Global Body In White Market

Market Size in USD Billion

CAGR :

%

USD

90.19 Billion

USD

110.40 Billion

2025

2033

USD

90.19 Billion

USD

110.40 Billion

2025

2033

| 2026 –2033 | |

| USD 90.19 Billion | |

| USD 110.40 Billion | |

| % | |

|

Body in White Market Size

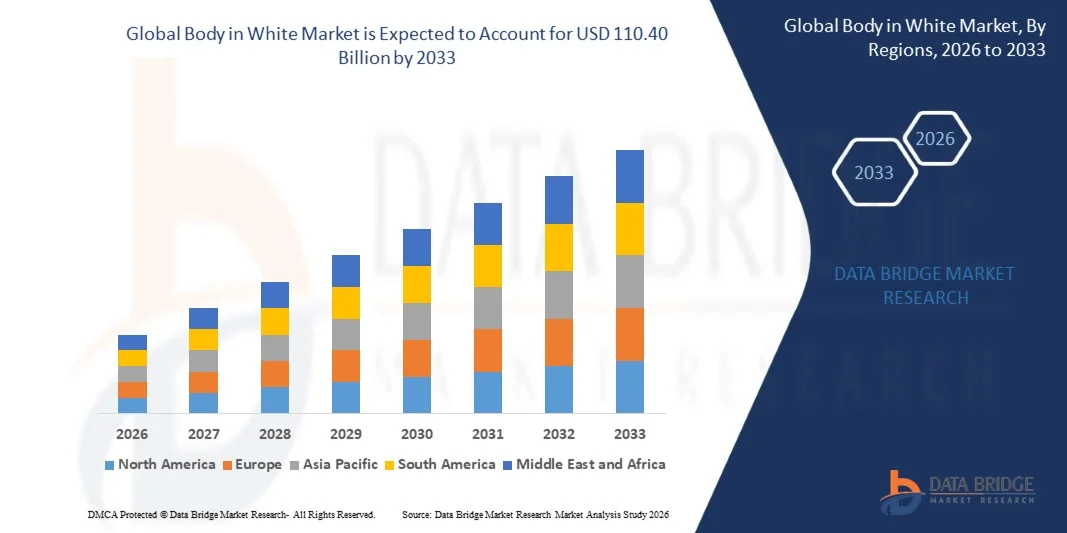

- The global body in white market size was valued at USD 90.19 billion in 2025 and is expected to reach USD 110.40 billion by 2033, at a CAGR of 2.56% during the forecast period

- The market growth is largely fueled by the increasing demand for lightweight, fuel-efficient, and crash-resistant vehicle structures across passenger and commercial vehicle segments, leading to greater adoption of advanced Body in White engineering and manufacturing solutions

- Furthermore, rapid expansion of electric vehicle production, rising focus on vehicle safety regulations, and continuous advancements in high-strength materials and automated manufacturing technologies are strengthening the need for optimized Body in White architectures. These converging factors are accelerating the adoption of modern BIW solutions, thereby significantly boosting the industry’s growth

Body in White Market Analysis

- Body in White refers to the stage in automotive manufacturing where a vehicle’s sheet metal components are assembled into a single structure before painting and final assembly, forming the core structural frame of the vehicle

- The escalating demand for Body in White systems is primarily driven by rising vehicle production, increasing emphasis on structural safety and lightweight design, and the growing shift toward electric and next-generation vehicle platforms

- Asia-Pacific dominated the body in white market in 2025, due to high automotive production volumes and strong presence of leading OEM manufacturing hubs

- North America is expected to be the fastest growing region in the body in white market during the forecast period due to rising demand for electric vehicles, pickup trucks, and lightweight automotive structures

- Monocoque segment dominated the market with a market share of 62.3% in 2025, due to its widespread use in passenger vehicles due to superior weight efficiency and structural integration. Monocoque construction enables better crash energy distribution and improved fuel economy, making it the preferred choice for modern automotive design

Report Scope and Body in White Market Segmentation

|

Attributes |

Body in White Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Body in White Market Trends

“Increasing Use of Lightweight Materials in Body in White Structures”

- A significant trend in the Body in White market is the increasing use of lightweight materials such as high-strength steel, aluminum alloys, and composite materials combined with advanced joining technologies to improve structural efficiency and crash performance. This shift is driven by the automotive industry’s focus on vehicle weight reduction, safety enhancement, and improved manufacturing precision across mass production platforms

- For instance, BMW Group extensively integrates aluminum and carbon-fiber reinforced polymers in its Body in White structures across models such as the BMW i series to reduce vehicle weight and improve efficiency. Such applications strengthen structural rigidity while supporting compliance with stringent emission and safety regulations

