Global Automotive Fuel Cell Market

Market Size in USD Billion

CAGR :

%

USD

6.71 Billion

USD

209.20 Billion

2025

2033

USD

6.71 Billion

USD

209.20 Billion

2025

2033

| 2026 –2033 | |

| USD 6.71 Billion | |

| USD 209.20 Billion | |

| % | |

|

Automotive Fuel Cell Market Size

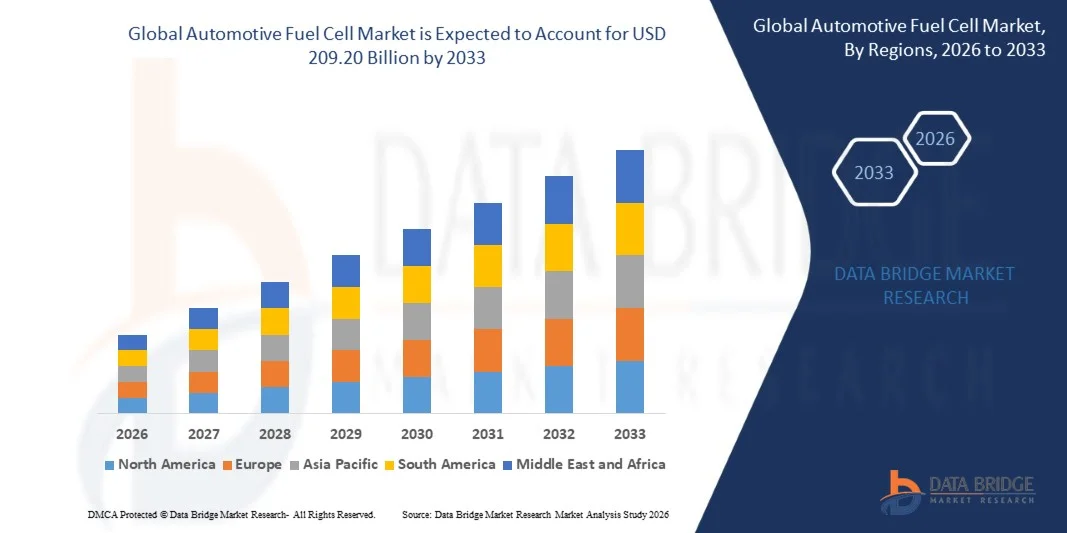

- The global automotive fuel cell market size was valued at USD 6.71 billion in 2025and is expected to reach USD 209.20 billion by 2033, at a CAGR of 53.72% during the forecast period

- The market growth is largely fuelled by the increasing adoption of zero-emission vehicles, rising government initiatives supporting hydrogen infrastructure development, and growing investments in sustainable transportation technologies

- Increasing demand for long-range and fast-refuelling electric vehicles, particularly in commercial transportation and heavy-duty mobility applications, is further accelerating the adoption of automotive fuel cell technologies globally

Automotive Fuel Cell Market Analysis

- The automotive fuel cell market is witnessing rapid growth due to the global transition toward low-carbon transportation solutions and the increasing emphasis on reducing greenhouse gas emissions across the automotive sector

- Manufacturers are increasingly investing in fuel cell vehicle development, hydrogen refuelling infrastructure, and advanced energy management systems to improve vehicle efficiency, durability, and commercial scalability

- North America dominated the automotive fuel cell market with the largest revenue share in 2025, driven by increasing government investments in hydrogen infrastructure and rising demand for zero-emission transportation solutions across passenger and commercial vehicle segments

- Asia-Pacific region is expected to witness the highest growth rate in the global automotive fuel cell market, driven by rapid industrialization, strong government support for hydrogen mobility, expanding fuel cell vehicle manufacturing, and increasing investments in clean transportation infrastructure

- The PEMFC segment held the largest market revenue share in 2025 driven by its high energy efficiency, compact structure, and suitability for automotive applications requiring rapid start-up and low operating temperatures. PEMFC technology is widely adopted in passenger and commercial fuel cell vehicles due to its enhanced performance, lightweight design, and compatibility with hydrogen-powered transportation systems

Report Scope and Automotive Fuel Cell Market Segmentation

|

Attributes |

Automotive Fuel Cell Key Market Insights |

|

Segments Covered |

· By Electrolyte Type: PEMFC and PAFC · By Component Type: Fuel Stack, Fuel Processor and Power Conditioner · By Power Capacity: <100 Kw Power Output, 100–200 Kw Power Output, and >200 Kw Power Output · By Vehicle Type: PC, LCV, Bus, and Truck · By Operating Miles: 0-250 Miles, 251-500 Miles and Above 500 Miles |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Toshiba India Pvt. Ltd. (India) |

|

Market Opportunities |

• Expansion Of Hydrogen Refuelling Infrastructure Networks |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Fuel Cell Market Trends

