Global Automatic Fare Collection System Market

Market Size in USD Billion

CAGR :

%

USD

70.24 Billion

USD

198.69 Billion

2025

2033

USD

70.24 Billion

USD

198.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 70.24 Billion | |

| USD 198.69 Billion | |

| % | |

|

Automatic Fare Collection System Market Overview

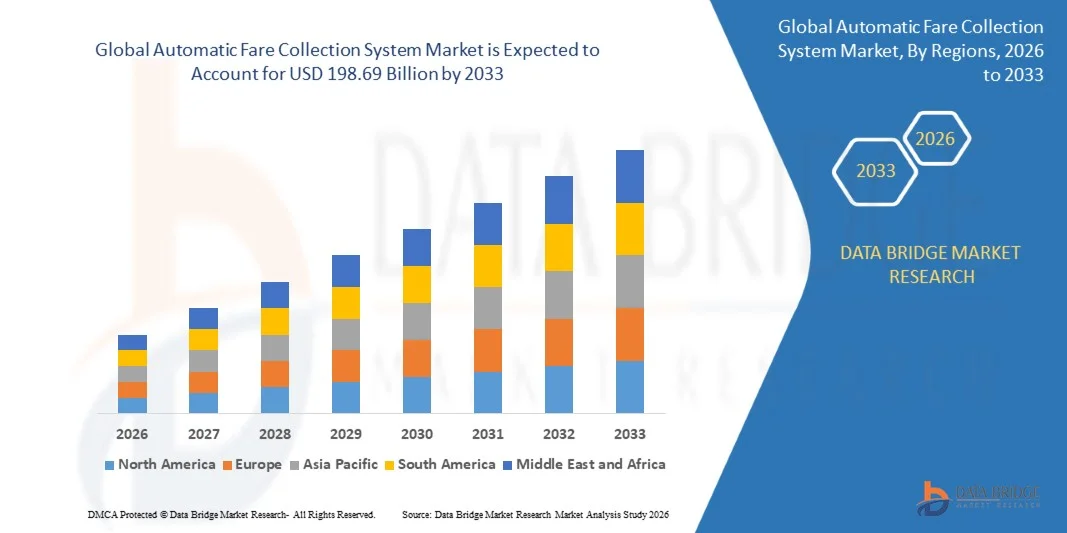

The Automatic Fare Collection System Market was valued at USD 70.24 billion in 2025 and is projected to reach USD 198.69 billion by 2033, growing at a CAGR of 13.88% from 2026 to 2033. The market is experiencing rapid expansion driven by increasing urbanization, rising demand for contactless payment solutions in public transport, and widespread adoption of smart mobility infrastructure across metro, bus, and rail networks.

The growing shift toward digital ticketing systems and integrated transport payment platforms is significantly transforming public transportation efficiency. Governments and transit authorities are increasingly investing in automated fare collection technologies such as smart cards, mobile ticketing, and QR based systems to reduce congestion, minimize cash handling, and improve passenger convenience across urban transit ecosystems.

Key Market Trends & Insights

- North America dominated the automatic fare collection system market with the largest revenue share of approximately 37.9% in 2025, supported by strong deployment of advanced transit infrastructure, widespread adoption of contactless payment technologies, and increasing modernization of metro and bus networks. The region benefits from high digital payment penetration, strong government support for public transport digitization, and growing focus on reducing fare leakage and improving operational efficiency in urban mobility systems.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 14.5–15.2% from 2026 to 2033. Growth is driven by rapid urbanization, large scale expansion of metro rail systems, increasing smart city initiatives, and rising government investments in modern public transportation infrastructure in countries such as China, India, and Japan. Strong adoption of QR based ticketing, mobile wallets, and smart card systems is further accelerating regional market growth.

- The Hardware segment held the largest market revenue share of approximately 58.2% in 2025 driven by widespread deployment of smart card readers, ticket vending machines, fare gates, and validation terminals across metro, bus, and rail networks. Hardware components are essential for physical fare validation and passenger access control, making them a core investment area for transit authorities upgrading infrastructure.

