Global Air Suspension Market

Market Size in USD Billion

CAGR :

%

USD

9.74 Billion

USD

16.97 Billion

2025

2033

USD

9.74 Billion

USD

16.97 Billion

2025

2033

| 2026 –2033 | |

| USD 9.74 Billion | |

| USD 16.97 Billion | |

| % | |

|

Air Suspension Market Overview

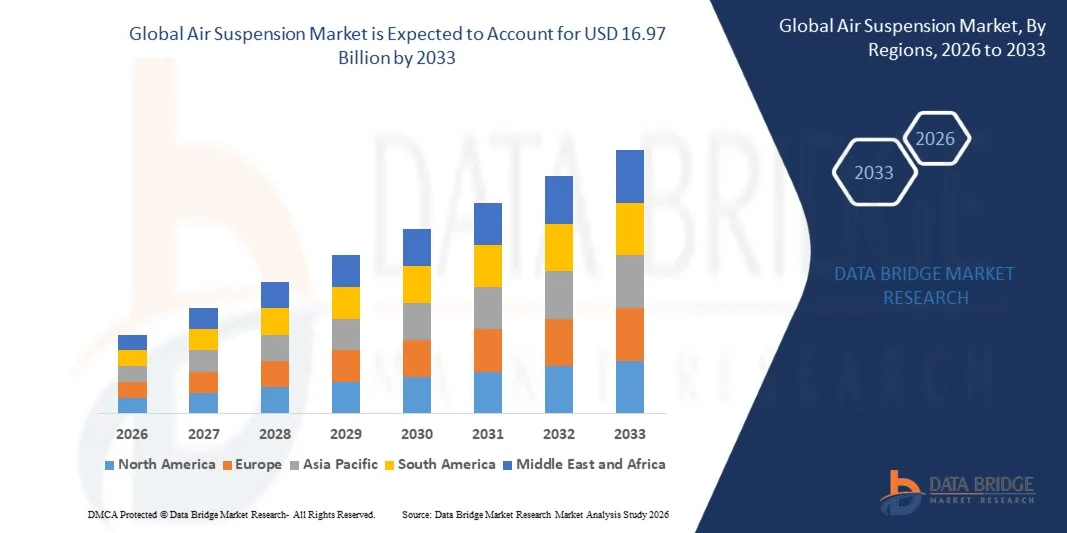

The global air suspension market was valued at USD 9.74 billion in 2025 and is projected to reach USD 16.97 billion by 2033, growing at a CAGR of 7.19% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for enhanced ride comfort, rising adoption of luxury and commercial vehicles, and growing focus on vehicle stability, load-bearing efficiency, and advanced suspension technologies across the automotive industry.

The growing production of heavy-duty trucks, buses, and premium passenger vehicles, combined with rising consumer preference for smooth driving experiences and improved vehicle handling, is accelerating the adoption of air suspension systems globally. Technological advancements such as electronically controlled air suspension systems, lightweight components, and integration with advanced driver assistance systems (ADAS) are further supporting market expansion. In addition, stringent government regulations related to vehicle safety, fuel efficiency, and emission reduction are encouraging automotive manufacturers to incorporate advanced suspension solutions to improve overall vehicle performance and operational efficiency.

Key Market Trends & Insights

· North America dominated the air suspension market with the largest revenue share of 38.42% in 2025, supported by strong demand for premium passenger vehicles, heavy commercial trucks, and advanced vehicle comfort technologies across the automotive sector.

- Asia-Pacific air suspension market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing vehicle production, and rising disposable incomes across countries such as China, Japan, South Korea, and India.

- The Trucks segment held the largest market revenue share of approximately 52.8% in 2025 driven by increasing deployment of air suspension systems in heavy-duty transportation fleets to improve cargo stability, ride comfort, and long-distance operational efficiency. Rising investments in logistics infrastructure and growing demand for fuel-efficient commercial transportation are further supporting segment dominance.

- The Bus segment is projected to register the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by increasing modernization of public transportation fleets and growing adoption of air suspension technologies to improve passenger comfort, vibration reduction, and vehicle stability across urban and intercity transportation systems.

