Global Artificial Eye Market

Market Size in USD Billion

CAGR :

%

USD

3.75 Billion

USD

6.65 Billion

2025

2033

USD

3.75 Billion

USD

6.65 Billion

2025

2033

| 2026 –2033 | |

| USD 3.75 Billion | |

| USD 6.65 Billion | |

| % | |

|

Artificial Eye Market Size

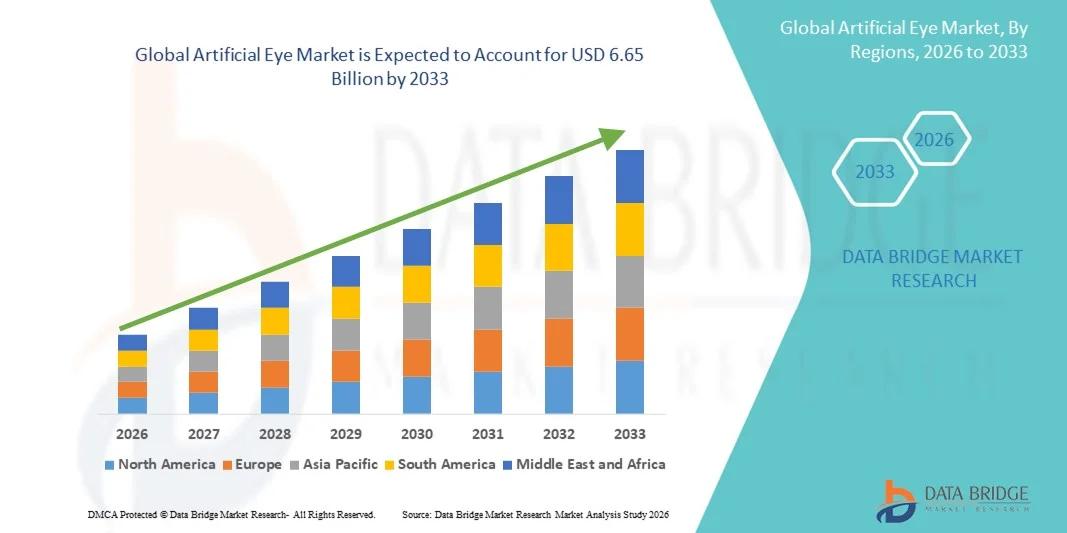

- The global artificial eye market size was valued at USD 3.75 billion in 2025 and is expected to reach USD 6.65 billion by 2033, at a CAGR of 7.43% during the forecast period

- The market growth is largely driven by the rising prevalence of ocular disorders, vision loss, and eye-related trauma, coupled with increasing awareness and acceptance of prosthetic eye solutions. Technological advancements in ocular prosthetics, including improved materials and customization techniques, are contributing to greater adoption across both developed and developing healthcare systems

- Furthermore, growing demand for aesthetically realistic, comfortable, and patient-specific artificial eye solutions is positioning artificial eyes as an essential component of ocular rehabilitation. These factors, along with expanding access to ophthalmic care and supportive reimbursement policies in certain regions, are significantly accelerating the uptake of Artificial Eye solutions and boosting overall market growth

Artificial Eye Market Analysis

- Artificial eyes, also known as ocular prostheses, are essential medical devices used for cosmetic and psychological rehabilitation following eye loss due to trauma, congenital conditions, tumors, or severe ocular diseases. Advances in prosthetic materials, customization techniques, and digital imaging are improving aesthetic realism and patient comfort, increasing adoption across healthcare settings

- The growing demand for artificial eyes is primarily driven by the rising incidence of eye injuries and ocular disorders, increasing awareness of ocular prosthetic solutions, and improvements in ophthalmic healthcare infrastructure. In addition, the emphasis on patient-centered care and aesthetic restoration is encouraging greater acceptance of artificial eye procedures worldwide

- North America dominated the artificial eye market with a revenue share of approximately 38.5% in 2025, supported by advanced ophthalmic care facilities, higher healthcare spending, strong reimbursement frameworks, and the presence of specialized ocular prosthetic clinics. The U.S. accounts for the majority of regional demand due to higher awareness levels and access to skilled ocularists

