis

- The agricultural drones market is witnessing steady growth due to the rising need for efficient farm management, labor cost reduction, and improved agricultural productivity through advanced aerial monitoring technologies

- Increasing investments in precision agriculture solutions, combined with advancements in drone sensors, analytics software, and autonomous flight capabilities, are strengthening the role of drones in modern farming operations

- North America dominated the agricultural drones market with the largest revenue share in 2025, driven by the rapid adoption of precision agriculture technologies and strong investments in smart farming solutions

- Asia-Pacific region is expected to witness the highest growth rate in the global agricultural drones market, driven by rapid urbanization, increasing food demand, modernization of agriculture, and supportive government policies. Countries such as China, India, and Japan are investing heavily in smart farming technologies, enabling widespread adoption of agricultural drones for crop monitoring, spraying, and field management

- The Rotary Wing segment held the largest market revenue share in 2025 driven by its ability to hover, perform vertical take-off and landing, and operate effectively in smaller or irregular farm fields. Rotary wing drones are widely used for crop spraying, crop monitoring, and field surveillance, making them a preferred choice among farmers and agricultural service providers

Report Scope and Agricultural Drones Market Segmentation

|

Attributes |

Agricultural Drones Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• DJI (China) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Agricultural Drones Market Trends

“Increasing Adoption of Precision Agriculture and Smart Farming Technologies”

• The rapid adoption of precision agriculture practices is significantly shaping the agricultural drones market, as farmers increasingly rely on advanced technologies to optimize crop productivity and resource efficiency. Agricultural drones are widely used for crop monitoring, soil analysis, and field mapping, enabling farmers to collect real-time data and make informed decisions. This trend is encouraging manufacturers to introduce drones with improved sensors, AI-powered analytics, and automated flight capabilities to enhance farming efficiency and reduce operational costs

• Growing demand for efficient crop management and higher agricultural productivity is accelerating the adoption of agricultural drones across large-scale farming operations. Drones assist in tasks such as crop spraying, irrigation monitoring, and pest detection, allowing farmers to reduce chemical usage and improve yield quality. The integration of GPS, imaging technologies, and data analytics is further strengthening the role of drones in modern agriculture, encouraging wider adoption among commercial farms and agribusiness companies

• Technological advancements such as multispectral imaging, thermal sensors, and AI-based data analysis are transforming the functionality of agricultural drones. These technologies allow farmers to detect crop health issues, water stress, and nutrient deficiencies at an early stage, enabling timely intervention. As a result, agricultural technology companies are investing heavily in research and development to improve drone efficiency, battery life, and data accuracy to support precision farming applications

• For instance, in 2024, companies such as DJI in China and Trimble Inc. in the U.S. introduced advanced agricultural drone solutions equipped with high-resolution imaging and automated spraying systems. These drones were launched to support precision agriculture practices and were widely adopted by commercial farms and agritech service providers. The products were distributed through agricultural equipment dealers and digital platforms to expand accessibility among farmers

• While adoption of agricultural drones is expanding rapidly, sustained market growth depends on continuous technological improvements, cost-effective drone solutions, and regulatory support for commercial drone operations. Companies are also focusing on improving battery efficiency, flight endurance, and data integration capabilities to deliver scalable and reliable solutions for modern agriculture

Agricultural Drones Market Dynamics

Driver

“Rising Adoption of Precision Agriculture and Data-Driven Farming”

• Increasing global demand for food production and efficient farming practices is a major driver for the agricultural drones market. Farmers are adopting drone technology to monitor crop health, manage irrigation, and optimize fertilizer application, improving productivity while reducing resource wastage. These solutions enable data-driven decision-making, supporting sustainable agricultural practices and higher crop yields

• Expanding use of drones in crop spraying, planting analysis, livestock monitoring, and field mapping is accelerating market growth. Agricultural drones provide high-resolution aerial imagery and detailed field insights that help farmers detect pest infestations, nutrient deficiencies, and crop diseases early. This capability improves farm management efficiency and reduces dependency on manual field inspections

• Governments and agricultural organizations are increasingly promoting drone adoption through subsidies, pilot programs, and regulatory frameworks aimed at supporting digital agriculture. These initiatives encourage farmers and agribusiness companies to integrate drone technology with existing farm management systems, driving innovation and adoption across the agricultural sector

• For instance, in 2023, companies such as AeroVironment Inc. and Parrot SA expanded their agricultural drone portfolios with advanced aerial imaging and crop monitoring capabilities. These innovations were introduced to meet increasing demand for data-driven farming solutions and were promoted through collaborations with agricultural technology providers and farm management platforms

