Global Anal Cancer Market

Market Size in USD Billion

CAGR :

%

USD

1.02 Billion

USD

1.64 Billion

2025

2033

USD

1.02 Billion

USD

1.64 Billion

2025

2033

| 2026 –2033 | |

| USD 1.02 Billion | |

| USD 1.64 Billion | |

| % | |

|

Anal Cancer Market Size

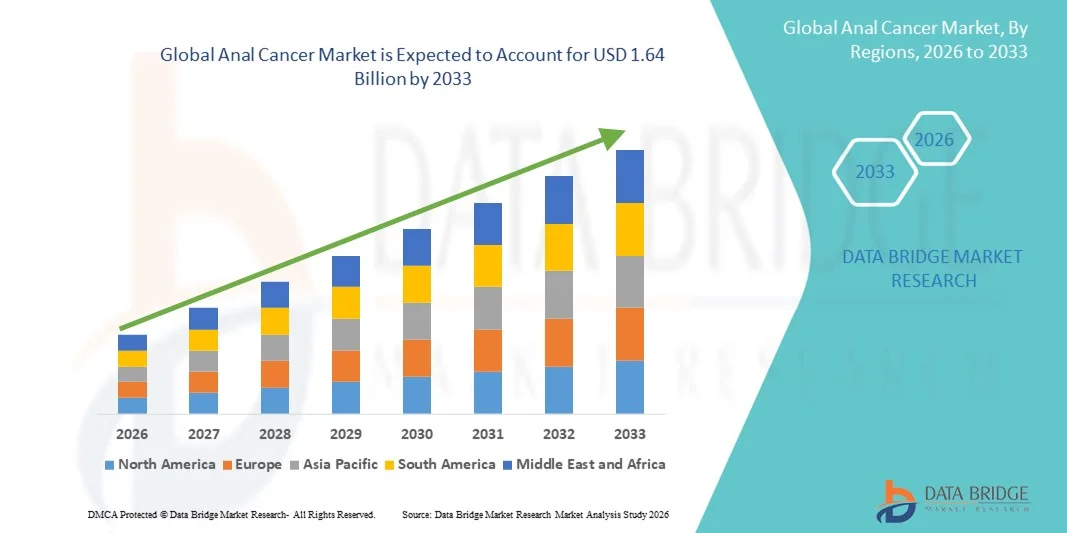

- The global anal cancer market size was valued at USD 1.02 billion in 2025 and is expected to reach USD 1.64 billion by 2033, at a CAGR of 6.17% during the forecast period

- The market growth is largely driven by the rising global incidence of anal cancer, particularly cases linked to human papillomavirus (HPV), increasing research and development activities, and the introduction of advanced diagnostic and therapeutic solutions that improve patient outcomes

- Furthermore, greater awareness of screening programs, expanding adoption of immunotherapies and targeted treatments, and enhanced healthcare infrastructure worldwide are increasing demand for effective anal cancer management. These converging factors are accelerating the uptake of innovative treatment options and supportive care, thereby significantly boosting the industry’s growth

Anal Cancer Market Analysis

- Anal cancer, a rare malignancy affecting the anal canal, is increasingly recognized as a critical area of oncology due to rising incidence rates linked to human papillomavirus (HPV) infection, immunocompromised populations, and lifestyle-related risk factors. Its management now involves advanced diagnostic, therapeutic, and targeted treatment options, improving survival and quality of life

- The escalating demand for effective anal cancer treatment is primarily fueled by growing awareness of early detection and screening programs, increased research in immunotherapies and targeted therapies, and rising healthcare expenditure in oncology care

- North America dominated the anal cancer market with a revenue share of 42.5% in 2025, attributed to early adoption of advanced treatment modalities, well-established healthcare infrastructure, and strong presence of key oncology drug manufacturers, with the U.S. witnessing substantial growth in patient access to HPV vaccines, immunotherapy treatments, and minimally invasive surgical options

- Asia-Pacific is expected to be the fastest growing region driven by increasing healthcare infrastructure, government initiatives for cancer screening, and rising awareness of HPV vaccination programs

