Global Apoptosis Assays Market

Market Size in USD Billion

CAGR :

%

USD

4.66 Billion

USD

9.21 Billion

2025

2033

USD

4.66 Billion

USD

9.21 Billion

2025

2033

| 2026 –2033 | |

| USD 4.66 Billion | |

| USD 9.21 Billion | |

| % | |

|

Apoptosis Assays Market Overview

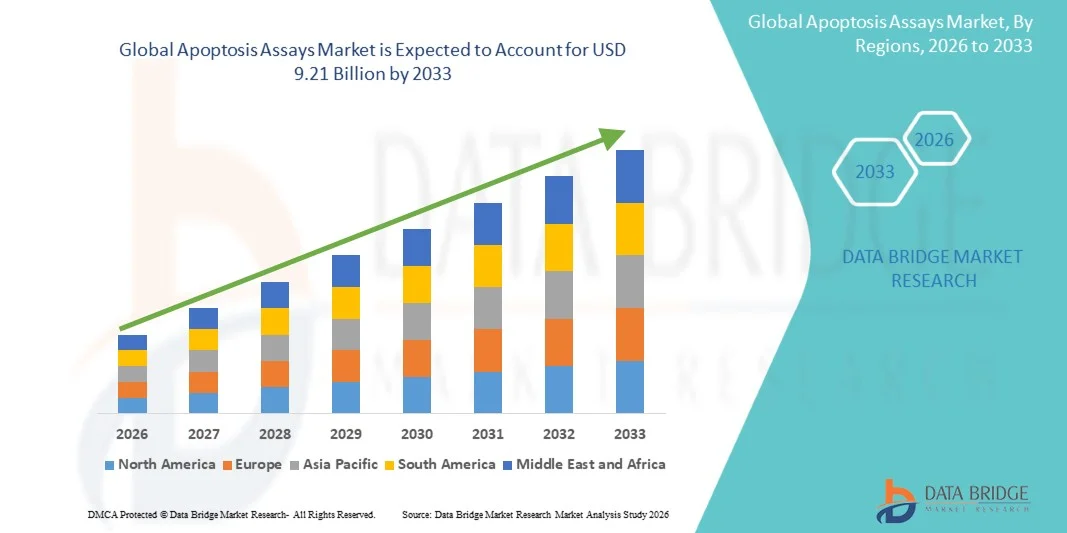

The global Apoptosis Assays market was valued at USD 4.66 billion in 2025 and is projected to reach USD 9.21 billion by 2033, growing at a CAGR of 8.90% from 2026 to 2033. The Global Apoptosis Assays Market is experiencing consistent growth driven by rising prevalence of cancer and chronic diseases, increasing adoption of cell-based research in drug discovery, and rapid advancements in fluorescence-based, luminescence-based, and flow cytometry assay technologies. Growing focus on understanding programmed cell death mechanisms in oncology, immunology, and neurodegenerative disease research is further strengthening demand for apoptosis detection tools across pharmaceutical and biotechnology industries.

The increasing investment in life sciences research, combined with expanding drug development pipelines and rising demand for high-throughput screening platforms, is encouraging pharmaceutical companies, academic research institutes, and contract research organizations (CROs) to adopt advanced apoptosis assay solutions. Kits, reagents, and instrument-based assay systems are increasingly replacing conventional cell viability testing methods, offering higher sensitivity, accuracy, and reproducibility in detecting early and late-stage apoptosis. In addition, growing use of automated imaging systems, multiplex assays, and AI-assisted data analysis is improving research efficiency and accelerating adoption across both developed and emerging research markets.

Key Market Trends & Insights

- North America dominated the global Apoptosis Assays market with the largest revenue share of 36.9% in 2025, supported by strong biomedical research infrastructure, high R&D investments by pharmaceutical and biotechnology companies, and widespread adoption of advanced apoptosis detection technologies across clinical and academic settings.

- The Assay Kits segment led the market with a 41.8% share in 2025, driven by high demand for standardized, easy-to-use, and reproducible solutions in drug screening, disease research, and laboratory diagnostics.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.5% from 2026 to 2033, fueled by increasing government funding for life sciences research, expanding pharmaceutical manufacturing, rising clinical diagnostics demand, and growing adoption of advanced laboratory technologies in China, India, and Japan.

- The Flow Cytometry segment is the fastest-growing technology category, projected to register a CAGR of 7.3%, driven by its high accuracy, ability to analyze large cell populations rapidly, and increasing use in cancer research, immunology, and drug discovery applications.

