Global Apheresis Market

Market Size in USD Billion

CAGR :

%

USD

2.20 Billion

USD

4.36 Billion

2025

2033

USD

2.20 Billion

USD

4.36 Billion

2025

2033

| 2026 –2033 | |

| USD 2.20 Billion | |

| USD 4.36 Billion | |

| % | |

|

Apheresis Market Size

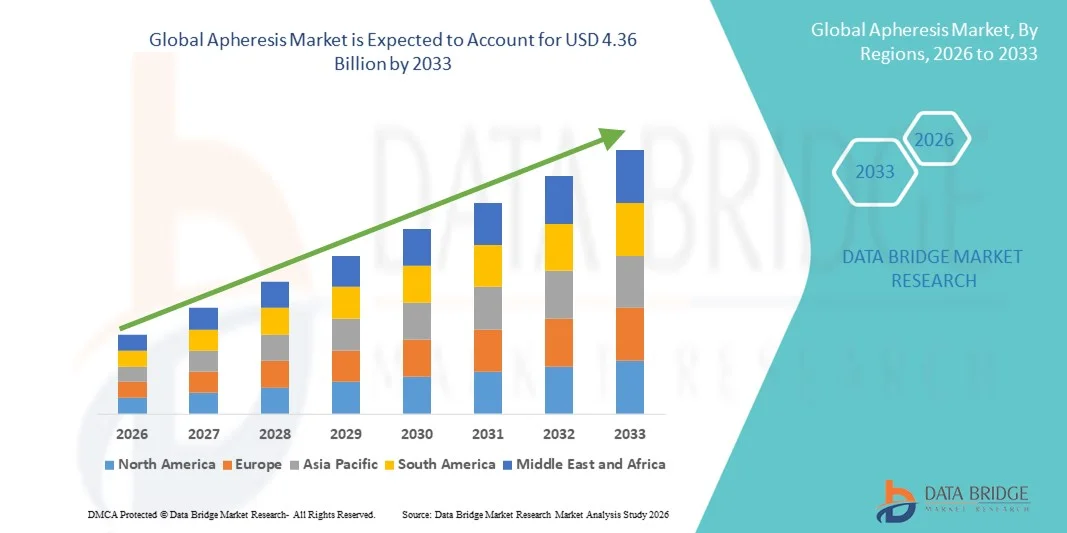

- The global Apheresis market size was valued at USD 2.20 billion in 2025 and is expected to reach USD 4.36 billion by 2033, at a CAGR of 8.95% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases and the increasing demand for advanced blood component separation procedures in healthcare settings. The growing need for effective treatments for conditions such as autoimmune disorders, hematological diseases, and neurological disorders is encouraging the adoption of apheresis procedures across hospitals and specialized clinics

- Furthermore, continuous technological advancements in apheresis devices and the expanding use of therapeutic plasma exchange, plateletpheresis, and leukapheresis are enhancing treatment efficiency and patient outcomes. Increasing awareness among healthcare professionals, along with the rising number of blood donation and plasma collection programs worldwide, is establishing apheresis as a vital therapeutic and blood component collection technique, thereby significantly driving the growth of the Apheresis market

Apheresis Market Analysis

- Apheresis, a medical technology used to separate and collect specific blood components such as plasma, platelets, leukocytes, or red blood cells, has become an essential therapeutic and blood collection procedure in modern healthcare systems due to its effectiveness in treating various hematologic, autoimmune, and neurological disorders

- The escalating demand for apheresis procedures is primarily driven by the rising prevalence of chronic and blood-related diseases, increasing need for plasma-derived therapies, and the growing number of blood donation and plasma collection programs worldwide. In addition, technological advancements in automated apheresis devices and improved safety and efficiency of procedures are further accelerating market adoption

- North America dominated the apheresis market with the largest revenue share of around 42.8% in 2025, supported by advanced healthcare infrastructure, high awareness regarding blood component donation, and the strong presence of major industry players. The U.S. accounts for a significant share due to the growing demand for plasma collection centers and the increasing use of therapeutic apheresis in the treatment of autoimmune and hematological conditions

- Asia-Pacific is expected to be the fastest-growing region in the apheresis market during the forecast period due to improving healthcare infrastructure, rising healthcare expenditure, and growing awareness regarding blood component therapies. Countries such as China, India, and Japan are witnessing increasing adoption of apheresis systems in hospitals and blood banks

- The centrifugation segment accounted for the largest market revenue share of nearly 68.1% in 2025, driven by its widespread adoption in modern apheresis systems

