Global Autologous Stem Cell And Non Stem Cell Based Therapies Market

Market Size in USD Billion

CAGR :

%

USD

116.71 Billion

USD

162.82 Billion

2025

2033

USD

116.71 Billion

USD

162.82 Billion

2025

2033

| 2026 –2033 | |

| USD 116.71 Billion | |

| USD 162.82 Billion | |

| % | |

|

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Size

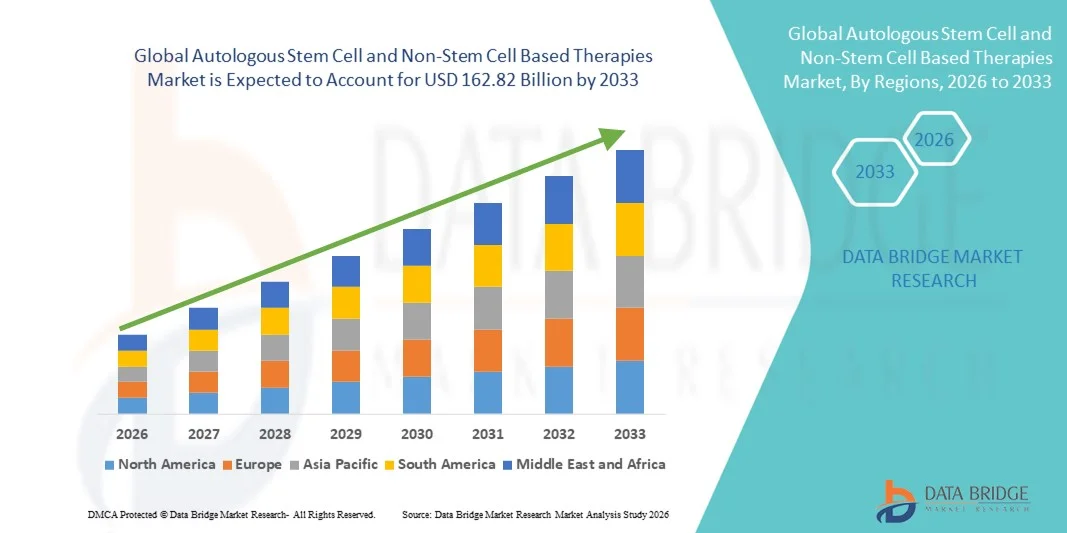

- The global autologous stem cell and non-stem cell based therapies market size was valued at USD 116.71 billion in 2025 and is expected to reach USD 162.82 billion by 2033, at a CAGR of 4.25% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within connected healthcare and regenerative medicine technologies, leading to increased availability of advanced cell therapy solutions in both clinical and research settings

- Furthermore, rising patient demand for personalized, safe, and effective treatment options is establishing autologous stem cell and non-stem cell based therapies as critical interventions for various degenerative and hematological disorders. These converging factors are accelerating the uptake of Autologous Stem Cell and Non-Stem Cell Based Therapies solutions, thereby significantly boosting the industry's growth

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Analysis

- Cell-based therapies, including autologous stem cell and non-stem cell based treatments, are increasingly vital components of modern regenerative medicine and advanced clinical care due to their targeted efficacy, personalized treatment potential, and integration with cutting-edge therapeutic platforms

- The escalating demand for these therapies is primarily fueled by the rising prevalence of degenerative, hematological, and autoimmune disorders, growing awareness of regenerative medicine benefits, and an increasing preference for minimally invasive, personalized treatment options

- North America dominated the autologous stem cell and non-stem cell based therapies market with the largest revenue share of 43.7% in 2025, characterized by well-established healthcare infrastructure, high adoption of advanced therapies, and a strong presence of key industry players, with the U.S. experiencing substantial growth in therapy adoption, driven by innovations from both established biotech companies and startups focusing on gene and cell therapy platforms

- Asia-Pacific is expected to be the fastest growing region in the autologous stem cell and non-stem cell based therapies market during the forecast period, with a projected CAGR of 13.2%, due to increasing research investments, supportive regulatory frameworks, rising patient demand for advanced regenerative therapies, and expanding healthcare access in emerging economies

