Global Angina Pectoris Drugs Market

Market Size in USD Billion

CAGR :

%

USD

11.14 Billion

USD

17.09 Billion

2025

2033

USD

11.14 Billion

USD

17.09 Billion

2025

2033

| 2026 –2033 | |

| USD 11.14 Billion | |

| USD 17.09 Billion | |

| % | |

|

Angina Pectoris Drugs Market Size

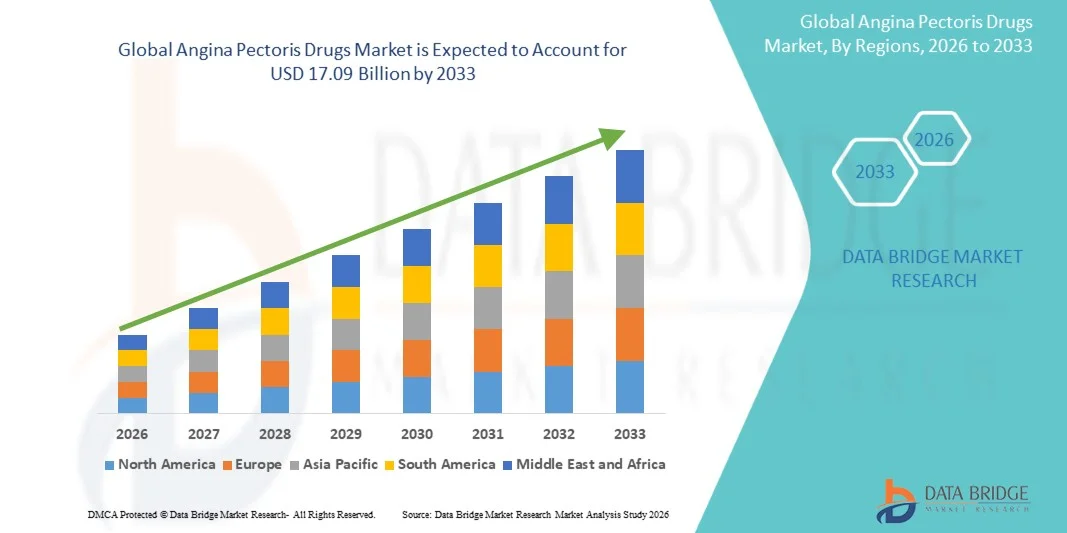

- The global angina pectoris drugs market size was valued at USD 11.14 billion in 2025 and is expected to reach USD 17.09 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases and increasing incidence of angina pectoris, driven by aging populations, sedentary lifestyles, and growing risk factors such as hypertension, diabetes, and obesity

- Furthermore, continuous advancements in anti-anginal therapies, expanding adoption of combination drug regimens, and improved access to cardiovascular care across both developed and emerging healthcare systems are supporting market expansion and strengthening treatment uptake in clinical practice

Angina Pectoris Drugs Market Analysis

- Angina pectoris drugs, primarily used to manage chest pain and improve myocardial oxygen supply-demand balance, are essential therapeutic agents in cardiovascular care, widely utilized in hospitals and outpatient settings for both chronic stable angina and acute coronary syndrome management due to their ability to reduce ischemic episodes and improve patient quality of life

- The escalating demand for angina pectoris drugs is primarily driven by the rising global burden of cardiovascular diseases, increasing prevalence of risk factors such as hypertension, diabetes, obesity, and smoking, along with a growing aging population more susceptible to coronary artery disorders

- North America dominated the angina pectoris drugs market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis and treatment rates, strong adoption of branded and novel anti-anginal therapies, and the presence of major pharmaceutical companies, with the U.S. accounting for significant drug utilization in both inpatient and outpatient cardiac care

- Asia-Pacific is expected to be the fastest growing region in the angina pectoris drugs market during the forecast period due to rising healthcare expenditure, improving access to cardiovascular treatments, increasing awareness of heart disease management, and rapid urbanization contributing to lifestyle-related cardiac risk factors

- The Beta-adrenergic Blocking Agents segment dominated the angina pectoris drugs market with the largest share of 41.8% in 2025, attributed to their strong clinical efficacy, cost-effectiveness, and widespread use as first-line therapy for reducing myocardial oxygen demand and preventing recurrent angina episodes

Report Scope and Angina Pectoris Drugs Market Segmentation

|

Attributes |

Angina Pectoris Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Angina Pectoris Drugs Market Trends

“Shift Toward Novel Mechanism-Based and Combination Anti-Anginal Therapies”

- A significant and accelerating trend in the global angina pectoris drugs market is the increasing focus on novel mechanism-based therapies and combination regimens that go beyond traditional nitrate and beta-blocker treatment to improve symptom control in refractory angina patients