- The Software segment is projected to register the fastest growth at a CAGR of 14.6% from 2026 to 2033, driven by increasing adoption of cloud based ticketing platforms, mobile payment integration, and real time fare management systems. Rising demand for data analytics, passenger flow optimization, and interoperable mobility platforms is further accelerating software adoption across smart transit ecosystems.

- The Train segment held the largest market revenue share of approximately 41.5% in 2025 driven by extensive deployment of AFC systems in metro rail networks, suburban rail corridors, and high speed rail infrastructure. Increasing investments in urban rail modernization and rising passenger volumes are further strengthening segment dominance.

- The Bus segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033, driven by rapid adoption of contactless ticketing systems, mobile QR based payments, and smart card integration in urban bus fleets. Government initiatives for digitizing public transportation and reducing cash handling are further supporting segment expansion.

- The Smart Card segment held the largest market revenue share of approximately 46.8% in 2025 driven by widespread adoption in metro systems and integrated transit networks due to high security, durability, and interoperability across multiple transport modes.

- The NFC segment is projected to register the fastest growth at a CAGR of 16.2% from 2026 to 2033, driven by rising smartphone penetration and increasing use of mobile wallets for contactless fare payments. Growing adoption of tap and go systems in urban transit and integration with digital payment ecosystems is further accelerating NFC based AFC deployment across global cities.

Market Size & Forecast

- Global Market Value (2025): USD 70.24 Billion

- Expected Market Value (2033): USD 198.69 Billion

- Forecast CAGR (2026–2033): 13.88%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automatic Fare Collection System Market Segmentation

|

Attributes |

Automatic Fare Collection System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Thales Group (France) |

|

Market Opportunities |

• Expansion Of Contactless Payment Infrastructure In Public Transportation Networks |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automatic Fare Collection System Market Trends

Trend: Growth In Contactless Mobility And Smart Transit Payment Systems

Increasing demand for seamless, cashless, and interoperable public transportation payment solutions is driving rapid adoption of automatic fare collection systems across metro, bus, rail, and multimodal transport networks. Conventional ticketing methods involving cash transactions and manual validation are increasingly being replaced by smart cards, QR based tickets, and mobile wallet integrations, improving operational efficiency and passenger convenience.

In modern transit ecosystems, authorities are integrating AFC technologies such as contactless smart cards, NFC enabled mobile payments, and account based ticketing systems to enhance commuter experience and reduce boarding time. For instance in metro rail systems, contactless fare gates significantly reduce passenger congestion during peak hours while improving revenue collection accuracy. In urban bus networks, mobile QR ticketing systems are being deployed to eliminate paper tickets and streamline fare validation processes.

The rapid expansion of smart city infrastructure and digital mobility platforms is also increasing demand for integrated payment ecosystems that connect multiple transport modes under a single fare system. In addition, high speed rail and airport transit systems continue to rely on advanced AFC solutions for secure, scalable, and real time fare management. Industry deployments in 2025 across major cities in Asia-Pacific reported reduction in average boarding time by nearly 20–35% after implementation of integrated smart card based AFC systems.

Automatic Fare Collection System Market Dynamics

Key Market Driver: Rising Urbanization And Adoption Of Digital Transit Infrastructure

Rapid urbanization and increasing commuter volumes in metropolitan cities are driving strong demand for efficient and automated fare collection systems. Governments and transport authorities are investing heavily in digital transit infrastructure to reduce congestion, improve revenue management, and enhance passenger experience across public transportation networks.

AFC systems are widely deployed in metro rail networks, bus rapid transit systems, and suburban rail services to enable seamless fare collection and reduce dependence on manual ticketing. For instance in major urban transit projects, smart card based systems are integrated with centralized databases to enable real time fare deduction and travel tracking.

Similarly, smart mobility initiatives and public transport modernization programs are accelerating adoption of interoperable payment platforms. Large scale deployments in 2024 across Europe reported improvement of nearly 15–25% in operational efficiency and fare collection accuracy after transitioning to automated ticketing systems.

Key Restraint/Challenge: High Implementation Costs And Integration Complexity

Despite strong growth potential, the market faces challenges due to high initial deployment costs, infrastructure upgrades, and system integration complexities. Implementation of AFC systems requires installation of electronic gates, backend servers, payment gateways, and secure communication networks, which significantly increases capital expenditure for transit authorities.

