Global Almond Flour Market

Market Size in USD Billion

CAGR :

%

USD

4.89 Billion

USD

9.15 Billion

2025

2033

USD

4.89 Billion

USD

9.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.89 Billion | |

| USD 9.15 Billion | |

| % | |

|

Almond Flour Market Overview

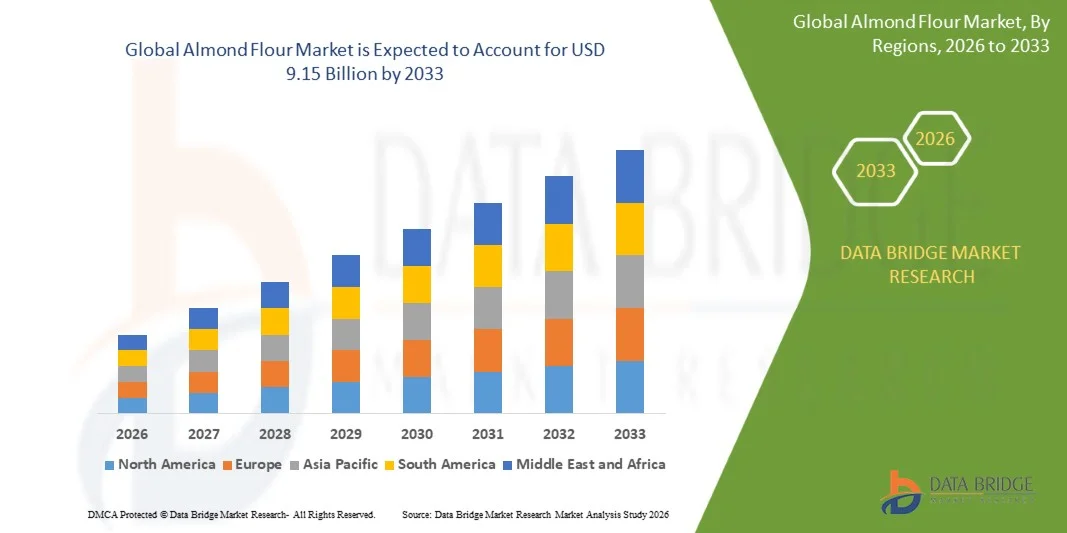

The Almond Flour Market was valued at USD 4.89 Billion in 2025 and is projected to reach USD 9.15 Billion by 2033, growing at a CAGR of 8.15% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for gluten-free and low-carb food alternatives, increasing consumer preference for clean-label and plant-based ingredients, and expanding use of almond flour in bakery, confectionery, and functional food applications. Growing health awareness, along with strong adoption of keto and paleo diets, is further accelerating product demand across both developed and emerging markets.

The increasing global shift toward healthier dietary habits, combined with rising prevalence of food allergies and gluten intolerance, is significantly boosting the adoption of almond flour as a wheat flour substitute. Food manufacturers are increasingly incorporating almond flour into premium bakery products, snacks, and dietary formulations to meet evolving consumer preferences for nutrient-dense and minimally processed ingredients. In addition, expansion of e-commerce food retailing and continuous product innovation in organic and specialty flour segments are further strengthening market growth globally.

Key Market Trends & Insights

- North America dominated the Almond Flour Market with the largest revenue share of 37.7% in 2025, supported by strong consumer demand for gluten-free, keto-friendly, and clean-label food products along with high penetration of health-focused dietary habits

- The conventional almond powder segment led the market with a 71% share in 2025, driven by its wide availability, cost efficiency, and strong adoption across mass-market bakery and processed food industries

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.3% from 2026 to 2033, fueled by rising disposable incomes, increasing awareness of healthy dietary habits, and expanding adoption of Western-style bakery products

- Organic almond powder is the fastest-growing nature type, projected to register a CAGR of 11.2% from 2026 to 2033, supported by increasing consumer shift toward organic and chemical-free food ingredients

