Global Anti Ship Missile Defense System Market

Market Size in USD Billion

CAGR :

%

USD

97.42 Billion

USD

153.75 Billion

2025

2033

USD

97.42 Billion

USD

153.75 Billion

2025

2033

| 2026 –2033 | |

| USD 97.42 Billion | |

| USD 153.75 Billion | |

| % | |

|

Anti-Ship Missile Defense System Market Size

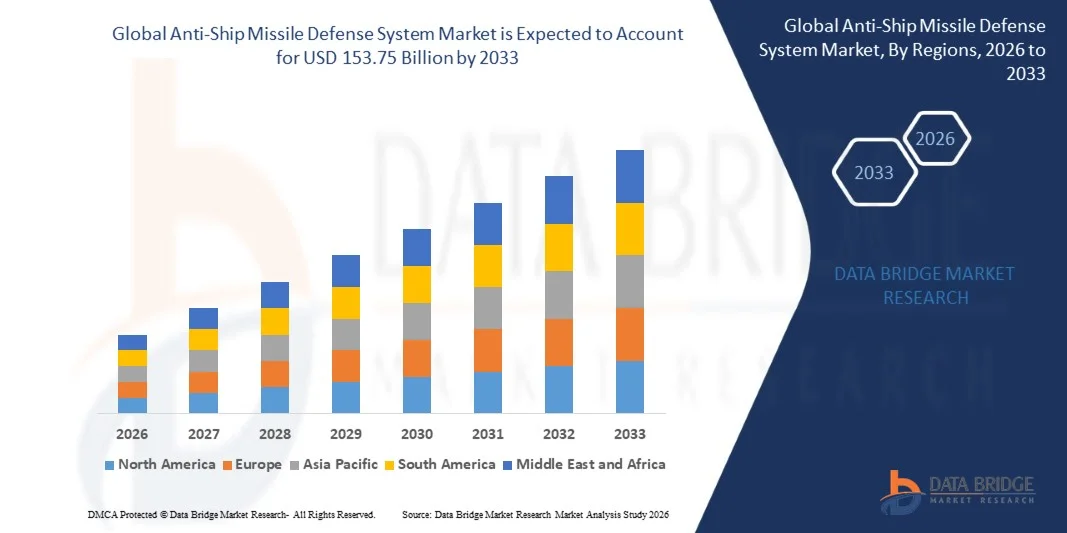

- The global anti-ship missile defense system market size was valued at USD 97.42 billion in 2025 and is expected to reach USD 153.75 billion by 2033, at a CAGR of 5.87% during the forecast period

- The market growth is largely fuelled by the increasing naval modernization programs across major economies, with countries upgrading their fleets to incorporate advanced missile defense capabilities

- Rising geopolitical tensions and maritime security concerns are driving defense spending, as nations prioritize safeguarding strategic sea lanes and territorial waters

Anti-Ship Missile Defense System Market Analysis

- Growing demand for multi-layered naval defense systems among naval forces, including surface-to-air missiles, close-in weapon systems, and electronic countermeasures for comprehensive protection

- Shift towards integrated network-centric defense solutions for real-time threat response, enabling faster communication between ships, sensors, and command centers

- North America dominated the anti-ship missile defense system market with the largest revenue share of 38.50% in 2025, driven by increasing defense budgets, modernization of naval fleets, and growing concerns over maritime security.

- Asia-Pacific region is expected to witness the highest growth rate in the global anti-ship missile defense system market, driven by rising defense budgets, expanding naval fleets, and increasing geopolitical tensions in strategic maritime zones. Countries such as China, Japan, India, and South Korea are adopting advanced radar, missile interceptors, and networked command systems to strengthen regional maritime security

- The radar segment held the largest market revenue share in 2025, owing to its critical role in detecting, tracking, and providing early warning of incoming missile threats. Advanced radar systems enable real-time threat assessment, target prioritization, and integration with missile interceptors, enhancing situational awareness for naval forces. These systems are increasingly being upgraded with phased-array, 3D, and AI-assisted technologies to improve detection accuracy, reduce response time, and counter evolving supersonic and hypersonic threats. Continuous R&D and investments in radar innovation are further driving adoption across major naval fleets globally

Report Scope and Anti-Ship Missile Defense System Market Segmentation

|

Attributes |

Anti-Ship Missile Defense System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• MBDA Inc. (France) |

|

Market Opportunities |

• Rising Adoption Of Autonomous Naval Defense Systems |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Anti-Ship Missile Defense System Market Trends

“Increasing Demand for Advanced Naval Defense Capabilities”

• Growing geopolitical tensions and rising maritime security threats are significantly shaping the anti-ship missile defense system market, as countries increasingly invest in modern naval assets to protect strategic sea lanes and territorial waters. Modernization programs focus on integrating advanced radar, missile interception, and electronic warfare technologies to enhance fleet survivability