“Increasing Adoption of Hydrogen-Powered Zero-Emission Vehicles”

- The growing focus on reducing carbon emissions and achieving sustainable transportation goals is significantly shaping the automotive fuel cell market, as governments and consumers increasingly prefer zero-emission mobility solutions. Automotive fuel cells are gaining traction due to their ability to provide longer driving range, fast refuelling capabilities, and improved energy efficiency compared to conventional battery-powered systems. This trend is strengthening their adoption across passenger vehicles, buses, trucks, and commercial fleets, encouraging manufacturers to invest in advanced hydrogen mobility solutions

- Increasing awareness regarding environmental sustainability, clean energy transition, and fuel efficiency has accelerated the demand for automotive fuel cell vehicles across developed and emerging economies. Governments and environmentally conscious consumers are actively supporting hydrogen-powered transportation, prompting automotive manufacturers and energy companies to prioritize hydrogen infrastructure development and fuel cell innovation. This has also led to collaborations between vehicle manufacturers, hydrogen suppliers, and technology providers to enhance fuel cell performance and commercial scalability

- Sustainability and decarbonization trends are influencing purchasing and investment decisions, with manufacturers emphasizing low-emission technologies, renewable hydrogen integration, and advanced fuel cell systems. These factors are helping companies differentiate products in a competitive automotive market while also driving investments in hydrogen production and refuelling networks. Companies are increasingly using strategic partnerships and marketing initiatives to highlight the environmental and operational benefits of fuel cell vehicles to strengthen market positioning and consumer adoption

- For instance, in 2024, Toyota Motor Corporation in Japan and Hyundai Motor Company in South Korea expanded their hydrogen fuel cell vehicle portfolios and increased investments in hydrogen refuelling infrastructure. These developments were introduced in response to rising demand for sustainable transportation and government support for clean mobility initiatives, with deployment across commercial fleets and passenger vehicle segments. The companies also emphasized carbon neutrality and energy efficiency benefits to improve consumer confidence and strengthen long-term market competitiveness

- While demand for automotive fuel cells is growing, sustained market expansion depends on continuous technological advancements, cost-efficient hydrogen production, and the development of widespread refuelling infrastructure. Manufacturers are also focusing on improving fuel cell durability, supply chain efficiency, and scalable production capabilities to support broader adoption across the global automotive sector

Automotive Fuel Cell Market Dynamics

Driver

“Growing Government Support for Zero-Emission Transportation”

- Rising government initiatives promoting low-carbon transportation and clean energy adoption are major drivers for the automotive fuel cell market. Governments across various countries are increasingly supporting hydrogen fuel cell vehicle deployment through subsidies, incentives, emission regulations, and infrastructure investments. This trend is also encouraging research into advanced fuel cell technologies and renewable hydrogen production, supporting long-term market growth and technological innovation

- Expanding applications in passenger vehicles, commercial trucks, buses, and industrial transportation are influencing market growth. Automotive fuel cells help improve driving range, reduce refuelling time, and lower greenhouse gas emissions while supporting efficient and sustainable mobility solutions. The increasing demand for heavy-duty and long-distance transportation alternatives globally further reinforces this trend

- Automotive manufacturers and energy companies are actively promoting fuel cell vehicle adoption through strategic partnerships, pilot projects, and infrastructure expansion initiatives. These efforts are supported by the growing consumer preference for environmentally sustainable transportation solutions, while also encouraging collaborations between hydrogen producers, mobility providers, and automotive OEMs to improve operational efficiency and reduce carbon footprints

- For instance, in 2023, Honda Motor Co., Ltd. in Japan and BMW Group in Germany reported increased investments in hydrogen fuel cell vehicle development and pilot deployment programs. This expansion followed growing demand for clean transportation solutions and stronger government support for hydrogen mobility infrastructure, driving technological advancements and product differentiation. Both companies also emphasized sustainability and energy transition strategies to strengthen consumer trust and market competitiveness

- Although increasing clean energy initiatives support market growth, wider adoption depends on hydrogen infrastructure availability, fuel cost optimization, and scalable fuel cell manufacturing processes. Investment in hydrogen distribution networks, renewable energy integration, and advanced fuel cell technologies will be critical for meeting future transportation demand and maintaining competitive advantage

