Global Automotive Homologation Services Market

Market Size in USD Billion

USD

1.95 Billion

USD

2.42 Billion

2025

2033

USD

1.95 Billion

USD

2.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.95 Billion | |

| USD 2.42 Billion | |

| % | |

|

Automotive Homologation Services Market Size

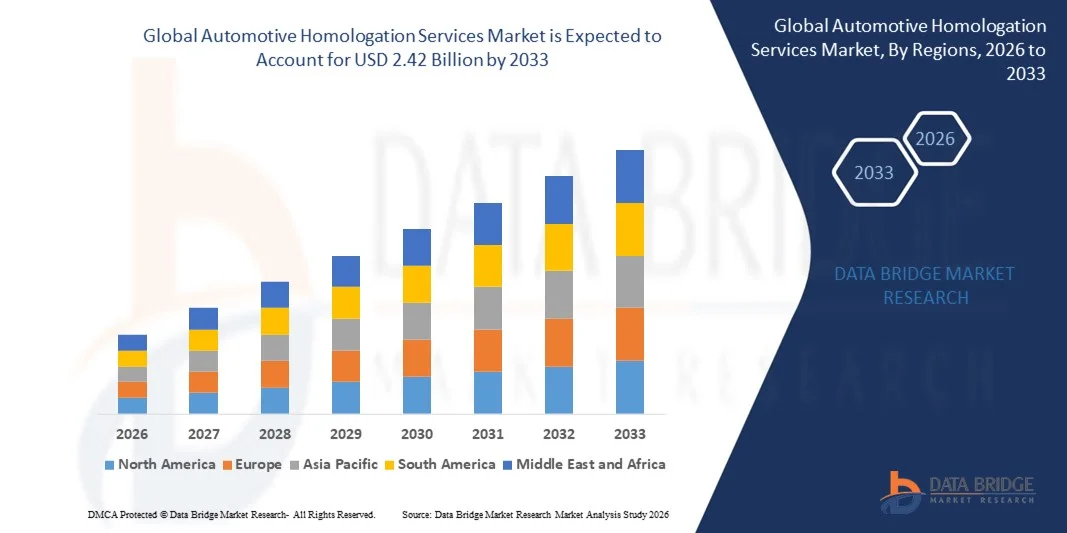

- The global automotive homologation services market size was valued at USD 1.95 billion in 2025 and is expected to reach USD 2.42 billion by 2033, at a CAGR of 2.75% during the forecast period

- The market growth is primarily driven by increasing global vehicle production, stringent regulatory requirements for safety, emissions, and environmental compliance, and the rising complexity of automotive technologies, including electric and autonomous vehicles. These factors are prompting manufacturers to rely on specialized homologation services to ensure regulatory approval and market entry across multiple regions

- Furthermore, the growing expansion of international automotive trade and cross-border vehicle launches is intensifying the demand for standardized testing, certification, and compliance services. Automotive OEMs and component suppliers are increasingly outsourcing homologation activities to reduce operational burden, accelerate time-to-market, and ensure adherence to evolving global standards, significantly boosting market growth

Automotive Homologation Services Market Analysis

- Automotive homologation services, which include testing, inspection, and certification of vehicles and components, are becoming essential for manufacturers to validate compliance with regulatory frameworks and safety standards. The adoption of advanced vehicle technologies such as connected systems, electric powertrains, and autonomous driving functions further increases the need for comprehensive homologation solutions

- Rising investments in electric vehicles (EVs) and hybrid mobility are expanding the scope of homologation services, as these vehicles require specialized testing for battery safety, charging systems, emissions, and software compliance. Manufacturers increasingly depend on homologation providers to navigate regulatory complexities, which accelerates service adoption

- Asia-Pacific dominated the automotive homologation services market with a share of 48.62% in 2025, due to high vehicle production volumes, expanding automotive exports, and evolving emission and safety regulations across major economies

- North America is expected to be the fastest growing region in the automotive homologation services market during the forecast period due to tightening emission regulations, expansion of electric vehicle production, and increasing cross-border vehicle trade

- Outsourced services segment dominated the market with a market share of 62.9% in 2025, due to the increasing complexity of global regulatory frameworks and the need for specialized technical expertise across multiple regions. Automotive manufacturers and component suppliers rely on third-party homologation providers to manage certification, testing, documentation, and regulatory approvals efficiently