- The Air Spring segment held the largest market revenue share of approximately 31.7% in 2025 driven by its critical role in shock absorption, load balancing, and ride height management across passenger and commercial vehicles. Increasing integration in premium vehicles and heavy transportation platforms is accelerating segment growth globally.

- The Electronic Control Unit (ECU) segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing integration of electronically controlled suspension technologies, predictive ride management systems, and intelligent vehicle control platforms. Growing adoption of adaptive suspension systems in electric and autonomous vehicles is further supporting market expansion.

- The Electronic Controlled segment held the largest market revenue share of approximately 63.4% in 2025 driven by rising demand for adaptive suspension adjustment, improved driving dynamics, and enhanced ride comfort in luxury passenger vehicles and commercial transportation fleets. Automotive manufacturers are increasingly integrating intelligent air suspension technologies to support premium mobility and vehicle automation trends.

- The Electronic Controlled segment is also projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by rapid advancements in smart sensors, autonomous driving technologies, and AI-assisted vehicle control systems. Increasing penetration of electric vehicles and premium SUVs is accelerating segment adoption globally.

- The Original Equipment Manufacturers (OEMs) segment held the largest market revenue share of approximately 71.6% in 2025 driven by increasing factory-level integration of advanced air suspension systems in premium passenger vehicles, buses, and heavy commercial transportation fleets. Automotive OEMs are increasingly prioritizing advanced ride comfort and vehicle stability technologies to strengthen competitive positioning and product differentiation.

- The Aftermarket segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising replacement demand for suspension components in aging commercial fleets and increasing customization trends among luxury and off-road vehicle owners. Expansion of specialized automotive maintenance services and performance upgrade solutions is further supporting segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 9.74 Billion

- Expected Market Value (2033): USD 16.97 Billion

- Forecast CAGR (2026–2033): 7.19%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Air Suspension Market Segmentation

|

Attributes |

Air Suspension Key Market Insights |

|

Segments Covered |

· By Vehicle Type: Light Commercial Vehicles (LCV), Trucks, Bus · By Component: Air Spring, Tank, Solenoid Valve, Shock Absorber, Air Compressor, Electronic Control Unit (ECU), Height and Pressure Sensor, and Air Reservoir · By Technology Type: Electronic Controlled and Non-Electronic Controlled · By Sales Channel Type: Original Equipment Manufacturers (OEMs), and Aftermarket |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Continental AG (Germany) |

|

Market Opportunities |

• Growing Adoption Of Electric And Autonomous Vehicles |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Global Air Suspension Market Trends

Trend: Increasing Integration Of Electronically Controlled And Adaptive Air Suspension Systems

Growing consumer demand for enhanced ride comfort, superior vehicle stability, and improved driving dynamics is accelerating the adoption of advanced air suspension technologies across passenger cars, luxury SUVs, and heavy commercial vehicles. Conventional mechanical suspension systems often provide limited adaptability across varying road and load conditions, encouraging automotive manufacturers to integrate electronically controlled air suspension systems capable of automatically adjusting ride height, damping force, and load balancing in real time.

In modern premium vehicles, manufacturers are integrating adaptive air suspension systems, For instance in luxury SUVs and electric vehicles, to improve passenger comfort, aerodynamic efficiency, and off-road capability while reducing vibration and cabin noise. In commercial transportation, fleet operators are increasingly deploying air suspension systems in buses and heavy-duty trucks to enhance cargo protection, reduce driver fatigue, and improve fuel efficiency through optimized vehicle height management.

The rapid expansion of electric vehicle production and autonomous driving technologies is also increasing demand for intelligent suspension systems capable of supporting enhanced vehicle control and weight distribution. In addition, advanced predictive suspension technologies integrated with onboard sensors and AI-driven vehicle control systems are gaining traction across Europe and North America. Real-world vehicle testing programs conducted in 2025 integrating adaptive air suspension systems into premium EV platforms demonstrated improvements of nearly 6–9% in ride stability and approximately 4–7% enhancement in aerodynamic efficiency under highway driving conditions.