Restraint/Challenge

“High Infrastructure Costs And Limited Hydrogen Refuelling Networks”

- The relatively high cost of hydrogen fuel cell systems and limited refuelling infrastructure remain key challenges, restricting adoption among consumers and fleet operators. High production costs for fuel cells, hydrogen storage systems, and associated infrastructure contribute to elevated vehicle pricing and operational expenses. In addition, limited availability of hydrogen refuelling stations can further affect consumer confidence and market penetration

- Consumer awareness and infrastructure accessibility remain uneven, particularly in developing markets where hydrogen mobility ecosystems are still emerging. Limited understanding of fuel cell technology benefits and concerns regarding hydrogen availability restrict adoption across certain transportation segments. This also leads to slower commercialization in regions with insufficient government support and limited hydrogen distribution capabilities

- Supply chain and infrastructure challenges also impact market growth, as hydrogen fuel cell systems require specialized materials, advanced manufacturing processes, and large-scale hydrogen production facilities. Logistical complexities, infrastructure investment requirements, and hydrogen transportation costs increase operational challenges. Companies must invest in efficient hydrogen storage, distribution systems, and collaborative infrastructure development to improve market accessibility and reliability

- For instance, in 2024, fleet operators and automotive distributors in India and Southeast Asia reported slower adoption of fuel cell vehicles due to limited hydrogen refuelling stations and high vehicle acquisition costs compared to battery electric alternatives. Infrastructure investment requirements and supply chain limitations were additional barriers affecting commercialization efforts. These factors also prompted some transportation providers to prioritize battery electric vehicle deployment over hydrogen fuel cell technologies in cost-sensitive markets

- Overcoming these challenges will require cost-efficient fuel cell production, expanded hydrogen refuelling networks, and stronger public-private partnerships for infrastructure development. Collaboration among automotive manufacturers, energy companies, and government agencies can help unlock the long-term growth potential of the global automotive fuel cell market. Furthermore, improving hydrogen accessibility, reducing production costs, and strengthening consumer awareness regarding fuel cell benefits will be essential for widespread adoption

Automotive Fuel Cell Market Scope

The market is segmented on the basis of electrolyte type, component type, power capacity, vehicle type, and operating miles.

- By Electrolyte Type

On the basis of electrolyte type, the automotive fuel cell market is segmented into PEMFC and PAFC. The PEMFC segment held the largest market revenue share in 2025 driven by its high energy efficiency, compact structure, and suitability for automotive applications requiring rapid start-up and low operating temperatures. PEMFC technology is widely adopted in passenger and commercial fuel cell vehicles due to its enhanced performance, lightweight design, and compatibility with hydrogen-powered transportation systems.

The PAFC segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing advancements in fuel cell durability and growing demand for reliable energy systems in heavy-duty transportation applications. PAFC-based systems are gaining attention for their operational stability and ability to support long-duration energy generation in commercial mobility solutions.

- By Component Type

On the basis of component type, the automotive fuel cell market is segmented into Fuel Stack, Fuel Processor and Power Conditioner. The Fuel Stack segment held the largest market revenue share in 2025 driven by its critical role in converting hydrogen into electricity for vehicle propulsion. Fuel stacks are considered the core component of automotive fuel cell systems and are witnessing increasing investments aimed at improving efficiency, durability, and power density across fuel cell vehicles.

The Power Conditioner segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for advanced power management solutions that improve energy conversion efficiency and optimize vehicle performance. Increasing integration of intelligent energy control systems in fuel cell vehicles is further supporting segment expansion globally.

- By Power Capacity

On the basis of power capacity, the automotive fuel cell market is segmented into <100 Kw Power Output, 100–200 Kw Power Output, and >200 Kw Power Output. The 100–200 Kw Power Output segment held the largest market revenue share in 2025 driven by its extensive use in passenger vehicles, buses, and medium-duty commercial transportation applications. This power range provides an effective balance between vehicle performance, driving range, and operational efficiency, supporting its widespread adoption among automotive manufacturers.

The >200 Kw Power Output segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of fuel cell technology in heavy-duty trucks, long-haul transportation, and industrial mobility applications. Higher power output systems are gaining popularity for their ability to support extended driving ranges and high-load commercial operations.

- By Vehicle Type

On the basis of vehicle type, the automotive fuel cell market is segmented into PC, LCV, Bus, and Truck. The PC segment held the largest market revenue share in 2025 driven by rising consumer demand for zero-emission passenger vehicles, supportive government incentives, and increasing investments by automotive manufacturers in hydrogen-powered mobility solutions. Fuel cell passenger cars are increasingly preferred for their fast refuelling capabilities and long-distance driving performance.

