Global Automotive Active Health Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

4.73 Billion

USD

43.23 Billion

2025

2033

USD

4.73 Billion

USD

43.23 Billion

2025

2033

| 2026 –2033 | |

| USD 4.73 Billion | |

| USD 43.23 Billion | |

| % | |

|

Automotive Active Health Monitoring Market Size

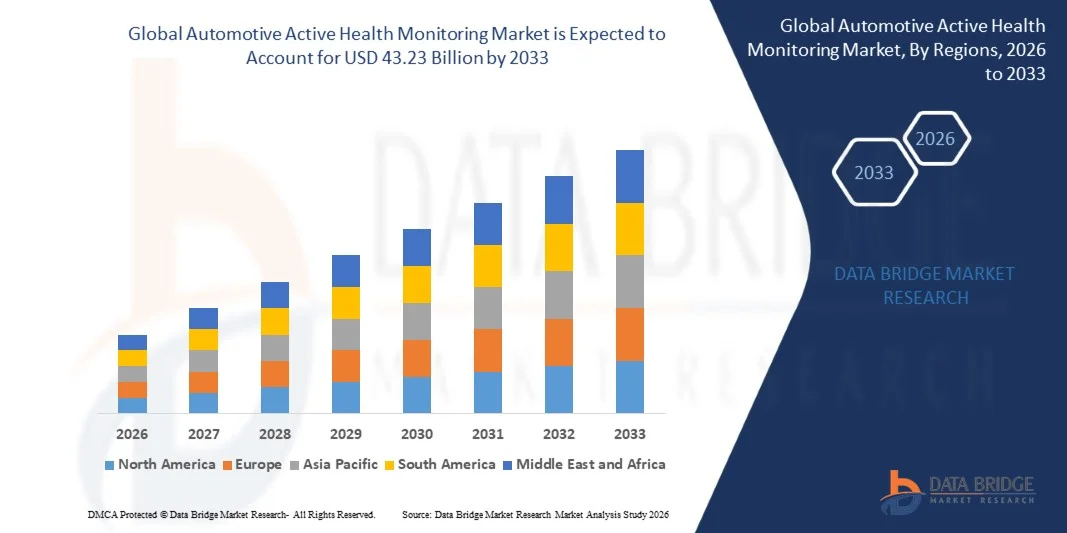

- The global automotive active health monitoring market size was valued at USD 4.73 billion in 2025 and is expected to reach USD 43.23 billion by 2033, at a CAGR of 31.85% during the forecast period

- The market growth is largely fueled by the increasing adoption of connected and smart vehicles, along with technological advancements in in-vehicle health monitoring systems, which enable real-time tracking of driver and passenger vital signs

- Furthermore, rising awareness of driver safety, fatigue management, and overall vehicle wellness is driving demand for integrated health monitoring solutions. These converging factors are accelerating the deployment of sensors, AI-driven monitoring platforms, and infotainment integration, thereby significantly boosting market growth

Automotive Active Health Monitoring Market Analysis

- Automotive active health monitoring systems, providing real-time assessment of driver and passenger vital signs such as heart rate, blood pressure, and fatigue levels, are becoming essential features in modern passenger and commercial vehicles due to their potential to enhance safety, comfort, and driving performance

- The escalating demand for these systems is primarily fueled by increasing vehicle connectivity, growing regulatory focus on road safety, rising adoption of advanced driver-assistance systems (ADAS), and consumer preference for technology-enabled wellness and monitoring features within vehicles

- North America dominated the automotive active health monitoring market with a share of around 40% in 2025, due to rising adoption of connected vehicles, advanced driver assistance systems, and growing awareness of in-vehicle health monitoring solutions

- Asia-Pacific is expected to be the fastest growing region in the automotive active health monitoring market during the forecast period due to rising urbanization, increasing vehicle sales, and growing awareness of driver health in countries such as China, Japan, and India