- The blanched almond flour segment dominated the form category with a 62% revenue share in 2025, led by its fine texture, neutral taste profile, and high suitability for premium bakery and confectionery applications

- Bakery segment accounted for 48% of the market in 2025, preferred by extensive use of almond flour in gluten-free bread, cakes, cookies, and pastries

- The cosmetics segment is the fastest-growing application category, with a CAGR of 10.5% from 2026 to 2033, driven by rising use of almond flour as a natural exfoliant and skin-conditioning ingredient in skincare formulations

Market Size & Forecast

- Global Market Value (2025): USD 4.89 Billion

- Expected Market Value (2033): USD 9.15 Billion

- Forecast CAGR (2026–2033): 8.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Almond Flour Market Segmentation

|

Attributes |

Almond Flour Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Rolling Hills Nut Company (U.S.) · Ekowarehouse Ltd. (U.K.) · Hodgson Mill (U.S.) · WellBees (U.S.) · Honest to Goodness (Australia) · Blue Diamond Growers (U.S.) · TREEHOUSE ALMONDS (U.S.) · Bob’s Red Mill Natural Foods (U.S.) · Grain-Free JK Gourmet (Canada) · Nature’s Eats (U.S.) · Nature's Choice Food (U.S.) · Anthony's Goods (U.S.) · Barney Butter (U.S.) · Oleander Bio (South Africa) · SHILOH FARMS (U.S.) · King Arthur Baking Company, Inc (U.S.) |

|

Market Opportunities |

· Expansion in Functional and Keto-Friendly Food Applications · Growth in Organic and Premium Almond Flour Product Segments · Rising Adoption in Emerging E-Commerce and Direct-to-Consumer Channels |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Almond Flour Market Trends

Trend: Clean-Label and Gluten-Free Demand

Global consumers are increasingly shifting toward clean-label, gluten-free, and plant-based food products, significantly boosting almond flour adoption in bakery and packaged food applications. Almond flour is widely used as a wheat substitute in keto, paleo, and allergen-free diets due to its high protein, low carbohydrate profile, and natural nutritional value. Strong retail expansion of health-focused bakery products and premium flour alternatives is further accelerating market penetration across developed and emerging regions.

Companies such as Bob’s Red Mill Natural Foods and King Arthur Baking Company are actively expanding gluten-free and almond flour-based product portfolios, strengthening mainstream adoption of almond flour in consumer baking applications.

Almond Flour Market Dynamics

Key Market Driver: Health Awareness and Diet Shift

Rising global awareness of obesity, diabetes, and gluten intolerance is significantly driving demand for almond flour as a healthier alternative to refined wheat flour. Consumers are increasingly adopting low-carb, keto, and high-protein diets, pushing food manufacturers to integrate almond flour into bakery, snacks, and functional food formulations. Expanding demand for nutrient-dense and minimally processed ingredients is further supporting market growth across retail and industrial channels.

Companies such as Blue Diamond Growers and Hodgson Mill are expanding almond flour production and product lines to meet rising demand from health-conscious consumers and industrial food manufacturers.

Key Restraint/Challenge: High Raw Almond Price Volatility

Fluctuations in raw almond prices due to weather variability, water-intensive cultivation, and supply chain disruptions pose a significant challenge for almond flour manufacturers. Almond cultivation is highly concentrated in regions such as California, making the market vulnerable to drought conditions and yield instability, which directly impacts production costs. Rising input costs further affect pricing stability for downstream bakery and packaged food industries.

For instance, California almond production fluctuations reported by the Almond Board of California have historically influenced global pricing trends, creating cost pressure for manufacturers such as Blue Diamond Growers.

Key Market Opportunity: Expansion in Functional and Keto-Friendly Food Applications

Growing demand for functional foods, keto-friendly diets, and high-protein nutrition products is creating strong opportunities for almond flour across multiple applications. Almond flour is increasingly used in protein bars, low-carb bakery items, dietary supplements, and fortified food formulations due to its nutrient density and versatility. Continuous innovation in functional food development is expanding its usage beyond traditional baking into health and wellness categories.