The Truck segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing demand for sustainable heavy-duty transportation solutions and the growing need to reduce carbon emissions in logistics and freight operations. Fuel cell trucks are gaining strong traction due to their extended operational range, lower refuelling time, and suitability for long-distance commercial transportation.

- By Operating Miles

On the basis of operating miles, the automotive fuel cell market is segmented into 0-250 Miles, 251-500 Miles and Above 500 Miles. The 251-500 Miles segment held the largest market revenue share in 2025 driven by the growing preference for fuel cell vehicles capable of delivering balanced range performance for daily commuting and commercial transportation activities. Vehicles operating within this range offer efficient energy consumption and improved practicality for both residential and fleet applications.

The Above 500 Miles segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for long-range fuel cell vehicles in commercial logistics, intercity transportation, and heavy-duty mobility applications. Advancements in hydrogen storage systems and fuel cell efficiency are further supporting the adoption of vehicles capable of extended driving distances.

Automotive Fuel Cell Market Regional Analysis

- North America dominated the automotive fuel cell market with the largest revenue share in 2025, driven by increasing government investments in hydrogen infrastructure and rising demand for zero-emission transportation solutions across passenger and commercial vehicle segments

- Consumers and fleet operators in the region highly value the long driving range, fast refuelling capabilities, and reduced carbon emissions offered by hydrogen fuel cell vehicles compared to conventional internal combustion engine vehicles

- This widespread adoption is further supported by strong clean energy policies, advanced hydrogen research initiatives, and growing partnerships between automotive manufacturers and energy companies, establishing fuel cell vehicles as a promising solution for sustainable mobility across commercial and residential transportation sectors

U.S. Automotive Fuel Cell Market Insight

The U.S. automotive fuel cell market captured the largest revenue share in 2025 within North America, fueled by the rapid expansion of hydrogen infrastructure projects and increasing investments in clean transportation technologies. Consumers and commercial fleet operators are increasingly prioritizing zero-emission mobility solutions supported by government incentives and emission reduction targets. The growing demand for hydrogen-powered trucks, buses, and passenger vehicles, combined with increasing collaboration among automotive OEMs, hydrogen suppliers, and technology providers, further propels the automotive fuel cell market. Moreover, the integration of hydrogen energy solutions into public transportation and logistics networks is significantly contributing to market expansion.

Europe Automotive Fuel Cell Market Insight

The Europe automotive fuel cell market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent emission regulations and increasing investments in sustainable transportation infrastructure. The rising focus on decarbonization, renewable energy integration, and hydrogen mobility initiatives is fostering the adoption of fuel cell vehicles across the region. European consumers and industries are also attracted to the long-range and fast-refuelling capabilities offered by fuel cell vehicles. The region is experiencing significant growth across passenger vehicles, commercial transportation, and public transit applications, with hydrogen-powered mobility solutions increasingly incorporated into both urban and long-distance transportation systems.

U.K. Automotive Fuel Cell Market Insight

The U.K. automotive fuel cell market is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing transition toward low-carbon transportation and growing government support for hydrogen-powered mobility solutions. In addition, rising investments in hydrogen refuelling infrastructure and sustainable logistics networks are encouraging fleet operators and automotive manufacturers to adopt fuel cell technologies. The U.K.’s focus on clean energy transition, alongside expanding research and innovation activities in hydrogen mobility, is expected to continue stimulating market growth.

Germany Automotive Fuel Cell Market Insight

The Germany automotive fuel cell market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for advanced zero-emission transportation technologies and the country’s strong emphasis on sustainability and automotive innovation. Germany’s well-developed industrial infrastructure, combined with its leadership in automotive engineering and hydrogen research, promotes the adoption of fuel cell vehicles, particularly in commercial and heavy-duty transportation sectors. The integration of fuel cell systems into public transportation and logistics fleets is also becoming increasingly prevalent, with a strong preference for energy-efficient and environmentally sustainable mobility solutions aligning with local market expectations.

Asia-Pacific Automotive Fuel Cell Market Insight

The Asia-Pacific automotive fuel cell market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, increasing investments in hydrogen infrastructure, and strong government support for clean transportation technologies in countries such as China, Japan, and South Korea. The region’s growing focus on sustainable mobility and carbon neutrality initiatives is driving the adoption of fuel cell vehicles across passenger and commercial transportation applications. Furthermore, as APAC emerges as a major manufacturing hub for fuel cell components and hydrogen technologies, the affordability and accessibility of fuel cell vehicles are expanding to a wider consumer and industrial base.