The Autol ogous Stem Cells segment dominated the largest market revenue share of 54.3% in 2025, driven by their established efficacy in tissue regeneration and personalized therapeutic applications

ogous Stem Cells segment dominated the largest market revenue share of 54.3% in 2025, driven by their established efficacy in tissue regeneration and personalized therapeutic applications

Report Scope and Autologous Stem Cell and Non-Stem Cell Based Therapies Market Segmentation

|

Attributes |

Autologous Stem Cell and Non-Stem Cell Based Therapies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Trends

Rising Demand for Advanced Regenerative Treatments

- The global demand for autologous stem cell and non-stem cell-based therapies is being driven by the increasing prevalence of chronic diseases, degenerative conditions, and traumatic injuries. Patients and healthcare providers are seeking advanced regenerative medicine solutions that can improve recovery outcomes and reduce long-term healthcare costs

- For instance, in June 2024, Mesoblast Limited announced the expansion of its clinical trial program for allogeneic and autologous stem cell therapies targeting cardiovascular and orthopedic disorders, demonstrating strong industry commitment to innovation

- The trend towards personalized medicine, where therapies are tailored to individual patient profiles, is encouraging investment in autologous therapies, while non-stem cell approaches, such as platelet-rich plasma (PRP) and exosome therapies, are gaining traction for their safety and effectiveness

- Advancements in biomanufacturing and cellular processing technologies are further facilitating the scalability and accessibility of these therapies, enabling hospitals and specialized clinics to offer cutting-edge regenerative treatments

- The rising awareness among patients, coupled with increasing physician adoption of regenerative approaches, is fostering robust growth across both developed and emerging markets

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Dynamics

Driver

Expansion of Clinical Research and Regulatory Approvals

- A key trend shaping this market is the rapid increase in clinical trials, research initiatives, and regulatory approvals for both autologous and non-stem cell therapies. This trend underscores the growing maturity of the regenerative medicine sector

- For instance, in March 2023, the U.S. FDA granted Fast Track designation to a new CAR-T-based autologous therapy for hematologic malignancies, reflecting accelerating regulatory support for innovative therapies

- The development of standardized protocols for cell isolation, culture, and administration is improving the reliability and safety of treatments, which in turn is attracting new market entrants and venture capital investment

- Academic and industry collaborations, particularly in North America, Europe, and Asia-Pacific, are enhancing the pace of innovation and enabling the translation of experimental therapies into commercially viable products

- The integration of precision medicine principles and biomarker-driven patient selection is also shaping treatment strategies, leading to higher efficacy and better clinical outcomes

Restraint/Challenge

High Costs and Limited Accessibility in Certain Regions

- The high cost of autologous and advanced non-stem cell therapies poses a challenge to broader market adoption, particularly in price-sensitive regions and for patients without comprehensive insurance coverage

- For instance, stem cell therapies for orthopedic or cardiovascular indications can exceed tens of thousands of dollars per treatment, limiting access despite their clinical efficacy

- Complex manufacturing processes, stringent quality control requirements, and regulatory compliance add to production costs, while logistical challenges such as cryopreservation, transportation, and cold chain management further impact accessibility

- In addition, inconsistent reimbursement policies and limited awareness in certain developing markets are restraining adoption, as many healthcare providers and patients remain hesitant to adopt high-cost, novel therapies

- Overcoming these challenges through scalable manufacturing, cost-reduction strategies, and expanded insurance coverage will be critical for achieving sustained growth in the autologous and non-stem cell therapy sector

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Scope

The market is segmented on the basis of type, product, applications, and end-user.

- By Type

On the basis of type, the market is segmented into Autologous Stem Cells and Autologous Non-Stem Cells. The Autologous Stem Cells segment dominated the largest market revenue share of 54.3% in 2025, driven by their established efficacy in tissue regeneration and personalized therapeutic applications. Stem cell therapies are increasingly adopted for neurodegenerative disorders, autoimmune diseases, and cardiovascular repair. Hospitals and specialty centers favor autologous stem cells due to reduced risk of immune rejection and high patient-specific compatibility. Clinical evidence supports improved patient outcomes and faster recovery times. Stem cell banks and processing facilities enhance availability. Continuous innovation in isolation and expansion techniques strengthens market presence. Regulatory approvals in key markets improve adoption. Integration with advanced delivery systems ensures precision therapy. High patient acceptance and positive safety profiles further reinforce dominance. Insurance reimbursement schemes for stem cell treatments are expanding. Research collaborations between academia and industry support pipeline growth. Adoption in regenerative medicine programs enhances clinical acceptance. These factors collectively maintain autologous stem cells as the leading type segment in 2025.