- For instance, drugs such as ranolazine and ivabradine are increasingly being used as add-on therapies in patients who remain symptomatic despite standard treatment, helping improve exercise tolerance and reduce angina frequency without significantly affecting heart rate or blood pressure

- Advancements in cardiovascular pharmacology are enabling more targeted modulation of myocardial oxygen demand and coronary blood flow, with newer therapeutic approaches focusing on metabolic pathways and late sodium current inhibition to improve ischemic efficiency

- Furthermore, fixed-dose combination therapies are gaining traction as they enhance patient adherence, simplify treatment regimens, and provide synergistic benefits in long-term angina management, particularly in elderly patients with comorbidities

- Growing integration of digital health monitoring tools and cardiac wearables is supporting better disease management by enabling real-time symptom tracking and medication optimization in angina patients

- This trend toward more personalized and mechanism-diverse treatment strategies is reshaping clinical practice, with pharmaceutical companies increasingly investing in R&D for next-generation anti-anginal agents and improved drug delivery formulations

- The growing demand for safer, more effective, and long-acting angina therapies is rapidly increasing across both developed and emerging healthcare markets, as clinicians prioritize optimized symptom control and improved cardiovascular outcomes

Angina Pectoris Drugs Market Dynamics

Driver

“Rising Global Cardiovascular Disease Burden and Expanding Treatment Access”

- The increasing prevalence of cardiovascular diseases, particularly coronary artery disease and angina pectoris, combined with a growing aging population, is a major driver fueling demand for angina pectoris drugs globally

- For instance, in 2025, healthcare systems across multiple regions have reported a steady rise in outpatient and emergency visits linked to ischemic heart disease, leading to higher prescription rates for anti-anginal medications in both hospital and ambulatory care settings

- As awareness of early diagnosis and long-term management of angina improves, more patients are being initiated on pharmacological therapies such as beta-blockers, calcium channel blockers, and nitrates to prevent disease progression and complications

- Furthermore, expanding healthcare infrastructure in emerging economies and improved reimbursement coverage for cardiovascular treatments are increasing patient access to essential angina medications

- The availability of generic drug alternatives and inclusion of essential cardiovascular medicines in national healthcare programs are further accelerating treatment adoption across diverse patient populations

- Rising adoption of preventive cardiology and routine cardiovascular screening programs is also contributing to earlier detection and higher prescription volumes of angina-related therapies

- Increasing collaboration between pharmaceutical companies and healthcare providers for awareness campaigns is further improving diagnosis rates and treatment initiation in high-risk populations

Restraint/Challenge

“Adverse Effects, Drug Tolerance, and Treatment Compliance Limitations”

- Despite strong demand, the angina pectoris drugs market faces challenges related to drug-related side effects, tolerance development (especially with long-term nitrate use), and patient non-compliance, which can reduce overall treatment effectiveness

- For instance, prolonged nitrate therapy may lead to tolerance, requiring nitrate-free intervals and careful dose management, which can complicate long-term treatment adherence in chronic angina patients

- In addition, side effects such as hypotension, dizziness, and fatigue associated with beta-blockers and calcium channel blockers can lead to discontinuation or dose adjustment in sensitive patient groups

- The chronic nature of angina management requires lifelong medication adherence, but patients often struggle with consistent drug intake due to symptom variability and polypharmacy burden in elderly populations

- Furthermore, variability in treatment response and the need for individualized therapy selection increase complexity for clinicians, particularly in patients with multiple comorbid conditions

- Limited patient awareness in developing regions about long-term disease management often results in delayed treatment continuation and suboptimal therapeutic outcomes

- Stringent regulatory requirements and lengthy approval timelines for novel anti-anginal drugs can also delay market entry of advanced therapies, restricting innovation-driven growth

- Addressing these challenges through improved drug formulations, patient education, and development of better-tolerated therapies will be critical for sustaining long-term market growth

Angina Pectoris Drugs Market Scope

The market is segmented on the basis of type, drug class, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the angina pectoris drugs market is segmented into stable angina, unstable angina, and Prinzmetal’s (variant) angina. The stable angina segment dominated the market with the largest revenue share of 52.4% in 2025, driven by its high global prevalence among patients with chronic coronary artery disease and long-term cardiovascular risk factors such as hypertension, diabetes, and hyperlipidemia. Stable angina is typically managed through long-term pharmacological therapy, leading to consistent and sustained drug demand across outpatient and hospital settings. The segment also benefits from well-established treatment protocols involving beta-blockers, nitrates, and calcium channel blockers, ensuring widespread clinical adoption.

