Global Autorefractor Keratometer Device Market

Market Size in USD Billion

CAGR :

%

USD

1.28 Billion

USD

2.23 Billion

2025

2033

USD

1.28 Billion

USD

2.23 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.28 Billion | |

| USD 2.23 Billion | |

| % | |

|

Autorefractor Keratometer Device Market Overview

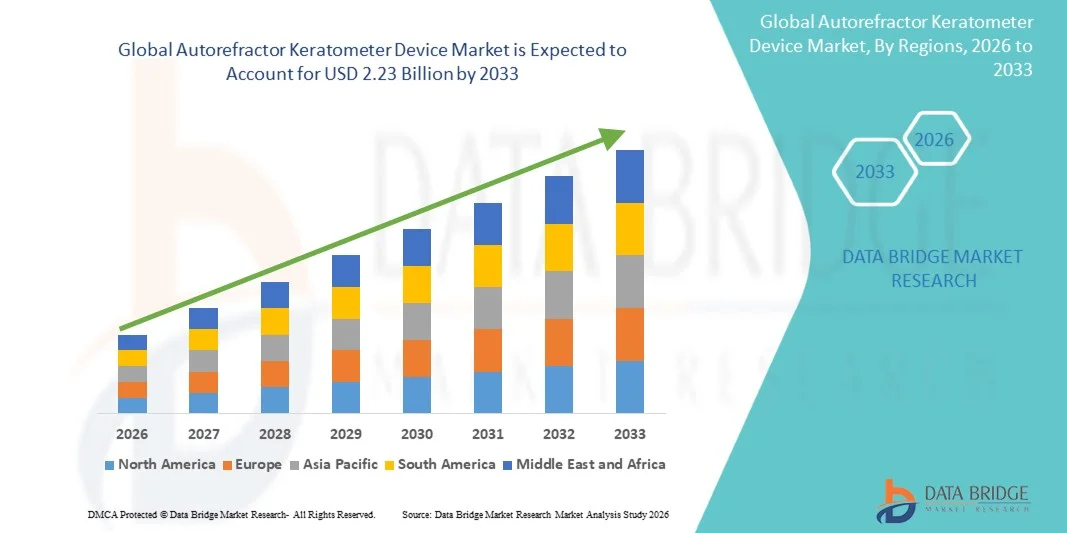

The global autorefractor keratometer device market was valued at USD 1.28 billion in 2025 and is projected to reach USD 2.23 billion by 2033, growing at a CAGR of 7.2% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of refractive vision disorders, increasing demand for early and accurate eye examination, and rapid adoption of automated ophthalmic diagnostic equipment across healthcare facilities.

The growing burden of myopia, hyperopia, and astigmatism globally, particularly among aging populations and digitally exposed younger demographics, is significantly increasing the need for precise and efficient vision assessment tools. In addition, technological advancements such as wavefront-based autorefractors, AI-integrated keratometers, and portable handheld devices are improving diagnostic accuracy and workflow efficiency. Expanding ophthalmology clinics, rising eye screening programs, and increasing investments in vision care infrastructure are further accelerating the adoption of autorefractor keratometer systems in both developed and emerging markets.

Key Market Trends & Insights

- North America dominated the global autorefractor keratometer device market with the largest revenue share of 38.6% in 2025, supported by advanced ophthalmic infrastructure, high adoption of digital eye examination technologies, and strong presence of key medical device manufacturers.

- The Corneal Topography Systems segment led the market with a 28.32% share in 2025, driven by its critical role in mapping corneal curvature and detecting refractive errors with high precision.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% during 2026–2033, fueled by rising prevalence of refractive errors, expanding eye care accessibility, and increasing investments in optical healthcare services across emerging economies.

- Wavefront Aberrometers are the fastest-growing product type, projected to register a CAGR of 7.0%, reflecting the surge in demand for highly precise and personalized vision correction solution.

- The Tabletop Devices segment dominated the portability category with a 60.65% revenue share in 2025, led by their widespread use in hospitals, ophthalmic clinics, and diagnostic centers.

- Myopia accounted for 45.48% of the market, preferred by the rapidly increasing global prevalence of nearsightedness, particularly among children and young adults.