- Asia-Pacific is expected to be the fastest-growing region in the artificial eye market during the forecast period, driven by a rising patient pool, increasing incidence of ocular trauma, improving healthcare access, and growing investments in eye care services across countries such as China, India, and Japan

- The Mechanical technology segment held the largest market revenue share of 62.4% in 2025, primarily due to its long-standing clinical acceptance, reliability, and lower cost

Report Scope and Artificial Eye Market Segmentation

|

Attributes |

Artificial Eye Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Artificial Eye Market Trends

Technological Advancements in Prosthetic Design and Material Innovation

- A prominent and accelerating trend in the global artificial eye market is the continuous advancement in prosthetic eye design, driven by innovations in biomaterials, manufacturing techniques, and customization technologies. Modern artificial eyes are increasingly designed to closely mimic the natural appearance, movement, and comfort of a human eye, significantly improving patient satisfaction and quality of life

- For instance, in October 2023, several leading ocular prosthetic laboratories in the U.S. and Europe adopted high-resolution digital iris photography and 3D scanning systems to create patient-specific artificial eyes, enabling more precise color matching and anatomical accuracy compared to traditional hand-painted methods. This shift has improved cosmetic realism and reduced the number of adjustment visits required

- Manufacturers are focusing on the use of lightweight, biocompatible materials such as medical-grade acrylics, silicone, and advanced polymers that offer enhanced durability, reduced irritation, and long-term safety. These materials allow for better tissue compatibility and reduce complications such as inflammation or discomfort

- The adoption of advanced surface finishing and polishing techniques is enhancing the natural shine and lifelike appearance of artificial eyes, making them visually indistinguishable from natural eyes under normal lighting conditions

- The market is also witnessing growing collaboration between ocularists, ophthalmologists, and research institutions to develop next-generation prosthetic eyes with improved fit, comfort, and synchronized movement, reshaping patient expectations across the global Artificial Eye market

Artificial Eye Market Dynamics

Driver

Rising Incidence of Eye Disorders, Trauma, and Congenital Conditions

- The increasing prevalence of eye disorders, traumatic injuries, ocular cancers, and congenital eye conditions resulting in eye loss is a major driver of growth in the global Artificial Eye market. Road accidents, workplace injuries, sports-related trauma, and disease-related complications continue to contribute significantly to demand

- For instance, in May 2024, healthcare organizations highlighted a rise in pediatric eye removals due to retinoblastoma in developing regions, increasing the need for early-stage ocular prosthetic fitting as part of post-surgical rehabilitation programs. Such cases are directly driving demand for pediatric artificial eyes globally

- Growing awareness regarding cosmetic rehabilitation and psychological well-being following eye loss is encouraging patients to opt for artificial eye solutions rather than untreated facial disfigurement

- Advances in ophthalmic surgery and post-operative care have increased survival and recovery rates, resulting in a higher number of patients eligible for prosthetic eye fitting

- In addition, improvements in healthcare infrastructure and access to ophthalmology services, particularly in Asia-Pacific and Latin America, are supporting broader adoption of artificial eyes across both pediatric and adult populations

Restraint/Challenge

High Cost of Customization and Limited Access to Skilled Ocularists

- One of the primary challenges restraining the Artificial Eye market is the high cost associated with customized prosthetic eye solutions, which require specialized materials, skilled craftsmanship, and multiple fitting sessions

- For instance, in July 2022, ophthalmic associations reported that many regions in Africa and parts of Southeast Asia had fewer than one trained ocularist per million people, significantly limiting access to high-quality artificial eye services and increasing treatment wait times. This shortage directly affects market penetration in underserved areas

- The lack of reimbursement coverage for artificial eyes in several healthcare systems further exacerbates affordability concerns, particularly in low-income populations

- Pediatric patients often require frequent replacement and refitting of artificial eyes as they grow, increasing long-term costs and creating financial strain for families

- Addressing these challenges will require expanded ocularist training programs, development of cost-effective prosthetic solutions, and improved reimbursement frameworks to ensure equitable access and sustainable market growth

Artificial Eye Market Scope

The Global Artificial Eye market is segmented on the basis of product, technology, end-use, type, and shell type.