The unstable angina segment is expected to witness the fastest growth rate of 7.9% during 2026–2033, driven by increasing incidence of acute coronary syndromes requiring emergency medical intervention. Rising hospital admissions due to sudden cardiac events and improved diagnostic capabilities in emergency care settings are significantly boosting drug utilization. The segment is also supported by growing use of antiplatelet agents and anticoagulants in acute management protocols. Expanding cardiovascular emergency infrastructure in emerging economies further accelerates treatment adoption. In addition, increased awareness of early symptom recognition is leading to faster hospital visits and timely pharmacological intervention.

- By Drugs

On the basis of drug class, the market is segmented into nitrates, antiplatelet agents, beta-adrenergic blocking agents, calcium channel blockers, anti-ischemic agents, statins, antihypertensive agents, and others. The beta-adrenergic blocking agents segment dominated the market with the largest revenue share of 41.8% in 2025, owing to their strong clinical efficacy as first-line therapy in reducing myocardial oxygen demand and preventing recurrent angina episodes. These drugs are widely prescribed across both chronic and acute care settings due to their proven mortality and morbidity benefits in cardiovascular disease management. Their cost-effectiveness and inclusion in standard treatment guidelines further reinforce dominance.

The anti-ischemic agents segment is expected to witness the fastest growth rate of 8.3% during 2026–2033, driven by increasing adoption of newer therapies such as ranolazine that target cellular energy metabolism and ischemic pathways. These drugs are gaining traction in patients with refractory angina who do not respond adequately to traditional therapies. Growing clinical preference for mechanism-based treatment approaches is further supporting demand. Rising R&D investment in novel anti-anginal agents is expanding the pipeline of advanced therapies. In addition, improved guideline recommendations for combination therapy are accelerating adoption in both developed and emerging healthcare markets.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, transdermal, and others. The oral segment dominated the market with the largest revenue share of 67.5% in 2025, driven by its ease of administration, high patient compliance, and suitability for long-term chronic therapy. Most first-line angina drugs such as beta-blockers, nitrates, and calcium channel blockers are available in oral formulations, making this route the standard in outpatient management. Oral drugs are also preferred due to lower cost and wide availability of generic formulations.

The transdermal segment is expected to witness the fastest growth rate of 7.6% during 2026–2033, driven by increasing use of nitroglycerin patches for controlled and sustained drug release. Transdermal delivery offers improved patient compliance by reducing dosing frequency and minimizing gastrointestinal side effects. It is particularly beneficial for elderly patients with swallowing difficulties. Growing preference for non-invasive drug delivery systems is further supporting adoption. In addition, advancements in patch technology enabling better absorption and controlled dosing are accelerating market growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share of 48.9% in 2025, due to the high volume of acute angina cases and emergency cardiovascular admissions requiring immediate pharmacological intervention. Hospitals serve as the primary point of diagnosis and treatment initiation, especially for unstable angina and high-risk patients. Availability of advanced cardiac monitoring systems and specialist care further supports drug utilization.

The homecare segment is expected to witness the fastest growth rate of 9.1% during 2026–2033, driven by increasing preference for long-term chronic disease management at home and rising adoption of oral maintenance therapies. Growing aging population and expansion of remote patient monitoring systems are further supporting this shift. Patients increasingly prefer home-based care due to convenience and reduced hospitalization costs. Advancements in telecardiology and digital health tools are enabling better adherence and monitoring. In addition, rising availability of prescription refills via digital pharmacies is boosting homecare adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share of 46.3% in 2025, driven by high prescription volumes from inpatient and emergency care settings. Hospital pharmacies play a critical role in dispensing acute care medications for unstable angina and post-cardiac events. Their integration with hospital treatment protocols ensures immediate drug availability.

The online pharmacy segment is expected to witness the fastest growth rate of 10.4% during 2026–2033, driven by increasing digitalization of healthcare and rising demand for convenient home delivery of chronic disease medications. Patients with stable angina increasingly prefer online platforms for regular prescription refills. Expansion of e-prescription systems and telemedicine consultations is further accelerating adoption. Growing smartphone penetration and digital payment systems support market growth. In addition, discounts and subscription-based medicine delivery models are enhancing patient adherence and boosting online pharmacy penetration.

Angina Pectoris Drugs Market Regional Analysis

- North America dominated the angina pectoris drugs market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis and treatment rates, strong adoption of branded and novel anti-anginal therapies

- Patients in the region benefit from early disease detection, high prescription rates of anti-anginal therapies, and strong adoption of both branded and generic cardiovascular drugs across hospital and outpatient settings

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage, and the presence of leading pharmaceutical companies, making angina pectoris drugs a standard component of long-term cardiac care management

U.S. Angina Pectoris Drugs Market Insight

The U.S. angina pectoris drugs market captured the largest revenue share of 81% in North America in 2025, fueled by the high prevalence of coronary artery disease and the rapid adoption of advanced cardiovascular therapies. Patients are increasingly prioritizing effective long-term management of angina through evidence-based pharmacological treatments and early diagnosis. The growing preference for guideline-directed therapy, combined with strong demand for combination drug regimens and novel anti-ischemic agents, further propels the market. Moreover, the increasing integration of preventive cardiology programs and digital health monitoring is significantly contributing to market expansion.

