Global Automotive Surround View Systems Market

Market Size in USD Billion

CAGR :

%

USD

1.22 Billion

USD

3.30 Billion

2025

2033

USD

1.22 Billion

USD

3.30 Billion

2025

2033

| 2026 –2033 | |

| USD 1.22 Billion | |

| USD 3.30 Billion | |

| % | |

|

Automotive Surround View Systems Market Size

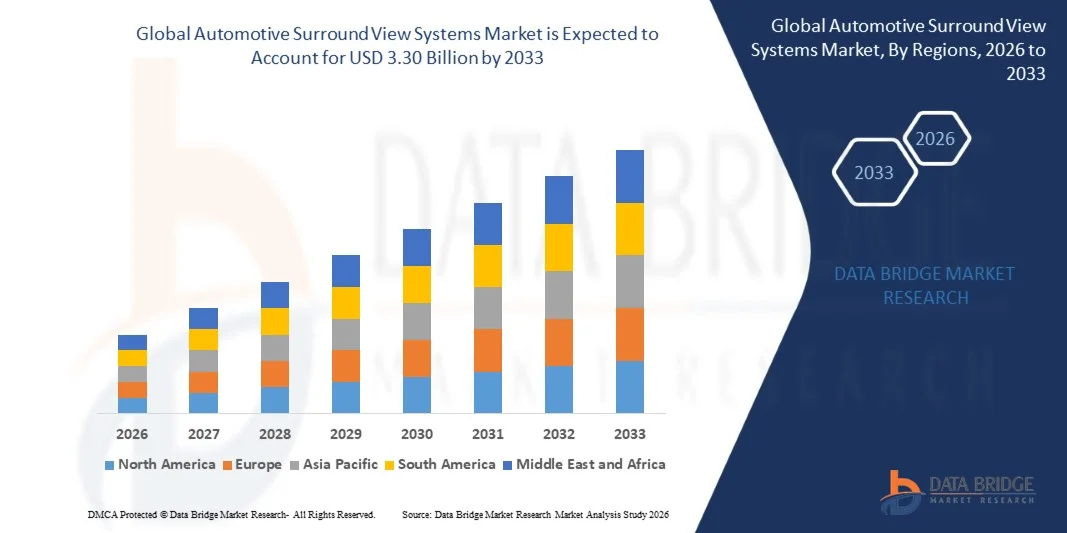

- The global automotive surround view systems market size was valued at USD 1.22 billion in 2025 and is expected to reach USD 3.30 billion by 2033, at a CAGR of 13.23% during the forecast period

- The market growth is largely fuelled by the increasing demand for enhanced vehicle safety features and growing integration of advanced driver assistance systems to improve driver awareness and reduce accident risks

- Rising adoption of premium and luxury vehicles, along with increasing consumer preference for parking assistance and convenience technologies, is further supporting the expansion of surround view system integration

Automotive Surround View Systems Market Analysis

- The market is witnessing rapid growth driven by increasing regulatory focus on vehicle safety and growing automaker emphasis on integrating camera-based monitoring systems to enhance visibility and reduce blind spots

- Technological advancements in camera sensors, image processing, and real-time monitoring, along with rising production of passenger vehicles and electric vehicles, are contributing to sustained market expansion

- North America dominated the automotive surround view systems market with the largest revenue share of 38.75% in 2025, driven by the growing demand for advanced driver assistance systems (ADAS), vehicle safety features, and parking convenience technologies

- Asia-Pacific region is expected to witness the highest growth rate in the global automotive surround view systems market, driven by increasing urbanization, rising vehicle ownership, and strong adoption of connected and safety-enhanced vehicles in countries such as China, Japan, and India. In addition, regional manufacturing capabilities for cameras and sensors, along with supportive government initiatives, are expanding accessibility and adoption of surround view systems

- The 4 Camera segment held the largest market revenue share in 2025, driven by its widespread adoption in mid-range and premium passenger vehicles and its cost-effective ability to provide complete 360-degree coverage. These systems offer sufficient visibility for parking and maneuvering, making them the preferred choice for most OEMs

Report Scope and Automotive Surround View Systems Market Segmentation

|

Attributes |

Automotive Surround View Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Surround View Systems Market Trends

“Rising Demand For Advanced Driver Assistance And Parking Safety Technologies”