Report Scope and Apheresis Market Segmentation

|

Attributes |

Apheresis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Apheresis Market Trends

Increasing Adoption of Automated and Advanced Apheresis Technologies

- A significant and accelerating trend in the global apheresis market is the increasing adoption of automated and technologically advanced apheresis systems designed to improve efficiency, safety, and clinical outcomes. Healthcare providers are increasingly shifting toward automated apheresis devices that enable precise separation of blood components while minimizing procedure time and manual intervention

- For instance, several healthcare institutions are adopting advanced apheresis platforms that allow continuous blood processing and automated monitoring, improving treatment efficiency in procedures such as therapeutic plasma exchange and plateletpheresis. These innovations help clinicians achieve more accurate blood component separation while ensuring patient safety

- Technological advancements are enabling features such as real-time monitoring of blood parameters, improved filtration systems, and automated control of blood flow rates. These capabilities enhance procedural accuracy and reduce the risk of complications during apheresis procedures

- Furthermore, modern apheresis systems are increasingly designed with user-friendly interfaces, integrated safety protocols, and data management capabilities that allow healthcare professionals to monitor procedures more effectively. These improvements support the growing demand for efficient blood component collection in blood banks and hospitals

- The trend toward automation and advanced device capabilities is transforming the way apheresis procedures are conducted, improving clinical efficiency while supporting the increasing need for plasma, platelets, and other blood components

- As a result, manufacturers are focusing on developing next-generation apheresis technologies with improved performance, enhanced safety features, and greater operational efficiency to meet the growing global demand for blood component therapies

Apheresis Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Increasing Demand for Blood Components

- The growing prevalence of chronic diseases, including hematologic disorders, autoimmune diseases, and neurological conditions, is a key factor driving the demand for apheresis procedures worldwide. Apheresis plays a crucial role in therapeutic treatments such as plasma exchange and leukapheresis, which are commonly used to manage complex medical condition

- For instance, therapeutic apheresis is widely used in the treatment of disorders such as sickle cell disease, myasthenia gravis, and certain autoimmune diseases, where the removal or replacement of specific blood components helps improve patient outcomes

- In addition, the increasing need for blood components such as plasma and platelets for transfusions, trauma care, and oncology treatments is significantly contributing to the growth of the apheresis market. Blood banks and healthcare institutions are increasingly relying on apheresis-based collection methods to obtain high-quality blood components efficiently

- The expansion of healthcare infrastructure, improved access to advanced medical treatments, and growing awareness about blood donation are also encouraging the adoption of apheresis technologies in both developed and emerging economies

- As a result, the rising burden of chronic diseases and the increasing requirement for specialized blood components are expected to significantly drive the growth of the global apheresis market during the forecast period

Restraint/Challenge

High Cost of Apheresis Equipment and Limited Availability of Skilled Professionals

- The high cost associated with apheresis equipment and procedures represents a major challenge for the growth of the global apheresis market. Advanced apheresis systems require substantial investment for procurement, maintenance, and operation, which can limit adoption in smaller healthcare facilities and developing regions

- For instance, In addition to equipment costs, apheresis procedures require trained healthcare professionals to operate specialized devices and manage patient safety during the process. The shortage of skilled professionals with expertise in apheresis technology can restrict the expansion of these procedures in certain healthcare settings

- Furthermore, the operational complexity of apheresis procedures and the need for continuous monitoring may increase healthcare costs, making it challenging for some institutions to adopt these technologies widely

- Limited reimbursement policies in certain regions can also affect the adoption of therapeutic apheresis procedures, particularly in healthcare systems with constrained budgets

- Addressing these challenges through cost-effective device innovations, improved training programs for healthcare professionals, and supportive healthcare policies will be essential to ensure sustainable growth of the global apheresis market

Apheresis Market Scope

The Apheresis market is segmented on the basis of product, disease, procedure, technology, and end-user.

