Global Automotive Over The Air Updates Market

Market Size in USD Billion

CAGR :

%

USD

6.38 Billion

USD

25.32 Billion

2025

2033

USD

6.38 Billion

USD

25.32 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.38 Billion | |

| USD 25.32 Billion | |

| % | |

|

Automotive Over the Air Updates Market Overview

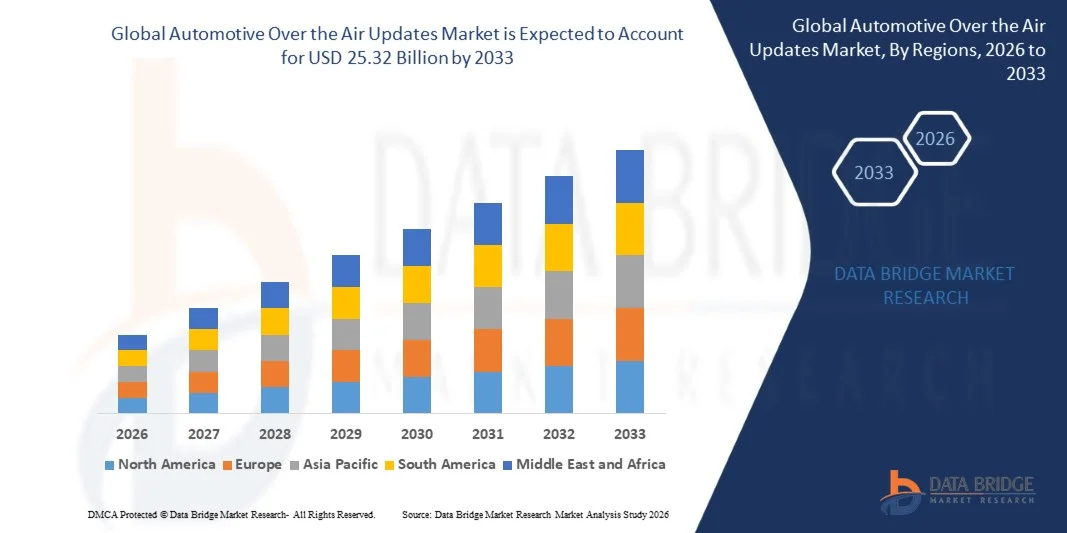

The Automotive Over the Air Updates Market was valued at USD 6.38 billion in 2025 and is projected to reach USD 25.32 billion by 2033, growing at a CAGR of 18.81% from 2026 to 2033. . The market is witnessing rapid expansion driven by the rising adoption of connected vehicles, increasing integration of advanced telematics systems, and growing demand for real-time software upgrades without requiring physical service center visits. Automakers are increasingly leveraging OTA platforms to enhance vehicle performance, improve infotainment systems, and deliver safety and cybersecurity patches efficiently.

The growing shift toward software-defined vehicles, combined with accelerating electric vehicle adoption and autonomous driving development, is significantly boosting the deployment of OTA update solutions. Automotive manufacturers are focusing on continuous feature enhancement, predictive maintenance, and lifecycle software monetization, which is further strengthening demand for secure and scalable OTA architectures across global automotive ecosystems.

Key Market Trends & Insights

- North America dominated the automotive over the air updates market with the largest revenue share in 2025, supported by strong penetration of connected vehicles, early adoption of electric vehicles, and presence of leading technology-driven automotive OEMs. The region benefits from advanced cloud infrastructure, widespread 5G deployment, and high consumer demand for digital in-vehicle experiences such as infotainment upgrades and ADAS enhancements, strengthening large-scale OTA implementation across both premium and mass-market vehicles.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of from 2026 to 2033. Growth is driven by rapid expansion of electric vehicle manufacturing in China, Japan, and South Korea, increasing government support for smart mobility ecosystems, and rising adoption of connected vehicle platforms among domestic automakers. The region’s strong electronics supply chain and large-scale digital infrastructure development are further accelerating OTA deployment across high-volume automotive production hubs.

- The Software Over-The-Air Technology segment held the largest market revenue share of approximately 58.6% in 2025 driven by its extensive use in infotainment systems, connected services, and continuous feature enhancement in software-defined vehicles. OEMs prefer software OTA due to its ability to enable real-time updates, reduce recall costs, and improve customer experience without physical intervention.