- Sensors segment dominated the market with a market share of 62.5% in 2025, due to The sensors segment dominated the market with the largest revenue share of 62.5% in 2025, driven by the growing integration of advanced health monitoring sensors in vehicles for real-time tracking of vital signs. These sensors provide accurate measurements of pulse rate, blood pressure, and other health parameters, enhancing driver safety and vehicle health intelligence. Automakers prioritize sensors due to their reliability, compact design, and compatibility with modern vehicle electronics

Report Scope and Automotive Active Health Monitoring Market Segmentation

|

Attributes |

Automotive Active Health Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Active Health Monitoring Market Trends

“Growing Integration of AI and IoT in Vehicle Health Monitoring”

- A significant trend in the automotive active health monitoring market is the increasing integration of artificial intelligence (AI) and the Internet of Things (IoT) into vehicle diagnostic systems, driven by the rising need for real-time data collection and predictive maintenance. This integration is enabling vehicles to continuously monitor engine performance, battery health, and component wear, enhancing safety, reliability, and operational efficiency across personal and commercial fleets

- For instance, Bosch offers AI-powered vehicle health monitoring solutions that use IoT-enabled sensors to track engine parameters, tire pressure, and battery performance, allowing predictive alerts for maintenance and reducing unexpected breakdowns. Such systems are improving fleet uptime and lowering repair costs while providing actionable insights for drivers and fleet managers

- Automakers are increasingly embedding advanced telematics and cloud-based monitoring in connected vehicles to support real-time diagnostics and data-driven decision-making. This trend is positioning automotive active health monitoring systems as critical tools for enhancing vehicle longevity and operational performance

- The adoption of these technologies is also extending to electric vehicles (EVs) where battery management systems and AI-based diagnostics monitor charge cycles, thermal performance, and efficiency losses, helping manufacturers and users optimize EV performance

- Fleet operators and logistics companies are leveraging AI and IoT-enabled health monitoring to reduce downtime, optimize maintenance schedules, and ensure regulatory compliance. This is driving greater adoption of connected diagnostic systems across commercial vehicle segments

- The market is witnessing strong growth as consumers and commercial operators increasingly prioritize predictive maintenance, safety, and operational efficiency. The integration of AI and IoT into vehicle health systems is reinforcing the shift toward smarter, data-driven vehicle management across the global automotive industry

Automotive Active Health Monitoring Market Dynamics

Driver

“Rising Consumer Demand for Real-Time Vehicle Diagnostics”

- The growing need for real-time vehicle diagnostics is driving the adoption of automotive active health monitoring systems, as consumers and fleet operators seek to prevent breakdowns and reduce maintenance costs. Real-time monitoring provides immediate insights into vehicle conditions, allowing proactive servicing and operational efficiency

- For instance, Continental AG supplies connected vehicle diagnostic solutions that provide continuous data on engine performance, tire conditions, and fuel efficiency, helping fleet operators make timely decisions and improve safety standards. These solutions also integrate with mobile apps to inform drivers of potential issues before they escalate

- Rising vehicle complexity, especially in EVs and hybrid vehicles, is increasing reliance on real-time diagnostic tools to track multiple subsystems simultaneously. These systems enhance the ability to detect anomalies early and prevent costly repairs

- Automakers are investing in telematics and cloud-based platforms to capture vehicle health data continuously, which supports predictive analytics and maintenance optimization. This is driving innovation in sensor technologies and AI algorithms used in health monitoring systems

- The increasing consumer preference for connected and smart vehicles continues to support market growth. The demand for seamless, real-time monitoring is positioning automotive active health monitoring systems as essential features in modern vehicles

Restraint/Challenge

“High Implementation and Maintenance Costs”

- The automotive active health monitoring market faces challenges due to the high costs associated with system implementation and ongoing maintenance. Installing sensors, telematics units, and software platforms requires significant investment, which can limit adoption, especially among smaller fleet operators and cost-sensitive consumers

- For instance, ZF Friedrichshafen AG provides advanced vehicle monitoring systems that involve sophisticated sensors, AI software, and cloud integration, leading to higher upfront and operational costs. These expenses can act as barriers to widespread deployment despite the benefits of predictive maintenance

- Maintaining and updating these systems requires specialized technical support, software upgrades, and periodic calibration of sensors to ensure accurate diagnostics. This adds to operational complexity and increases the total cost of ownership for vehicle owners

- Integration with existing vehicle architectures can be complex, particularly for older models, requiring additional retrofitting or adaptation costs. These technical challenges can slow market penetration and adoption rates

- The market also faces constraints related to cost-performance balance, as manufacturers strive to provide high-quality, reliable monitoring solutions while keeping prices competitive. These financial and technical challenges collectively influence market growth and adoption rates

Automotive Active Health Monitoring Market Scope

The market is segmented on the basis of component, application, vehicle type, and sales channel.