- The growing transition toward electric vehicle platforms is accelerating the redesign of Body in White architectures to accommodate battery packs and optimize structural space utilization. This is enabling manufacturers to develop dedicated EV platforms with improved load distribution and enhanced crash management systems

- Automotive OEMs are increasingly adopting advanced joining processes such as laser welding, adhesive bonding, and self-piercing riveting to improve assembly precision and structural durability. This is enhancing production quality while enabling efficient integration of multi-material vehicle bodies

- The demand for modular vehicle platforms is also influencing Body in White design strategies, allowing manufacturers to use common structural architectures across multiple models. This is improving production scalability and reducing overall development complexity

- The market is witnessing a broader shift toward digital simulation and virtual prototyping in Body in White development, enabling early-stage optimization of structural performance. This is reducing material waste and improving overall manufacturing efficiency across automotive production ecosystems

Body in White Market Dynamics

Driver

“Rising Demand for Fuel Efficiency and EV Production”

- The increasing demand for fuel-efficient vehicles and the rapid expansion of electric vehicle production are driving the need for optimized Body in White structures that reduce weight while maintaining safety and performance standards. This is encouraging automotive manufacturers to redesign vehicle frameworks to achieve improved energy efficiency and extended EV range

- For instance, Tesla Inc. utilizes optimized Body in White architectures in its Model 3 and Model Y platforms to support battery integration and improve structural efficiency. These designs enhance vehicle range while maintaining high safety standards through reinforced structural engineering

- The global push toward emission reduction regulations is accelerating the adoption of lightweight Body in White designs that support lower fuel consumption and reduced carbon emissions. This is pushing OEMs to invest in advanced materials and innovative manufacturing processes

- The rapid expansion of electric mobility is increasing the need for structurally efficient vehicle platforms capable of accommodating heavy battery systems without compromising performance. This is reshaping traditional automotive body engineering approaches across global manufacturers

- The sustained growth in passenger and commercial electric vehicle demand continues to reinforce this driver, making Body in White optimization a key enabler of next-generation automotive development

Restraint/Challenge

“High Capital Cost of Automated Body in White Systems”

- The Body in White market faces significant challenges due to the high capital investment required for automated production systems, robotics, and precision welding technologies used in modern automotive manufacturing plants. This creates financial barriers for manufacturers aiming to upgrade or expand production capabilities

- For instance, Mercedes-Benz operates highly automated Body in White production lines in its Sindelfingen plant in Germany, utilizing advanced robotics and flexible manufacturing systems that require substantial investment and ongoing maintenance costs. These systems demand continuous technological upgrades to maintain efficiency and competitiveness

- The integration of complex automation systems into existing manufacturing infrastructure increases operational complexity and requires highly skilled technical expertise. This adds to training costs and slows down the adoption of fully automated Body in White production lines.

- The need for synchronization between multiple robotic systems and precision assembly equipment increases the risk of production bottlenecks and system downtime. This affects overall manufacturing efficiency and output consistency across automotive plants

- The market continues to face challenges in balancing automation efficiency with cost-effectiveness, making capital-intensive infrastructure a key restraint in the widespread adoption of advanced Body in White manufacturing technologies

Body in White Market Scope

The market is segmented on the basis of vehicle type, construction type, manufacturing method, component position, component, and material type.

• By Vehicle Type

On the basis of vehicle type, the Body in White market is segmented into PC, LCV, M&HCV, and EV. The PC segment dominated the largest market revenue share in 2025, driven by high global production volumes of passenger cars and continuous demand for lightweight yet rigid body structures. Passenger cars extensively use Body in White assemblies to achieve crash safety compliance, structural integrity, and improved fuel efficiency. Large-scale OEM manufacturing and standardized platform architectures further strengthen PC dominance across both developed and emerging automotive markets. Increasing consumer preference for comfort and safety features continues to reinforce this segment’s leadership.

The EV segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by rapid electrification trends and rising investments in electric mobility platforms. EV manufacturers require optimized Body in White structures to accommodate battery packs, enhance rigidity, and reduce overall vehicle weight. In addition, the shift toward dedicated EV platforms is accelerating redesign of structural architectures and material usage. Growing regulatory pressure for emission reduction and supportive government incentives further drive adoption of EV-specific BIW solutions.

• By Construction Type

On the basis of construction type, the market is segmented into frame mounted and monocoque structures. The monocoque segment dominated the largest market revenue share of 62.3% in 2025, driven by its widespread use in passenger vehicles due to superior weight efficiency and structural integration. Monocoque construction enables better crash energy distribution and improved fuel economy, making it the preferred choice for modern automotive design. High adoption across compact and mid-size cars, along with ease of mass production, continues to strengthen its market position. OEM focus on lightweight architectures further supports its dominance.