In addition, integration with legacy transportation systems and multiple payment platforms creates operational challenges, particularly in developing regions with fragmented transit infrastructure. Ensuring interoperability across different transport modes and vendors also adds complexity to system deployment and maintenance.

Pilot projects in emerging economies have shown that AFC implementation costs can account for a significant portion of overall transit modernization budgets, especially in large metro rail expansions, creating financial constraints for widespread adoption.

Key Market Opportunity: Expansion Of Smart Cities And Mobility As A Service Platforms

The expansion of smart cities and Mobility as a Service platforms is creating significant opportunities for automatic fare collection systems. Increasing focus on integrated urban mobility is driving demand for unified payment systems that combine metro, bus, ride sharing, and micro mobility services under a single digital platform.

Transit authorities are increasingly adopting account based ticketing systems and cloud based fare management solutions to enable flexible pricing models and seamless passenger experience. For instance in smart city projects, AFC systems are being integrated with mobile applications that allow users to plan, book, and pay for multi modal journeys in real time.

In addition, advancements in artificial intelligence and data analytics are enhancing fare optimization, passenger flow management, and fraud detection capabilities. Smart transit deployments in 2025 across China and Singapore reported up to 30% improvement in fare collection efficiency and significant reduction in revenue leakage after implementing integrated AFC and digital mobility platforms.

Automatic Fare Collection System Market Scope

The market is segmented on the basis of component, application, and technology platform.

• By Component

On the basis of component, the automatic fare collection system market is segmented into Hardware and Software. The Hardware segment held the largest market revenue share of approximately 58.2% in 2025 driven by widespread deployment of smart card readers, ticket vending machines, fare gates, and validation terminals across metro, bus, and rail networks. Hardware components are essential for physical fare validation and passenger access control, making them a core investment area for transit authorities upgrading infrastructure.

The Software segment is projected to register the fastest growth at a CAGR of 14.6% from 2026 to 2033, driven by increasing adoption of cloud based ticketing platforms, mobile payment integration, and real time fare management systems. Rising demand for data analytics, passenger flow optimization, and interoperable mobility platforms is further accelerating software adoption across smart transit ecosystems.

• By Application

On the basis of application, the market is segmented into Bus, Toll, Car Rental, and Train. The Train segment held the largest market revenue share of approximately 41.5% in 2025 driven by extensive deployment of AFC systems in metro rail networks, suburban rail corridors, and high speed rail infrastructure. Increasing investments in urban rail modernization and rising passenger volumes are further strengthening segment dominance.

The Bus segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033, driven by rapid adoption of contactless ticketing systems, mobile QR based payments, and smart card integration in urban bus fleets. Government initiatives for digitizing public transportation and reducing cash handling are further supporting segment expansion.

• By Technology Platform

On the basis of technology platform, the market is segmented into Smart Card, NFC, Optical Character Recognition, Magnetic Strip, and Barcodes. The Smart Card segment held the largest market revenue share of approximately 46.8% in 2025 driven by widespread adoption in metro systems and integrated transit networks due to high security, durability, and interoperability across multiple transport modes.

The NFC segment is projected to register the fastest growth at a CAGR of 16.2% from 2026 to 2033, driven by rising smartphone penetration and increasing use of mobile wallets for contactless fare payments. Growing adoption of tap and go systems in urban transit and integration with digital payment ecosystems is further accelerating NFC based AFC deployment across global cities.

Automatic Fare Collection System Market Regional Analysis

North America Automatic Fare Collection System Market Insight

North America dominated the automatic fare collection system market with the largest revenue share of approximately 37.9% in 2025, supported by rapid adoption of smart mobility infrastructure, increasing investment in public transportation modernization, and strong demand for contactless payment solutions. The region benefits from advanced transit networks, high smartphone penetration, and growing integration of digital payment platforms across metro, bus, and rail systems. This widespread adoption is further supported by government initiatives for smart city development, rising commuter volumes, and the strong preference for cashless and seamless travel experiences across urban transit ecosystems.