Companies such as Simple Mills and Anthony’s Goods are expanding product lines focused on keto-friendly and functional baking mixes, strengthening almond flour’s position in the premium health food segment globally.

Almond Flour Market Scope

The almond flour market is segmented on the basis of form, nature, application, distribution channel, end user, and distribution channel.

- By Form

On the basis of form, the Almond Flour Market is segmented into Blanched Almond Flour and Natural Almond Flour. The Blanched Almond Flour segment dominated the market with the largest share of 62% in 2025, driven by its fine texture, neutral taste profile, and high suitability for premium bakery and confectionery applications. Food manufacturers increasingly prefer blanched variants for consistent product quality and improved binding performance in gluten-free formulations. Strong demand from commercial bakeries and packaged food producers further strengthens its leading position across developed and emerging markets.

The Natural Almond Flour segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising consumer preference for minimally processed and nutrient-dense ingredients. Increasing adoption in clean-label and health-focused food products is accelerating its demand across retail and specialty food channels. Growing awareness of fiber and micronutrient retention in natural variants is further supporting uptake. Expanding use in home baking and organic product formulations continues to boost segment expansion globally.

- By Nature

On the basis of nature, the Almond Flour Market is segmented into Conventional Almond Powder and Organic Almond Powder. The Conventional Almond Powder segment dominated the market with a share of 71% in 2025, supported by its wide availability, cost efficiency, and strong adoption across mass-market bakery and processed food industries. Large-scale manufacturers prefer conventional variants due to stable supply chains and consistent pricing structures. High consumption in industrial food processing further reinforces its dominant position across global markets.

The Organic Almond Powder segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by increasing consumer shift toward organic and chemical-free food ingredients. Rising penetration of certified organic products in supermarkets and specialty health stores is accelerating demand. Growing concerns regarding pesticide-free cultivation and sustainable sourcing practices are further strengthening adoption. Expanding use in premium health foods and dietary applications continues to support strong growth momentum.

- By Application

On the basis of application, the Almond Flour Market is segmented into Bakery, Confectionery, Cosmetics, and Other. The Bakery segment dominated the market with the largest share of 48% in 2025, driven by extensive use of almond flour in gluten-free bread, cakes, cookies, and pastries. Increasing demand for low-carb and keto-friendly bakery products is further enhancing adoption across commercial and artisanal bakeries. Strong product innovation in healthy baked goods continues to reinforce its leading position globally.

The Cosmetics segment is projected to register the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by rising use of almond flour as a natural exfoliant and skin-conditioning ingredient in skincare formulations. Growing preference for plant-based and chemical-free cosmetic products is accelerating its adoption in scrubs, face masks, and cleansing formulations. Expanding demand from personal care brands focusing on sustainable ingredients further supports segment growth. Increasing awareness of almond-derived skin nourishment benefits continues to strengthen market penetration.

- By End User

On the basis of end user, the Almond Flour Market is segmented into Household, Foodservice, Industrial, Cosmetic Industry, and Dietary Supplements. The Industrial segment dominated the market with a share of 44% in 2025, driven by large-scale utilization in packaged food manufacturing, bakery production, and processed food formulations. High-volume procurement by food companies for consistent product output strengthens its dominant position. Increasing demand for gluten-free and functional food products further supports industrial consumption globally.

The Dietary Supplements segment is projected to register the fastest growth at a CAGR of 12% from 2026 to 2033, driven by rising consumer focus on protein-rich and nutrient-dense nutritional supplements. Growing popularity of plant-based diets and fitness-oriented nutrition products is accelerating adoption of almond flour in supplement formulations. Increasing use in protein blends and meal replacement products further enhances demand. Expanding health awareness and preventive nutrition trends continue to drive strong segment growth.