The Autologous Non-Stem Cells segment is projected to witness the fastest growth at a CAGR of 12.8% from 2026 to 2033, driven by increasing use of immune cell therapies, platelet-rich plasma (PRP), and other cell-based interventions. Non-stem cell therapies are gaining traction for oncology support, cardiovascular repair, and wound healing. Hospital and ambulatory surgical centers are expanding infrastructure to support these therapies. Advanced processing technologies improve cell viability and clinical outcomes. Rising awareness among clinicians and patients accelerates adoption. Integration with combination therapies enhances efficacy. Growing clinical trials and approval of novel autologous cell products fuel market expansion. Favorable reimbursement and government incentives in regenerative medicine increase access. Training programs for medical staff ensure safe administration. Rising prevalence of chronic and degenerative diseases supports demand. Home-based and outpatient therapy models contribute to increased utilization. These combined drivers position autologous non-stem cells as the fastest-growing type segment.

- By Product

On the basis of product, the market is segmented into Blood Pressure (BP) Monitoring Devices, Pulmonary Pressure Monitoring Devices, and Intracranial Pressure (ICP) Monitoring Devices. The BP Monitoring Devices segment dominated with a 46.5% revenue share in 2025, owing to widespread clinical use in cardiovascular disease management and monitoring therapy outcomes. Continuous patient monitoring supports early detection of complications. Hospitals and clinics prioritize BP devices for preoperative and postoperative assessments. Integration with digital platforms enhances real-time data tracking. Standardized protocols improve treatment accuracy. High adoption in homecare and outpatient settings further supports market dominance. Compatibility with mobile apps allows remote monitoring and alerts. Increasing prevalence of hypertension drives demand. Automated devices reduce manual intervention, improving workflow efficiency. Reusable sensors and connectivity features support long-term cost-effectiveness. Hospital investment in multi-parameter monitoring expands adoption. Physician preference and patient familiarity reinforce segment dominance. These factors collectively sustain BP monitoring devices as the leading product segment.

The Pulmonary Pressure Monitoring Devices segment is expected to witness the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by rising prevalence of pulmonary hypertension, heart failure, and critical care interventions. Hospitals and specialized centers are increasingly deploying minimally invasive devices for real-time pressure monitoring. Integration with ICU management systems ensures continuous patient assessment. Advanced sensor technology enhances data accuracy and safety. Expansion of ambulatory monitoring programs supports growth. Awareness of pulmonary complications in chronic diseases drives adoption. Telehealth integration allows remote tracking of pulmonary pressures. Rising approvals for implantable and wearable devices further accelerate uptake. Training of healthcare professionals strengthens clinical confidence. Increased patient demand for precision monitoring fuels market expansion. Government initiatives supporting critical care infrastructure enhance penetration. Research programs and clinical trials contribute to innovation. These combined factors make pulmonary pressure monitoring devices the fastest-growing product segment.

- By Applications

On the basis of applications, the market is segmented into Neurodegenerative Disorders, Autoimmune Diseases, Cancer and Tumors, and Cardiovascular Diseases. The Cancer and Tumors segment dominated with a 48.7% revenue share in 2025, owing to the widespread adoption of autologous cell therapies in oncology. Hematologic malignancies and solid tumors increasingly rely on cell-based interventions. Hospitals and ambulatory surgical centers deploy therapies as adjuncts to chemotherapy, radiation, and immunotherapy. Clinical studies demonstrate improved remission and survival rates. Personalized therapy options enhance treatment efficacy. Regulatory approvals support expanded clinical use. Rising patient awareness and demand for precision oncology fuel adoption. Integration with digital treatment monitoring improves outcomes. Specialized oncology centers expand treatment capacity. Collaboration between research institutes and hospitals accelerates innovation. Insurance coverage for targeted therapies supports uptake. Early diagnosis and intervention drive high-volume usage. Continuous expansion of treatment pipelines reinforces market dominance in 2025.