• By Component

On the basis of component, the automotive active health monitoring market is segmented into sensors and infotainment systems. The sensors segment dominated the market with the largest revenue share of 62.5% in 2025, driven by the growing integration of advanced health monitoring sensors in vehicles for real-time tracking of vital signs. These sensors provide accurate measurements of pulse rate, blood pressure, and other health parameters, enhancing driver safety and vehicle health intelligence. Automakers prioritize sensors due to their reliability, compact design, and compatibility with modern vehicle electronics. The market also sees strong adoption due to increasing consumer demand for health-focused vehicle features and regulatory push for driver monitoring systems.

The infotainment systems segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising incorporation of health monitoring dashboards and smart interfaces in connected vehicles. For instance, Bosch’s infotainment systems integrate driver health alerts and real-time vitals tracking, providing actionable insights while driving. The increasing trend of multi-functional displays that combine navigation, entertainment, and health monitoring drives adoption in passenger and commercial vehicles. Enhanced user experience and customizable health alerts make infotainment systems a preferred choice among tech-savvy consumers.

• By Application

On the basis of application, the automotive active health monitoring market is segmented into pulse rate, blood sugar level, blood pressure, and others. The pulse rate segment dominated the market in 2025 due to its critical role in alerting drivers to fatigue, stress, or abnormal cardiac activity. Sensors capable of real-time pulse monitoring provide early warnings, reducing the risk of accidents caused by health-related issues. Vehicle manufacturers emphasize pulse monitoring systems for their accuracy, reliability, and ability to integrate with other safety and telematics systems. The growing awareness of driver well-being and rising adoption of connected cars contribute to the strong demand for pulse rate monitoring applications.

The blood sugar level segment is anticipated to witness the fastest growth from 2026 to 2033, driven by increasing prevalence of diabetes and the need for continuous glucose monitoring during driving. For instance, Hyundai has piloted vehicles equipped with non-invasive blood sugar sensors integrated into seatbelts and steering systems, alerting drivers to abnormal glucose levels. Adoption is also encouraged by health-conscious consumers seeking proactive monitoring of chronic conditions while on the road. Blood sugar monitoring in vehicles complements other health applications, expanding the scope of automotive health monitoring systems.

• By Vehicle Type

On the basis of vehicle type, the automotive active health monitoring market is segmented into passenger vehicles and commercial vehicles. The passenger vehicle segment dominated the market in 2025, driven by increasing demand for premium health monitoring features in luxury and connected cars. Vehicle owners prioritize passenger safety and driver wellness, motivating OEMs to integrate advanced health sensors and monitoring systems in personal cars. The growing trend of family-focused and tech-enabled vehicles further supports the adoption of health monitoring technologies. Rising awareness of health and safety benefits, along with regulatory encouragement, reinforces the strong presence of passenger vehicles in the market.

The commercial vehicle segment is expected to witness the fastest growth from 2026 to 2033, fueled by fleet operators adopting health monitoring solutions to improve driver safety and reduce downtime. For instance, Volvo Trucks integrates driver health monitoring systems to track fatigue and stress levels in long-haul drivers, enhancing operational efficiency and safety compliance. Growing concerns over driver wellness, combined with the need to minimize accidents and liability, are driving faster adoption in buses, trucks, and logistics vehicles.