- The Handheld Devices segment is the fastest-growing portability category, with a CAGR of 7.5%, driven by rising demand for portable and point-of-care vision screening solutions.

Market Size & Forecast

- Global Market Value (2025): USD 1.28 Billion

- Expected Market Value (2033): USD 2.23 Billion

- Forecast CAGR (2026–2033): 7.2%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Autorefractor Keratometer Device Market Segmentation

|

Attributes |

Autorefractor Keratometer Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Topcon Healthcare (Japan) · NIDEK Co., Ltd. (Japan) · Carl Zeiss Meditec AG (Germany) · Canon Medical Systems (Japan) · Haag-Streit AG (Switzerland) · Essilor Instruments (France) · Righton Optical Co., Ltd. (Japan) · Reichert Technologies (U.S.) · Keeler Ltd. (U.K.) · Marco Ophthalmic, Inc. (U.S.) · Tomey Corporation (Japan) · Rexxam Co., Ltd. (Japan) · Essilor Group (France) · Bon Optic Vertriebsgesellschaft (Germany) · Huvitz Co., Ltd. (South Korea) · Unicos Co., Ltd. (South Korea) · Potec Co., Ltd. (South Korea) · Luneau Technology Group (France) · CSO - Costruzione Strumenti Oftalmici (Italy) · Medmont International Pty Ltd (Australia) |

|

Market Opportunities |

· Growing adoption of AI-powered autorefractor–keratometer systems · Expansion of mobile and community-based vision screening programs · Rising integration of ophthalmic diagnostic devices into tele-ophthalmology platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global Autorefractor Keratometer Device Market Trends

Trend: Rising Adoption of AI-Integrated Ophthalmic Diagnostic Systems

Eye care providers are increasingly shifting toward AI-enabled autorefractor–keratometer devices as clinics and hospitals aim to improve diagnostic precision and reduce examination time per patient. These systems use automated algorithms to analyze refractive errors such as myopia, hyperopia, and astigmatism with higher consistency compared to manual methods. Integration of digital corneal mapping and wavefront analysis is also improving the accuracy of prescriptions, especially in complex cases. In addition, the adoption of portable and digital systems is expanding rapidly in outpatient clinics, optical retail chains, and mobile eye screening units. This is particularly important in emerging economies, where large populations require fast, cost-effective vision testing. The growing use of connected devices that can store and transfer patient data digitally is further improving workflow efficiency and enabling better long-term patient monitoring.

Global Autorefractor Keratometer Device Market Dynamics

Key Market Driver: Increasing Prevalence of Refractive Errors and Vision Disorders

A major growth driver for the market is the rising global burden of refractive errors, especially myopia, which is increasing significantly among children and young adults due to prolonged screen exposure and digital device usage. At the same time, aging populations are contributing to higher cases of hyperopia and other vision-related disorders, increasing overall demand for routine eye examinations. Healthcare systems are under pressure to handle large patient volumes efficiently, which is accelerating the shift from manual refraction methods to automated autorefractor keratometer devices. These systems help eye care professionals reduce consultation time while maintaining diagnostic accuracy, making them essential in high-traffic hospitals, ophthalmic clinics, and optical chains. Governments and NGOs are also expanding vision screening programs, further driving device adoption in both urban and rural healthcare settings.

Key Restraint/Challenge: High Cost of Advanced Ophthalmic Diagnostic Systems

Despite strong demand, the market faces a significant barrier due to the high cost of advanced autorefractor–keratometer systems, particularly those with AI integration, digital imaging, and multi-functional diagnostic capabilities. These systems require substantial upfront investment, which limits adoption in small clinics, independent optometry practices, and low-resource healthcare environments. Beyond initial purchase costs, ongoing expenses such as calibration, software licensing, technical servicing, and periodic upgrades add to the total cost of ownership. In addition, training requirements for staff to effectively operate advanced systems can further slow adoption. As a result, many small-scale providers continue to rely on traditional or semi-automated devices, especially in price-sensitive regions

Key Market Opportunity: Expansion of Portable and Tele-Ophthalmology Enabled Devices

One of the most promising opportunities in the market is the rapid expansion of portable autorefractor keratometer devices integrated with tele-ophthalmology platforms. These solutions enable remote vision screening, allowing eye care professionals to assess patients in rural, remote, or underserved regions without requiring physical clinic visits. Handheld and mobile devices are becoming increasingly important in large-scale screening programs conducted by governments, NGOs, and corporate eye health initiatives. When combined with cloud-based data storage and real-time connectivity, these devices allow instant sharing of diagnostic results with specialists located elsewhere, improving referral efficiency and treatment timelines. This shift toward decentralized and connected eye care is expected to significantly expand market penetration, particularly in emerging economies where access to ophthalmic specialists is limited but demand for vision correction services is rapidly increasing.

