Global Artificial Tendons And Ligaments Market

Market Size in USD Billion

CAGR :

%

USD

44.50 Billion

USD

117.46 Billion

2025

2033

USD

44.50 Billion

USD

117.46 Billion

2025

2033

| 2026 –2033 | |

| USD 44.50 Billion | |

| USD 117.46 Billion | |

| % | |

|

Artificial Tendons and Ligaments Market Size

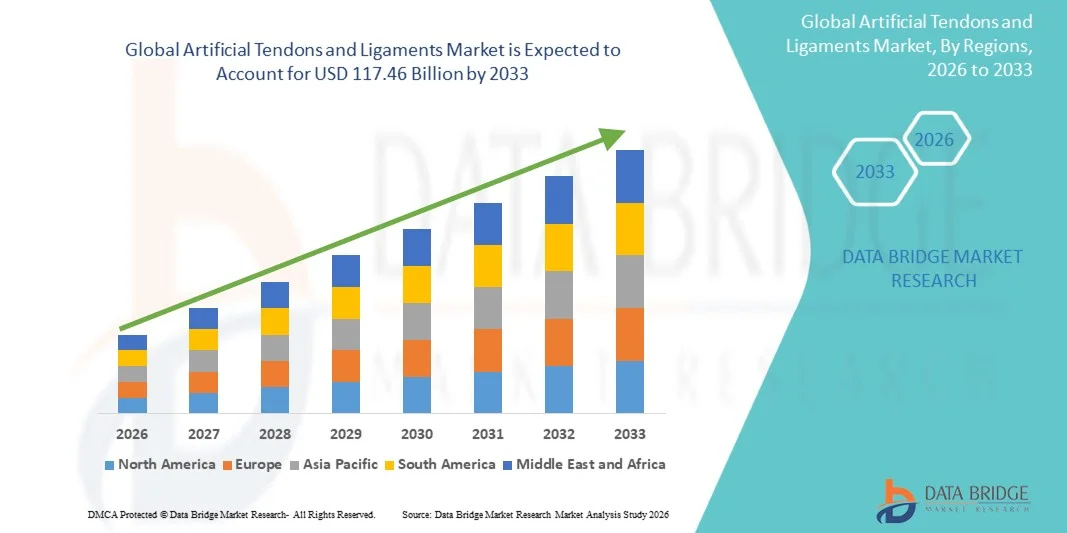

- The global artificial tendons and ligaments market size was valued at USD 44.50 billion in 2025 and is expected to reach USD 117.46 billion by 2033, at a CAGR of 12.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of sports injuries, orthopedic disorders, and rising number of ligament reconstruction surgeries, along with advancements in biomaterials and tissue engineering, leading to greater adoption of artificial tendons and ligaments in clinical applications

- Furthermore, growing demand for minimally invasive surgical procedures, faster recovery times, and improved patient outcomes is establishing artificial tendons and ligaments as a preferred solution in orthopedic treatments. These converging factors are accelerating the uptake of Artificial Tendons and Ligaments solutions, thereby significantly boosting the market growth

Artificial Tendons and Ligaments Market Analysis

- Artificial tendons and ligaments, used for the reconstruction and repair of damaged connective tissues, are becoming increasingly vital in modern orthopedic treatments due to their ability to restore mobility, enhance joint stability, and improve patient outcomes

- The escalating demand for artificial tendons and ligaments is primarily fueled by the rising incidence of sports injuries, growing geriatric population, and increasing number of orthopedic surgeries, along with advancements in biomaterials and tissue engineering technologies

- North America dominated the artificial tendons and ligaments market with the largest revenue share of approximately 41.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of orthopedic procedures, and strong presence of key medical device companies, with the U.S. leading in sports medicine and reconstructive surgeries

- Asia-Pacific is expected to be the fastest growing region in the artificial tendons and ligaments market during the forecast period due to increasing healthcare investments, rising awareness about advanced treatment options, and growing demand for minimally invasive orthopedic procedures

- The Knee Injuries segment dominated the largest market revenue share of 44.7% in 2025, driven by the high prevalence of ACL and ligament injuries worldwide

Report Scope and Artificial Tendons and Ligaments Market Segmentation

|

Attributes |

Artificial Tendons and Ligaments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Artificial Tendons and Ligaments Market Trends

“Advancements in Biomaterials and Regenerative Orthopedic Solutions”