• By Sales Channel

On the basis of sales channel, the automotive active health monitoring market is segmented into OEM and after-market. The OEM segment dominated the market in 2025, driven by the integration of health monitoring systems directly during vehicle manufacturing for better reliability and seamless functionality. OEM-installed systems often provide higher accuracy, longer lifespan, and full compatibility with other vehicle electronic systems, encouraging automakers to offer these as standard or optional features. Consumers prefer OEM solutions for warranty coverage, professional installation, and maintenance support. Government safety initiatives and increasing demand for connected and smart vehicles further strengthen OEM adoption in this market.

The after-market segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising consumer interest in retrofitting existing vehicles with health monitoring solutions. For instance, companies such as Continental provide plug-and-play sensor kits and infotainment integrations for older cars, offering real-time health insights. The flexibility of after-market solutions to upgrade vehicles without full replacement drives strong adoption among health-conscious drivers. Increasing awareness about vehicle safety and personalized health monitoring systems is projected to accelerate growth in this segment.

Automotive Active Health Monitoring Market Regional Analysis

- North America dominated the automotive active health monitoring market with the largest revenue share of around 40% in 2025, driven by rising adoption of connected vehicles, advanced driver assistance systems, and growing awareness of in-vehicle health monitoring solutions

- Consumers in the region highly value real-time monitoring of vital signs, such as pulse rate and blood pressure, integrated seamlessly with vehicle infotainment and telematics systems

- This widespread adoption is further supported by high disposable incomes, technologically inclined consumers, and stringent vehicle safety regulations, positioning automotive health monitoring systems as a preferred solution in both passenger and commercial vehicles

U.S. Automotive Active Health Monitoring Market Insight

The U.S. automotive active health monitoring market captured the largest revenue share in 2025 within North America, fueled by the rapid uptake of connected and smart vehicles. Consumers are increasingly prioritizing driver wellness and safety, encouraging OEMs to integrate health monitoring sensors and infotainment solutions. For instance, Ford and General Motors have introduced pilot programs incorporating pulse rate and fatigue monitoring systems in passenger vehicles. The rising trend of telematics-enabled fleet management and connected car ecosystems further propels market growth, supported by advanced mobile app integration for driver health alerts.

Europe Automotive Active Health Monitoring Market Insight

The Europe market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent vehicle safety regulations and growing awareness of driver health and wellness. Increasing urbanization, the rise of connected vehicles, and demand for advanced driver assistance systems foster adoption of automotive health monitoring. Consumers are drawn to solutions offering convenience, enhanced safety, and integration with infotainment and telematics systems. The market is witnessing significant growth across passenger and commercial vehicles, with both OEMs and after-market providers contributing to adoption.

U.K. Automotive Active Health Monitoring Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising demand for in-vehicle health monitoring to enhance driver safety and reduce fatigue-related accidents. Increasing adoption of connected and smart vehicles, alongside strong regulatory focus on road safety, encourages integration of health monitoring solutions. Consumers and fleet operators are adopting systems capable of monitoring pulse rate, blood pressure, and driver alertness. The U.K.’s robust automotive technology infrastructure and increasing awareness of digital health solutions are expected to continue driving market growth.

Germany Automotive Active Health Monitoring Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, driven by growing awareness of driver safety, stringent vehicle safety standards, and adoption of connected vehicle technologies. Germany’s emphasis on innovation, technology, and sustainability promotes the integration of health monitoring systems in both passenger and commercial vehicles. OEMs are increasingly incorporating sensors and infotainment-based health solutions in new vehicles, with a preference for highly reliable and accurate systems. The integration with advanced driver assistance and telematics systems further enhances market adoption.

Asia-Pacific Automotive Active Health Monitoring Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR during 2026–2033, driven by rising urbanization, increasing vehicle sales, and growing awareness of driver health in countries such as China, Japan, and India. The region’s adoption of connected vehicles and telematics systems is accelerating demand for in-vehicle health monitoring solutions. Government initiatives promoting road safety and smart vehicle technologies are supporting widespread adoption. Growing production of automotive sensors and affordable integration solutions in APAC is expanding accessibility to health monitoring systems.