• Although precision agriculture trends are supporting strong demand, long-term market expansion will depend on improved affordability, enhanced drone durability, and reliable data analytics platforms. Investments in AI integration, sensor technologies, and farmer training programs will be essential to maximize the benefits of agricultural drone adoption globally

Restraint/Challenge

“High Initial Investment and Regulatory Restrictions for Drone Operations”

• The relatively high initial cost of agricultural drones and supporting software remains a significant challenge for small and medium-scale farmers. Advanced drones equipped with multispectral sensors, AI analytics, and automated spraying systems require substantial investment, limiting accessibility for farmers with limited financial resources. Maintenance, training, and software subscription costs can further increase overall operational expenses

• Regulatory restrictions on commercial drone operations also pose barriers to market growth in several countries. Strict airspace regulations, licensing requirements, and safety standards may delay drone deployment for agricultural purposes. Compliance with these regulations requires additional training and certification for drone operators, increasing operational complexity for farmers and agribusinesses

• Technical limitations such as limited flight time, battery constraints, and data processing requirements can affect operational efficiency. Large agricultural fields may require multiple drone flights to collect comprehensive data, increasing operational time and costs. In addition, farmers may face challenges in interpreting complex drone-generated data without specialized analytical tools or technical expertise

• For instance, in 2024, agricultural drone distributors in countries such as Brazil and India reported slower adoption among small-scale farmers due to high equipment costs and regulatory approval requirements. Some farming cooperatives also highlighted challenges related to operator training and data management, which limited the use of drone technology across smaller farms

• Addressing these challenges will require cost-efficient drone solutions, simplified regulatory frameworks, and improved training programs for farmers and agribusiness operators. Collaboration between drone manufacturers, governments, and agricultural organizations will be essential to expand awareness, improve accessibility, and unlock the full potential of agricultural drones in modern farming systems

Agricultural Drones Market Scope

The market is segmented on the basis of offering, component, range, farm size, and application.

• By Offering

On the basis of offering, the agricultural drones market is segmented into Fixed Wing, Rotary Wing, and Hybrid Wing. The Rotary Wing segment held the largest market revenue share in 2025 driven by its ability to hover, perform vertical take-off and landing, and operate effectively in smaller or irregular farm fields. Rotary wing drones are widely used for crop spraying, crop monitoring, and field surveillance, making them a preferred choice among farmers and agricultural service providers.

The Hybrid Wing segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to combine the long flight endurance of fixed wing drones with the hovering capabilities of rotary wing drones. Hybrid drones are increasingly being adopted for large-scale agricultural mapping and monitoring applications where extended coverage and operational flexibility are required.

• By Component

On the basis of component, the agricultural drones market is segmented into Cameras, Batteries, Navigation Systems, and Others. The Cameras segment held the largest market revenue share in 2025 driven by the growing use of high-resolution, multispectral, and thermal imaging cameras for crop monitoring and field analysis. These cameras enable farmers to detect crop health issues, pest infestations, and nutrient deficiencies, supporting precision farming practices.

The Navigation Systems segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of GPS, GNSS, and AI-enabled navigation technologies that enable autonomous drone operations. Advanced navigation systems improve flight stability, mapping accuracy, and automated route planning, making them essential components for modern agricultural drone applications.

• By Range

On the basis of range, the agricultural drones market is segmented into Visual Line of Sight (VLOS) and Beyond Visual Line of Sight (BVLOS). The VLOS segment held the largest market revenue share in 2025 driven by regulatory frameworks in many countries that require drone operators to maintain direct visual contact during operations. VLOS drones are widely used for crop monitoring, spraying, and small-field surveillance due to their operational simplicity and lower regulatory barriers.

The BVLOS segment is expected to witness the fastest growth rate from 2026 to 2033, driven by advancements in drone communication systems, satellite navigation, and regulatory developments supporting long-distance drone operations. BVLOS drones enable large-scale agricultural monitoring and mapping, allowing farmers to cover extensive farmland more efficiently.

• By Farm Size

On the basis of farm size, the agricultural drones market is segmented into Small Farms, Mid-Sized Farms, and Large Farms. The Large Farms segment held the largest market revenue share in 2025 driven by the higher adoption of advanced agricultural technologies and the need for efficient monitoring across extensive farmland areas. Agricultural drones help large farms improve productivity through automated crop monitoring, spraying, and data-driven decision-making.

The Mid-Sized Farms segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing awareness of precision agriculture and growing affordability of drone technologies. Farmers operating mid-sized farms are increasingly adopting drone solutions to enhance crop management, reduce operational costs, and improve yield quality.