- The Firmware Over-The-Air Technology segment is projected to register the fastest growth at a CAGR of 19.4% from 2026 to 2033, driven by increasing integration of advanced electronic control units, ADAS systems, and vehicle cybersecurity requirements. Rising deployment in critical vehicle systems is accelerating adoption due to the need for secure, remote firmware patching and system-level performance upgrades.

- The Infotainment segment held the largest market revenue share of approximately 32.7% in 2025 driven by strong consumer demand for connected entertainment systems, navigation upgrades, and smartphone integration features. Automakers are continuously updating infotainment platforms to enhance user experience and maintain competitive differentiation.

- The Safety and Security segment is projected to register the fastest growth at a CAGR of 20.1% from 2026 to 2033, driven by increasing cybersecurity threats, regulatory focus on vehicle safety, and rising deployment of ADAS-enabled systems. Continuous OTA-based safety updates are becoming essential for maintaining vehicle compliance and operational reliability.

- The Passenger Car segment held the largest market revenue share of approximately 71.2% in 2025 driven by high adoption of connected features, strong consumer demand for smart mobility solutions, and increasing integration of infotainment and telematics systems in mid-range and premium vehicles.

- The Commercial Car segment is projected to register the fastest growth at a CAGR of 17.8% from 2026 to 2033, driven by expanding fleet digitization, logistics optimization, and demand for remote diagnostics and predictive maintenance solutions. Fleet operators are increasingly adopting OTA updates to reduce downtime and improve operational efficiency.

- The Battery Electric Vehicle segment held the largest market revenue share of approximately 46.5% in 2025 driven by rapid global EV adoption, strong government incentives, and high dependency on software-driven battery management and vehicle control systems.

- The Battery Electric Vehicle segment is projected to register the fastest growth at a CAGR of 21.3% from 2026 to 2033, driven by expanding charging infrastructure, rising environmental regulations, and continuous software upgrades for battery optimization, range improvement, and energy efficiency management.

Market Size & Forecast

- Global Market Value (2025): USD 6.38 Billion

- Expected Market Value (2033): USD 25.32 Billion

- Forecast CAGR (2026–2033): 18.81%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Over the Air Updates Market Segmentation

|

Attributes |

Automotive Over the Air Updates Key Market Insights |

|

Segments Covered |

· By Technology: Firmware Over-The-Air Technology, and Software Over-The-Air Technology · By Application Type: Electronic Control Unit, Infotainment, Safety and Security, Telematics Control Unit, and Others · By Vehicle Type: Passenger Car and Commercial Car · By Electric Vehicles: Battery Electric Vehicle, Hybrid Electric Vehicles, and Plug-In Hybrid Electric Vehicles |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Robert Bosch GmbH (Germany) |

|

Market Opportunities |

• Expansion Of Software Defined Vehicles Ecosystem |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Over the Air Updates Market Trends

Trend: Rapid Expansion Of Software Defined Vehicles And Connected Mobility Ecosystem

The automotive over the air updates market is witnessing strong growth driven by the rapid transition toward software defined vehicles, increasing vehicle connectivity, and rising demand for continuous feature upgrades without physical service intervention. Traditional vehicle update mechanisms are being replaced by cloud based OTA platforms that enable seamless delivery of software, firmware, and cybersecurity patches across global vehicle fleets.

In modern vehicles, manufacturers are increasingly integrating OTA systems, For instance to update infotainment systems, navigation maps, advanced driver assistance systems, and battery management software in electric vehicles, improving performance, safety, and user experience. Leading OEMs such as Tesla reported that over 90% of its global vehicle fleet regularly receives OTA updates, enabling continuous product improvement and reduced recall dependency.

The rapid expansion of electric vehicles and autonomous driving technologies is also accelerating demand for real time software optimization and remote diagnostics capabilities. In addition, fleet operators and mobility service providers are increasingly adopting OTA solutions to manage large connected vehicle networks efficiently, reduce downtime, and improve operational efficiency. Industry deployments in 2025 across North America and China demonstrated that OTA-enabled predictive updates reduced vehicle software related service visits by approximately 25–30%, improving lifecycle cost efficiency.