- By Product

On the basis of product, the Apheresis market is segmented into apheresis devices and apheresis disposables. The apheresis disposables segment dominated the largest market revenue share of around 62.8% in 2025, driven by the recurring need for single-use components such as tubing sets, needles, filters, and collection kits used during each apheresis procedure. Disposables are essential for maintaining sterility and preventing cross-contamination between patients, which makes them indispensable in clinical practice. The increasing number of therapeutic and donor apheresis procedures worldwide is significantly contributing to the consistent demand for disposables. Hospitals and blood collection centers prefer disposable products due to their convenience, safety, and compliance with infection control protocols. In addition, stringent regulatory guidelines regarding patient safety encourage the use of sterile, single-use products during procedures. Manufacturers are also investing in advanced disposable kits that improve workflow efficiency and compatibility with modern apheresis devices. The growing demand for plasma-derived therapies further increases the use of disposable components. The expansion of blood donation programs and plasma collection centers globally also supports segment growth. As healthcare providers focus on improving safety standards and procedural efficiency, the disposable segment continues to maintain strong market dominance.

The apheresis devices segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by technological advancements and increasing installation of automated apheresis systems in hospitals and specialized centers. Modern devices offer improved automation, precision, and real-time monitoring, making procedures safer and more efficient for both patients and clinicians. The growing prevalence of chronic and blood-related diseases requiring therapeutic apheresis is fueling demand for advanced equipment. In addition, healthcare facilities are increasingly investing in technologically advanced systems that can perform multiple procedures such as plasmapheresis and leukapheresis on a single platform. Integration of digital interfaces, improved centrifugation technologies, and enhanced patient safety features are further accelerating adoption. Emerging economies are also investing in upgrading healthcare infrastructure, which supports device installations in new hospitals and blood centers. Moreover, the rising number of clinical trials and research activities involving cell therapies is creating additional demand for advanced apheresis equipment. As healthcare providers seek to improve treatment efficiency and expand service capabilities, the demand for modern apheresis devices is projected to grow rapidly.

- By Disease

On the basis of disease, the Apheresis market is segmented into haematology, autoimmune diseases, cardiovascular diseases, neurology, metabolic disorders, and renal diseases. The haematology segment accounted for the largest market revenue share of approximately 31.6% in 2025, primarily driven by the extensive use of apheresis procedures in the treatment of blood-related disorders. Conditions such as leukemia, sickle cell disease, and thrombocytosis often require therapeutic apheresis to remove abnormal blood components and improve patient outcomes. Apheresis is widely used in platelet and plasma collection for transfusions, making it a vital procedure in hematological treatment protocols. The growing prevalence of blood cancers and hereditary blood disorders worldwide significantly contributes to segment dominance. In addition, advancements in targeted therapies and hematology treatments are increasing the adoption of specialized apheresis procedures. Hospitals and blood banks frequently rely on apheresis systems to collect platelets and plasma from healthy donors for patients undergoing cancer treatments. Increasing awareness of blood donation and expanding transfusion services further support the segment’s growth. The presence of well-established clinical guidelines for therapeutic apheresis in hematology also strengthens its adoption across healthcare facilities. As the global burden of blood disorders continues to rise, the demand for hematology-related apheresis procedures remains strong.

The autoimmune diseases segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by the increasing prevalence of autoimmune conditions such as lupus, myasthenia gravis, and Guillain-Barré syndrome. Therapeutic apheresis plays a crucial role in removing harmful antibodies and immune complexes from the bloodstream, helping to manage disease symptoms and prevent complications. The growing awareness among healthcare providers regarding the effectiveness of apheresis in autoimmune disease management is significantly boosting its adoption. In addition, rising research activities and clinical trials are exploring new applications of apheresis in treating complex immune-mediated conditions. Increasing healthcare spending and improved access to advanced treatment options are further supporting segment expansion. The aging population is also more susceptible to autoimmune disorders, which contributes to rising treatment demand. Moreover, advancements in plasma exchange technologies are enhancing the safety and efficiency of procedures for autoimmune patients. As the global incidence of immune-related diseases continues to increase, the demand for apheresis-based therapeutic interventions is expected to grow rapidly.

- By Procedure

On the basis of procedure, the Apheresis market is segmented into plasmapheresis, LDL-apheresis, plateletpheresis, photopheresis, leukapheresis, erythrocytapheresis, and therapeutic cytapheresis. The plasmapheresis segment held the largest market revenue share of about 36.4% in 2025, primarily due to its widespread use in both therapeutic treatments and plasma collection for plasma-derived medicines. Plasmapheresis involves the removal and replacement of plasma from blood, which is particularly useful in treating autoimmune diseases, neurological disorders, and certain metabolic conditions. The increasing demand for plasma-derived therapies such as immunoglobulins and clotting factors significantly drives the adoption of plasmapheresis procedures. Plasma donation centers worldwide rely heavily on plasmapheresis technology to collect plasma efficiently from donors. In addition, the rising incidence of chronic diseases requiring plasma exchange treatments further strengthens market demand. Healthcare providers favor plasmapheresis because it is highly effective in rapidly removing harmful antibodies or toxins from the bloodstream. Continuous technological improvements in apheresis equipment are also making the procedure safer and more efficient. The expansion of plasma fractionation facilities globally further increases the need for plasma collection through plasmapheresis. As the demand for plasma-based therapeutics grows, this procedure continues to dominate the market.