• Expansion of naval fleets in Asia-Pacific, Europe, and the Middle East has accelerated demand for multi-layered defense systems capable of countering advanced anti-ship missile threats. Countries are adopting a combination of surface-to-air missiles, close-in weapon systems, and directed-energy solutions to strengthen naval defense posture

• Technological innovation in radar, tracking, and interception systems is driving adoption, with new solutions offering higher accuracy, faster response times, and enhanced threat detection. Integration with network-centric command and control systems enables real-time situational awareness and coordinated defense across multiple platforms

• For instance, in 2024, the U.S. and France expanded naval defense programs by deploying next-generation missile defense systems on destroyers and frigates. These deployments were aimed at countering emerging supersonic and hypersonic missile threats, with testing and operational exercises conducted across strategic maritime regions

• While the demand for advanced anti-ship missile defense systems is growing, sustained market expansion depends on continuous R&D, cost-effective production, and seamless integration with existing naval platforms. Manufacturers are also focusing on reliability, interoperability, and lifecycle support to meet evolving defense requirements

Anti-Ship Missile Defense System Market Dynamics

Driver

“Rising Geopolitical Tensions And Naval Modernization Programs”

• Increasing geopolitical tensions across key maritime regions, including the South China Sea, Persian Gulf, and Eastern Mediterranean, are driving defense budgets and prioritization of advanced missile defense systems. Nations are upgrading older naval platforms and commissioning new vessels with integrated defense capabilities to ensure strategic deterrence

• Growing naval modernization programs focus on multi-layered defense strategies, incorporating advanced radar, anti-missile interceptors, electronic countermeasures, and integrated command-and-control systems. These programs aim to enhance fleet survivability and operational readiness in high-threat environments

• Defense manufacturers are investing heavily in R&D to develop next-generation missile detection and interception technologies, including AI-assisted tracking, networked sensor integration, and long-range guided interceptors. Collaboration with naval forces enables customized solutions tailored to specific threat scenarios

• For example, in 2023, India and Japan reported accelerated deployment of advanced missile defense systems on destroyers and corvettes. These initiatives were aimed at strengthening maritime deterrence and enhancing interoperability with allied naval forces, supporting broader strategic objectives

• Although modernization and security concerns support market growth, wider adoption depends on procurement budgets, technological sophistication, and geopolitical stability. Efficient integration with existing fleets, along with cost optimization, will be critical for meeting defense requirements and ensuring operational effectiveness

Restraint/Challenge

“High Cost And Complex Integration Requirements”

• The relatively high cost of advanced anti-ship missile defense systems remains a key challenge, limiting adoption among nations with constrained defense budgets. Expenditure includes R&D, procurement, platform integration, and long-term maintenance, making investment decisions highly strategic

• Complex system integration with existing naval vessels and networked command structures can create operational challenges. Ensuring seamless interoperability between sensors, interceptors, and onboard systems requires extensive testing and engineering expertise

• Supply chain and manufacturing constraints also impact market growth, as advanced components require precision engineering and certified suppliers. Delays in production, technology transfer restrictions, and quality compliance issues can further affect deployment timelines

• For instance, in 2024, several Southeast Asian and Middle Eastern countries faced delays in commissioning advanced missile defense systems due to high costs, integration challenges, and limited local expertise. These issues affected fleet readiness and prompted phased deployment strategies

• Overcoming these challenges will require cost-effective production, robust supplier networks, and skilled personnel for integration and maintenance. Collaboration with allied nations, joint development programs, and modular system designs can help unlock the long-term growth potential of the global anti-ship missile defense system market

Anti-Ship Missile Defense System Market Scope

The market is segmented on the basis of component, launch platform, application, and end use.

• By Component

On the basis of component, the anti-ship missile defense system market is segmented into radar and missile interceptors. The radar segment held the largest market revenue share in 2025, owing to its critical role in detecting, tracking, and providing early warning of incoming missile threats. Advanced radar systems enable real-time threat assessment, target prioritization, and integration with missile interceptors, enhancing situational awareness for naval forces. These systems are increasingly being upgraded with phased-array, 3D, and AI-assisted technologies to improve detection accuracy, reduce response time, and counter evolving supersonic and hypersonic threats. Continuous R&D and investments in radar innovation are further driving adoption across major naval fleets globally.

The missile interceptor segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing need for multi-layered defense against advanced anti-ship missiles. Missile interceptors are designed to directly neutralize threats at varying ranges, often operating in conjunction with radar systems for precision targeting. Technological advancements in guidance, propulsion, and warhead design have enhanced interception success rates, making these systems crucial for high-threat maritime regions. Rising geopolitical tensions and expansion of naval capabilities are expected to further fuel the demand for missile interceptors.