- By Product

On the basis of product, the Artificial Eye market is segmented into Integrated, Semi-Integrated, and Non-Integrated artificial eyes. The Integrated artificial eye segment dominated the largest market revenue share of 46.8% in 2025, driven by its superior aesthetic appearance, enhanced mobility, and better synchronization with natural eye movements. Integrated artificial eyes are designed to work in coordination with orbital implants, allowing improved comfort and a more natural look, which is highly preferred by patients. Growing awareness regarding facial rehabilitation, rising demand for customized prosthetics, and increasing availability of skilled ocularists are further supporting segment dominance. In addition, improved biocompatible materials and technological advancements in implant design continue to enhance patient satisfaction, driving widespread adoption across developed healthcare systems.

The Semi-Integrated artificial eye segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, owing to its cost-effectiveness and balanced functionality. Semi-integrated products offer moderate movement and aesthetic outcomes at a lower price point compared to fully integrated solutions, making them highly attractive in emerging markets. Increasing access to ophthalmic care, growing medical tourism, and rising incidence of eye trauma and congenital ocular disorders are accelerating demand. Furthermore, improving manufacturing techniques and expanding distribution channels are expected to fuel rapid growth during the forecast period.

- By Technology

On the basis of technology, the Artificial Eye market is segmented into Electronic and Mechanical technologies. The Mechanical technology segment held the largest market revenue share of 62.4% in 2025, primarily due to its long-standing clinical acceptance, reliability, and lower cost. Mechanical artificial eyes do not rely on electronic components, making them easier to maintain and widely accessible, especially in low- and middle-income regions. High adoption in hospitals and rehabilitation centers, combined with minimal post-implantation complications, has reinforced the dominance of this segment. In addition, mechanical prostheses remain the preferred option for pediatric and elderly patients due to their simplicity and durability.

The Electronic technology segment is projected to register the fastest CAGR of 9.1% from 2026 to 2033, driven by rapid technological advancements and increasing R&D investments. Electronic artificial eyes offer enhanced movement, improved cosmetic outcomes, and better integration with orbital implants. Growing interest in advanced prosthetic solutions, rising healthcare expenditure, and increasing patient willingness to adopt innovative technologies are key growth drivers. Moreover, continuous improvements in sensor-based systems and lightweight electronic components are expected to significantly boost adoption rates.

- By End-Use

On the basis of end-use, the Artificial Eye market is segmented into Hospitals, Ambulatory Surgical Centers, and Others. The Hospitals segment accounted for the largest market revenue share of 54.2% in 2025, supported by the availability of specialized ophthalmology departments and advanced surgical infrastructure. Hospitals serve as primary centers for complex ocular surgeries, post-trauma rehabilitation, and prosthetic fitting procedures. The presence of skilled surgeons, multidisciplinary care teams, and reimbursement coverage further strengthens hospital dominance. In addition, increasing hospital admissions for eye trauma, cancer-related enucleation, and congenital ocular conditions continue to drive sustained demand.

The Ambulatory Surgical Centers segment is anticipated to witness the fastest CAGR of 8.4% from 2026 to 2033, driven by the shift toward outpatient surgical care. These centers offer faster procedures, reduced hospitalization costs, and shorter recovery times, making them increasingly preferred by patients. Rising adoption of minimally invasive ocular surgeries, growing investments in specialty eye clinics, and improved accessibility are accelerating growth. Furthermore, favorable regulatory support and expanding insurance coverage for outpatient procedures are expected to boost market expansion.

- By Type

On the basis of type, the Artificial Eye market is segmented into Moulded Prosthesis and Cosmetic Shell. The Moulded Prosthesis segment dominated the market with a revenue share of 58.6% in 2025, owing to its customized fit and superior aesthetic outcomes. These prostheses are individually crafted to match the patient’s eye socket and skin tone, offering enhanced comfort and natural appearance. High adoption among patients requiring full ocular replacement and increasing preference for personalized medical solutions are key factors driving dominance. Technological advancements in impression techniques and material processing further support segment leadership.