Global Air Suspension Market Dynamics

Key Market Driver: Rising Demand For Enhanced Ride Comfort And Commercial Vehicle Efficiency

Automotive manufacturers and fleet operators worldwide are increasingly focusing on improving passenger comfort, vehicle handling, and operational efficiency to meet evolving transportation standards and customer expectations. Conventional suspension systems often struggle to maintain optimal ride quality under varying load conditions, creating strong demand for advanced air suspension technologies capable of delivering superior shock absorption and automatic load leveling.

Commercial vehicle manufacturers are increasingly deploying air suspension systems, For instance in heavy-duty trucks, trailers, and intercity buses, to improve cargo stability, reduce vehicle wear, and enhance long-distance driving comfort. Automotive OEMs are actively integrating electronically controlled air suspension systems into luxury passenger vehicles and electric SUVs to support premium driving experiences and improved vehicle dynamics.

Similarly, logistics companies and public transportation operators are adopting air suspension-equipped fleets to minimize maintenance costs and improve operational reliability across long-haul transportation networks. Real-world fleet modernization programs implemented in Germany and the U.S. during 2024 reported reductions of approximately 10–14% in suspension-related maintenance costs and nearly 5% improvements in fuel efficiency after deploying advanced air suspension systems in commercial truck fleets.

Key Restraint/Challenge: High System Costs And Complex Maintenance Requirements

Advanced air suspension systems involve sophisticated electronic controls, air compressors, sensors, and pneumatic components that significantly increase overall vehicle costs compared to traditional suspension technologies. The complexity of installation and maintenance creates affordability challenges, particularly in cost-sensitive automotive markets and entry-level vehicle segments where manufacturers prioritize lower production costs.

In addition, air leaks, compressor failures, and sensor malfunctions can increase long-term maintenance expenses and reduce system reliability in harsh operating environments. Limited availability of specialized repair infrastructure and trained service technicians further restricts adoption across developing regions where aftermarket support for advanced suspension technologies remains limited.

Commercial performance benchmarking studies indicate that maintenance and replacement costs associated with electronically controlled air suspension systems can be approximately 25–40% higher than conventional mechanical suspension systems over the vehicle lifecycle, particularly in high-mileage commercial fleet operations operating under demanding road conditions.

Key Market Opportunity: Expansion Of Electric Vehicles And Luxury Mobility Solutions

The rapid growth of electric vehicles, premium SUVs, and intelligent mobility platforms is creating significant opportunities for advanced air suspension technologies capable of improving vehicle comfort, energy efficiency, and driving stability. Electric vehicle manufacturers increasingly require lightweight and adaptive suspension systems to compensate for heavy battery packs and maintain balanced vehicle dynamics across diverse driving conditions.

Automotive companies are increasingly integrating air suspension technologies, For instance for automatic ride height adjustment, terrain adaptation, and aerodynamic optimization, to improve EV range, passenger comfort, and vehicle handling without increasing mechanical complexity. In luxury mobility solutions, rising consumer preference for premium driving experiences is accelerating the adoption of predictive and semi-autonomous suspension systems integrated with onboard cameras and road-scanning sensors.

In addition, advancements in lightweight composite materials, smart sensors, and AI-assisted vehicle control systems are expanding opportunities across autonomous transportation, luxury buses, and next-generation electric commercial vehicles in Asia-Pacific and Europe. EV development programs conducted in 2025 across China and Germany reported ride comfort improvements of approximately 12–15% and battery efficiency gains of nearly 4–6% after integrating adaptive air suspension systems with intelligent vehicle control platforms.

Global Air Suspension Market Scope

The market is segmented on the basis of vehicle type, component, technology type, and sales channel type.

- By Vehicle Type

On the basis of vehicle type, the air suspension market is segmented into Light Commercial Vehicles (LCV), Trucks, and Bus. The Trucks segment held the largest market revenue share of approximately 52.8% in 2025 driven by increasing deployment of air suspension systems in heavy-duty transportation fleets to improve cargo stability, ride comfort, and long-distance operational efficiency. Rising investments in logistics infrastructure and growing demand for fuel-efficient commercial transportation are further supporting segment dominance.

The Bus segment is projected to register the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by increasing modernization of public transportation fleets and growing adoption of air suspension technologies to improve passenger comfort, vibration reduction, and vehicle stability across urban and intercity transportation systems.