The photopheresis segment is expected to register the fastest CAGR of 9.7% from 2026 to 2033, driven by its increasing use in treating immune-mediated diseases and certain cancers such as cutaneous T-cell lymphoma. Photopheresis combines apheresis with ultraviolet light therapy to modify immune cells before re-infusing them into the patient’s bloodstream. This innovative treatment approach helps regulate abnormal immune responses and improve patient outcomes in complex conditions. Growing clinical evidence supporting the effectiveness of extracorporeal photopheresis is encouraging healthcare providers to adopt the procedure. It is increasingly used in transplant medicine to manage graft-versus-host disease, which further contributes to segment growth. Technological advancements in photopheresis systems are also improving treatment efficiency and safety. In addition, the growing focus on personalized and targeted therapies in modern healthcare is increasing interest in advanced apheresis procedures such as photopheresis. The rising number of specialized treatment centers and research initiatives is also supporting adoption. As awareness of its therapeutic benefits expands, photopheresis is expected to experience rapid growth during the forecast period.

- By Technology

On the basis of technology, the Apheresis market is segmented into centrifugation and membrane separation. The centrifugation segment accounted for the largest market revenue share of nearly 68.1% in 2025, driven by its widespread adoption in modern apheresis systems. Centrifugation technology separates blood components based on differences in density, allowing healthcare providers to efficiently isolate plasma, platelets, or white blood cells. This method is widely used in both therapeutic and donor apheresis procedures due to its high efficiency and reliability. Hospitals and blood collection centers prefer centrifugation systems because they can perform multiple procedures using a single platform. Continuous technological advancements have further improved automation, accuracy, and safety in centrifugation-based devices. The technology also allows for higher collection yields, which is particularly important in plasma donation centers. In addition, centrifugation systems are compatible with a wide range of disposable kits, making them versatile for different procedures. The growing number of blood donation programs and therapeutic treatments requiring component separation further strengthens the segment’s market position. As healthcare facilities prioritize efficiency and precision in blood processing, centrifugation technology continues to dominate the market.

The membrane separation segment is projected to witness the fastest CAGR of 8.5% from 2026 to 2033, driven by its advantages in specific therapeutic applications and growing technological innovations. Membrane filtration technology separates blood components using specialized semi-permeable membranes, providing a gentler and more controlled separation process. This technology is particularly beneficial for patients requiring selective removal of plasma components while preserving essential blood cells. Increasing research efforts and technological advancements are improving membrane durability and filtration efficiency, which is encouraging wider adoption. In addition, membrane-based systems are gaining popularity in therapeutic plasma exchange procedures due to their precision and safety profile. The growing demand for advanced treatment options for autoimmune and metabolic disorders further supports the segment’s growth. Healthcare providers are also exploring hybrid systems that combine membrane filtration with other technologies to improve performance. As medical research continues to develop new therapeutic applications for apheresis, membrane separation technology is expected to experience significant growth.

- By End-User

On the basis of end-user, the Apheresis market is segmented into blood collection centres, hospitals, and ambulatory centres. The blood collection centres segment dominated the market with the largest revenue share of around 44.5% in 2025, primarily driven by the increasing demand for plasma and platelet donations worldwide. These centers play a critical role in collecting blood components that are later used for transfusions and manufacturing plasma-derived therapies. The expansion of plasma donation facilities and national blood donation programs significantly contributes to the growth of this segment. Blood collection centers are equipped with specialized apheresis systems that allow efficient and safe component collection from donors. In addition, the rising global demand for immunoglobulins and clotting factor concentrates increases the need for plasma collection through apheresis. Governments and healthcare organizations are also promoting voluntary blood donation campaigns to ensure a stable supply of blood products. The presence of dedicated infrastructure and trained personnel further supports the widespread use of apheresis systems in these centers. Continuous investments in improving donor safety and collection efficiency also contribute to segment dominance.