- By Distribution Channel

On the basis of distribution channel, the Almond Flour Market is segmented into Direct and Indirect channels. The Indirect segment dominated the market with a share of 68% in 2025, supported by strong penetration through supermarkets, hypermarkets, specialty stores, and e-commerce platforms. Wide product availability and strong retail networks enhance consumer accessibility and drive higher sales volumes. Increasing preference for convenient purchasing channels further strengthens the dominance of indirect distribution.

The Direct segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by rising manufacturer-to-consumer sales through brand-owned websites and subscription-based models. Growing demand for bulk procurement from food processors and commercial buyers is further accelerating direct sales adoption. Expansion of digital commerce platforms and personalized purchasing experiences is strengthening channel growth. Increasing focus on margin optimization and supply chain efficiency continues to support segment expansion.

Almond Flour Market Regional Analysis

North America dominated the almond flour market and accounted for the largest revenue share of 37.7% in 2025, driven by strong consumer demand for gluten-free, keto-friendly, and clean-label food products along with high penetration of health-focused dietary habits. The region benefits from a well-established packaged food industry, advanced bakery manufacturing ecosystem, and widespread adoption of plant-based nutrition trends. Strong presence of major food processing companies and high retail availability across supermarkets and e-commerce platforms further strengthen market expansion. In addition, rising preference for nutrient-rich alternative flours in functional foods continues to reinforce North America’s leading position in the global market.

U.S. Almond Flour Market Insight

The U.S. Almond Flour market is witnessing strong growth driven by increasing adoption of gluten-free diets, rising prevalence of lifestyle-related health concerns, and expanding demand for low-carb and high-protein food alternatives. Consumers are increasingly shifting toward almond-based baking ingredients across household and commercial applications. The country’s strong packaged food industry and high innovation in clean-label bakery products are supporting large-scale adoption. In addition, growing presence of health-focused retail chains and e-commerce platforms is further accelerating market penetration across the U.S.

Canada Almond Flour Market Insight

The Canada Almond Flour market is experiencing steady growth supported by rising awareness of plant-based nutrition and increasing demand for organic and minimally processed food ingredients. Consumers are actively adopting almond flour in home baking and dietary meal preparations due to its perceived health benefits. The country’s expanding health food retail sector and growing penetration of specialty organic stores are further supporting market development. In addition, increasing focus on preventive nutrition and clean eating trends continues to drive consistent demand across Canada.

Europe Almond Flour Market Insight

The Europe Almond Flour market is expanding steadily due to strong demand for gluten-free bakery products, increasing adoption of vegan and plant-based diets, and rising consumer preference for natural food ingredients. The region’s well-established bakery industry and high consumption of premium confectionery products further support market growth. Strict food quality regulations and strong focus on clean-label certifications are encouraging adoption of almond flour in processed foods. In addition, growing innovation in healthy snacking and functional food products continues to strengthen regional market expansion.

U.K. Almond Flour Market Insight

The U.K. Almond Flour market is growing steadily driven by rising health consciousness, increasing demand for gluten-free baking ingredients, and strong penetration of premium bakery and confectionery products. Consumers are increasingly incorporating almond flour into home baking due to its nutritional profile and suitability for low-carb diets. The country’s advanced retail infrastructure and strong e-commerce penetration are supporting easy product availability. In addition, growing adoption of vegan and plant-based diets is further accelerating market demand in the U.K.

Germany Almond Flour Market Insight

The Germany Almond Flour market is expanding due to increasing consumer preference for organic food products, strong demand for high-quality bakery ingredients, and rising focus on healthy eating habits. The country’s robust bakery sector and strong inclination toward natural and sustainable food products are driving adoption of almond flour. Strict food safety regulations and high awareness of nutritional labeling further support market penetration. In addition, growing demand for functional and allergen-free food products continues to strengthen market growth in Germany.

Asia-Pacific Almond Flour Market Insight

The Asia-Pacific Almond Flour market is expected to register the fastest growth with a CAGR of 6.3% from 2026 to 2033, driven by rising disposable incomes, increasing awareness of healthy dietary habits, and expanding adoption of Western-style bakery products. Growing penetration of e-commerce platforms and increasing availability of premium health food products are significantly boosting market demand. Countries such as China, India, Japan, and South Korea are witnessing strong growth in gluten-free and plant-based food consumption. In addition, rising urbanization and growing fitness-oriented nutrition trends are further accelerating regional market expansion.