- By Component

On the basis of component, the air suspension market is segmented into Air Spring, Tank, Solenoid Valve, Shock Absorber, Air Compressor, Electronic Control Unit (ECU), Height and Pressure Sensor, and Air Reservoir. The Air Spring segment held the largest market revenue share of approximately 31.7% in 2025 driven by its critical role in shock absorption, load balancing, and ride height management across passenger and commercial vehicles. Increasing integration in premium vehicles and heavy transportation platforms is accelerating segment growth globally.

The Electronic Control Unit (ECU) segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing integration of electronically controlled suspension technologies, predictive ride management systems, and intelligent vehicle control platforms. Growing adoption of adaptive suspension systems in electric and autonomous vehicles is further supporting market expansion.

- By Technology Type

On the basis of technology type, the air suspension market is segmented into Electronic Controlled and Non-Electronic Controlled. The Electronic Controlled segment held the largest market revenue share of approximately 63.4% in 2025 driven by rising demand for adaptive suspension adjustment, improved driving dynamics, and enhanced ride comfort in luxury passenger vehicles and commercial transportation fleets. Automotive manufacturers are increasingly integrating intelligent air suspension technologies to support premium mobility and vehicle automation trends.

The Electronic Controlled segment is also projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by rapid advancements in smart sensors, autonomous driving technologies, and AI-assisted vehicle control systems. Increasing penetration of electric vehicles and premium SUVs is accelerating segment adoption globally.

- By Sales Channel Type

On the basis of sales channel type, the air suspension market is segmented into Original Equipment Manufacturers (OEMs) and Aftermarket. The Original Equipment Manufacturers (OEMs) segment held the largest market revenue share of approximately 71.6% in 2025 driven by increasing factory-level integration of advanced air suspension systems in premium passenger vehicles, buses, and heavy commercial transportation fleets. Automotive OEMs are increasingly prioritizing advanced ride comfort and vehicle stability technologies to strengthen competitive positioning and product differentiation.

The Aftermarket segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising replacement demand for suspension components in aging commercial fleets and increasing customization trends among luxury and off-road vehicle owners. Expansion of specialized automotive maintenance services and performance upgrade solutions is further supporting segment growth.

Global Air Suspension Market Regional Analysis

North America Air Suspension Market Insight

North America dominated the air suspension market with the largest revenue share of 38.42% in 2025, supported by strong demand for premium passenger vehicles, heavy commercial trucks, and advanced vehicle comfort technologies across the automotive sector. Consumers and fleet operators in the region highly value enhanced ride comfort, vehicle stability, improved load balancing, and fuel efficiency offered by electronically controlled air suspension systems in both passenger and commercial transportation applications. This widespread adoption is further supported by advanced automotive manufacturing infrastructure, rising penetration of electric and luxury vehicles, and increasing investments in intelligent transportation technologies, establishing air suspension systems as a preferred solution across logistics fleets, public transportation, and premium mobility platforms.

U.S. Air Suspension Market Insight

The U.S. air suspension market captured the largest revenue share in 2025 within North America, fueled by rising adoption of luxury SUVs, electric vehicles, and heavy-duty commercial trucks equipped with advanced suspension technologies. Fleet operators are increasingly prioritizing ride stability, cargo protection, and driver comfort to improve long-haul transportation efficiency. The growing deployment of adaptive air suspension systems in premium vehicles, combined with increasing investments in electric mobility and autonomous driving technologies, is further propelling the air suspension industry. Moreover, the presence of major automotive OEMs and advanced logistics infrastructure is significantly contributing to market expansion.

Europe Air Suspension Market Insight

The Europe air suspension market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent vehicle safety regulations, increasing focus on emission reduction, and growing demand for premium mobility solutions. The rapid expansion of electric vehicle production and luxury automotive manufacturing is fostering the adoption of electronically controlled air suspension systems across the region. European consumers are also increasingly demanding enhanced ride comfort and intelligent vehicle technologies. The region is experiencing strong growth across passenger cars, intercity buses, and heavy commercial transportation fleets, with air suspension systems being integrated into both conventional and electric vehicle platforms.