• The growing focus on vehicle safety and driver convenience is significantly shaping the automotive surround view systems market, as consumers increasingly prefer vehicles equipped with 360-degree camera systems that reduce blind spots and improve parking accuracy. Surround view systems are gaining traction due to their ability to provide enhanced situational awareness and minimize accident risks, strengthening adoption across passenger and commercial vehicles and encouraging automakers to innovate with new camera and sensor technologies

• Increasing awareness around road safety, urban congestion, and advanced driver assistance systems (ADAS) has accelerated the demand for surround view systems in passenger cars, commercial vehicles, and SUVs. Safety-conscious consumers and fleet operators are actively seeking vehicles with enhanced monitoring systems, prompting manufacturers to prioritize integration of multi-camera setups and intelligent processing solutions

• Safety, convenience, and technological advancement trends are influencing purchasing decisions, with automakers emphasizing high-definition imaging, seamless integration with ADAS, and real-time monitoring capabilities. These factors help brands differentiate vehicles in a competitive market and build consumer trust, while also driving the adoption of advanced safety packages and connected vehicle solutions

• For instance, in 2024, Toyota in Japan and Ford in the U.S. expanded their vehicle portfolios by incorporating surround view camera systems in SUVs and premium passenger vehicles. These launches were introduced in response to rising consumer preference for advanced safety and parking assistance features, with distribution across dealerships and online channels. The products were also marketed as convenience- and safety-oriented solutions, enhancing brand loyalty and repeat purchases among target audiences

• While demand for surround view systems is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining performance reliability comparable to traditional parking aids. Manufacturers are also focusing on improving scalability, sensor accuracy, and developing innovative solutions that balance cost, quality, and functionality for broader adoption

Automotive Surround View Systems Market Dynamics

Driver

“Growing Focus On Vehicle Safety And Parking Assistance”

• Rising consumer demand for enhanced safety features and driver convenience is a major driver for the automotive surround view systems market. Automakers are increasingly integrating 360-degree camera solutions to reduce blind spots, support parking, and enhance situational awareness, aligning with safety regulations and customer expectations

• Expanding applications in SUVs, passenger cars, and commercial vehicles are influencing market growth. Surround view systems help improve parking efficiency, minimize collision risks, and support advanced driver assistance, enabling manufacturers to meet consumer expectations for technologically advanced and safe vehicles

• Vehicle manufacturers are actively promoting surround view camera systems through product innovation, bundled ADAS packages, and marketing campaigns. These efforts are supported by growing consumer preference for technologically advanced and safety-oriented vehicles, and they also encourage partnerships between camera system suppliers and automakers to enhance system functionality and reliability

• For instance, in 2023, BMW in Germany and General Motors in the U.S. reported increased incorporation of surround view systems across premium and mid-range vehicles. This expansion followed higher consumer demand for integrated safety and parking assistance solutions, driving repeat purchases and product differentiation. Both companies also highlighted system reliability and ADAS integration in marketing campaigns to strengthen consumer trust and brand loyalty

• Although rising safety and convenience trends support growth, wider adoption depends on cost optimization, sensor accuracy, and scalable production processes. Investment in supply chain efficiency, advanced imaging technology, and calibration systems will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Cost And Integration Complexity Compared To Conventional Parking Systems”

• The relatively higher cost of surround view systems compared to conventional parking aids remains a key challenge, limiting adoption among price-sensitive vehicle segments. High sensor and camera component costs, along with complex calibration and integration requirements, contribute to elevated pricing

• Consumer and manufacturer awareness of advanced surround view systems remains uneven, particularly in emerging markets where ADAS adoption is still developing. Limited understanding of system benefits restricts adoption across certain vehicle categories, leading to slower uptake in price-sensitive regions

• Integration and production challenges also impact market growth, as surround view systems require precise calibration, software integration with ADAS, and compatibility with existing vehicle electronics. Additional engineering complexity and testing requirements increase operational costs, and manufacturers must invest in training and development to maintain product performance

• For instance, in 2024, distributors in India and Thailand supplying passenger and commercial vehicles reported slower uptake of surround view systems due to higher prices and limited awareness of functional advantages compared to conventional parking aids. Calibration requirements and integration complexity were additional barriers, and some automakers limited inclusion to premium models

• Overcoming these challenges will require cost-efficient production, simplified integration processes, and focused educational initiatives for manufacturers and consumers. Collaboration between sensor suppliers, automakers, and certification bodies can help unlock the long-term growth potential of the global automotive surround view systems market. Furthermore, developing cost-competitive solutions and strengthening marketing strategies around safety and convenience benefits will be essential for widespread adoption

Automotive Surround View Systems Market Scope

The market is segmented on the basis of type, camera functioning, vehicle type, end user market, and component.