- The Pharmaceutical and Biotechnology Companies segment dominates the end-user category with a 43.2% revenue share in 2025, led by extensive use of apoptosis assays in drug discovery, toxicity testing, and therapeutic development pipelines.

- The Drug Discovery and Development segment dominates the application category with a 46.1% revenue share in 2025, supported by rising demand for targeted therapies, increasing oncology research, and growing need for early-stage drug screening.

- The Academic and Research Institutes segment is expected to be the fastest-growing end-user category, registering a CAGR of 7.0% from 2026 to 2033, driven by expanding government research funding, growing publication output, and increased adoption of advanced cell biology techniques.

- The Cell Imaging and Analysis Systems segment is the fastest-growing technology category, projected to register a CAGR of 7.2%, driven by advancements in high-resolution imaging, automation, and AI-based image analysis for apoptosis detection.

- The Drug Discovery and Development segment dominated the market with the largest revenue share of 46.1% in 2025 due to the critical role of apoptosis assays in screening drug efficacy, evaluating cytotoxicity, and identifying therapeutic mechanisms

Market Size & Forecast

- Global Market Value (2025): USD 4.66 Billion

- Expected Market Value (2033): USD 9.21 Billion

- Forecast CAGR (2026–2033): 8.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Global Apoptosis Assays Market Segmentation

|

Attributes |

Apoptosis Assays Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Thermo Fisher Scientific Inc. (U.S.) |

|

Market Opportunities |

· Increasing demand for targeted drug discovery and precision medicine presents a strong opportunity · Growing demand for autonomous vehicle validation platforms · Growing adoption of advanced technologies such as flow cytometry |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Apoptosis Assays Market Trends

Trend: Rising Adoption of High-Throughput Cell Death Analysis in Drug Discovery

The global apoptosis assays market is witnessing strong growth driven by the increasing use of high-throughput screening (HTS) technologies in pharmaceutical and biotechnology research. Apoptosis assays are widely used to study programmed cell death in cancer, neurodegenerative diseases, and immunological disorders. For instance, fluorescence-based assays and flow cytometry platforms are increasingly used in oncology drug pipelines to evaluate compound toxicity and therapeutic efficacy at early-stage screening. According to multiple life sciences industry reports, over 65% of oncology drug discovery workflows now incorporate apoptosis-based assays for preclinical evaluation. The integration of automated imaging systems and multi-well plate readers is further improving assay speed, reproducibility, and scalability across research laboratories globally.

Global Apoptosis Assays Market Dynamics

Key Market Driver: Expanding Cancer Research and Increasing R&D Investment

A major driver of the apoptosis assays market is the rising global burden of cancer and the increasing investment in oncology research. According to the World Health Organization (WHO), cancer accounted for nearly 10 million deaths in 2020, significantly increasing demand for advanced cell biology tools such as apoptosis detection kits. Pharmaceutical companies such as Roche, Novartis, and Pfizer are increasingly integrating apoptosis assays in drug development pipelines to evaluate anti-cancer drug efficacy and cytotoxicity. In addition, government-funded research programs such as the U.S. National Cancer Institute (NCI) and EU Horizon initiatives are significantly boosting adoption of flow cytometry and caspase activity assays in academic and clinical research. The growing focus on precision medicine and targeted therapies is further accelerating demand for reliable apoptosis measurement technologies.

Key Restraint/Challenge: High Cost and Technical Complexity of Advanced Assay Platforms

Despite strong demand, the apoptosis assays market faces challenges related to the high cost and technical complexity of advanced platforms such as flow cytometers, high-content imaging systems, and automated cell analysis instruments. A single advanced flow cytometry system can cost between USD 50,000 to over USD 300,000, making adoption difficult for small research laboratories and academic institutes in developing regions. Additionally, apoptosis assays require skilled personnel for sample preparation, data interpretation, and protocol optimization, which limits widespread adoption in resource-constrained settings. Variability in assay results due to biological sample differences and reagent sensitivity also remains a technical challenge, impacting reproducibility across studies.

A notable example is the increasing dependency on centralized core facilities in universities and hospitals, where expensive apoptosis detection instruments are shared across multiple departments to reduce cost burden—highlighting infrastructure limitations in smaller research environments.