Report Scope and Automotive Homologation Services Market Segmentation

|

Attributes |

Automotive Homologation Services Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Homologation Services Market Trends

Increasing Adoption of Electric and Autonomous Vehicles

- A significant trend in the automotive homologation services market is the rising adoption of electric and autonomous vehicles, which is driving the need for comprehensive testing and certification across safety, environmental, and regulatory standards. This shift is compelling OEMs and suppliers to engage with specialized homologation service providers to ensure global compliance and market readiness

- For instance, TÜV SÜD provides extensive homologation and type approval services for electric vehicles, including battery safety, EMC testing, and regulatory certification, supporting manufacturers in global market entry. Such services are critical as vehicle designs evolve with autonomous driving technologies that require new safety and functional validations

- The increasing complexity of vehicle electronics, software, and connectivity systems is expanding the scope of homologation services. Components such as advanced driver-assistance systems (ADAS) and infotainment modules demand rigorous testing under varied environmental and regulatory conditions

- Emerging trends in global mobility policies are encouraging OEMs to prioritize homologation processes early in the development cycle. This proactive approach reduces time-to-market risks and ensures adherence to region-specific emissions, safety, and performance requirements

- Automotive standards for crashworthiness, battery performance, and environmental impact are becoming stricter, reinforcing the relevance of professional homologation services. Compliance ensures brand credibility, consumer safety, and alignment with international automotive norms

- The market is witnessing growth in collaborative testing programs between OEMs and regulatory bodies, which is enhancing the efficiency of homologation workflows. This is positioning service providers as strategic partners in achieving safer, compliant, and market-ready vehicle solutions

Automotive Homologation Services Market Dynamics

Driver

Rising Global Regulatory Compliance Requirements

- The rising complexity and expansion of global regulatory frameworks are driving demand for automotive homologation services, as manufacturers must meet diverse safety, environmental, and performance standards to access multiple markets. Regulatory compliance ensures vehicles meet local and international norms, reducing legal and financial risks

- For instance, SGS offers comprehensive vehicle type approval and regulatory compliance testing for emissions, safety, and radio frequency standards, assisting OEMs in meeting EU, U.S., and Asian market regulations. Their services enable efficient certification across multiple jurisdictions, minimizing market entry delays

- Stricter emission and fuel efficiency standards are compelling OEMs to validate technologies such as hybrid drivetrains and lightweight materials through homologation processes. These validations ensure that vehicles conform to global environmental and safety expectations

- Consumer safety awareness and government enforcement programs are increasing scrutiny on vehicle compliance, making homologation services essential for brand trust and liability mitigation. Manufacturers rely on these services to demonstrate adherence to critical safety standards

- The growing international expansion of automotive players necessitates harmonized certification procedures. This is encouraging OEMs to collaborate with global homologation service providers to streamline approvals, maintain consistency, and reduce operational redundancies

Restraint/Challenge

High Complexity and Cost of Homologation Processes

- The automotive homologation services market faces challenges due to the intricate nature and high cost of testing, certification, and regulatory approvals for modern vehicles, which involve multiple subsystems, components, and software layers. These processes require specialized facilities, skilled personnel, and advanced testing equipment

- For instance, DEKRA operates advanced crash test facilities and conducts detailed EMC, safety, and environmental testing that involve significant capital investment and operational expenditure. The high cost and technical complexity of such services can be a barrier for smaller OEMs and new entrants

- The diverse and constantly evolving regulatory requirements across regions add to procedural complexity. Manufacturers must navigate varying standards, conduct repeated testing, and maintain meticulous documentation, which extends project timelines and increases costs

- Advanced vehicle technologies such as ADAS, electrification, and connectivity demand additional homologation procedures, including functional safety validation and cybersecurity assessments. These added layers of testing amplify cost pressures and resource requirements

- The challenge of balancing thorough compliance with time-to-market constraints continues to pressure OEMs and service providers. High process complexity can limit flexibility, slow product launches, and necessitate careful project management to control expenses

Automotive Homologation Services Market Scope

The market is segmented on the basis of sourcing type and vehicle type.