The Neurodegenerative Disorders segment is projected to witness the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by increasing prevalence of Alzheimer’s, Parkinson’s, and multiple sclerosis. Autologous stem cell therapies show promise in neuroregeneration and slowing disease progression. Hospitals and specialty centers are establishing dedicated programs for neurodegenerative therapy. Clinical trials demonstrate safety and efficacy, boosting physician adoption. Integration with rehabilitation and homecare services enhances therapy accessibility. Innovative delivery techniques, including intrathecal and intranasal routes, expand clinical utility. Supportive government funding for neurodegenerative research accelerates adoption. Patient advocacy and awareness campaigns strengthen demand. Expansion of global stem cell registries supports therapy matching. Early intervention strategies improve long-term outcomes. Telemedicine and remote monitoring support ongoing treatment management. These factors collectively position neurodegenerative therapies as the fastest-growing application segment.

- By End-User

On the basis of end-user, the market is segmented into Hospitals and Ambulatory Surgical Centers. The Hospitals segment dominated with a 57.9% revenue share in 2025, owing to advanced infrastructure, specialized staff, and high patient throughput for complex autologous therapies. Hospitals maintain stem cell processing units, supporting multiple therapy types. High inpatient volumes for oncology, cardiovascular, and autoimmune diseases drive revenue. Investment in ICU and monitoring facilities ensures safe therapy delivery. Favorable reimbursement policies enhance adoption. Integration with hospital IT systems improves treatment tracking and reporting. Hospitals participate in clinical trials, supporting early access to novel therapies. Long-term patient monitoring programs increase therapy adherence. Collaboration with research institutes strengthens pipeline access. Skilled hematologists and regenerative medicine teams ensure safe administration. Expansion of hospital networks supports scalability. These factors collectively reinforce hospitals as the dominant end-user segment in 2025.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth at a CAGR of 13.4% from 2026 to 2033, driven by increasing demand for outpatient autologous therapies and minimally invasive procedures. Centers offer focused services for oncology, autoimmune, and cardiovascular treatments. Shorter hospital stays and reduced healthcare costs drive patient preference. Technological advancements in portable stem cell processing devices support adoption. Integration with homecare and telemedicine services enhances accessibility. Rising patient awareness and convenience of outpatient care accelerate demand. Regulatory approvals for outpatient therapy delivery expand opportunities. Growing insurance coverage supports treatment affordability. Expansion of private ambulatory centers enhances regional access. Training programs for specialized staff ensure high-quality care. Telemonitoring and remote follow-up programs improve patient outcomes. These combined drivers position ambulatory surgical centers as the fastest-growing end-user segment.

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Regional Analysis

- North America dominated the autologous stem cell and non-stem cell based therapies market with the largest revenue share of 43.7% in 2025

- Characterized by well-established healthcare infrastructure, high adoption of advanced therapies, and a strong presence of key industry players

- The region benefits from favorable reimbursement policies, high healthcare expenditure, and robust R&D investments, enabling rapid commercialization of advanced regenerative therapies

U.S. Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

The U.S. autologous stem cell and non-stem cell based therapies market captured the majority of regional revenue in 2025, witnessing substantial growth in therapy adoption. This growth is driven by innovations from both established biotech companies and startups focusing on gene and cell therapy platforms. High patient awareness, supportive healthcare policies, and a strong network of clinical research centers further fuel market expansion.

Europe Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

Europe autologous stem cell and non-stem cell based therapies market is projected to grow steadily during the forecast period, supported by increasing investments in biotechnology and regenerative medicine, as well as strong clinical research initiatives across Germany, the U.K., and France. Stringent regulatory frameworks and well-established healthcare systems are facilitating the adoption of autologous and non-stem cell therapies in hospitals and specialized clinics. Growing awareness among physicians and patients, coupled with the region’s focus on innovative treatments for hematologic and orthopedic conditions, is further driving market expansion.