Japan Automotive Fuel Cell Market Insight

The Japan automotive fuel cell market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s strong hydrogen economy initiatives, advanced automotive technologies, and increasing focus on carbon-neutral transportation systems. The Japanese market places significant emphasis on clean energy innovation, and the adoption of fuel cell vehicles is driven by rising investments in hydrogen refuelling infrastructure and smart mobility solutions. The integration of fuel cell vehicles into public transportation, logistics, and passenger mobility systems is fueling growth. Moreover, Japan’s long-term commitment to hydrogen-based energy systems is further supporting the expansion of automotive fuel cell technologies across residential and commercial transportation sectors.

China Automotive Fuel Cell Market Insight

The China automotive fuel cell market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapid industrialization, expanding hydrogen infrastructure, and increasing adoption of clean transportation technologies. China stands as one of the largest markets for electric and hydrogen-powered vehicles, and fuel cell vehicles are becoming increasingly popular in buses, trucks, and commercial fleet operations. The push toward carbon neutrality, strong government subsidies, and the presence of domestic automotive and hydrogen technology manufacturers are key factors propelling the automotive fuel cell market in China.

Automotive Fuel Cell Market Share

The Automotive Fuel Cell industry is primarily led by well-established companies, including:

• Toshiba India Pvt. Ltd. (India)

• Ballard Power Systems (Canada)

• Hydrogenics (Canada)

• ITM Power (U.K.)

• PLUG POWER INC. (U.S.)

• Ceres Power Holdings plc (U.K.)

• Nedstack Fuel Cell Technology BV (Netherlands)

• NUVERA FUEL CELLS, LLC (U.S.)

• Toyota Motor Sales, U.S.A., Inc. (U.S.)

• American Honda Motor Co., Inc. (U.S.)

• Hyundai Motor Company (South Korea)

• Daimler AG (Germany)

• Nissan (Japan)

• TW Horizon Fuel Cell Technologies (China)

• Altergy (U.S.)

• Intelligent Energy Limited (U.K.)

• K- Pas Instronic Engineers India Private Limited (India)

• Fuji Electric Co., Ltd (Japan)

Latest Developments in Global Automotive Fuel Cell Market

- In February 2026, automotive manufacturers and hydrogen technology providers accelerated investments in next-generation fuel cell systems with improved efficiency, durability, and reduced platinum catalyst usage. These developments are expected to lower production costs, enhance vehicle performance, and support wider commercialization of hydrogen-powered transportation solutions. The trend is likely to strengthen the long-term scalability and competitiveness of the automotive fuel cell market globally

- In February 2025, Toyota Motor Corporation began commercial production of its next-generation fuel cell system designed for heavy-duty commercial vehicles. The new system achieved significant cost reduction and improved durability through advanced catalyst optimization and manufacturing enhancements. This development is expected to strengthen hydrogen mobility adoption and improve the commercial viability of fuel cell-powered transportation solutions worldwide

- In January 2025, Nikola Corporation successfully completed one million mile durability testing for its fuel cell powertrain systems targeting commercial vehicle applications. This achievement demonstrated improved reliability and operational performance for hydrogen-powered heavy-duty vehicles. The development is likely to increase fleet operator confidence and accelerate adoption of fuel cell trucks in logistics and long-haul transportation sectors

- In August 2024, hydrogen infrastructure developers and automotive OEMs expanded hydrogen refuelling station networks across North America and Europe to support the growing deployment of fuel cell vehicles. These investments improved accessibility to hydrogen fuel and strengthened the supporting ecosystem for zero-emission mobility solutions. The expansion is expected to accelerate commercialization and consumer adoption of fuel cell vehicles across commercial and passenger transportation applications

- In May 2023, Hyundai Motor Company commercialized its XCIENT fuel cell tractor for the North American commercial vehicle market to strengthen hydrogen mobility initiatives and support carbon neutrality goals. The launch of the Class 8 fuel cell electric vehicle improved the company’s presence in the heavy-duty transportation segment and enhanced the adoption of sustainable logistics solutions in the region

- In November 2022, Cummins Inc. signed a memorandum of understanding with Tata Motors to collaborate on the development of low and zero-emission propulsion technologies for commercial vehicles in India. The partnership focused on fuel cells, battery electric vehicle systems, and hydrogen-powered internal combustion technologies to encourage green mobility adoption. This collaboration is expected to strengthen hydrogen technology deployment and expand the customer base for fuel cell solutions in emerging markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.