• By Launch Platform

On the basis of launch platform, the market is segmented into air, surface, and submarine. The surface platform segment held the largest market share in 2025 due to its wide deployment across destroyers, frigates, and corvettes, which serve as primary combat vessels in most navies. Surface-based systems provide operational flexibility, rapid response, and integration with onboard sensors and command systems. Advancements in modular and multi-layered defense architectures have further increased the efficiency of surface-launched systems, enabling simultaneous tracking and interception of multiple threats. Investments in fleet modernization programs are anticipated to sustain the growth of surface-based anti-ship defense platforms.

The air-launched segment is projected to witness rapid growth from 2026 to 2033, driven by its ability to extend engagement range and provide rapid interception of anti-ship threats before they approach naval formations. Air-launched defense systems are increasingly integrated with fighter aircraft, UAVs, and helicopters to enhance mobility and provide strategic coverage beyond the immediate maritime perimeter. This segment benefits from advances in missile miniaturization, propulsion, and guidance systems, which improve speed, accuracy, and operational flexibility. Growing adoption in allied and emerging naval forces is expected to accelerate market growth.

• By Application

On the basis of application, the market is segmented into ballistic missile defense and conventional missile defense. The conventional missile defense segment held the largest market share in 2025, supported by the widespread threat of anti-ship cruise missiles, supersonic, and subsonic missiles in tactical maritime operations. Conventional systems are deployed to protect naval assets during close- to medium-range engagements and are widely used in high-threat scenarios. Advancements in interception accuracy, multi-target handling, and integration with shipboard defense systems are enhancing system effectiveness. Increasing fleet expansions and regional maritime security concerns are expected to maintain the dominance of conventional missile defense applications.

The ballistic missile defense segment is expected to witness the fastest growth from 2026 to 2033, driven by the rising need to counter long-range, high-speed ballistic missile threats. These systems rely on advanced detection, guidance, and interception technologies to neutralize incoming missiles at high altitudes and extended ranges. Investments in AI-based targeting, improved propulsion, and kinetic interception technologies are supporting the rapid adoption of ballistic missile defense solutions. Navies across Europe, Asia-Pacific, and the Middle East are increasingly incorporating these capabilities into modern multi-layered defense architectures to ensure strategic deterrence.

• By End Use

On the basis of end use, the market is segmented into weapon guidance and detection. The detection segment held the largest revenue share in 2025, owing to its vital role in early threat identification, situational awareness, and coordinated defense. Detection systems integrate advanced radar, sonar, and electronic surveillance capabilities to monitor maritime threats continuously and provide real-time data for decision-making. Upgrades in AI-assisted analytics, sensor fusion, and long-range monitoring have enhanced detection accuracy and reduced response times. Adoption of networked detection systems enables seamless communication with interceptors, command centers, and allied naval forces.

The weapon guidance segment is projected to witness rapid growth from 2026 to 2033, fueled by technological advancements in missile targeting, AI-assisted interception, and precision guidance. Effective weapon guidance ensures accurate neutralization of incoming threats, improving the overall efficiency and reliability of anti-ship missile defense systems. Continuous R&D efforts in navigation, seeker technology, and propulsion systems are enhancing targeting performance across diverse operational conditions. Growing demand for highly precise, rapid-response defense solutions among modern naval fleets is expected to drive market expansion in this segment.

Anti-Ship Missile Defense System Market Regional Analysis

• North America dominated the anti-ship missile defense system market with the largest revenue share of 38.50% in 2025, driven by increasing defense budgets, modernization of naval fleets, and growing concerns over maritime security.

• The U.S. and Canada prioritize upgrading surface ships, submarines, and aircraft with advanced radar, missile interceptors, and integrated command systems to strengthen deterrence against emerging threats.

• High investment in R&D, advanced manufacturing capabilities, and collaborations between defense contractors and the military support widespread adoption, making North America a key market for anti-ship missile defense solutions.

U.S. Anti-Ship Missile Defense System Market Insight

The U.S. anti-ship missile defense system market captured the largest revenue share in 2025 within North America, fueled by ongoing naval modernization programs and the rapid deployment of multi-layered missile defense architectures. Advanced systems integrating radar, missile interceptors, and AI-assisted targeting enhance operational readiness against both conventional and ballistic threats. Rising investments in fleet expansion, ship retrofitting, and development of next-generation defense technologies further strengthen the market. Government contracts and strategic alliances with leading defense manufacturers are driving procurement and long-term adoption.