- By Sourcing Type

On the basis of sourcing type, the automotive homologation services market is segmented into in house services and outsourced services. The outsourced services segment dominated the market with the largest revenue share of 62.9% in 2025, driven by the increasing complexity of global regulatory frameworks and the need for specialized technical expertise across multiple regions. Automotive manufacturers and component suppliers rely on third-party homologation providers to manage certification, testing, documentation, and regulatory approvals efficiently. Outsourcing enables companies to reduce operational burden, accelerate time to market, and ensure compliance with evolving emission, safety, and environmental standards across diverse markets. The availability of established testing infrastructure and regulatory knowledge among service providers further strengthens the dominance of outsourced services.

The in house services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by growing investments by large OEMs in dedicated compliance and regulatory departments. Automakers are increasingly building internal homologation capabilities to maintain greater control over confidential vehicle data, streamline product development cycles, and ensure faster adaptation to changing regulations. The rising development of electric and autonomous vehicles, which require continuous regulatory validation and software updates, is encouraging companies to strengthen internal expertise. In house homologation also supports long-term cost optimization for high-volume manufacturers operating across multiple global markets.

- By Vehicle Type

On the basis of vehicle type, the automotive homologation services market is segmented into motorcycle, passenger vehicles, commercial vehicles, trailers, and agricultural equipment. The passenger vehicles segment dominated the market with the largest revenue share in 2025, driven by high global production volumes and frequent model launches across domestic and international markets. Stringent safety, emission, and fuel efficiency regulations applicable to passenger cars require extensive testing and certification procedures before market entry. The increasing shift toward electric and hybrid passenger vehicles further intensifies homologation requirements, particularly related to battery safety, charging systems, and advanced driver assistance systems. Continuous technological upgrades and evolving regulatory standards sustain strong demand for homologation services in this segment.

The commercial vehicles segment is projected to witness the fastest growth rate from 2026 to 2033, supported by tightening emission norms and safety regulations for heavy-duty trucks and buses. Governments across major markets are introducing stricter compliance mandates for fuel efficiency, load standards, and telematics integration in commercial fleets. The expansion of cross-border trade and logistics operations also necessitates adherence to multiple regional certification requirements. As fleet operators increasingly adopt electric and alternative fuel commercial vehicles, the need for comprehensive homologation and regulatory validation services is expected to accelerate significantly.

Automotive Homologation Services Market Regional Analysis

- Asia-Pacific dominated the automotive homologation services market with the largest revenue share of 48.62% in 2025, driven by high vehicle production volumes, expanding automotive exports, and evolving emission and safety regulations across major economies

- The region’s strong presence of passenger and commercial vehicle manufacturers, increasing investments in electric vehicle development, and tightening regulatory frameworks are accelerating demand for certification and compliance services

- Rising cross-border vehicle trade, frequent new model launches, and harmonization efforts with international automotive standards are contributing to higher adoption of homologation services across emerging automotive hubs

China Automotive Homologation Services Market Insight

China held the largest share in the Asia-Pacific automotive homologation services market in 2025, supported by its position as the world’s largest automobile producer and exporter. Strict emission standards, evolving New Energy Vehicle regulations, and mandatory safety certification requirements are increasing demand for comprehensive testing and approval services. Continuous product innovation and rapid rollout of electric and hybrid vehicles require extensive validation and compliance verification. Expansion of domestic brands into global markets further strengthens homologation service requirements.

India Automotive Homologation Services Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by implementation of Bharat Stage emission norms and growing vehicle safety mandates. Rising vehicle production, increasing exports, and expansion of electric mobility initiatives are driving certification activities. Government focus on automotive manufacturing under industrial development programs is encouraging compliance with global standards. Growing investments in testing infrastructure and regulatory alignment are supporting sustained market expansion.

Europe Automotive Homologation Services Market Insight

The Europe automotive homologation services market is expanding steadily, supported by stringent regulatory frameworks related to emissions, vehicle safety, and environmental sustainability. The region’s strong focus on carbon reduction targets and electrification is increasing demand for advanced validation and approval services. Presence of established automotive OEMs and component manufacturers contributes to consistent certification requirements. Continuous updates to Euro emission standards and type approval regulations sustain market growth.