- A significant and accelerating trend in the global artificial tendons and ligaments market is the growing use of advanced biomaterials and regenerative medicine approaches to improve the performance and longevity of implantable orthopedic solutions

- For instance, modern artificial tendons and ligaments are increasingly being developed using biocompatible materials such as polyethylene terephthalate (PET) and other polymer-based composites that mimic the mechanical properties of natural tissues

- Continuous innovations in tissue engineering and scaffold design are enhancing the integration of artificial implants with surrounding biological tissues, improving patient outcomes

- Furthermore, the incorporation of bioactive coatings and growth factors is supporting faster healing and reducing the risk of implant rejection

- Increasing adoption of minimally invasive surgical techniques is also promoting the use of advanced artificial ligament and tendon implants

- This trend toward more durable, biocompatible, and regenerative orthopedic solutions is significantly shaping the global Artificial Tendons and Ligaments market

Artificial Tendons and Ligaments Market Dynamics

Driver

“Rising Incidence of Sports Injuries and Orthopedic Disorders”

- The increasing global prevalence of sports-related injuries and musculoskeletal disorders is a major driver of the Artificial Tendons and Ligaments market

- For instance, injuries such as anterior cruciate ligament (ACL) tears, rotator cuff injuries, and tendon ruptures are becoming more common due to active lifestyles and participation in sports activities

- Growing awareness regarding advanced treatment options and faster recovery solutions is encouraging patients to opt for artificial implants over traditional treatments

- In addition, the rising geriatric population, which is more prone to degenerative joint conditions, is further supporting market growth

- Expanding healthcare infrastructure and improved access to orthopedic surgical procedures in emerging economies are also contributing to increased adoption

- Increasing investments in orthopedic research and development are further accelerating innovation and market expansion globally

Restraint/Challenge

“High Cost of Implants and Risk of Post-Surgical Complications”

- The high cost associated with artificial tendons and ligament implants remains a significant challenge, particularly in developing and price-sensitive markets

- Advanced surgical procedures and implant materials can increase the overall cost of treatment, limiting accessibility for a large patient population

- For instance, complex ligament reconstruction surgeries involving high-quality synthetic grafts and specialized surgical techniques can be financially burdensome for patients without adequate insurance coverage

- In addition, risks associated with post-surgical complications such as infection, implant failure, or inflammation may affect patient acceptance

- Limited availability of skilled orthopedic surgeons and advanced surgical facilities in certain regions further restricts market growth

- Variability in reimbursement policies and healthcare funding across countries can also impact adoption rates

- Addressing these challenges through cost-effective innovations, improved surgical techniques, and enhanced patient awareness will be essential for sustained growth of the Artificial Tendons and Ligaments market

Artificial Tendons and Ligaments Market Scope

The market is segmented on the basis of implants, materials, application, and end user.

• By Implants

On the basis of implants, the Artificial Tendons and Ligaments market is segmented into Silastic-Rod Implant, Carbon-Fiber Implant, and Marlex Mesh. The Carbon-Fiber Implant segment dominated the largest market revenue share of 41.8% in 2025, driven by its superior strength, biocompatibility, and durability in orthopedic reconstruction procedures. Carbon-fiber implants are widely preferred due to their high tensile strength and ability to mimic natural tendon and ligament behavior. Increasing prevalence of sports injuries and trauma cases is significantly boosting demand for these implants. Surgeons favor carbon-fiber implants for their reliability and long-term performance outcomes. Technological advancements in composite materials are further enhancing implant efficiency. Growing adoption in minimally invasive surgical procedures is also supporting segment growth. Hospitals are increasingly incorporating advanced implant materials to improve patient recovery rates. Rising geriatric population suffering from musculoskeletal disorders is contributing to demand. North America dominates this segment due to advanced healthcare infrastructure and high surgical volumes. Europe is also witnessing steady growth owing to rising orthopedic procedures. Continuous innovation in biomaterials is strengthening the segment’s position. Overall, this segment remains the leading contributor due to its clinical effectiveness and durability.