Global Autorefractor Keratometer Device Market Scope

The autorefractor keratometer device market is segmented on the basis of product type, portability, application, and end user.

- By Product Type

On the basis of product type, the global autorefractor keratometer device market is segmented into retinoscopes, OCT scanners, corneal topography systems, visual field analyzers, ophthalmic ultrasound systems, fundus cameras, ophthalmoscopes, optical biometry systems, specular microscopes, wavefront aberrometers, other equipment types, and accessories. The Corneal Topography Systems segment dominated the market with an 28.32% share in 2025, owing to its critical role in mapping corneal curvature and detecting refractive errors with high precision. These systems are widely used in ophthalmic clinics and hospitals for pre-operative assessments, contact lens fitting, and diagnosis of corneal disorders. Their integration with autorefractor keratometers enhances diagnostic accuracy and workflow efficiency. Increasing demand for advanced refractive surgery procedures such as LASIK is further supporting this segment. In addition, technological improvements in imaging resolution and automation are strengthening its clinical adoption. High reliability and diagnostic depth make it the most widely utilized segment in comprehensive eye examinations.

The Wavefront Aberrometers segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by increasing demand for highly precise and personalized vision correction solutions. These devices provide detailed analysis of optical imperfections beyond standard refractive errors, enabling customized treatment planning. Rising adoption in premium ophthalmic care centers and refractive surgery clinics is significantly boosting demand. Integration with AI-based diagnostic platforms is further improving accuracy and clinical decision-making. Growing awareness of advanced vision correction techniques among patients is also supporting adoption. In addition, continuous advancements in optical imaging technologies are reducing complexity and improving usability.

- By Portability

On the basis of portability, the global autorefractor keratometer device market is segmented into tabletop devices and handheld devices. The Tabletop Devices segment dominated the market with an 60.65% share in 2025, driven by their widespread use in hospitals, ophthalmic clinics, and diagnostic centers. These systems offer high accuracy, stability, and multi-functionality, making them suitable for comprehensive eye examinations. They are often integrated into full diagnostic workstations, enabling efficient patient flow in high-volume healthcare settings. Their ability to deliver consistent and precise measurements makes them the standard choice for professional eye care. Continuous technological upgrades, including automated alignment and digital output systems, are enhancing usability. Strong institutional demand ensures their continued dominance in the market.

The Handheld Devices segment is projected to grow at the fastest CAGR of 7.5% from 2026 to 2033, driven by rising demand for portable and point-of-care vision screening solutions. These devices are increasingly used in rural outreach programs, mobile eye camps, and pediatric screening initiatives. Their lightweight design and ease of use make them ideal for large-scale community screening. Growing tele-ophthalmology adoption is further enhancing their utility by enabling remote diagnosis. Declining device costs and improving accuracy are accelerating market penetration. Expanding healthcare access in emerging economies is also a key growth driver.

- By Application

On the basis of application, the global autorefractor keratometer device market is segmented into hyperopia, myopia, and other ophthalmic conditions. The Myopia segment dominated the market with an 45.48% share in 2025, driven by the rapidly increasing global prevalence of nearsightedness, particularly among children and young adults. Rising screen time, digital device usage, and urban lifestyle changes are major contributing factors. Myopia screening programs in schools and communities are significantly increasing device utilization. Autorefractor keratometers play a key role in early detection and prescription accuracy for corrective lenses. Growing awareness of myopia progression and its complications is further supporting demand. The segment continues to expand due to increasing global eye health initiatives.