- Chemotherapy segment dominated the market with a market share of 44.3% in 2025, driven by its established efficacy in treating advanced-stage anal cancer and integration with combination therapies that improve patient outcomes

Report Scope and Anal Cancer Market Segmentation

|

Attributes |

Anal Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Anal Cancer Market Trends

Advancement in Immunotherapy and Targeted Treatments

- A significant and accelerating trend in the global anal cancer market is the growing adoption of immunotherapy and targeted therapy regimens, which are improving survival rates and reducing side effects compared to traditional chemotherapy

- For instance, the combination of PD-1 inhibitors with chemotherapy has shown improved response rates in advanced anal cancer patients, offering new hope for those with limited treatment options

- Personalized medicine approaches, including genomic profiling and biomarker-driven therapies, are enabling oncologists to tailor treatments to individual patient profiles, enhancing efficacy and minimizing unnecessary toxicity

- The integration of immunotherapy and targeted therapy with conventional treatment protocols is increasingly standardizing care pathways, providing multi-modal treatment options that improve patient outcomes

- This trend towards precision oncology and immunotherapy-driven interventions is reshaping clinician and patient expectations, leading to increased demand for innovative treatment solutions

- Adoption of minimally invasive surgical techniques for early-stage anal cancer is rising, reducing recovery time and hospital stays, and complementing systemic therapies

- Integration of digital health platforms and tele-oncology services allows patients to monitor treatment progress and consult specialists remotely, improving adherence and accessibility

- The demand for novel, effective, and less toxic treatment options is growing rapidly across both developed and emerging markets, as healthcare providers aim to improve quality of life while managing treatment costs

Anal Cancer Market Dynamics

Driver

Rising HPV-Linked Anal Cancer Incidence and Awareness Programs

- The increasing prevalence of HPV-related anal cancer cases, coupled with greater awareness of screening programs, is a significant driver for the heightened demand for effective treatment options

- For instance, in March 2025, a public health initiative in North America expanded HPV vaccination coverage, directly impacting the early detection and prevention of anal cancer

- As awareness of risk factors and early symptoms improves, patients are more likely to seek timely medical care, boosting adoption of preventive, diagnostic, and therapeutic interventions

- Growing investments in oncology R&D and healthcare infrastructure, particularly in immunotherapy and targeted treatment development, are facilitating access to advanced treatment options

- The availability of multidisciplinary care teams, patient support programs, and clinical guidelines integrating new therapies enhances adoption, making these interventions more accessible and effective in both urban and semi-urban regions

- Increasing government funding for cancer screening and vaccination programs in emerging economies is driving early diagnosis, creating a larger patient pool for effective treatment

- Partnerships between pharmaceutical companies and research institutes to develop novel drugs and combination therapies are accelerating market growth and expanding treatment portfolios

Restraint/Challenge

High Treatment Costs and Limited Access in Developing Regions

- The high cost of immunotherapies, targeted therapies, and advanced diagnostic tools poses a significant challenge to broader market penetration, especially in developing countries

- For instance, limited availability of PD-1 inhibitors or targeted combination therapies in low-income regions restricts patient access to effective treatment options

- Ensuring equitable access requires significant investment in healthcare infrastructure, supply chains, and public health initiatives, which can be a barrier to rapid market expansion

- In addition, disparities in awareness about anal cancer screening and prevention programs contribute to delayed diagnosis, reducing the effectiveness of treatment interventions

- While some cost-reduction strategies, such as biosimilars and government subsidies, are emerging, affordability remains a critical concern, particularly for rural populations or uninsured patients

- Overcoming these challenges through policy support, insurance coverage, and regional healthcare capacity building will be vital for sustained growth in the anal cancer market

- Limited trained oncology specialists and inadequate hospital facilities in some regions restrict access to advanced therapies, slowing market adoption

- Regulatory hurdles and lengthy approval processes for novel immunotherapies or targeted drugs can delay patient access and affect market growth timelines

Anal Cancer Market Scope

The market is segmented on the basis of type, cancer type, treatment type, and end user.