Key Market Opportunity: Integration of AI, Automation, and Advanced Imaging in Cell Death Analysis

A significant opportunity in the apoptosis assays market lies in the integration of artificial intelligence (AI), machine learning, and automated imaging technologies. AI-powered image analysis platforms are increasingly being used to detect early-stage apoptotic markers with higher accuracy and reduced human error. Companies such as Thermo Fisher Scientific and Bio-Rad are developing automated high-content screening systems that combine fluorescence imaging with AI-based pattern recognition to accelerate drug discovery workflows. In addition, the adoption of cloud-based data analysis platforms and multiplex apoptosis assays is enabling researchers to analyze multiple biomarkers simultaneously, improving efficiency in cancer and immunology research. The expansion of personalized medicine and organoid-based disease modeling is further expected to drive demand for advanced apoptosis assay technologies across pharmaceutical, academic, and clinical research settings globally.

Global Apoptosis Assays Market Scope

The Apoptosis Assays market is segmented on the basis of product, technology, end user, and application.

- By Product

On the basis of product, the global Apoptosis Assays market is segmented into assay kits, reagents, microplates, and instruments. The Assay Kits segment dominated the market with the largest revenue share of 41.8% in 2025 due to its standardized workflow compatibility, high reproducibility, and extensive use in drug discovery and toxicity screening applications. These kits simplify apoptosis detection by integrating multiple reagents into ready-to-use formats, reducing experimental variability and improving laboratory efficiency. Strong adoption by pharmaceutical and biotechnology companies for oncology research, neurodegenerative disease studies, and high-throughput screening further supports segment dominance. Increasing preference for cost-effective and time-saving solutions in academic and clinical research is also driving demand. Continuous innovation in multiplex and fluorescence-based assay kits is enhancing sensitivity and accuracy across research workflows. Rising global investment in life sciences research infrastructure further strengthens market penetration.

The Instruments segment is expected to witness the fastest growth, registering a CAGR of 7.4% from 2026 to 2033, driven by increasing adoption of automated flow cytometers, high-content imaging systems, and advanced cell analyzers. Growing demand for precision-based apoptosis measurement and real-time cellular analysis is accelerating instrument deployment. Integration of AI-powered imaging, automated sample processing, and cloud-based data analysis is further enhancing research efficiency. Pharmaceutical companies and research institutes are increasingly investing in laboratory automation to improve throughput and reproducibility. Expansion of biotechnology R&D centers in emerging economies is also boosting instrument adoption. In addition, rising demand for personalized medicine and targeted therapy development is supporting long-term growth.

- By Technology

On the basis of technology, the global Apoptosis Assays market is segmented into flow cytometry, cell imaging and analysis systems, spectrophotometry, and other detection technologies. The Flow Cytometry segment dominated the market with the largest revenue share of 39.6% in 2025 due to its high accuracy, rapid analysis capability, and ability to evaluate multiple apoptotic markers simultaneously. It is widely used in cancer research, immunology, and drug discovery applications across pharmaceutical and academic laboratories. The technology enables high-throughput single-cell analysis, making it essential for modern biomedical research. Increasing use of fluorescent labeling and multi-parameter detection is further enhancing its performance. Strong adoption in clinical diagnostics and translational research is also reinforcing its leadership position. Growing investments in advanced cytometry platforms by major life science companies are expanding global usage.

The Cell Imaging and Analysis Systems segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by advancements in high-content screening technologies and automated microscopy platforms. These systems enable real-time visualization of apoptotic processes with high spatial and temporal resolution. Integration of AI and machine learning algorithms for image recognition and data interpretation is significantly improving accuracy. Rising demand for phenotypic screening in drug discovery is accelerating adoption. Increasing use in stem cell research and cancer biology studies is also boosting growth. Continuous improvements in fluorescence imaging and multiplex detection technologies are further enhancing performance. Expansion of research laboratories globally is supporting strong long-term demand.

- By End User

On the basis of end user, the global Apoptosis Assays market is segmented into pharmaceutical and biotechnology companies, hospital and diagnostic laboratories, and academic and research institutes. The Pharmaceutical and Biotechnology Companies segment dominated the market with the largest revenue share of 43.2% in 2025 due to extensive use of apoptosis assays in drug discovery, toxicity testing, and preclinical development pipelines. These companies rely heavily on apoptosis analysis for evaluating anticancer drug efficacy and identifying novel therapeutic compounds. High R&D expenditure and increasing focus on precision medicine further support segment dominance. Growing oncology drug development programs and biologics research are key contributors. Widespread adoption of automated high-throughput screening systems is improving research efficiency. Strong collaboration between biotech firms and research organizations is also expanding application scope. Increasing global demand for targeted therapies is further strengthening market leadership.