Europe Angina Pectoris Drugs Market Insight

The Europe angina pectoris drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by a high burden of ischemic heart disease and stringent healthcare policies supporting cardiovascular treatment access. The increase in aging population, coupled with rising awareness of early disease management, is fostering the adoption of angina drugs. European healthcare systems are also focused on cost-effective treatment approaches, encouraging widespread use of generic beta-blockers, nitrates, and calcium channel blockers. The region is experiencing steady growth across hospital and outpatient care settings, with angina therapies being widely integrated into chronic disease management programs.

U.K. Angina Pectoris Drugs Market Insight

The U.K. angina pectoris drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing incidence of coronary artery disease and strong emphasis on early diagnosis and preventive care. In addition, rising awareness of cardiovascular health and structured prescribing practices under the NHS are encouraging consistent use of standard anti-anginal therapies. The UK’s strong healthcare accessibility and growing outpatient management programs are expected to continue to stimulate market growth.

Germany Angina Pectoris Drugs Market Insight

The Germany angina pectoris drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by a high prevalence of cardiovascular conditions and strong focus on advanced clinical treatment standards. Germany’s well-developed healthcare infrastructure and strong pharmaceutical production base ensure steady availability of both branded and generic angina drugs. The integration of innovative treatment approaches and emphasis on long-term disease management are also supporting adoption of combination and anti-ischemic therapies.

Asia-Pacific Angina Pectoris Drugs Market Insight

The Asia-Pacific angina pectoris drugs market is poised to grow at the fastest CAGR of 8.9% during the forecast period of 2026 to 2033, driven by rising cardiovascular disease burden, rapid urbanization, and improving healthcare access across emerging economies. Increasing awareness of heart disease management and expanding availability of affordable generic drugs are significantly boosting treatment adoption in the region. Government initiatives promoting healthcare infrastructure development and preventive cardiology programs are further supporting market expansion.

Japan Angina Pectoris Drugs Market Insight

The Japan angina pectoris drugs market is gaining momentum due to the country’s rapidly aging population, high healthcare standards, and strong focus on cardiovascular disease management. The market is driven by widespread adoption of advanced anti-anginal therapies and combination drug regimens supported by universal healthcare coverage. Integration of precision medicine and continuous patient monitoring is further enhancing treatment adherence and improving clinical outcomes.

India Angina Pectoris Drugs Market Insight

The India angina pectoris drugs market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to a rapidly growing patient pool, increasing prevalence of cardiovascular diseases, and improving healthcare access. Expanding middle-class population, rising awareness of heart health, and strong demand for affordable generic cardiovascular drugs are key factors driving market growth. Government initiatives supporting preventive healthcare and expanding healthcare infrastructure are further accelerating diagnosis rates and drug utilization in the country.

Angina Pectoris Drugs Market Share

The Angina Pectoris Drugs industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- AstraZeneca (U.K.)

- Sanofi (France)

- Merck & Co., Inc. (U.S.)

- GSK plc (U.K.)

- Eli Lilly and Company (U.S.)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Abbott (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Servier (France)

- Viatris Inc. (U.S.)

What are the Recent Developments in Global Angina Pectoris Drugs Market?

- In June 2025, a cardiovascular pharmacology study reported that ranolazine showed additional pleiotropic effects beyond angina relief, including antioxidant and anti-ischemic activity, supporting its continued investigation as a multi-benefit therapy in chronic coronary syndromes and angina management

- In March 2025, a comprehensive clinical review highlighted that ranolazine remains a key second-line therapy for chronic stable angina, particularly in patients who remain symptomatic despite beta-blockers and calcium channel blockers, reinforcing its continued clinical relevance in guideline-based management of refractory angina symptoms

- In February 2025, a pharmacology research update reported that ivabradine, ranolazine, and trimetazidine continue to be widely studied as add-on antianginal therapies, especially for patients with microvascular or non-obstructive coronary artery disease where traditional revascularization strategies are less effective

- In January 2025, emerging clinical evidence published in cardiovascular journals highlighted expanded investigational interest in ranolazine beyond symptom control, including potential anti-arrhythmic benefits in chronic coronary syndrome patients, reinforcing its evolving therapeutic profile in angina management

- In October 2024, a comparative clinical study showed that ranolazine demonstrated superior improvement in exercise tolerance and quality-of-life scores compared to trimetazidine in patients with stable angina, supporting its growing preference as an add-on therapy in symptomatic coronary artery disease management

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.