- By Type

On the basis of type, the anal cancer market is segmented into fluorouracil, cisplatin, carboplatin, and other drugs. The Fluorouracil segment dominated the market with the largest market revenue share of 38.6% in 2025, driven by its long-standing clinical use and proven efficacy in combination chemotherapy regimens for anal cancer. Fluorouracil is widely preferred by oncologists due to its ability to effectively target rapidly dividing tumor cells while maintaining manageable side effects. The segment benefits from established clinical guidelines recommending Fluorouracil-based chemoradiation as a first-line treatment, particularly for squamous cell carcinoma. Hospitals and oncology centers often stock Fluorouracil due to its accessibility, cost-effectiveness, and compatibility with radiation therapy. Ongoing clinical trials continue to explore combination therapies involving Fluorouracil, further reinforcing its dominant position in the market.

The Cisplatin segment is expected to witness the fastest growth rate of 8.9% from 2026 to 2033, fueled by its rising use in combination therapies with radiation and immunotherapy for advanced-stage anal cancer. Cisplatin’s efficacy in improving treatment outcomes for high-risk patients, along with growing adoption in clinical protocols, is boosting its uptake. In addition, increasing awareness among oncologists regarding Cisplatin’s benefits in chemoradiation regimens is driving demand, particularly in North America and Europe. Emerging markets are also witnessing accelerated adoption due to ongoing efforts to expand oncology treatment infrastructure and access to advanced chemotherapy drugs.

- By Cancer Type

On the basis of cancer type, the anal cancer market is segmented into carcinoma in situ, squamous cell carcinoma, adenocarcinoma, basal cell carcinoma, melanoma, and others. The Squamous Cell Carcinoma (SCC) segment dominated the market with a revenue share of 61.2% in 2025, owing to its high prevalence among anal cancer patients. SCC is strongly associated with HPV infection, and treatment protocols for this subtype are well-established, including chemoradiation and targeted therapies. The segment’s dominance is further supported by screening programs and early detection initiatives that prioritize SCC due to its aggressive nature and higher treatment success rates when caught early. Hospitals and specialized oncology centers actively manage SCC cases, contributing to consistent demand for therapeutic drugs and supportive care. Clinical research continues to focus on improving SCC outcomes through immunotherapy and combination therapies, reinforcing its market leadership.

The Adenocarcinoma segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by growing awareness of its rising incidence in both developed and developing regions. Adenocarcinoma cases often require multimodal treatment, including surgery and chemotherapy, creating opportunities for novel therapeutics. Advancements in diagnostic imaging and molecular profiling allow for earlier detection, further fueling growth. The need for personalized treatment strategies and increasing adoption of targeted therapies is accelerating market penetration for this subtype.

- By Treatment Type

On the basis of treatment type, the anal cancer market is segmented into chemotherapy, surgery, radiation therapy, and immunotherapy. The Chemotherapy segment dominated the market with a revenue share of 44.3% in 2025, driven by its central role in standard treatment protocols for both early and advanced-stage anal cancer. Chemotherapy drugs such as Fluorouracil and Cisplatin are widely used in combination with radiation therapy to improve treatment efficacy and survival rates. Hospitals and cancer centers routinely administer chemotherapy due to its clinical efficacy and established guidelines. The segment benefits from ongoing clinical trials exploring combination regimens with immunotherapies, further solidifying its dominant market position. In addition, chemotherapy remains more accessible and cost-effective compared to newer therapies in many regions, reinforcing its wide adoption.

The Immunotherapy segment is expected to witness the fastest growth rate of 12.1% from 2026 to 2033, fueled by increasing approval of PD-1/PD-L1 inhibitors for advanced anal cancer and growing clinical evidence supporting their efficacy. Immunotherapy is increasingly used in patients with treatment-resistant or recurrent disease, creating high unmet demand. Rising investment in research and development, coupled with increasing patient awareness and insurance coverage in developed markets, is driving adoption. Healthcare providers are expanding immunotherapy programs to include combination therapies, further accelerating market growth.