• By Type

On the basis of type, the automotive surround view systems market is segmented into 4 Camera, 5 Camera, 6 Camera, and Others. The 4 Camera segment held the largest market revenue share in 2025, driven by its widespread adoption in mid-range and premium passenger vehicles and its cost-effective ability to provide complete 360-degree coverage. These systems offer sufficient visibility for parking and maneuvering, making them the preferred choice for most OEMs.

The 5 Camera and 6 Camera segments are expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for higher precision, enhanced safety features, and integration with advanced driver assistance systems (ADAS). Vehicles equipped with additional cameras provide superior blind spot detection, curbside monitoring, and improved situational awareness, supporting adoption in premium and commercial vehicle segments.

• By Camera Functioning

On the basis of camera functioning, the market is segmented into Automatic and Manual. The Automatic segment held the largest market revenue share in 2025, fueled by convenience, real-time image processing, and integration with ADAS for collision avoidance and parking assistance. Automatic systems are increasingly preferred by consumers and fleet operators due to reduced human error and enhanced operational safety.

The Manual segment is expected to witness the fastest growth rate from 2026 to 2033, driven by demand in commercial and budget vehicle segments where cost-effective systems are implemented with selective driver activation. Manual operation provides flexibility and reduces system complexity for basic surround view functionality.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Vehicles and Commercial Vehicles. The Passenger Vehicle segment held the largest market revenue share in 2025, supported by rising consumer preference for safety, parking convenience, and integration with ADAS features in SUVs, sedans, and luxury cars.

The Commercial Vehicle segment is expected to witness the fastest growth rate from 2026 to 2033, driven by fleet modernization, government regulations on driver safety, and the need for enhanced visibility during urban and long-haul operations. Surround view systems are increasingly deployed to reduce blind spots and accidents in trucks, buses, and delivery vehicles.

• By End User Market

On the basis of end user market, the market is segmented into OEMs and Aftermarket. The OEM segment held the largest market revenue share in 2025, as automakers increasingly integrate surround view systems into new vehicles to enhance safety, comply with regulatory standards, and provide additional convenience features.

The Aftermarket segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer interest in retrofitting existing vehicles with 360-degree camera systems for improved safety and parking assistance. Aftermarket adoption is particularly high in regions with aging vehicle fleets.

• By Component

On the basis of component, the market is segmented into Sensors, Camera, and ECU. The Camera segment held the largest market revenue share in 2025, driven by advancements in high-definition imaging, wide-angle lenses, and integration with real-time processing software to deliver accurate surround view functionality.

The Sensors and ECU segments are expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing focus on ADAS integration, automated parking, and enhanced system performance. Sensors and ECUs improve obstacle detection, system reliability, and overall safety, encouraging adoption in both passenger and commercial vehicles.

Automotive Surround View Systems Market Regional Analysis

• North America dominated the automotive surround view systems market with the largest revenue share of 38.75% in 2025, driven by the growing demand for advanced driver assistance systems (ADAS), vehicle safety features, and parking convenience technologies

• Consumers in the region highly value the enhanced visibility, accident reduction, and seamless integration offered by surround view systems with other in-vehicle safety and infotainment technologies

• This widespread adoption is further supported by high vehicle production, increasing sales of premium vehicles, and a technologically inclined population, establishing surround view systems as a favored solution for both passenger and commercial vehicles

U.S. Automotive Surround View Systems Market Insight

The U.S. automotive surround view systems market captured the largest revenue share in 2025 within North America, fueled by rapid adoption of connected vehicles and advanced safety technologies. Consumers are increasingly prioritizing vehicle safety and parking assistance through 360-degree camera systems. The growing preference for ADAS-equipped vehicles, combined with robust demand for SUVs, sedans, and premium vehicles with integrated safety packages, further propels the market. Moreover, increasing integration of surround view systems with parking sensors, blind-spot detection, and infotainment interfaces is significantly contributing to market expansion.

Europe Automotive Surround View Systems Market Insight

The Europe automotive surround view systems market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent vehicle safety regulations and rising consumer demand for technologically advanced and eco-conscious vehicles. Increasing urbanization and the adoption of connected vehicles are fostering the integration of surround view systems. The region is experiencing significant growth across passenger and commercial vehicles, with systems being incorporated into both new models and retrofit programs.