The Other Ophthalmic Conditions segment is expected to grow at the fastest CAGR of 6.5% from 2026 to 2033, driven by rising diagnosis of astigmatism, presbyopia, and corneal abnormalities. Increasing adoption of comprehensive eye screening programs is expanding the use of diagnostic devices beyond basic refractive errors. Integration of advanced imaging technologies is enabling detection of complex ocular conditions. Growing aging population is also contributing to higher prevalence of multifactorial vision disorders. Expansion of preventive eye care services is further accelerating demand.

- By End User

On the basis of end user, the global autorefractor keratometer device market is segmented into hospitals, ophthalmic clinics, and diagnostic centers. The Ophthalmic Clinics segment dominated the market with an 50.55% share in 2025, owing to their primary role in routine vision testing, refractive error diagnosis, and prescription services. These clinics handle high patient volumes requiring fast and accurate diagnostic tools. Autorefractor keratometers are essential equipment in optometry workflows, enabling efficient patient throughput. Increasing demand for outpatient eye care services is further strengthening this segment. Continuous upgrades in diagnostic infrastructure within private clinics are supporting growth. The segment benefits from strong dependence on regular vision correction needs across populations.

The Diagnostic Centers segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising demand for centralized, technology-driven eye screening services. These centers are increasingly equipped with advanced ophthalmic imaging and diagnostic systems. Growing outsourcing of diagnostic services by hospitals and clinics is boosting utilization. Expansion of preventive healthcare programs is also supporting growth. Increasing adoption of automated and AI-based diagnostic workflows is improving efficiency. Rising healthcare investments in emerging markets are further accelerating expansion.

Global Autorefractor Keratometer Device Market Regional Analysis

North America dominated the global autorefractor keratometer device market with the largest revenue share of 38.6% in 2025, supported by advanced ophthalmic infrastructure, high adoption of digital eye examination technologies, and strong presence of key medical device manufacturers. The region also benefits from high healthcare expenditure, widespread availability of routine eye screening services, and strong insurance coverage for vision care. Increasing prevalence of refractive errors, particularly myopia and presbyopia, along with growing demand for early diagnosis and preventive eye care, is further driving market growth. Rising integration of AI-enabled and digital ophthalmic diagnostic systems continues to strengthen North America’s leadership position in the global market.

U.S. Autorefractor Keratometer Device Market Insight

The U.S. autorefractor keratometer device market is witnessing strong growth due to high prevalence of refractive errors, advanced ophthalmic healthcare infrastructure, and widespread adoption of automated diagnostic technologies. The country’s well-established network of ophthalmology clinics and optical chains, along with strong reimbursement systems, is driving demand for accurate and efficient vision testing solutions. In addition, increasing use of AI-enabled diagnostic devices and growing focus on preventive eye care are supporting market expansion across hospitals and specialty eye care centers. Rising adoption of digital eye examination systems further strengthens the U.S. position as a key market.

Europe Autorefractor Keratometer Device Market Insight

The Europe autorefractor keratometer device market remains a major contributor to global revenue, supported by strong healthcare systems, high awareness of vision disorders, and increasing adoption of advanced ophthalmic diagnostic equipment. The region benefits from structured eye screening programs, favorable regulatory frameworks, and growing investment in modern optometry infrastructure. Rising prevalence of myopia and age-related vision conditions is further boosting demand for automated refractive testing devices. In addition, increasing integration of digital and AI-based ophthalmic technologies continues to enhance diagnostic efficiency across the region.

U.K. Autorefractor Keratometer Device Market Insight

The U.K. autorefractor keratometer device market is experiencing steady growth, driven by rising demand for efficient eye screening solutions in both public healthcare and private optical chains. Increasing investment in ophthalmic clinics and growing focus on early detection of refractive errors are supporting market expansion. The adoption of portable and digital diagnostic systems is improving accessibility in community eye care programs. Furthermore, integration of advanced imaging and automated refraction technologies is enhancing clinical accuracy and workflow efficiency.

Germany Autorefractor Keratometer Device Market Insight

The Germany autorefractor keratometer device market is expanding steadily due to the country’s strong healthcare infrastructure, high adoption of medical technologies, and increasing focus on precision diagnostics. Ophthalmic clinics and diagnostic centers are widely deploying automated refractive systems for efficient patient management. Growing prevalence of vision disorders among aging populations and increasing demand for advanced eye examination tools are further driving market growth. Continuous innovation in optical diagnostics and strong emphasis on quality healthcare services are supporting Germany’s market position.