• By Application

On the basis of application, the agricultural drones market is segmented into Precision Agriculture, Livestock Monitoring, Smart Greenhouse, Irrigation, Precision Fish Farming, and Others. The Precision Agriculture segment held the largest market revenue share in 2025 driven by the widespread use of drones for crop monitoring, soil analysis, and precision spraying. These drones provide real-time data and aerial insights that help farmers optimize resource usage and improve overall farm productivity.

The Livestock Monitoring segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing use of drones to track animal movement, monitor grazing patterns, and detect health issues in livestock. Drone-based monitoring helps farmers manage large herds more efficiently while reducing manual labor and improving overall farm management.

Agricultural Drones Market Regional Analysis

• North America dominated the agricultural drones market with the largest revenue share in 2025, driven by the rapid adoption of precision agriculture technologies and strong investments in smart farming solutions

• Farmers and agribusinesses in the region increasingly rely on drones for crop monitoring, field mapping, irrigation analysis, and precision spraying to improve productivity and reduce operational costs

• This widespread adoption is further supported by advanced agricultural infrastructure, high awareness of digital farming technologies, and strong presence of agritech companies, establishing agricultural drones as a critical tool for modern farm management across large commercial farms

U.S. Agricultural Drones Market Insight

The U.S. agricultural drones market captured the largest revenue share in 2025 within North America, fueled by the increasing adoption of precision agriculture and advanced farm management technologies. Farmers are increasingly using drones for crop health monitoring, pest detection, and yield optimization. The presence of major agricultural technology providers and supportive government initiatives encouraging the use of digital farming tools further support market growth. In addition, the integration of drones with data analytics platforms and farm management software is enhancing operational efficiency and driving the adoption of agricultural drones across commercial farming operations.

Europe Agricultural Drones Market Insight

The Europe agricultural drones market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing emphasis on sustainable agriculture and the adoption of advanced farming technologies. The region is experiencing growing demand for precision agriculture solutions that help optimize resource utilization and reduce environmental impact. European farmers are increasingly adopting drones for crop monitoring, irrigation management, and soil analysis. Furthermore, supportive regulatory frameworks and rising investments in agricultural innovation are encouraging the adoption of drone technologies across the region.

U.K. Agricultural Drones Market Insight

The U.K. agricultural drones market is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of precision farming techniques and the need to improve agricultural productivity. Farmers are increasingly integrating drones into crop monitoring and field mapping operations to enhance decision-making and optimize input usage. In addition, the country’s strong focus on technological innovation and sustainable farming practices is supporting the growth of agricultural drone adoption across both large-scale farms and agribusiness operations.

Germany Agricultural Drones Market Insight

The Germany agricultural drones market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong emphasis on agricultural efficiency, sustainability, and digital transformation. German farmers are increasingly adopting drone technologies to monitor crop conditions, detect plant diseases, and manage irrigation more efficiently. The country’s advanced technological infrastructure and strong focus on research and development are also encouraging the integration of drone-based solutions into modern farming practices.

Asia-Pacific Agricultural Drones Market Insight

The Asia-Pacific agricultural drones market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid population growth, increasing food demand, and the modernization of farming practices in countries such as China, Japan, and India. Governments across the region are promoting the adoption of precision agriculture technologies to improve productivity and reduce resource wastage. In addition, the presence of large agricultural land areas and the growing availability of affordable drone technologies are encouraging farmers to adopt drone-based solutions for crop monitoring and farm management.

Japan Agricultural Drones Market Insight

The Japan agricultural drones market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced technological ecosystem and strong focus on agricultural automation. Japanese farmers are increasingly using drones for crop spraying, monitoring rice fields, and improving farm efficiency. The integration of drones with smart farming systems and IoT-based agricultural solutions is further driving adoption. In addition, the country’s aging farming population is encouraging the use of automated technologies such as drones to reduce manual labor and improve operational efficiency.

China Agricultural Drones Market Insight

The China agricultural drones market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large agricultural sector, rapid technological adoption, and strong government support for smart agriculture initiatives. China has emerged as a major hub for agricultural drone manufacturing and innovation, enabling widespread availability of cost-effective drone solutions. The increasing use of drones for crop spraying, field surveillance, and agricultural data collection is significantly contributing to the growth of the agricultural drones market across the country.

Agricultural Drones Market Share

The Agricultural Drones industry is primarily led by well-established companies, including:

• Parrot Drones SAS (France)

• Aurora Flight Sciences (U.S.)

• Denel SOC Ltd (South Africa)

• Draganfly Inc. (Canada)

• 3DR (U.S.)