Japan Almond Flour Market Insight

The Japan Almond Flour market is witnessing steady growth supported by high consumer focus on health, strong demand for low-calorie bakery products, and increasing adoption of functional foods. Consumers are increasingly incorporating almond flour into traditional and modern recipes due to its nutritional benefits. The country’s advanced food processing industry and strong retail infrastructure are further supporting product availability. In addition, growing interest in plant-based and allergen-free diets continues to strengthen market demand in Japan.

China Almond Flour Market Insight

The China Almond Flour market is growing rapidly due to expanding health awareness, rising demand for premium bakery ingredients, and increasing penetration of Western dietary patterns. Consumers are increasingly adopting almond flour in home baking and packaged food consumption driven by its perceived health benefits. Strong e-commerce expansion and rapid growth of health food brands are further accelerating market adoption. In addition, rising urban middle-class population and increasing focus on nutrition-rich diets continue to drive strong market growth in China.

Almond Flour Market Share

The almond flour industry is primarily led by well-established companies, including:

- Rolling Hills Nut Company (U.S.)

- Ekowarehouse Ltd. (U.K.)

- Hodgson Mill (U.S.)

- WellBees (U.S.)

- Honest to Goodness (Australia)

- Blue Diamond Growers (U.S.)

- TREEHOUSE ALMONDS (U.S.)

- Bob’s Red Mill Natural Foods (U.S.)

- Grain-Free JK Gourmet (Canada)

- Nature’s Eats (U.S.)

- Nature's Choice Food (U.S.)

- Anthony's Goods (U.S.)

- Barney Butter (U.S.)

- Oleander Bio (South Africa)

- SHILOH FARMS (U.S.)

- King Arthur Baking Company, Inc (U.S.)

Latest Developments in Almond Flour Market

- In April 2025, Simple Mills expanded its almond flour-based product portfolio with the launch of new pancake and waffle mixes, strengthening its position in the clean-label breakfast segment. This development is impacting the market by accelerating consumer shift toward convenient gluten-free bakery solutions and increasing retail penetration of almond flour-based ready-to-use mixes. The launch is further intensifying competition among branded health food manufacturers focused on functional and nutrient-rich baking products

- In March 2025, Hodgson Mill introduced a new organic, non-GMO almond flour range targeting premium retail and e-commerce channels, reinforcing its presence in the specialty health food segment. This development is influencing the market by expanding the availability of certified organic almond flour products and strengthening consumer trust in clean-label sourcing. It is also pushing broader industry movement toward organic certification and differentiated premium product offerings

- In November 2024, Blue Diamond Growers expanded its almond processing and flour production capacity in California to address rising global demand from industrial bakery and packaged food manufacturers. This expansion is impacting the market by improving supply stability and reducing raw material constraints for large-scale almond flour users. It also reinforces Blue Diamond’s leadership position in the global almond ingredient supply chain through enhanced production efficiency

- In October 2024, Once Again Foods acquired Big Tree Organic Farms to strengthen its integrated organic almond supply and expand its almond-based ingredient portfolio, including almond flour. This acquisition is impacting the market by consolidating organic almond sourcing capabilities and enhancing downstream product development for clean-label and organic food manufacturers. It is also increasing competitive pressure among mid-sized organic ingredient producers

- In 2024, Blue Diamond Growers entered a sustainability partnership with Divert Inc. to convert almond processing byproducts into renewable energy, improving environmental efficiency across its almond ingredient operations. This initiative is influencing the market by increasing sustainability benchmarks within almond flour production and encouraging waste valorization practices across the industry. It also supports long-term ESG-driven differentiation among major almond ingredient producers

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Almond Flour Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Almond Flour Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Almond Flour Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.