The Silastic-Rod Implant segment is expected to witness the fastest CAGR of 18.6% from 2026 to 2033, driven by increasing use in staged tendon reconstruction procedures. These implants are widely utilized in complex cases where temporary support is required before permanent reconstruction. Rising awareness among surgeons regarding flexible and adaptable implant options is supporting adoption. Silastic rods offer advantages such as ease of insertion and reduced tissue damage. Growing demand for reconstructive surgeries in developing regions is further accelerating growth. Advancements in silicone-based biomaterials are improving safety and performance. Increasing number of trauma and accident cases globally is contributing to segment expansion. Healthcare providers are focusing on improving surgical outcomes with innovative implant solutions. Expanding healthcare infrastructure in emerging markets is supporting adoption. Research activities aimed at improving implant longevity are also driving innovation. Government investments in orthopedic care are boosting procedural volumes. Overall, this segment is growing rapidly due to its versatility and expanding clinical applications.

• By Materials

On the basis of materials, the Artificial Tendons and Ligaments market is segmented into Carbon, Carbon and Polyester, Leeds-Keio Polyester, Dacron, Bovine Glutaraldehyde-Fixed Xenograft, and Gore-Tex Polytetrafluoroethylene. The Carbon material segment dominated the largest market revenue share of 36.9% in 2025, driven by its high mechanical strength and excellent compatibility with human tissues. Carbon-based materials are widely used due to their durability and ability to withstand repetitive stress. Increasing demand for long-lasting orthopedic solutions is supporting segment dominance. Surgeons prefer carbon materials for their predictable performance in ligament reconstruction. Technological advancements in carbon composites are improving flexibility and safety. Rising number of sports-related injuries is boosting demand for robust implant materials. Healthcare facilities are adopting advanced materials to enhance surgical success rates. North America leads due to high adoption of advanced biomaterials. Europe is also witnessing strong demand due to increasing orthopedic procedures. Continuous R&D investments are enhancing product innovation. Growing awareness regarding advanced implant materials is further driving adoption. Overall, carbon materials remain the preferred choice due to reliability and clinical outcomes.

The Gore-Tex Polytetrafluoroethylene segment is expected to witness the fastest CAGR of 17.4% from 2026 to 2033, driven by its excellent biocompatibility and flexibility. This material is gaining traction due to its ability to reduce inflammation and improve patient comfort. Increasing demand for minimally invasive and patient-friendly solutions is supporting growth. Gore-Tex materials offer superior resistance to wear and tear, enhancing implant longevity. Rising focus on advanced synthetic graft materials is boosting adoption. Healthcare providers are increasingly adopting these materials for complex reconstruction procedures. Growing investments in biomaterial research are accelerating innovation. Emerging economies are witnessing rising demand due to improving healthcare access. Technological advancements are improving product safety and effectiveness. Increasing awareness among surgeons is supporting clinical adoption. Expanding applications in ligament and tendon repair are further driving growth. Overall, this segment is growing rapidly due to its advanced properties and patient-centric benefits.

• By Application

On the basis of application, the Artificial Tendons and Ligaments market is segmented into Knee Injuries, Shoulder Injuries, Foot and Ankle Injuries, and Other Injuries. The Knee Injuries segment dominated the largest market revenue share of 44.7% in 2025, driven by the high prevalence of ACL and ligament injuries worldwide. Increasing participation in sports and physical activities is leading to a surge in knee-related injuries. Knee reconstruction surgeries are among the most commonly performed orthopedic procedures globally. Growing awareness regarding early treatment and surgical intervention is supporting segment growth. Technological advancements in surgical techniques are improving patient outcomes. Hospitals are increasingly adopting advanced implants for knee reconstruction. Rising geriatric population with joint-related disorders is also contributing to demand. North America leads due to high sports injury incidence and advanced healthcare systems. Europe follows with increasing orthopedic procedures. Continuous innovation in ligament repair technologies is boosting adoption. Government initiatives promoting sports safety are indirectly supporting growth. Overall, this segment dominates due to high procedure volume and clinical necessity.

The Shoulder Injuries segment is expected to witness the fastest CAGR of 16.8% from 2026 to 2033, driven by increasing cases of rotator cuff injuries and sports-related trauma. Rising awareness about shoulder reconstruction procedures is boosting demand. Advances in minimally invasive arthroscopic techniques are supporting segment growth. Increasing aging population is prone to shoulder degeneration and injuries. Healthcare providers are focusing on improving mobility and quality of life for patients. Growing adoption of artificial ligaments in shoulder repair is accelerating market expansion. Expanding healthcare infrastructure in emerging markets is supporting treatment access. Surgeons are increasingly adopting advanced implants for better recovery outcomes. Technological innovations are improving surgical precision and success rates. Rising demand for outpatient procedures is also contributing to growth. Increased participation in fitness activities is leading to higher injury rates. Overall, this segment is expanding rapidly due to rising awareness and improved treatment options.