Europe Anti-Ship Missile Defense System Market Insight

The Europe market is expected to witness significant growth from 2026 to 2033, primarily driven by regional security concerns, increasing naval modernization programs, and the need to counter advanced anti-ship missile threats. Countries such as France, Germany, and Italy are upgrading existing naval assets with integrated radar and interceptor systems to ensure fleet survivability. In addition, European nations are investing in AI-assisted detection, electronic warfare solutions, and interoperability enhancements to maintain operational superiority. Rising geopolitical tensions and focus on joint naval defense exercises are expected to accelerate market adoption.

U.K. Anti-Ship Missile Defense System Market Insight

The U.K. anti-ship missile defense system market is projected to witness strong growth from 2026 to 2033, driven by modernization of the Royal Navy and a focus on protecting territorial waters and overseas maritime assets. Programs aimed at upgrading destroyers, frigates, and submarines with advanced radar, missile interceptors, and weapon guidance systems are a key factor supporting demand. In addition, integration with NATO-led command networks and focus on multi-layered defense strategies is fueling adoption in both conventional and ballistic missile defense applications.

Germany Anti-Ship Missile Defense System Market Insight

The Germany market is expected to witness significant growth from 2026 to 2033, fueled by increasing awareness of maritime security threats and ongoing fleet modernization initiatives. German naval forces are investing in next-generation radar, missile interceptors, and detection systems to enhance operational readiness. The emphasis on technology-driven, eco-conscious, and highly precise defense solutions is promoting adoption in both military and allied fleet operations. Integration with European joint defense programs and network-centric command systems further enhances system effectiveness.

Asia-Pacific Anti-Ship Missile Defense System Market Insight

The Asia-Pacific market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing defense budgets, rapid naval expansion, and heightened geopolitical tensions in regions such as the South China Sea and the Indo-Pacific. Countries including China, India, Japan, and South Korea are deploying advanced radar, missile interceptors, and networked command systems to strengthen maritime security. In addition, local manufacturing capabilities, government defense initiatives, and adoption of AI-assisted detection technologies are contributing to rapid market expansion.

Japan Anti-Ship Missile Defense System Market Insight

The Japan market is expected to witness strong growth from 2026 to 2033, fueled by the country’s focus on strengthening its Self-Defense Forces and protecting key maritime trade routes. Modernization programs include deploying advanced radar systems, air-launched interceptors, and integrated fleet defense networks. The rising adoption of smart, networked naval platforms and increasing investments in indigenous missile defense technologies are driving market growth. Heightened security concerns and ongoing collaboration with allied navies further support demand.

China Anti-Ship Missile Defense System Market Insight

The China market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapid naval modernization, expanding fleet, and increasing focus on maritime security. China is investing in next-generation radar, missile interceptors, and submarine-launched defense systems to enhance operational capabilities. Government-backed R&D initiatives, strong domestic defense manufacturing, and the integration of AI-assisted targeting and networked command systems are key factors propelling market growth. The strategic development of multi-layered anti-ship missile defense architectures is expected to sustain the market’s expansion.

Anti-Ship Missile Defense System Market Share

The Anti-Ship Missile Defense System industry is primarily led by well-established companies, including:

• MBDA Inc. (France)

• General Dynamics Corporation (U.S.)

• BAE Systems (U.K.)

• Boeing (U.S.)

• L3Harris Technologies, Inc. (U.S.)

• Thales Group (France)

• Textron Inc. (U.S.)

• Rheinmetall AG (Germany)

• Alliant Techsystems (U.S.)

• IAI – Israel Aerospace Industries (Israel)

• Denel Dynamics (South Africa)

• Northrop Grumman (U.S.)

• Saab (Sweden)

• Airbus S.A.S. (France)

• Aselsan (Turkey)

• Rafael Advanced Defense Systems Ltd. (Israel)

• Diehl Stiftung & Co. KG (Germany)

• Leonardo (Italy)

• Lockheed Martin Corporation (U.S.)

• Raytheon Technologies Corporation (U.S.)

Latest Developments in Global Anti-Ship Missile Defense System Market

- In August 2022, BrahMos Aerospace Private Ltd signed a contract with the Philippines to supply anti-ship versions of the BrahMos supersonic cruise missile. This $375 million deal marked the missile’s first export purchase, strengthening the Philippines’ maritime defense capabilities. The contract is expected to enhance regional naval security and boost demand for advanced supersonic missile systems, driving growth in the export segment of the anti-ship missile defense market

- In April 2022, Raytheon Missiles and Defense secured a USD 972 million contract with the U.S. Air Force, U.S. Navy, and militaries of 19 other nations, including the U.K., Australia, Italy, Saudi Arabia, and Japan, to supply AMRAAMs. The contract covers AIM-120D3 and AIM-120C8 variants with upgraded guidance systems (F3R), enhancing missile accuracy and effectiveness against advanced threats. This development strengthens multi-national air defense capabilities and underscores growing global demand for precision-guided missile systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.