Automotive Over the Air Updates Market Dynamics

Key Market Driver: Rising Adoption Of Connected And Software Defined Vehicles

Automotive manufacturers are increasingly shifting toward software centric vehicle architectures where core functionalities are controlled through digital platforms rather than mechanical systems. This transition is being driven by rising consumer demand for connected features, regulatory focus on vehicle safety, and the need for continuous improvement in vehicle performance.

OEMs are actively deploying OTA systems, For instance to push performance upgrades, cybersecurity patches, and new infotainment features directly to vehicles, reducing dependency on dealership based updates. Major automakers such as Ford and BMW have expanded OTA capabilities across millions of connected vehicles globally, enabling faster recall management and improved customer engagement.

Similarly, electric vehicle manufacturers are leveraging OTA updates to optimize battery efficiency, charging performance, and energy management systems. Real world deployments in 2024 indicated that OTA based battery optimization updates improved EV range efficiency by approximately 5–8% in selected vehicle models across European and Asian markets.

Key Restraint/Challenge: Cybersecurity Risks And Complex Software Integration

The increasing reliance on connected vehicle ecosystems exposes automotive systems to cybersecurity vulnerabilities, data privacy risks, and potential remote hacking threats. As vehicles become more software dependent, ensuring secure communication channels and robust encryption protocols becomes critical for OEMs and suppliers.

In addition, integration challenges across multiple electronic control units, legacy vehicle platforms, and diverse global regulatory frameworks increase development complexity and deployment costs. Automakers must ensure compatibility across different vehicle models and regions, which slows down OTA rollout cycles.

Industry assessments indicate that cybersecurity related risks account for a significant portion of connected vehicle system development costs, with some OEMs allocating nearly 15–20% of their software development budgets toward security and compliance measures.

Key Market Opportunity: Expansion Of Electric Vehicles And Autonomous Driving Platforms

The rapid growth of electric vehicles and autonomous driving systems is creating substantial opportunities for OTA update solutions, as these platforms require continuous software improvements for performance, navigation accuracy, and safety enhancements. Modern vehicles increasingly depend on real time data processing and cloud connectivity, making OTA updates essential for long term functionality.

Automotive companies are increasingly deploying OTA systems, For instance for autonomous driving algorithm updates, ADAS calibration improvements, and EV battery optimization enhancements, ensuring continuous product evolution throughout vehicle lifecycle. In China and South Korea, EV manufacturers have reported that OTA enabled updates improved system response efficiency by nearly 10–15% in advanced driver assistance applications during 2025 pilot programs.

In addition, advancements in 5G connectivity, edge computing, and vehicle to everything (V2X) communication are further strengthening OTA capabilities. These technologies are enabling faster update deployment, reduced latency, and enhanced data security across connected mobility ecosystems in Asia-Pacific, North America, and Europe.

Automotive Over the Air Updates Market Scope

The market is segmented on the basis of technology, application type, vehicle type, and electric vehicles.

- By Technology

On the basis of technology, the automotive over the air updates market is segmented into Firmware Over-The-Air Technology and Software Over-The-Air Technology. The Software Over-The-Air Technology segment held the largest market revenue share of approximately 58.6% in 2025 driven by its extensive use in infotainment systems, connected services, and continuous feature enhancement in software-defined vehicles. OEMs prefer software OTA due to its ability to enable real-time updates, reduce recall costs, and improve customer experience without physical intervention.

The Firmware Over-The-Air Technology segment is projected to register the fastest growth at a CAGR of 19.4% from 2026 to 2033, driven by increasing integration of advanced electronic control units, ADAS systems, and vehicle cybersecurity requirements. Rising deployment in critical vehicle systems is accelerating adoption due to the need for secure, remote firmware patching and system-level performance upgrades.

- By Application Type

On the basis of application type, the market is segmented into Electronic Control Unit, Infotainment, Safety and Security, Telematics Control Unit, and Others. The Infotainment segment held the largest market revenue share of approximately 32.7% in 2025 driven by strong consumer demand for connected entertainment systems, navigation upgrades, and smartphone integration features. Automakers are continuously updating infotainment platforms to enhance user experience and maintain competitive differentiation.