- By End User

On the basis of end user, the anal cancer market is segmented into hospitals and clinics, long-term care centers, pharmacies, research and academic institutes, and others. The Hospitals and Clinics segment dominated the market with a revenue share of 52.3% in 2025, attributed to its central role in diagnosis, treatment, and post-therapy care for anal cancer patients. Hospitals provide comprehensive oncology services including chemotherapy, radiation, surgery, and supportive care, making them the primary point of treatment. The segment also benefits from large-scale adoption of advanced treatment protocols and multidisciplinary care teams. Frequent updates to clinical guidelines and the availability of specialized oncology units further reinforce hospital dominance. In addition, hospitals in North America and Europe have established extensive HPV vaccination and screening programs, contributing to consistent patient inflow.

The Research and Academic Institutes segment is expected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by increasing clinical trials, translational research, and development of novel therapies targeting anal cancer. Institutes are at the forefront of exploring immunotherapies, targeted drugs, and combination regimens, generating demand for research materials and experimental drugs. Rising collaborations between pharmaceutical companies and academic centers are accelerating innovation and clinical adoption. Government funding for cancer research, along with growing awareness of anal cancer epidemiology, is further supporting growth in this segment.

Anal Cancer Market Regional Analysis

- North America dominated the anal cancer market with a revenue share of 42.5% in 2025, attributed to early adoption of advanced treatment modalities, well-established healthcare infrastructure, and strong presence of key oncology drug manufacturers, with the U.S. witnessing substantial growth in patient access to HPV vaccines, immunotherapy treatments, and minimally invasive surgical options

- Patients and healthcare providers in the region prioritize early detection, advanced therapies, and access to immunotherapy and targeted treatments, contributing to the widespread adoption of effective anal cancer management solutions

- This strong market presence is further supported by government initiatives promoting HPV vaccination and screening programs, increasing awareness of risk factors, and growing investments in cancer research and clinical trials, establishing North America as a leading region in the anal cancer treatment landscape

U.S. Anal Cancer Market Insight

The U.S. anal cancer market captured the largest revenue share of 83% in 2025 within North America, driven by high prevalence of HPV-linked cases and widespread access to advanced oncology treatments. Patients increasingly prioritize early detection through screening programs and access to immunotherapy, chemotherapy, and targeted therapies. The growing awareness of preventive HPV vaccination, combined with well-established healthcare infrastructure, further propels the market. Moreover, the integration of multidisciplinary oncology care and clinical trial availability is significantly contributing to improved patient outcomes and treatment adoption.

Europe Anal Cancer Market Insight

The Europe anal cancer market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent cancer care guidelines, high healthcare expenditure, and the increasing need for effective treatment solutions. Rising urbanization and advanced hospital infrastructure are fostering the adoption of modern therapies such as chemoradiation and immunotherapy. European patients also value early detection and preventive measures, supported by national HPV vaccination programs. The region is witnessing growth across both public and private healthcare sectors, with hospitals and cancer centers actively incorporating novel treatment protocols.

U.K. Anal Cancer Market Insight

The U.K. anal cancer market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising awareness of HPV vaccination, preventive screening programs, and the increasing prevalence of anal cancer. Patients and clinicians are increasingly adopting immunotherapy and targeted therapies to improve outcomes, particularly for advanced-stage disease. The U.K.’s robust healthcare infrastructure, combined with strong government support for cancer prevention initiatives, is expected to continue stimulating market growth. Early diagnosis and patient education campaigns are also driving higher treatment adoption.

Germany Anal Cancer Market Insight

The Germany anal cancer market is expected to expand at a considerable CAGR during the forecast period, driven by increasing awareness of anal cancer risk factors, advanced diagnostic capabilities, and access to multimodal treatment options. Germany’s focus on innovation in oncology care, along with high healthcare expenditure, promotes adoption of targeted therapies and immunotherapy. Hospitals and specialized oncology centers are incorporating advanced treatment protocols, emphasizing personalized patient care. The emphasis on early detection and patient support programs aligns with local regulatory standards and contributes to steady market growth.