• By End User

On the basis of end user, the Artificial Tendons and Ligaments market is segmented into Hospitals and Clinics and Ambulatory Surgery Centers. The Hospitals and Clinics segment dominated the largest market revenue share of 62.3% in 2025, driven by the availability of advanced surgical infrastructure and skilled healthcare professionals. Hospitals serve as primary centers for complex orthopedic procedures and trauma care. Increasing patient admissions for ligament and tendon injuries are supporting segment growth. Availability of advanced diagnostic and surgical technologies enhances treatment outcomes. Hospitals are preferred due to comprehensive post-operative care facilities. Rising healthcare expenditure is further strengthening this segment. North America dominates due to well-established hospital networks. Europe also contributes significantly due to high procedural volumes. Continuous investment in hospital infrastructure is improving service delivery. Growing number of specialized orthopedic centers is boosting adoption. Increasing insurance coverage for surgical procedures supports patient access. Overall, this segment remains dominant due to its comprehensive care capabilities.

The Ambulatory Surgery Centers segment is expected to witness the fastest CAGR of 15.9% from 2026 to 2033, driven by increasing preference for cost-effective and minimally invasive procedures. ASCs offer shorter hospital stays and faster recovery times, making them attractive to patients. Rising adoption of outpatient surgical procedures is significantly boosting growth. Technological advancements are enabling complex surgeries to be performed in outpatient settings. Healthcare systems are promoting ASCs to reduce hospital burden and costs. Increasing patient awareness regarding convenience and affordability is supporting adoption. Expansion of ASC facilities in emerging markets is further accelerating growth. Surgeons are increasingly performing ligament reconstruction procedures in these centers. Favorable reimbursement policies are also supporting segment expansion. Growing demand for same-day surgeries is driving market growth. Improved surgical equipment and techniques are enhancing outcomes in ASCs. Overall, this segment is rapidly growing due to efficiency, affordability, and patient preference.

Artificial Tendons and Ligaments Market Regional Analysis

- North America dominated the artificial tendons and ligaments market with the largest revenue share of approximately 41.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of orthopedic procedures, and a strong presence of key medical device companies

- The region benefits from a high volume of sports injuries, increasing incidence of musculoskeletal disorders, and widespread access to advanced surgical treatments. The U.S. leads the region in sports medicine and reconstructive surgeries, supported by well-established healthcare facilities and skilled professionals

- Rising demand for minimally invasive orthopedic procedures, increasing aging population, and growing awareness of advanced treatment options are key factors driving market growth. Technological advancements in biomaterials and synthetic grafts are further enhancing the adoption of artificial tendons and ligaments across North America

U.S. Artificial Tendons and Ligaments Market Insight

The U.S. artificial tendons and ligaments market captured the largest revenue share within North America in 2025, driven by high adoption of advanced orthopedic procedures and strong presence of leading medical device manufacturers. The country’s focus on sports medicine, coupled with increasing cases of ligament injuries such as ACL tears, is significantly boosting demand. In addition, continuous innovation in surgical techniques and implant materials is supporting market expansion.

Europe Artificial Tendons and Ligaments Market Insight

The Europe artificial tendons and ligaments market is projected to expand at a substantial CAGR during the forecast period, supported by rising incidence of orthopedic disorders and increasing adoption of advanced surgical treatments. Well-established healthcare systems and growing investment in medical technologies are contributing to market growth. In addition, rising awareness about early treatment and rehabilitation is further driving demand.

U.K. Artificial Tendons and Ligaments Market Insight

The U.K. artificial tendons and ligaments market is anticipated to grow at a noteworthy CAGR, driven by increasing demand for sports injury treatments and reconstructive surgeries. The presence of strong public healthcare infrastructure and growing focus on minimally invasive procedures are supporting adoption. Increasing participation in sports and physical activities is also contributing to market growth.

Germany Artificial Tendons and Ligaments Market Insight

The Germany artificial tendons and ligaments market is expected to expand at a considerable CAGR, fueled by advanced healthcare infrastructure and strong emphasis on precision orthopedic care. Germany’s well-developed medical device industry and focus on innovation are promoting the adoption of high-quality artificial grafts and implants. Increasing demand for joint repair and reconstruction procedures is further supporting market growth.