The ambulatory centres segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by the growing shift toward outpatient care and minimally invasive treatment settings. Ambulatory centers provide convenient and cost-effective treatment options for patients requiring therapeutic apheresis procedures. These facilities are increasingly adopting advanced apheresis technologies to expand their treatment capabilities and reduce hospital burden. Patients often prefer ambulatory centers due to shorter waiting times and personalized care services. In addition, healthcare systems worldwide are focusing on decentralizing specialized treatments to improve accessibility and reduce overall healthcare costs. Technological advancements have made apheresis devices more compact and suitable for outpatient environments. The increasing prevalence of chronic diseases requiring periodic therapeutic apheresis is also encouraging the expansion of ambulatory treatment facilities. As healthcare delivery models continue to evolve toward outpatient services, ambulatory centers are expected to play an increasingly important role in the apheresis market.

Apheresis Market Regional Analysis

- North America dominated the apheresis market with the largest revenue share of around 42.8% in 2025, supported by advanced healthcare infrastructure, high awareness regarding blood component donation, and the strong presence of major industry players. The region has a well-established network of hospitals, blood banks, and plasma collection centers that utilize advanced apheresis systems for both therapeutic treatments and blood component collection

- The growing demand for plasma-derived therapies, increasing prevalence of autoimmune and hematological disorders, and strong research activities in transfusion medicine are further accelerating the adoption of apheresis technologies across the region

- In addition, supportive healthcare policies, high healthcare spending, and continuous technological advancements in medical devices are contributing to the widespread implementation of apheresis systems in clinical and blood collection settings, strengthening the region’s market dominance

U.S. Apheresis Market Insight

The U.S. apheresis market captured the largest revenue share within North America in 2025, driven by the growing demand for plasma collection and the increasing use of therapeutic apheresis in the treatment of autoimmune, neurological, and hematological disorders. The country hosts a large number of plasma donation centers and advanced healthcare facilities that rely heavily on apheresis technologies for efficient blood component separation. Furthermore, strong investments in healthcare infrastructure, rising adoption of advanced medical technologies, and increasing awareness regarding blood donation programs are supporting market expansion. The presence of major industry players and continuous research in transfusion medicine are also significantly contributing to the growth of the apheresis market in the United States.

Europe Apheresis Market Insight

The Europe apheresis market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the increasing demand for plasma-derived therapies and the rising prevalence of chronic and autoimmune diseases. The region benefits from well-established healthcare systems, strong regulatory frameworks, and growing investments in advanced medical technologies. In addition, the rising awareness regarding blood component donation and the increasing adoption of therapeutic apheresis procedures in hospitals are contributing to market growth. Countries across Europe are increasingly focusing on improving blood collection infrastructure and ensuring an adequate supply of blood components for medical treatments.

U.K. Apheresis Market Insight

The U.K. apheresis market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the country’s advanced healthcare system and increasing demand for blood components used in complex medical treatments. Therapeutic apheresis is increasingly being utilized in the management of autoimmune diseases, neurological disorders, and certain hematological conditions. In addition, government initiatives encouraging blood donation, along with the expansion of hospital-based blood collection services, are contributing to the adoption of apheresis technologies in the country. Continuous improvements in healthcare infrastructure and the growing focus on patient-centered treatment approaches are also expected to support market growth.

Germany Apheresis Market Insight

The Germany apheresis market is expected to expand at a considerable CAGR during the forecast period, driven by strong healthcare infrastructure, increasing investments in advanced medical technologies, and growing demand for plasma-derived therapies. Germany has a well-developed network of hospitals and blood banks that utilize apheresis systems for both therapeutic procedures and blood component collection. Furthermore, increasing research in hematology and transfusion medicine, along with the rising incidence of chronic diseases requiring specialized blood treatments, is contributing to the expansion of the apheresis market in the country.

Asia-Pacific Apheresis Market Insight

The Asia-Pacific apheresis market is expected to grow at the fastest pace during the forecast period, driven by improving healthcare infrastructure, rising healthcare expenditure, and increasing awareness regarding blood component therapies. Rapid population growth and the rising burden of chronic diseases in countries such as China, India, and Japan are creating a strong demand for advanced blood collection and therapeutic technologies. In addition, expanding hospital networks, government initiatives promoting blood donation, and increasing investments in healthcare modernization are supporting the adoption of apheresis systems across the region. The growing presence of medical device manufacturers and improving accessibility to advanced healthcare technologies are further expected to accelerate market growth.