Asia-Pacific Anal Cancer Market Insight

The Asia-Pacific anal cancer market is poised to grow at the fastest CAGR of 9.1% during the forecast period of 2026 to 2033, driven by increasing healthcare infrastructure, rising awareness of HPV vaccination, and growing access to advanced cancer therapies in countries such as China, Japan, and India. Government initiatives promoting cancer screening and early detection are enhancing treatment uptake. Moreover, the expansion of oncology centers and improving reimbursement policies are making advanced treatments more accessible to patients. Increasing urbanization and rising disposable incomes are further supporting market growth across the region.

Japan Anal Cancer Market Insight

The Japan anal cancer market is gaining momentum due to the country’s high awareness of cancer prevention, advanced healthcare system, and increasing adoption of immunotherapy and targeted treatments. The Japanese market emphasizes early detection through national screening programs, while oncology centers are integrating personalized treatment approaches. The aging population is also likely to spur demand for effective, tolerable treatment options in both hospital and outpatient settings. Moreover, the integration of digital health platforms for patient monitoring is fueling growth in treatment adherence and outcomes.

India Anal Cancer Market Insight

The India anal cancer market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising HPV prevalence, expanding oncology infrastructure, and growing awareness of early detection programs. India’s healthcare system is rapidly upgrading to provide advanced treatments such as chemoradiation, immunotherapy, and targeted therapies. The increasing adoption of preventive HPV vaccination, combined with rising urbanization and a growing middle class, is driving treatment uptake. Government initiatives for cancer awareness and expansion of specialized cancer centers are key factors propelling market growth in India.

Anal Cancer Market Share

The Anal Cancer industry is primarily led by well-established companies, including:

- Incyte Corporation (U.S.)

- Merck & Co., Inc., (U.S.)

- Pfizer Inc. (U.S.)

- F. Hoffmann‑La Roche Ltd (Switzerland)

- Bristol‑Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Oncolytics Biotech Inc. (Canada)

- Antiva Biosciences, Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

What are the Recent Developments in Global Anal Cancer Market?

- In December 2025, the Japan Ministry of Health, Labour and Welfare (MHLW) approved Zynyz® (retifanlimab) in combination with carboplatin and paclitaxel as the first‑line treatment for advanced squamous cell carcinoma of the anal canal (SCAC) in Japan, providing a new standard of care for patients with advanced anal cancer in the Japanese market

- In October 2025, Oncolytics Biotech® reported updated clinical data from its ongoing GOBLET study showing that pelareorep in combination with the checkpoint inhibitor atezolizumab achieved an objective response rate (ORR) of 30% in second‑line or later metastatic squamous cell anal carcinoma (SCAC) patients, more than double the historic response rate of standard treatment, with several durable complete responses observed

- In May 2025, the U.S. Food and Drug Administration (FDA) approved retifanlimab‑dlwr (Zynyz) in combination with carboplatin and paclitaxel for the first‑line treatment of adults with inoperable locally recurrent or metastatic squamous cell carcinoma of the anal canal (SCAC), and also as a single‑agent for patients with disease progression or intolerance to platinum‑based chemotherapy, marking the first specific immunotherapy approved for advanced anal cancer in the U.S.

- In May 2025, results from the PLATO trial demonstrated a breakthrough in radiotherapy dosing for early‑stage anal cancer, showing that lower‑dose and shorter‑course radiotherapy resulted in higher complete cancer disappearance rates and fewer short‑term side effects compared with traditional regimens potentially changing clinical practice for radiation treatment worldwide

- In March 2025, researchers at MD Anderson Cancer Center identified potential biomarkers linked to longer survival in HPV‑positive metastatic anal cancer patients through analysis in a Phase II study of atezolizumab plus bevacizumab, offering insights that could inform future targeted immunotherapy strategies and personalized treatment approaches

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.