U.S. Automatic Fare Collection System Market Insight

The U.S. automatic fare collection system market captured the largest revenue share within North America in 2025, driven by large scale deployment of contactless ticketing systems across metro rail, bus rapid transit, and airport transit networks. Transit authorities are increasingly focusing on reducing operational costs, minimizing fare leakage, and improving passenger convenience through smart card and mobile based ticketing systems. Moreover, the growing integration of mobile wallets, account based ticketing, and real time fare analytics platforms is significantly contributing to the expansion of the AFC market in the country.

Europe Automatic Fare Collection System Market Insight

The Europe automatic fare collection system market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent regulatory support for digital transportation systems and strong emphasis on sustainable urban mobility. Increasing urbanization and rising demand for integrated multimodal transport networks are encouraging adoption of advanced AFC solutions. European transit operators are also focusing on interoperability across national transport systems, enhancing convenience for cross border commuters and supporting unified ticketing infrastructure across metro, bus, and rail services.

U.K. Automatic Fare Collection System Market Insight

The U.K. automatic fare collection system market is expected to witness strong growth from 2026 to 2033, driven by expanding smart transport initiatives and increasing adoption of contactless payment systems in public transit. Rising concerns over operational efficiency and passenger convenience are encouraging transport authorities to modernize fare collection infrastructure. The strong presence of digital banking systems and widespread use of contactless cards are further accelerating the transition toward fully automated fare collection ecosystems.

Germany Automatic Fare Collection System Market Insight

The Germany automatic fare collection system market is expected to witness steady growth from 2026 to 2033, fueled by increasing investments in smart mobility infrastructure and strong focus on sustainable public transportation systems. Germany’s well developed transit networks and emphasis on digital innovation are promoting adoption of advanced ticketing solutions. Integration of AFC systems with regional transport associations and digital mobility platforms is further enhancing operational efficiency and improving passenger experience across urban and suburban transit systems.

Asia-Pacific Automatic Fare Collection System Market Insight

The Asia-Pacific automatic fare collection system market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, expanding metro rail networks, and increasing government investments in smart city projects. Countries such as China, India, and Japan are heavily investing in modernizing public transportation systems through digital ticketing and contactless payment solutions. The region also benefits from large commuter populations, rising smartphone adoption, and growing demand for efficient and scalable transit payment systems.

Japan Automatic Fare Collection System Market Insight

The Japan automatic fare collection system market is expected to witness strong growth from 2026 to 2033 due to the country’s highly advanced transportation infrastructure and strong focus on efficiency and precision in public transit systems. Japan’s extensive metro and railway networks widely utilize smart card based fare systems, supported by high commuter volumes and strong technological integration. Increasing adoption of mobile ticketing and interoperability between transport modes is further enhancing convenience and efficiency in urban mobility systems.

China Automatic Fare Collection System Market Insight

The China automatic fare collection system market accounted for the largest market revenue share in Asia-Pacific of approximately 42.6% in 2025, attributed to rapid urbanization, large scale expansion of metro rail systems, and strong government focus on smart city development. China is one of the leading adopters of digital payment ecosystems, with widespread use of QR code based transit payments and smart card systems across urban transport networks. Strong domestic manufacturing capabilities and continuous innovation in mobility technology are key factors driving sustained market growth in the country.

Automatic Fare Collection System Market Share

The Automatic Fare Collection System industry is primarily led by well-established companies, including:

• Thales Group (France)

• NIPPON SIGNAL CO., LTD. (Japan)

• OMRON Corporation (Japan)

• Vix Technology (Australia)

• Scheidt & Bachmann GmbH (Germany)

• Indra Sistemas, S.A. (Spain)

• GMV Innovating Solutions S.L. (Spain)

• Siemens (Germany)

• Advanced Card Systems Ltd. (Hong Kong)

• NXP Semiconductors (Netherlands)

• Atos SE (France)

• Cubic Corporation (U.S.)

• LG CNS (South Korea)

• Sony Corporation (Japan)

• Singapore Technologies Engineering Ltd (Singapore)

• Masabi Ltd (U.K.)

• LECIP Holdings Corporation (Japan)

• Trapeze Group (Canada)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.