The Academic and Research Institutes segment is expected to witness the fastest CAGR of 7.0% from 2026 to 2033, driven by rising government funding for life sciences and expanding cellular biology research programs. Increasing focus on disease mechanism studies, especially cancer and neurodegenerative disorders, is accelerating adoption. Universities and research centers are increasingly using apoptosis assays for molecular and genetic research. Growth in publication output and international research collaboration is further boosting demand. Expansion of biotechnology education and training programs is also supporting market growth. Rising availability of advanced laboratory infrastructure in emerging economies is enhancing adoption. Increasing participation in global research initiatives is further strengthening segment expansion.

- By Application

On the basis of application, the global Apoptosis Assays market is segmented into drug discovery and development, clinical and diagnostic applications, basic research, and stem cell research. The Drug Discovery and Development segment dominated the market with the largest revenue share of 46.1% in 2025 due to the critical role of apoptosis assays in screening drug efficacy, evaluating cytotoxicity, and identifying therapeutic mechanisms. These assays are widely used in oncology pipelines where programmed cell death analysis is essential for anticancer drug validation. Increasing demand for high-throughput screening platforms and automation in pharmaceutical research further strengthens segment dominance. Strong investment in targeted therapy development and biologics is also contributing to growth. Expanding use of multiplex assays for faster compound screening is improving efficiency. Rising global burden of cancer and chronic diseases is further accelerating adoption. Continuous innovation in assay technologies is enhancing application scope.

The Stem Cell Research segment is expected to witness the fastest CAGR of 7.3% from 2026 to 2033, driven by rapid advancements in regenerative medicine and tissue engineering. Increasing use of apoptosis assays in stem cell differentiation and viability studies is boosting demand. Growing investments in cell-based therapies and personalized medicine research are supporting segment expansion. Rising interest in organoid models and 3D cell culture systems is further accelerating adoption. Academic and biotech collaborations are enhancing research output. Expanding funding for regenerative medicine programs globally is also contributing to growth. Increasing clinical translation of stem cell therapies is expected to drive long-term market demand.

Global Apoptosis Assays Market Regional Analysis

North America dominated the Apoptosis Assays market and accounted for the largest revenue share of 36.9% in 2025, supported by strong biomedical research infrastructure, high R&D investments by pharmaceutical and biotechnology companies, and widespread adoption of advanced apoptosis detection technologies across clinical and academic settings. The region benefits from the presence of leading life science companies, advanced laboratory automation systems, and strong government funding for cancer and cell biology research. Increasing focus on drug discovery, precision medicine, and oncology research is further strengthening market expansion. The high adoption of flow cytometry, high-content imaging systems, and automated assay platforms continues to reinforce North America’s leadership in the global market.

U.S. Apoptosis Assays Market Insight

The U.S. Apoptosis Assays market is witnessing strong growth due to increasing cancer research activities, rising pharmaceutical R&D investments, and strong adoption of advanced cell analysis technologies. Major biotech and pharmaceutical companies are increasingly integrating apoptosis assays into drug screening and toxicity testing workflows. Government funding from agencies such as the National Institutes of Health (NIH) is further supporting research expansion. In addition, the presence of advanced laboratory infrastructure and early adoption of AI-driven imaging systems is accelerating market growth across academic and clinical research institutions.

Europe Apoptosis Assays Market Insight

The Europe Apoptosis Assays market remains a significant contributor to global revenue, driven by strong research funding, increasing prevalence of chronic diseases, and high adoption of advanced cell biology technologies. The region benefits from well-established pharmaceutical companies and academic research institutions actively engaged in oncology and immunology studies. Rising focus on precision medicine and personalized therapeutics is further boosting demand for apoptosis assay solutions. Additionally, supportive government initiatives and collaborative research programs across EU countries are strengthening market expansion.

U.K. Apoptosis Assays Market Insight

The U.K. Apoptosis Assays market is experiencing steady growth due to increasing investment in biomedical research, expanding pharmaceutical sector activities, and strong academic research output. Universities and research institutes are widely adopting apoptosis assays for cancer biology and drug discovery studies. The integration of advanced imaging systems and flow cytometry technologies is improving research efficiency. In addition, government-backed life sciences initiatives and strong collaboration between academia and industry are supporting sustained market growth.

Germany Apoptosis Assays Market Insight

The Germany Apoptosis Assays market is expanding steadily due to strong pharmaceutical manufacturing, advanced biotechnology research, and increasing focus on oncology and neurodegenerative disease studies. Research institutions and biotech companies are heavily investing in high-throughput screening technologies and cell-based assay platforms. Growing adoption of automated laboratory systems and precision diagnostics is further enhancing research capabilities. In addition, government support for life sciences innovation is strengthening the country’s position in the global market.