Asia-Pacific Autorefractor Keratometer Device Market Insight

The Asia-Pacific autorefractor keratometer device market is expected to witness rapid growth, driven by rising prevalence of refractive errors, expanding healthcare infrastructure, and increasing adoption of modern ophthalmic diagnostic systems. Countries such as China, India, and Japan are experiencing strong demand due to growing awareness of vision health and expanding access to eye care services. Increasing government-led vision screening programs and rising investments in optical clinics are further supporting market expansion. In addition, growing penetration of portable diagnostic devices is accelerating adoption across rural and semi-urban regions.

Japan Autorefractor Keratometer Device Market Insight

The Japan autorefractor keratometer device market is witnessing consistent growth due to its advanced healthcare system, high technological adoption, and strong focus on preventive eye care. Ophthalmic clinics and hospitals are increasingly utilizing automated diagnostic systems for accurate and efficient refractive assessments. Rising cases of age-related vision disorders and increasing demand for precision ophthalmic diagnostics are further supporting market growth. In addition, integration of AI-based imaging and digital measurement technologies is enhancing diagnostic accuracy and workflow efficiency.

China Autorefractor Keratometer Device Market Insight

The China autorefractor keratometer device market is growing rapidly, driven by a large patient population, increasing prevalence of myopia, and expanding ophthalmic healthcare infrastructure. Rising government initiatives for vision screening in schools and communities are significantly boosting device adoption. The country is also witnessing strong growth in ophthalmic clinics and optical retail chains, increasing demand for automated diagnostic tools. Furthermore, rapid technological advancements, growing healthcare investments, and increasing awareness of eye health are positioning China as one of the fastest-growing markets globally.

Global Autorefractor Keratometer Device Market Share

The autorefractor keratometer device industry is primarily led by well-established companies, including:

- Topcon Healthcare (Japan)

- NIDEK Co., Ltd. (Japan)

- Carl Zeiss Meditec AG (Germany)

- Canon Medical Systems (Japan)

- Haag-Streit AG (Switzerland)

- Essilor Instruments (France)

- Righton Optical Co., Ltd. (Japan)

- Reichert Technologies (U.S.)

- Keeler Ltd. (U.K.)

- Marco Ophthalmic, Inc. (U.S.)

- Tomey Corporation (Japan)

- Rexxam Co., Ltd. (Japan)

- Essilor Group (France)

- Bon Optic Vertriebsgesellschaft (Germany)

- Huvitz Co., Ltd. (South Korea)

- Unicos Co., Ltd. (South Korea)

- Potec Co., Ltd. (South Korea)

- Luneau Technology Group (France)

- CSO - Costruzione Strumenti Oftalmici (Italy)

- Medmont International Pty Ltd (Australia)

Latest Developments in Global Autorefractor Keratometer Device Market

- In November 2025, Topcon Healthcare received FDA 510(k) clearance for its OMNIA 4-in-1 automated pretesting platform, which integrates autorefractor, keratometer, tonometer, and pachymeter functions into a single diagnostic system, improving workflow efficiency and expanding AI-enabled ophthalmic diagnostics in clinical settings

- In August 2024, EssilorLuxottica expanded its Visionix ophthalmic diagnostics ecosystem, strengthening integration of refraction and keratometry data into connected digital platforms to support improved eye examination workflows and long-term refractive error tracking across clinics

- In May 2023, NIDEK introduced advancements in its autorefractor and keratometer product line with enhanced automation and improved measurement accuracy, supporting faster and more consistent refractive testing in high-volume ophthalmic practices

- In March 2022, Canon Medical Systems highlighted upgrades to its ophthalmic diagnostic equipment portfolio, including improved autorefractor–keratometer performance and digital imaging integration aimed at enhancing clinical efficiency and diagnostic precision

- In June 2021, Haag-Streit strengthened its ophthalmic diagnostics offering by advancing automated refraction and keratometry capabilities within its eye examination systems, supporting more efficient workflows in optometry and ophthalmology clinics

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.