The Safety and Security segment is projected to register the fastest growth at a CAGR of 20.1% from 2026 to 2033, driven by increasing cybersecurity threats, regulatory focus on vehicle safety, and rising deployment of ADAS-enabled systems. Continuous OTA-based safety updates are becoming essential for maintaining vehicle compliance and operational reliability.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Car and Commercial Car. The Passenger Car segment held the largest market revenue share of approximately 71.2% in 2025 driven by high adoption of connected features, strong consumer demand for smart mobility solutions, and increasing integration of infotainment and telematics systems in mid-range and premium vehicles.

The Commercial Car segment is projected to register the fastest growth at a CAGR of 17.8% from 2026 to 2033, driven by expanding fleet digitization, logistics optimization, and demand for remote diagnostics and predictive maintenance solutions. Fleet operators are increasingly adopting OTA updates to reduce downtime and improve operational efficiency.

- By Electric Vehicles

On the basis of electric vehicles, the market is segmented into Battery Electric Vehicle, Hybrid Electric Vehicles, and Plug-In Hybrid Electric Vehicles. The Battery Electric Vehicle segment held the largest market revenue share of approximately 46.5% in 2025 driven by rapid global EV adoption, strong government incentives, and high dependency on software-driven battery management and vehicle control systems.

The Battery Electric Vehicle segment is projected to register the fastest growth at a CAGR of 21.3% from 2026 to 2033, driven by expanding charging infrastructure, rising environmental regulations, and continuous software upgrades for battery optimization, range improvement, and energy efficiency management.

Automotive Over the Air Updates Market Regional Analysis

North America Automotive Over The Air Updates Market Insight

North America dominated the automotive over the air updates market with the largest revenue share of 38.6% in 2025, supported by rapid penetration of connected vehicles, strong 5G infrastructure, and early adoption of software-defined vehicle platforms. Automakers in the region are increasingly deploying OTA solutions to remotely update infotainment, powertrain control, and advanced driver assistance systems, reducing recall costs and improving vehicle lifecycle management. The presence of leading automotive OEMs and technology companies, along with high consumer demand for connected car features, further strengthens regional dominance and accelerates large-scale OTA deployment across passenger and commercial vehicles.

U.S. Automotive Over The Air Updates Market Insight

The U.S. automotive over the air updates market captured the largest revenue share in North America in 2025, driven by rapid expansion of electric vehicles and software-centric automotive architectures. Companies such as Tesla demonstrated large-scale OTA capability by delivering frequent performance, safety, and infotainment upgrades to millions of vehicles globally, setting a benchmark for the industry. The integration of cloud computing, cybersecurity frameworks, and AI-driven diagnostics is further accelerating adoption, enabling automakers to enhance vehicle performance, reduce service center dependency, and improve customer engagement through continuous software upgrades.

Europe Automotive Over The Air Updates Market Insight

The Europe automotive over the air updates market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent vehicle safety regulations, rising EV adoption, and strong push toward connected mobility. European automakers are increasingly implementing OTA systems to comply with UNECE regulations on software update management and cybersecurity in vehicles. Growing demand for premium connected features in passenger vehicles, combined with expansion of electric mobility infrastructure, is supporting widespread deployment of OTA platforms across both OEMs and Tier-1 suppliers.

U.K. Automotive Over The Air Updates Market Insight

The U.K. automotive over the air updates market is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of connected and electric vehicles along with rising demand for digital vehicle maintenance solutions. Automotive OEMs in the U.K. are focusing on OTA integration to enhance fleet management efficiency and reduce downtime in commercial vehicles. The growing digital ecosystem, supported by advanced telecom infrastructure and rising consumer preference for smart mobility solutions, is further strengthening market expansion.

Germany Automotive Over The Air Updates Market Insight

The Germany automotive over the air updates market is expected to witness significant growth from 2026 to 2033, supported by strong automotive manufacturing capabilities and rapid transition toward software-defined vehicles. Leading German automakers are integrating OTA platforms to enable remote diagnostics, predictive maintenance, and continuous feature enhancement in premium vehicles. The country’s focus on engineering innovation and compliance with strict automotive safety standards is accelerating adoption across both internal combustion and electric vehicle segments.