The Cosmetic Shell segment is expected to grow at the fastest CAGR of 7.6% from 2026 to 2033, fueled by rising demand for non-invasive cosmetic correction. Cosmetic shells are used when the natural eye remains intact but disfigured, offering an affordable and less complex alternative. Increasing awareness about aesthetic rehabilitation, growing acceptance of cosmetic medical devices, and expanding availability in outpatient settings are propelling growth. In addition, shorter fitting time and reduced cost are driving adoption, particularly in emerging economies.

- By Shell Type

On the basis of shell type, the Artificial Eye market is segmented into Single Shell and Double Shell artificial eyes. The Single Shell segment held the largest market revenue share of 51.9% in 2025, due to its simpler design, lighter weight, and widespread clinical usage. Single-shell artificial eyes are easier to manufacture and fit, making them suitable for a wide patient population. Their cost-effectiveness and lower maintenance requirements have led to high adoption in both developed and developing regions. In addition, consistent performance and availability across hospitals and clinics further contribute to segment dominance.

The Double Shell segment is projected to register the fastest CAGR of 8.2% from 2026 to 2033, driven by its enhanced comfort and improved cosmetic outcomes. Double-shell designs offer better adaptability to socket movement and reduced irritation, improving patient satisfaction. Rising demand for advanced prosthetic designs, increasing disposable incomes, and growing focus on quality-of-life improvements are accelerating growth. Ongoing innovations in material flexibility and design precision are expected to further fuel segment expansion during the forecast period.

Artificial Eye Market Regional Analysis

- North America dominated the artificial eye market with a revenue share of approximately 38.5% in 2025, supported by advanced ophthalmic care facilities, higher healthcare spending, strong reimbursement frameworks, and the widespread presence of specialized ocular prosthetic clinic

- The region benefits from early diagnosis of ocular disorders, high awareness regarding cosmetic and functional rehabilitation after eye loss, and access to skilled ocularists

- Continuous advancements in artificial eye materials, digital customization technologies, and improved fitting techniques have enhanced patient satisfaction, reinforcing North America’s leadership position in the global market

U.S. Artificial Eye Market Insight

The U.S. artificial eye market accounted for the largest share within North America, contributing over 80% of regional revenue in 2025, driven by strong awareness levels and well-established ophthalmology and prosthetic care infrastructure. High incidence of ocular trauma, eye cancers such as retinoblastoma and melanoma, and congenital eye disorders continues to generate sustained demand. Favorable insurance coverage for post-surgical ocular rehabilitation and the availability of specialized ocular prosthetic centers further support market growth. Additionally, ongoing innovation in prosthetic aesthetics and comfort is improving quality-of-life outcomes, strengthening adoption across the country.

Europe Artificial Eye Market Insight

The Europe artificial eye market is expected to grow at a steady CAGR over the forecast period, supported by universal healthcare systems, rising prevalence of eye-related disorders, and growing emphasis on post-surgical rehabilitation. Countries across Western Europe benefit from established ophthalmology services and access to trained ocularists, encouraging wider adoption of customized artificial eyes. Increasing awareness regarding psychological and cosmetic restoration following eye loss, combined with advancements in biocompatible prosthetic materials, is contributing to long-term market expansion across the region.

U.K. Artificial Eye Market Insight

The U.K. artificial eye market is projected to expand at a noteworthy CAGR during the forecast period, driven by strong public healthcare support through the National Health Service (NHS). Rising cases of ocular trauma, eye cancers, and congenital anomalies are key contributors to demand. Improved referral systems, availability of specialized ocular prosthetic units, and increasing patient awareness regarding rehabilitation options are further supporting market growth. The U.K.’s commitment to accessible and standardized eye care services continues to create a favorable environment for market expansion.