Germany Automotive Homologation Services Market Insight

Germany’s automotive homologation services market is driven by its advanced automotive engineering ecosystem and leadership in premium vehicle manufacturing. Strong regulatory oversight and emphasis on compliance with EU type approval standards are increasing demand for structured testing and certification processes. Rapid development of electric and autonomous vehicle technologies requires extensive validation across performance and safety parameters. The country’s export-oriented automotive sector further sustains homologation service demand.

U.K. Automotive Homologation Services Market Insight

The U.K. market is supported by evolving vehicle approval frameworks and regulatory adjustments following changes in regional trade agreements. Growing focus on electric vehicle adoption and updated safety compliance standards is increasing certification requirements. Investments in automotive R&D and testing facilities enhance validation capabilities across new vehicle platforms. Continuous alignment with international automotive regulations ensures steady demand for homologation services.

North America Automotive Homologation Services Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by tightening emission regulations, expansion of electric vehicle production, and increasing cross-border vehicle trade. Regulatory bodies continue to strengthen compliance standards related to crash safety, fuel efficiency, and environmental performance. Rising adoption of advanced driver assistance systems and connected vehicle technologies requires extensive validation procedures. Ongoing modernization of testing infrastructure further supports regional growth.

U.S. Automotive Homologation Services Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its large automotive production base and comprehensive federal safety and emission regulations. Mandatory compliance with standards set by national regulatory agencies drives consistent demand for certification and validation services. Increasing development of electric, hybrid, and autonomous vehicles requires expanded testing across multiple performance parameters. Presence of established OEMs and independent testing laboratories strengthens the country’s position in the regional market.

Automotive Homologation Services Market Share

The automotive homologation services industry is primarily led by well-established companies, including:

- TÜV SÜD Group (Germany)

- Intertek Group plc (U.K.)

- DEKRA SE (Germany)

- Applus+ Services SA (Spain)

- SGS S.A. (Switzerland)

- Bureau Veritas (France)

- Eurofins Scientific (Luxembourg)

- MISTRAS Group (U.S.)

- Formel D Group (Germany)

- UL Solutions Inc. (U.S.)

- TÜV Rheinland AG (Germany)

- UTAC CERAM (France)

- IDIADA Automotive Technology (Spain)

- Element Materials Technology (U.K.)

Latest Developments in Global Automotive Homologation Services Market

- In January 2024, TÜV SÜD launched AI-powered homologation solutions designed to streamline regulatory approval processes for automotive manufacturers. By integrating artificial intelligence and machine learning into certification workflows, the company enhances testing accuracy, reduces approval timelines, and improves compliance efficiency. This development strengthens the competitive landscape of the automotive homologation services market by accelerating time-to-market for new vehicle models and promoting digital transformation across certification services

- In October 2023, DEKRA inaugurated a state-of-the-art automotive testing facility in China to address rising regional demand for regulatory compliance and vehicle certification. The new facility expands localized homologation capabilities, enabling faster testing cycles and improved service accessibility for domestic and international manufacturers operating in China. This expansion reinforces market growth by supporting high vehicle production volumes and strengthening global service providers’ footprint in the Asia-Pacific region

- In June 2023, Applus+ acquired Suzhou Chunfen Test Technology Services Co. Ltd. to enhance its automotive testing and homologation capabilities in China. The acquisition enables Applus+ to leverage expanded infrastructure and technical expertise, broadening its service portfolio for vehicle manufacturers requiring regulatory approval. This strategic move intensifies competition in the market and improves service capacity in one of the world’s largest automotive production hubs

- In March 2023, Bureau Veritas expanded its homologation services portfolio to include advanced validation solutions for electric and autonomous vehicles. The expansion addresses increasing regulatory complexity associated with battery systems, advanced driver assistance technologies, and next-generation vehicle platforms. This initiative enhances the company’s positioning in the evolving mobility landscape and supports growing demand for specialized certification services in the automotive homologation services market

- In February 2023, SGS SA strengthened its automotive homologation network by expanding accredited testing capabilities across Europe and Asia. The move improves cross-border certification support and ensures compliance with tightening emission and safety regulations in multiple jurisdictions. This development contributes to market expansion by increasing global testing capacity and facilitating faster regulatory approvals for vehicle manufacturers operating in international markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.