The frame mounted segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand in utility vehicles, off-road applications, and commercial transport systems. Frame mounted structures offer higher durability and load-bearing capacity, making them suitable for heavy-duty operations. Rising infrastructure development and logistics expansion are accelerating adoption in LCV and M&HCV categories. In addition, advancements in modular frame design are improving flexibility and manufacturing efficiency.

• By Manufacturing Method

On the basis of manufacturing method, the market is segmented into cold stamping, hot stamping, roll forming, and others. The cold stamping segment dominated the largest market revenue share in 2025, driven by its cost efficiency and suitability for high-volume production of complex BIW components. It is widely used for producing panels and structural parts with consistent dimensional accuracy. Established manufacturing infrastructure and faster cycle times further support its dominance in mass automotive production. OEMs continue to rely on cold stamping for standardized vehicle platforms.

The hot stamping segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-strength steel components in safety-critical applications. Hot stamping enables production of ultra-high-strength parts with reduced weight and improved crash performance. Its growing application in EVs and advanced passenger safety structures is accelerating adoption. Continuous technological advancements in press hardening processes further enhance efficiency and precision.

• By Component Position

On the basis of component position, the market is segmented into structural, inner, and exposed components. The structural segment dominated the largest market revenue share in 2025, driven by its critical role in ensuring vehicle rigidity, crash safety, and overall load distribution. Structural BIW components form the backbone of vehicle architecture and are extensively used across all vehicle types. High engineering focus on safety standards and durability requirements further strengthens this segment’s dominance. OEM investments in advanced structural design also support sustained demand.

The exposed segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing emphasis on vehicle aesthetics, aerodynamics, and lightweight exterior design. Exposed components are increasingly being optimized for surface quality and material efficiency in modern vehicle styling. Rising adoption of EVs and premium vehicles is further boosting demand for advanced exposed BIW structures. In addition, integration of lightweight materials enhances design flexibility and performance efficiency.

• By Component

On the basis of component, the market is segmented into fenders, closures, shock towers, A-post/B-post, and others. The closures segment dominated the largest market revenue share in 2025, driven by high production volumes of doors, hoods, and tailgates across all vehicle categories. Closures are essential for safety, access, and sealing performance, making them a major contributor to BIW assemblies. Standardization across global platforms further supports large-scale manufacturing efficiency. Continuous improvements in design and material optimization enhance their market presence.

The shock towers segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for improved suspension integration and structural reinforcement in EV and performance vehicles. Shock towers play a critical role in absorbing road impacts and maintaining chassis stability. Rising focus on vehicle safety and driving dynamics is accelerating innovation in this component category. Adoption of advanced materials and precision engineering further supports segment expansion.

• By Material Type

On the basis of material type, the market is segmented into steel, aluminum, magnesium, composites, and CFRP. The steel segment dominated the largest market revenue share in 2025, driven by its high strength, cost efficiency, and widespread availability in automotive manufacturing. Steel remains the primary material for BIW structures due to its excellent crash resistance and ease of forming. Extensive use in mass production vehicles further reinforces its dominance. Continuous improvements in advanced high-strength steel enhance performance and weight balance.

The CFRP segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for ultra-lightweight and high-strength materials in premium and electric vehicles. CFRP offers significant weight reduction benefits, improving vehicle efficiency and battery range. Increasing adoption in performance-oriented and luxury EV platforms is accelerating its market penetration. However, ongoing cost reductions and manufacturing advancements are expected to further support wider adoption.

Body in White Market Regional Analysis

- Asia-Pacific dominated the body in white market with the largest revenue share in 2025, driven by high automotive production volumes and strong presence of leading OEM manufacturing hubs

- The region benefits from large-scale vehicle assembly operations, cost-efficient manufacturing ecosystems, and extensive adoption of advanced Body in White technologies across passenger and commercial vehicles

- Rapid industrialization, increasing vehicle electrification, and rising investments in lightweight automotive structures are accelerating market expansion across the region

China Body in White Market Insight

China held the largest share in the Asia-Pacific Body in White market in 2025, supported by its dominant automotive production base and extensive OEM manufacturing infrastructure. The country has a strong supply chain for steel and aluminum components used in Body in White structures, enabling high-volume and cost-efficient production. Growing demand from passenger vehicles and electric vehicles is further strengthening market growth. In addition, continuous investments in advanced stamping technologies and smart manufacturing facilities are reinforcing China’s leadership in Body in White production.