Germany Artificial Eye Market Insight

Germany artificial eye market is expected to witness considerable growth in the Artificial Eye market over the forecast period, supported by advanced healthcare infrastructure, high medical expenditure, and a strong focus on precision medical technologies. An aging population and increasing incidence of chronic eye diseases and ocular injuries are driving demand for artificial eyes. Germany’s emphasis on high-quality, durable, and biocompatible prosthetic solutions aligns with patient expectations, supporting consistent market development across both public and private healthcare settings.

Asia-Pacific Artificial Eye Market Insight

The Asia-Pacific artificial eye market region is anticipated to register the fastest CAGR during the forecast period, driven by a growing patient pool, rising incidence of ocular trauma, and improving access to eye care services. Increasing awareness of ocular rehabilitation, expanding healthcare infrastructure, and rising healthcare expenditure in countries such as China, India, and Japan are accelerating adoption. Government initiatives aimed at strengthening ophthalmology services and increasing affordability of artificial eyes are further supporting rapid market growth across the region.

Japan Artificial Eye Market Insight

The Japan artificial eye market is experiencing steady growth due to the country’s advanced healthcare system, aging population, and high awareness of post-surgical ocular rehabilitation. Demand is driven by increasing prevalence of eye-related disorders and trauma, along with a strong focus on precision, comfort, and aesthetic quality. Continuous improvements in prosthetic design and fabrication techniques are enhancing patient outcomes, supporting sustained market expansion in Japan.

China Artificial Eye Market Insight

China artificial eye market accounted for the largest revenue share in the Asia-Pacific Artificial Eye market in 2025, driven by rapid urbanization, an expanding middle-class population, and improving access to ophthalmic care services. Rising incidences of ocular trauma, industrial injuries, and untreated eye diseases are contributing significantly to demand. Government investments in healthcare infrastructure and eye care programs, along with the presence of cost-effective domestic manufacturers, are improving accessibility and supporting strong market growth across both urban and semi-urban regions.

Artificial Eye Market Share

The Artificial Eye industry is primarily led by well-established companies, including:

• Carl Zeiss Meditec AG (Germany)

• Johnson & Johnson Vision (U.S.)

• Ocular Prosthetics, Inc. (U.S.)

• International Prosthetic Eye Center (U.S.)

• Stryker (U.S.)

• Second Sight Medical Products (U.S.)

• HumanOptics AG (Germany)

• Polytech Health & Aesthetics (Germany)

• CorneaGen (U.S.)

• Advanced Prosthetic Eyes (Australia)

• Fabtech Healthcare Systems Ltd. (India)

• Morcher GmbH (Germany)

• Orion Vision Group (U.S.)

• OcuLife Eye Prosthetics (Canada)

• Ercon Laboratories (India)

• Mediphacos (Brazil)

• Bionic Vision Technologies (Australia)

Latest Developments in Global Artificial Eye Market

- In February 2024, United Ocular completed the acquisition of Eye Prosthetics of Utah, a specialized ocular prosthetics manufacturer. This strategic move expanded United Ocular’s manufacturing capabilities and patient network for custom-made artificial eyes and scleral shells, reinforcing its position in the global ocular prosthetics market

- In May 2024, Second Sight Medical Products raised USD 30 million in a Series F funding round to accelerate development and commercialization of its Argus Gen2 and Orion retinal implant systems, aimed at advancing vision prosthesis technologies

- In June 2024, Retina Implant AG launched the Alpha AMS retinal prosthesis, a CE-marked product with multi-country deployment, representing an important commercial entry in advanced retinal prosthetics designed to partially restore visual function

- In March 2025, Pixium Vision announced a strategic partnership with Cambridge Consultants to co-develop next-generation subretinal implants and accelerate clinical programs for advanced retinal prostheses. This collaboration is aimed at advancing retinal implant technologies for broader clinical use

- In April 2025, Eye Max Prosthetics unveiled a new silicone ocular prosthesis featuring pigment-matched coloration and improved motility via an updated connecting mechanism, enhancing aesthetic and functional outcomes for patients requiring custom artificial eyes

- In April 2025, the European Commission approved the marketing authorization for the Orion Retinal Prosthesis System, expanding its availability beyond the United States and marking a significant regulatory milestone in retinal prosthesis deployment

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.