U.K. Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

The U.K. autologous stem cell and non-stem cell based therapies market is anticipated to grow at a healthy CAGR during the forecast period, fueled by government support for regenerative medicine, increasing clinical trials, and rising patient awareness. Investment in research and collaboration between academic institutions and biotech companies is helping accelerate the development of advanced therapies. The country’s healthcare infrastructure, combined with favorable funding mechanisms, encourages the adoption of both autologous and non-stem cell-based regenerative treatments.

Germany Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

Germany autologous stem cell and non-stem cell based therapies market is expected to maintain steady growth, driven by technological advancements, well-established clinical facilities, and high healthcare expenditure. The government’s strong support for regenerative medicine research and innovation, along with collaborations between academic and private sectors, is promoting therapy adoption. Demand for advanced treatments for cardiovascular, orthopedic, and hematologic disorders is further expanding the market in Germany.

Asia-Pacific Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

Asia-Pacific autologous stem cell and non-stem cell based therapies market is expected to be the fastest growing region in the autologous stem cell and non-stem cell-based therapies market during the forecast period, with a projected CAGR of 13.2%. Growth is driven by increasing research investments, supportive regulatory frameworks, rising patient demand for advanced regenerative therapies, and expanding healthcare access in emerging economies such as China, India, and South Korea. The expansion of clinical research centers, medical tourism, and government-backed healthcare initiatives are significantly contributing to market development.

Japan Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

Japan’s autologous stem cell and non-stem cell based therapies market is growing steadily due to a high prevalence of chronic and degenerative diseases, a strong emphasis on cutting-edge medical research, and well-developed healthcare infrastructure. Investment in regenerative medicine and government initiatives supporting stem cell therapy commercialization are key growth drivers. Rising patient awareness and demand for advanced therapies, including autologous treatments, is accelerating adoption across hospitals and specialized clinics.

China Autologous Stem Cell and Non-Stem Cell Based Therapies Market Insight

China autologous stem cell and non-stem cell based therapies market accounted for the largest revenue share in Asia-Pacific in 2025, owing to rapid urbanization, an expanding middle class, and increasing prevalence of chronic diseases. The government’s proactive regulatory support for cell and gene therapy, growing domestic biotech manufacturing capabilities, and rising healthcare expenditure are propelling market growth. Increasing clinical trials, collaborations between domestic and international biotech firms, and a growing patient base seeking regenerative therapies are further boosting the Chinese market.

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Share

The Autologous Stem Cell and Non-Stem Cell Based Therapies industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical (Japan)

- Roche (Switzerland)

- Novartis (Switzerland)

- Gilead Sciences (U.S.)

- Bristol-Myers Squibb (U.S.)

- Biogen (U.S.)

- Celgene (U.S.)

- Amgen (U.S.)

- Fresenius Kabi (Germany)

- Sanofi (France)

- Sigma-Aldrich (U.S.)

- Cytiva (U.S.)

- Stemcell Technologies (Canada)

- Bluebird Bio (U.S.)

- Mesoblast (Australia)

- Kite Pharma (U.S.)

- Legend Biotech (China)

- Fate Therapeutics (U.S.)

- Lonza Group (Switzerland)

Latest Developments in Global Autologous Stem Cell and Non-Stem Cell Based Therapies Market

- In March 2025, AstraZeneca announced its agreement to acquire EsoBiotec, a Belgian biotech specializing in technology that can genetically modify immune cells within the body, in a deal worth up to USD 1 billion aimed at accelerating in‑vivo cell therapy capabilities for cancer and other diseases

- In June 2025, the U.S. FDA approved label updates for CAR‑T cell therapies Breyanzi (liso‑cel) and Abecma (ide‑cel), reducing monitoring requirements and eliminating certain REMS programs to increase patient access for individuals with large B‑cell lymphoma and multiple myeloma, respectively

- In April 2024, Vertex Pharmaceuticals obtained an exclusive license for TreeFrog Therapeutics’ C‑Stem™ technology to enhance production of cell therapies for type 1 diabetes, enabling scalable generation of fully differentiated cells for therapeutic use

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.