Asia-Pacific Artificial Tendons and Ligaments Market Insight

The Asia-Pacific artificial tendons and ligaments market is expected to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, rising awareness about advanced treatment options, and growing demand for minimally invasive orthopedic procedures. Expanding healthcare infrastructure and improving access to specialized orthopedic care are key factors accelerating market growth across the region.

Japan Artificial Tendons and Ligaments Market Insight

The Japan artificial tendons and ligaments market is gaining momentum due to its advanced healthcare system and rapidly aging population, which is more prone to musculoskeletal disorders. High adoption of innovative surgical techniques and strong focus on rehabilitation are supporting market expansion. In addition, increasing demand for effective and durable orthopedic implants is driving growth.

China Artificial Tendons and Ligaments Market Insight

The China artificial tendons and ligaments market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid healthcare infrastructure development and rising demand for orthopedic treatments. Increasing incidence of sports injuries and growing awareness of advanced surgical options are boosting adoption. Furthermore, government initiatives to improve healthcare access and expanding hospital networks are key factors supporting market growth in China.

Artificial Tendons and Ligaments Market Share

The Artificial Tendons and Ligaments industry is primarily led by well-established companies, including:

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Smith & Nephew plc (U.K.)

- Johnson & Johnson (U.S.)

- Arthrex, Inc. (U.S.)

- Medtronic plc (Ireland)

- Integra LifeSciences Holdings Corporation (U.S.)

- CONMED Corporation (U.S.)

- B. Braun SE (Germany)

- DJO Global, Inc. (U.S.)

- Exactech, Inc. (U.S.)

- Corin Group plc (U.K.)

- RTI Surgical Holdings, Inc. (U.S.)

- Xiros Ltd. (U.K.)

- Neoligaments (U.K.)

- FH Orthopedics (France)

- Mathys AG Bettlach (Switzerland)

- BioPoly LLC (U.S.)

- Ossur hf. (Iceland)

- Wright Medical Group N.V. (Netherlands)

Latest Developments in Global Artificial Tendons and Ligaments Market

- In April 2022, CoNextions received FDA 510(k) clearance for its TR Tendon Repair System, developed for tendon lacerations in the hand, wrist, and forearm. The system offered stronger and faster repair compared with traditional suturing methods, marking a notable advancement in synthetic tendon repair technology

- In September 2023, manufacturers increasingly focused on biomaterials and tissue engineering technologies that improve strength, flexibility, and biocompatibility of artificial tendons and ligaments. These innovations supported better long-term clinical outcomes and wider use in orthopedic surgeries

- In July 2024, Stryker, a leading global medical technology company, completed the acquisition of Artelon, a company specializing in innovative soft tissue fixation products for foot and ankle and sports medicine procedures. Artelon’s synthetic technology is designed to enhance biological and mechanical ligament and tendon reconstruction, with over 60,000 implantations worldwide. This acquisition strengthened Stryker’s offerings in tendon and ligament repair solutions and reinforced its leadership in sports medicine and orthopedic reconstruction

- In June 2024, Stryker announced the signing of a definitive agreement to acquire Artelon, expanding its portfolio of differentiated solutions for ligament and tendon reconstruction. The move highlighted growing strategic investments in artificial tendon and ligament technologies aimed at improving surgical outcomes and soft tissue healing

- In May 2024, Enovis Corporation opened a new medical device production facility in San Daniele, Italy, significantly increasing manufacturing capacity for orthopedic and soft tissue repair products, including tendon and ligament reconstruction solutions. This expansion supported rising global demand for advanced orthopedic implants and surgical technologies

- In February 2024, Smith+Nephew unveiled its expanded Sports Medicine portfolio at the AAOS Annual Meeting, featuring the REGENETEN Bioinductive Implant, designed to support biological healing of tendon injuries. This development reflected the increasing shift toward regenerative and bio-integrative solutions in tendon and ligament repair

- In January 2024, Arthrex promoted advancements in Nano arthroscopy technology, a minimally invasive orthopedic surgical technique enabling faster recovery and reduced pain in tendon and ligament procedures. This development highlighted the growing use of minimally invasive approaches in soft tissue reconstruction

- In March 2025, ongoing innovation in artificial tendons and ligaments centered on tissue-engineered constructs and next-generation biomaterials designed to mimic natural tendon structure and function. These advancements are expected to further enhance recovery outcomes and expand treatment adoption globally

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.