Asia-Pacific Automotive Over The Air Updates Market Insight

The Asia-Pacific automotive over the air updates market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising EV production, expanding smartphone connectivity ecosystems, and government initiatives supporting smart mobility. Countries such as China, Japan, and South Korea are leading adoption due to strong digital infrastructure and large-scale electric vehicle deployment. The region’s growing automotive manufacturing base and increasing integration of connected vehicle technologies are significantly boosting demand for OTA platforms across mass-market and premium vehicles.

Japan Automotive Over The Air Updates Market Insight

The Japan automotive over the air updates market is expected to witness strong growth from 2026 to 2033 due to advanced automotive electronics adoption and high consumer preference for technologically sophisticated vehicles. Japanese automakers are increasingly utilizing OTA systems for navigation updates, safety enhancements, and energy efficiency optimization in hybrid and electric vehicles. The country’s emphasis on precision engineering and smart mobility solutions is further supporting integration of OTA capabilities across next-generation vehicle platforms.

China Automotive Over The Air Updates Market Insight

The China automotive over the air updates market accounted for the largest revenue share in Asia-Pacific in 2025, driven by massive electric vehicle adoption, strong domestic OEM ecosystem, and government support for intelligent connected vehicles. Leading Chinese automakers such as BYD and NIO are heavily utilizing OTA updates to enhance vehicle performance, introduce new digital features, and improve autonomous driving capabilities. Rapid expansion of 5G infrastructure and smart city initiatives is further accelerating OTA deployment across both passenger and commercial vehicle segments.

Automotive Over the Air Updates Market Share

The Automotive Over the Air Updates industry is primarily led by well-established companies, including:

• Robert Bosch GmbH (Germany)

• Aptiv (Ireland)

• Airbiquity Inc. (U.S.)

• Qualcomm Technologies, Inc. (U.S.)

• NVIDIA Corporation (U.S.)

• Infineon Technologies AG (Germany)

• Wind River Systems, Inc. (U.S.)

• VMware, Inc. (U.S.)

• Vector Informatik GmbH (Germany)

• Trillium Secure, Inc. (U.S.)

• Argus Cyber Security Ltd. (Israel)

• Continental AG (Germany)

• Excelfore (U.S.)

• HARMAN International (U.S.)

• HERE (Netherlands)

• Karamba Security (Israel)

• NXP Semiconductors (Netherlands)

• Verizon (U.S.)

• Intel Corporation (U.S.)

• Garmin Ltd. (U.S.)

Latest Developments in Automotive Over the Air Updates Market

- In May 2025, Hyundai introduced a software enhancement via over-the-air update enabling Plug-and-Charge authentication for its 2025 Ioniq 5 models. This development simplifies EV charging by allowing automatic vehicle authentication at compatible charging stations without manual input. The upgrade improves user convenience, reduces charging time friction, and strengthens Hyundai’s position in connected electric mobility solutions, supporting broader adoption of seamless EV ecosystems

- In January 2025, Rivian and Volkswagen announced a strategic joint venture valued at USD 5.8 billion to co-develop next-generation electric vehicle platforms with integrated over-the-air update capabilities. The collaboration focuses on scalable software-defined architectures expected to be deployed in future models from 2027 onward. This partnership enhances development efficiency, accelerates software integration across vehicle lines, and strengthens competitiveness in the global EV software ecosystem

- In September 2024, Volvo Cars deployed a large-scale over-the-air update across approximately 2.5 million vehicles globally. The update expanded infotainment functionality and introduced improved energy management algorithms for enhanced efficiency in electric and hybrid models. This rollout strengthens Volvo’s digital service ecosystem, reduces dealership dependency for software updates, and enhances customer experience through continuous vehicle performance improvements

- In June 2024, HARMAN International launched OTA 12.0, introducing distributed onboard orchestration and expanded high-resolution image support across its connected vehicle platform. The upgrade enhances system flexibility and performance for more than 40 global automakers using HARMAN solutions. This advancement improves in-vehicle user experience, accelerates software deployment cycles, and reinforces HARMAN’s leadership in automotive connectivity solutions

- In March 2024, NVIDIA announced increased adoption of its DRIVE Thor centralized vehicle computing platform by leading transportation and mobility companies. The system is being deployed in electric vehicles, autonomous trucks, robotaxis, and delivery fleets. This advancement enhances AI-driven autonomous driving capabilities, improves computing efficiency, and accelerates the shift toward centralized software-defined vehicle architectures across the global automotive industry

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.