U.K. Air Suspension Market Insight

The U.K. air suspension market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of luxury vehicles, rising electric vehicle penetration, and growing demand for advanced driving comfort technologies. In addition, expanding logistics and public transportation modernization programs are encouraging fleet operators to deploy air suspension-equipped commercial vehicles for improved operational efficiency and cargo stability. The U.K.’s focus on sustainable transportation and smart mobility solutions is expected to continue stimulating market growth.

Germany Air Suspension Market Insight

The Germany air suspension market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong automotive manufacturing ecosystem and increasing integration of advanced suspension systems in luxury and performance vehicles. Germany’s emphasis on engineering innovation, vehicle safety, and premium mobility experiences is promoting the adoption of adaptive air suspension technologies across passenger and commercial vehicles. The integration of predictive suspension systems with autonomous driving and smart vehicle control platforms is also becoming increasingly prevalent, aligning with growing demand for intelligent automotive technologies.

Asia-Pacific Air Suspension Market Insight

The Asia-Pacific air suspension market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing vehicle production, and rising disposable incomes across countries such as China, Japan, South Korea, and India. The region’s growing demand for premium passenger vehicles, electric mobility, and commercial transportation efficiency is driving adoption of advanced air suspension systems. Furthermore, expanding automotive manufacturing capabilities and increasing investments in EV infrastructure are improving the affordability and accessibility of electronically controlled suspension technologies across Asia-Pacific markets.

Japan Air Suspension Market Insight

The Japan air suspension market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced automotive sector, strong demand for vehicle comfort, and increasing adoption of electric and hybrid vehicles. The Japanese market places significant emphasis on ride quality, passenger safety, and technological innovation, driving the integration of adaptive air suspension systems across premium passenger vehicles and high-speed transportation fleets. The integration of intelligent suspension technologies with autonomous driving systems and EV platforms is further fueling market growth. Moreover, Japan’s aging population and focus on comfortable mobility solutions are encouraging adoption across public transportation and luxury mobility applications.

China Air Suspension Market Insight

The China air suspension market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive production capacity, rapid urbanization, and growing consumer preference for luxury and electric vehicles. China stands as one of the largest automotive markets globally, and air suspension systems are becoming increasingly popular in premium passenger cars, electric SUVs, heavy-duty trucks, and smart mobility platforms. The country’s push toward intelligent transportation systems, combined with strong domestic EV manufacturing and increasing investments in advanced automotive technologies, are key factors propelling the market in China.

Global Air Suspension Market Share

The Air Suspension industry is primarily led by well-established companies, including:

• Continental AG (Germany)

• thyssenkrupp AG (Germany)

• Hitachi, Ltd. (Japan)

• WABCO (Belgium)

• Firestone Industrial Products Company, LLC (U.S.)

• Hendrickson USA, L.L.C. (U.S.)

• Mando Corp. (South Korea)

• BWI Group (China)

• SAF-HOLLAND S.A. (Germany)

• ACCUAIR SUSPENSION (U.S.)

• Vibracoustic (Germany)

• Dunlop Tires (U.K.)

• VB-Airsuspension (Netherlands)

• Link (U.S.)

• Universal Air (U.S.)

• Liftmatic (India)

• STEMCO Products Inc. (U.S.)

• Arnott LLC (U.S.)

• Shanghai Komman Vehicle Component Systems Stock Co., Ltd. (China)

• Jamna Auto Industries Ltd. (India)

Latest Developments in Global Air Suspension Market

- In July 2025, Volvo Car Korea launched the S90 Launch Edition equipped with advanced rear air suspension technology to enhance premium ride comfort, driving stability, and passenger experience in luxury sedan applications. The limited-edition launch, restricted to only 50 units, highlighted the growing adoption of electronically controlled suspension systems in high-end vehicles. The development is expected to strengthen consumer interest in premium comfort-oriented automotive technologies and accelerate air suspension integration across luxury vehicle segments globally.

- In April 2025, InMotion introduced the V9 electric unicycle featuring Nimbus Air suspension with 60 mm suspension travel to improve riding comfort, shock absorption, and operational stability for urban mobility users and performance riders. The product launch demonstrated increasing penetration of compact air suspension technologies in personal electric mobility solutions. The innovation is expected to support broader adoption of lightweight suspension systems across next-generation electric transportation platforms and micro-mobility applications.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.