U.K. Automotive Surround View Systems Market Insight

The U.K. automotive surround view systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising awareness of vehicle safety, urban parking challenges, and the demand for driver convenience. In addition, government safety regulations and increasing fleet modernization are encouraging both private and commercial vehicle owners to adopt 360-degree camera systems. The U.K.’s strong automotive industry, e-commerce, and vehicle aftermarket infrastructure are expected to continue supporting market growth.

Germany Automotive Surround View Systems Market Insight

The Germany automotive surround view systems market is expected to witness the fastest growth rate from 2026 to 2033, fueled by high consumer focus on vehicle safety, technological innovation, and integration with advanced driver assistance systems. Germany’s well-developed automotive infrastructure and emphasis on eco-friendly and high-tech vehicles promote the adoption of surround view systems across both passenger and commercial segments. The integration of 360-degree cameras with ADAS and parking assist solutions is also becoming increasingly prevalent.

Asia-Pacific Automotive Surround View Systems Market Insight

The Asia-Pacific automotive surround view systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, rising vehicle production, and growing adoption of connected and safety-enhanced vehicles in countries such as China, Japan, and India. The region’s increasing inclination toward technologically advanced vehicles, supported by government initiatives promoting vehicle safety, is accelerating market adoption. Furthermore, as APAC emerges as a manufacturing hub for vehicle camera and sensor components, affordability and accessibility of surround view systems are expanding to a wider consumer base.

Japan Automotive Surround View Systems Market Insight

The Japan automotive surround view systems market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high-tech automotive culture, urbanization, and strong focus on vehicle safety. The Japanese market emphasizes convenience and accident prevention, and the adoption of surround view systems is driven by the growing number of ADAS-equipped vehicles. Integration with parking sensors, infotainment systems, and other connected technologies is fueling growth, while Japan’s aging population further supports demand for easier-to-use, secure visibility solutions in both passenger and commercial vehicles.

China Automotive Surround View Systems Market Insight

The China automotive surround view systems market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive production, rising middle-class vehicle ownership, and high adoption of advanced technologies. China stands as one of the largest markets for passenger and commercial vehicles, and surround view systems are becoming increasingly popular for enhanced safety and parking convenience. The push towards smart cities, government safety initiatives, and availability of cost-effective systems, alongside strong domestic component manufacturing, are key factors propelling the market in China

Automotive Surround View Systems Market Share

The Automotive Surround View Systems industry is primarily led by well-established companies, including:

- Magna International Inc. (Canada)

- Continental AG (Germany)

- Texas Instruments Incorporated (U.S.)

- FUJITSU (Japan)

- DENSO-Holding GmbH & Co. KG (Germany)

- Renesas Electronics Corporation (Japan)

- Clarion (Japan)

- AISIN SEIKI Co., Ltd. (Japan)

- Xylon d.o.o. (Slovenia)

- Ambarella International LP. (U.S.)

- Robert Bosch GmbH (Germany)

- Mobileye (Israel)

- BorgWarner Inc. (U.S.)

- HYUNDAI MOBIS (South Korea)

- SAMSUNG (South Korea)

- Intel Corporation (U.S.)

- OmniVision Technologies, Inc. (U.S.)

- Gazer Ltd. (Israel)

- NXP Semiconductors (Netherlands)

Latest Developments in Global Automotive Surround View Systems Market

- In January 2024, Renesas Electronics Corporation introduced the RAA279974 4-channel Automotive HD Link (AHL) video decoder as part of its AHL portfolio. This new solution processes four camera inputs simultaneously, enabling high-definition video transmission for surround-view and multi-camera automotive applications. By reducing reliance on expensive cables and connectors, it offers a cost-effective option for vehicle manufacturers, enhancing ADAS and parking assistance capabilities while supporting broader adoption of advanced camera systems across passenger and commercial vehicles

- In January 2023, ZF launched the Smart Camera 6, designed for automated driving and ADAS integration. The camera features an 8-megapixel sensor with a 120-degree field of view, providing over four times the image resolution of its predecessor. Its enhanced processing power allows for advanced functionalities such as real-time object detection, lane monitoring, and collision avoidance, strengthening vehicle safety and accelerating the deployment of sophisticated surround-view and ADAS technologies in the automotive market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.