Asia-Pacific Apoptosis Assays Market Insight

The Asia-Pacific Apoptosis Assays market is expected to witness rapid growth, recording a CAGR of 7.5% from 2026 to 2033, driven by increasing government funding for life sciences research, expanding pharmaceutical manufacturing, and rising clinical diagnostics demand. Countries such as China, India, and Japan are witnessing strong adoption of advanced laboratory technologies and increasing investment in biotechnology infrastructure. Growing focus on cancer research, rising patient population, and expansion of research institutions are further supporting regional market growth.

Japan Apoptosis Assays Market Insight

The Japan Apoptosis Assays market is witnessing consistent growth due to strong pharmaceutical research activities, advanced biotechnology sector, and increasing focus on regenerative medicine. The country’s research institutes and universities are actively adopting apoptosis assays for cell biology and drug development studies. Integration of high-precision imaging systems and automated analytical platforms is improving research efficiency. In addition, Japan’s strong focus on innovation in life sciences is supporting steady market expansion.

China Apoptosis Assays Market Insight

The China Apoptosis Assays market is growing rapidly, driven by increasing investments in biotechnology research, expanding pharmaceutical industry, and rising demand for advanced clinical diagnostics. Government support for life sciences innovation and growing number of research institutions are significantly boosting adoption of apoptosis assay technologies. Increasing focus on cancer research, stem cell studies, and precision medicine is further accelerating market growth. In addition, rapid expansion of laboratory infrastructure and rising collaboration with global biotech companies are positioning China as one of the fastest-growing markets globally.

Global Apoptosis Assays Market Share

The Apoptosis Assays industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Merck KGaA (Germany)

- Abcam plc (U.K.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Danaher Corporation (U.S.)

- PerkinElmer Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Promega Corporation (U.S.)

- Cell Signaling Technology, Inc. (U.S.)

- Sartorius AG (Germany)

- Lonza Group AG (Switzerland)

- Miltenyi Biotec (Germany)

- GE HealthCare (U.S.)

- Revvity (PerkinElmer Life Sciences) (U.S.)

- Bio-Techne Corporation (U.S.)

- Takara Bio Inc. (Japan)

- Sysmex Corporation (Japan)

- HiMedia Laboratories (India)

- Randox Laboratories Ltd. (U.K.)

- Tocris Bioscience (U.K.)

- Enzo Life Sciences (U.S.)

- Santa Cruz Biotechnology, Inc. (U.S.)

- Sigma-Aldrich (Merck Life Science) (Germany)

- Olympus Corporation (Japan)

- Nikon Corporation (Japan)

- Sartorius Stedim Biotech (France)

- Corning Incorporated (U.S.)

- Qiagen N.V. (Netherlands)

Latest Developments in Global Apoptosis Assays Market

- In August 2024, Bio-Rad Laboratories launched its Annexin V conjugated StarBright Dye panel, designed to enhance apoptosis detection through flow cytometry. The new multiplex fluorescent conjugates improve spectral resolution, reduce spillover, and enable more accurate identification of early and late apoptotic cells. This launch strengthens Bio-Rad’s position in high-precision cell analysis and supports growing demand for advanced flow cytometry-based apoptosis assays in oncology and immunology research

- In February 2025, Abcam announced a strategic collaboration with Genentech to co-develop multiplexed apoptosis assay kits for personalized oncology research. The partnership focuses on improving detection of programmed cell death pathways using high-sensitivity biomarkers, supporting next-generation cancer drug discovery workflows. This development reflects increasing industry emphasis on precision medicine and advanced multiplex assay platforms

- In March 2025, Bio-Rad Laboratories introduced the Clario Cytometer system, an AI-enabled high-throughput flow cytometry platform designed for apoptosis and cell viability analysis. The system integrates automated image interpretation and advanced analytics, enabling faster and more reproducible detection of apoptotic markers in large-scale drug screening applications. This launch highlights the accelerating integration of AI in apoptosis assay workflows

- In May 2025, Thermo Fisher Scientific launched the Invitrogen Attune Xenith Flow Cytometer, a spectral flow cytometry platform optimized for immunology and immuno-oncology research. The system supports high-resolution multi-parameter apoptosis analysis and improves throughput for complex cellular studies, reinforcing Thermo Fisher’s leadership in cell analysis technologies

- In July 2025, Thermo Fisher Scientific expanded its precision oncology portfolio with the Oncomine Comprehensive Assay Plus, enabling next-generation genomic profiling for cancer research applications linked with apoptosis pathways. The platform enhances biomarker discovery and supports deeper analysis of tumor cell death mechanisms in drug development pipelines

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.