Japan Apheresis Market Insight

The Japan apheresis market is gaining momentum due to the country’s advanced healthcare infrastructure, strong focus on medical innovation, and increasing demand for blood component therapies. The growing aging population and the rising prevalence of chronic and autoimmune diseases are increasing the need for therapeutic apheresis procedures in hospitals and specialized treatment centers. Moreover, Japan’s strong emphasis on medical research and the adoption of advanced healthcare technologies are encouraging the use of modern apheresis systems for efficient blood component separation and patient treatment.

China Apheresis Market Insight

The China apheresis market accounted for the largest market revenue share in the Asia-Pacific region in 2025, attributed to the country’s expanding healthcare infrastructure, rising healthcare spending, and increasing awareness regarding blood donation and plasma collection. China is witnessing rapid growth in hospitals, blood banks, and specialized medical facilities that utilize apheresis systems for blood component separation and therapeutic procedures. In addition, government initiatives aimed at strengthening healthcare services and improving access to advanced medical technologies are significantly contributing to the growth of the apheresis market in the country.

Apheresis Market Share

The Apheresis industry is primarily led by well-established companies, including:

- Terumo Corporation (Japan)

- Fresenius SE & Co. KGaA (Germany)

- Haemonetics Corporation (U.S.)

- B. Braun SE (Germany)

- Asahi Kasei Corporation (Japan)

- Kawasumi Laboratories Inc. (Japan)

- Kaneka Corporation (Japan)

- Miltenyi Biotec (Germany)

- Cerus Corporation (U.S.)

- Macopharma (France)

- Haier Biomedical (China)

- Nikkiso Co., Ltd. (Japan)

- Infomed SA (Switzerland)

- Baxter International Inc. (U.S.)

- Medica S.p.A. (Italy)

- HemaCare Corporation (U.S.)

- Otsuka Holdings Co., Ltd. (Japan)

- Fresenius Kabi (Germany)

- Terumo BCT (U.S.)

- Asahi Kasei Medical Co., Ltd. (Japan)

Latest Developments in Global Apheresis Market

- In March 2022, Terumo Blood and Cell Technologies announced that the U.S. FDA cleared its Rika Plasma Donation System, a next-generation plasma collection platform designed to enhance donor safety, improve operational efficiency, and streamline plasma collection processes for blood centers. The system integrates advanced safety controls, improved ergonomics, and faster collection capabilities, enabling plasma collection facilities to increase productivity while maintaining high donor comfort and safety standards

- In April 2023, Fresenius Kabi introduced a new single-needle venous access option for the Amicus Extracorporeal Photopheresis (ECP) System at the European Society for Blood and Marrow Transplantation (EBMT) annual meeting. This development was designed to improve patient comfort during photopheresis procedures and simplify vascular access, helping clinicians perform apheresis-based treatments more efficiently in patients with limited venous access

- In August 2023, Terumo Blood and Cell Technologies and Eliaz Therapeutics announced an exclusive collaboration to develop therapeutic approaches using apheresis technologies for the selective removal of Galectin-3 (Gal-3), an inflammatory protein linked to acute kidney injury and organ damage. The partnership aimed to leverage advanced blood purification and apheresis capabilities to support the development of targeted treatments for inflammatory and fibrotic diseases

- In August 2024, Fresenius Medical Care received CE MDR certification for its APRED apheresis pathogen reduction device and subsequently launched the system in Europe. Following the approval, the first lipoprotein apheresis treatments were successfully performed using the platform, highlighting its capability to deliver advanced therapeutic blood purification with improved monitoring and safety features

- In November 2024, Terumo Blood and Cell Technologies announced a strategic manufacturing partnership with Terumo Medical Products (Hangzhou) Co., Ltd. to establish local production of its blood and cell technologies products in Hangzhou, China. The initiative aimed to strengthen the company’s supply chain, expand access to apheresis technologies across Asia-Pacific, and support the growing demand for blood component collection and cell therapy manufacturing

- In May 2025, Fresenius Medical Care completed the acquisition of the kidney care business of Natera, Inc., including automated plasma exchange and filtration technologies. The acquisition strengthened Fresenius Medical Care’s therapeutic apheresis portfolio and expanded its capabilities in extracorporeal blood purification and kidney disease management

- In September 2025, Grifols received European Commission marketing authorization for the Spectra Optia Apheresis System, a fully automated disposable apheresis platform designed to improve operational efficiency and reduce procedural costs in hospitals and blood centers. The system offers advanced automation and disposable components that simplify workflows and enhance safety during blood component collection and therapeutic apheresis procedures

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.