• DJI (China)

• Aeryon Labs Inc. (Canada)

• Northrop Grumman (U.S.)

• Lockheed Martin Corporation (U.S.)

• Elbit Systems Ltd. (Israel)

• General Dynamics Corporation (U.S.)

• AeroVironment, Inc. (U.S.)

• Leptron Unmanned Aircraft Systems, Inc. (U.S.)

• PrecisionHawk (U.S.)

• YUNEEC (China)

• Trimble Inc. (U.S.)

• INSITU (U.S.)

• senseFly (Switzerland)

• Xiaomi (China)

• Sentera, Inc. (U.S.)

• AiRXOS (U.S.)

• General Electric (U.S.)

• QUADROCOPTER (Germany)

Latest Developments in Global Agricultural Drones Market

- In December 2025, Jyoti Global Plast launched the AeroCrop UAS, an agricultural drone designed to enhance efficiency, safety, and accuracy in crop spraying. Leveraging its 40 years of expertise in plastic and FRP molding, the company is expanding into the unmanned systems market. The AeroCrop UAS is aimed at addressing challenges faced by Indian farmers, including labor shortages and uneven crop coverage. Its adoption is expected to promote precision agriculture practices in India, improving yield quality and reducing operational costs. The launch strengthens Jyoti Global Plast’s position as a key player in the domestic agricultural drone market

- In August 2025, Terra Drone Corporation formed a sales partnership with PT. Yanmar Diesel Indonesia, a subsidiary of Yanmar Co., Ltd., to distribute the G20 and E16 agricultural drones. The partnership targets rice and field crop farmers, providing access to advanced drone technology for crop spraying and field monitoring. By enhancing regional availability, Terra Drone aims to boost adoption of precision agriculture solutions across Indonesia. The collaboration is expected to improve farm productivity, reduce chemical usage, and optimize resource management. This move also strengthens Terra Drone’s market presence in Southeast Asia, positioning it for further growth

- In July 2025, SZ DJI Technology Co., Ltd. introduced the Agras T100, T70P, and T25P agricultural drone series globally. These drones feature enhanced payload capacity, autonomous spraying and spreading, and advanced lifting capabilities. They are designed to support large-scale farming operations while ensuring precise application of fertilizers and pesticides. The launch reinforces DJI’s leadership in the global agricultural drone market and addresses growing demand for high-performance, automated farming solutions. Adoption of these drones is expected to increase operational efficiency, improve crop yields, and reduce labor dependency for farmers worldwide

- In May 2025, Hylio Inc. inaugurated a 40,000-square-foot agricultural drone manufacturing facility in Texas. The new facility increases production capacity approximately fivefold, enabling the company to produce around 5,000 drones annually. This expansion supports domestic precision agriculture adoption by making high-quality UAVs more accessible to U.S. farmers. The increased capacity also allows Hylio to meet rising demand from commercial farms and agribusinesses seeking automated crop spraying solutions. This development positions Hylio as a stronger competitor in the North American agricultural drone market

- In April 2024, DJI launched the Agras T50 and T25 drones globally, integrated with the SmartFarm app for comprehensive aerial application management. The T50 is tailored for large-scale farms, while the portable T25 suits smaller fields, providing flexibility for various farming operations. These drones improve spraying accuracy, reduce chemical waste, and optimize irrigation and crop monitoring processes. The launch strengthens DJI’s product portfolio in the precision agriculture sector and encourages adoption of smart farming solutions. Farmers benefit from improved efficiency, real-time data access, and reduced operational costs through these drones

- In July 2023, Pix4D SA released PIX4Dfields 2.4 with enhanced workflows for precision agriculture applications. The update introduces Targeted Operations, enabling users to create customized prescription maps quickly and efficiently. This enhancement simplifies drone data processing, improves planning accuracy, and supports precision spraying and fertilization practices. The launch provides farmers and agronomists with tools to optimize field management and reduce resource wastage. PIX4Dfields 2.4 contributes to broader adoption of data-driven farming practices, enhancing crop productivity and operational efficiency

- In December 2022, Connecticut, U.S., enacted Public Act 25-152 to expand legal use of drones for seeding, spraying, and crop surveying. This legislation modernizes regulations for agricultural UAV operations and aligns with Federal Aviation Administration requirements. The update facilitates broader adoption of drones by commercial farms, allowing more efficient crop management and monitoring. Farmers can leverage UAV technology for precise spraying, mapping, and data collection, improving yields and reducing labor costs. The act also encourages innovation in drone technology and supports growth in the domestic agricultural drone market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.