Japan Automotive Active Health Monitoring Market Insight

The Japan market is gaining momentum due to the country’s high-tech automotive ecosystem, aging driver population, and emphasis on safety and convenience. Adoption is fueled by the integration of health monitoring sensors with infotainment systems, driver alertness monitoring, and connected car features. The market is witnessing increased deployment in passenger vehicles, with OEMs offering advanced monitoring solutions as part of smart vehicle packages. The need for easy-to-use, reliable, and precise health monitoring for both personal and commercial drivers is expected to drive continued growth.

China Automotive Active Health Monitoring Market Insight

The China market accounted for the largest revenue share in APAC in 2025, supported by rapid vehicle electrification, high technological adoption, and growing middle-class consumer base. Connected and smart vehicles equipped with driver health monitoring systems are becoming standard in both passenger and commercial fleets. Government initiatives for road safety and smart vehicle adoption, coupled with strong domestic manufacturers, are key factors propelling market growth. Increasing awareness of driver wellness and fatigue management in long-haul and daily commuting vehicles further boosts adoption.

Automotive Active Health Monitoring Market Share

The automotive active health monitoring industry is primarily led by well-established companies, including:

- Faurecia (France)

- TATA Elxsi (India)

- Plessey Semiconductors (U.K.)

- Acellent Technologies, Inc (U.S.)

- Hoana Medical, Inc (U.S.)

- LORD (U.S.)

- Micro Strain Sensing Systems (U.S.)

- FLEX Ltd (India)

- Continental AG (Germany)

- Denso Corporation (Japan)

- Robert Bosch GmbH (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Harman International (U.S.)

Latest Developments in Global Automotive Active Health Monitoring Market

- In October 2025, Continental entered into a strategic partnership with a leading automotive OEM to co-develop an AI-enabled predictive health monitoring system. This collaboration is designed to enhance real-time vehicle and driver wellness insights, leveraging artificial intelligence to predict potential health or fatigue-related issues before they escalate. By combining AI analytics with advanced sensor data, the system enables proactive safety measures, improves overall driving performance, and strengthens Continental’s position in the market as a provider of next-generation automotive health monitoring solutions. This initiative reflects the growing emphasis on predictive and preventive technologies in connected and smart vehicles

- In July 2025, Denso expanded its capabilities by opening a new innovation center dedicated to automotive health monitoring technologies. The center focuses on accelerating research and development for next-generation sensors, infotainment integration, and driver wellness solutions. This strategic investment allows Denso to shorten development cycles, enhance product reliability, and address increasing demand from OEMs for comprehensive in-vehicle health monitoring systems. By focusing on innovation and rapid prototyping, Denso positions itself as a key player in enabling safer, more intelligent vehicles that monitor driver and passenger well-being in real time

- In 2024, Bosch unveiled an AI-powered driver assistance system with integrated health monitoring features, capable of detecting driver fatigue, stress, and alertness levels through infrared cameras and biometric sensors. By integrating health monitoring with advanced driver assistance systems (ADAS), Bosch enhances both vehicle safety and occupant comfort. The system provides real-time alerts to prevent accidents, promotes safer driving behaviors, and demonstrates how health monitoring is becoming an essential component of modern vehicle safety ecosystems, accelerating adoption in both passenger and commercial vehicles

- In June 2023, Magna International acquired Veoneer Active Safety for US$1.525 billion to expand its portfolio in advanced driver-assistance and active-safety technologies. By integrating Veoneer’s sensors, perception software, and system-integration capabilities, Magna strengthens its offerings in driver and occupant monitoring solutions. This acquisition enables Magna to provide OEMs with more comprehensive health monitoring and safety solutions, enhancing competitive advantage and responding to the rising demand for in-vehicle health monitoring systems in connected and autonomous vehicles

- In June 2022, Hyundai Mobis announced the Smart Cabin integrated vital signs controller, capable of monitoring a driver’s heart rate, posture, brainwaves, and overall stress levels. The system also evaluates CO2 levels in the cabin and can switch to autonomous driving if driver stress is detected. This development highlights Hyundai Mobis’s focus on integrating medical-grade sensing technology into vehicles to enhance safety and comfort. By offering real-time assessment of driver and passenger health, the Smart Cabin exemplifies the shift toward vehicles that actively support driver well-being and proactive accident prevention

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.