India Body in White Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by expanding passenger vehicle manufacturing, rising commercial vehicle demand, and increasing EV adoption. Government initiatives supporting domestic automotive production and localization of components are boosting Body in White manufacturing activities. Growing investments from global OEMs and tier-1 suppliers are strengthening production capacity. In addition, increasing focus on lightweight vehicle structures and safety compliance is accelerating long-term market expansion.

Europe Body in White Market Insight

The Europe Body in White market is expanding steadily, supported by strong automotive engineering capabilities and high adoption of advanced vehicle architectures. The region emphasizes lightweight construction, safety standards, and emission reduction targets, driving demand for optimized Body in White structures. Strong presence of luxury and performance vehicle manufacturers further supports market growth. In addition, regulatory focus on sustainability and material efficiency is encouraging innovation in manufacturing processes and material usage.

Germany Body in White Market Insight

Germany accounted for the largest share in the Europe Body in White market in 2025, driven by its strong automotive manufacturing base and advanced engineering capabilities. The country has extensive production of premium and luxury vehicles requiring high-precision Body in White structures. Strong integration of automation and robotics in manufacturing processes enhances efficiency and quality. In addition, continuous R&D in lightweight materials and structural optimization is reinforcing Germany’s leadership in the regional market.

U.K. Body in White Market Insight

The U.K. market is supported by strong demand from premium automotive manufacturing and increasing focus on electric vehicle production. The country’s automotive sector is transitioning toward lightweight and energy-efficient vehicle architectures, driving adoption of advanced Body in White solutions. Strong engineering expertise and research initiatives are supporting material innovation. In addition, increasing investments in EV manufacturing facilities are contributing to steady market expansion.

North America Body in White Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for electric vehicles, pickup trucks, and lightweight automotive structures. Strong adoption of advanced manufacturing technologies and automation is improving production efficiency. Continuous investments in EV platforms and safety-enhanced vehicle designs are further accelerating market growth. In addition, reshoring of automotive manufacturing and expansion of OEM facilities are supporting regional development.

U.S. Body in White Market Insight

The U.S. accounted for the largest share in the North America Body in White market in 2025, supported by strong automotive production and high demand for SUVs, trucks, and electric vehicles. The country benefits from advanced manufacturing infrastructure and strong presence of major OEMs and suppliers. Extensive use of high-strength steel and aluminum in Body in White structures supports lightweighting and safety requirements. In addition, continuous innovation in vehicle platforms and automation technologies is reinforcing the U.S. leadership in the regional market.

Body in White Market Share

The body in white industry is primarily led by well-established companies, including:

- Gestamp Automoción (Spain)

- Tower International (U.S.)

- Martinrea International Inc. (Canada)

- Benteler International (Germany)

- voestalpine Metal Forming GmbH (Austria)

- CIE Automotive (Spain)

- Magna International Inc. (Canada)

- AISIN SEIKI Co., Ltd. (Japan)

- Kirchhoff Automotive (Germany)

- JBM Group (India)

- thyssenkrupp System Engineering GmbH (Germany)

- DURA AUTOMOTIVE SYSTEMS (U.S.)

- AKKA (France)

- Autoneum (Switzerland)

- KWD AUTOMOTIVE AG & CO. KG (Germany)

- BADVE ENGINEERING LTD. (India)

- PANSE Group of Companies (India)

- Norsk Hydro ASA (Norway)

- AIDA ENGINEERING, LTD. (Japan)

Latest Developments in Global Body in White Market

- In March 2026, Magna International launched a new automated Body in White production line at its European facility to support rising demand for electric and lightweight vehicle platforms. The new line integrates AI-enabled robotics, advanced joining systems, and real-time quality monitoring to improve structural precision and manufacturing efficiency. This expansion is designed to support OEMs in accelerating EV production timelines while reducing material waste and improving overall vehicle safety performance. The development strengthens Magna’s position in next-generation Body in White manufacturing and supports the industry’s shift toward highly automated and sustainable production systems

- In June 2025, Benteler Automotive began construction of a new manufacturing facility in Kenitra, Morocco, aimed at strengthening its presence in the North African automotive market. The plant is focused on producing key Body in White components such as bumpers, crash management systems, and suspension parts, which are essential for vehicle structural integrity and safety performance. The investment in advanced high-tonnage cold stamping presses and automated welding systems is expected to enhance production efficiency and quality consistency. This development supports localized manufacturing for OEMs, reduces supply chain dependency, and strengthens regional automotive industrial growth while generating significant employment opportunities

- In December 2024, SSAB entered a long-term strategic partnership with Groupe Financière SNOP Dunois to supply fossil-free steel for Body in White applications, marking a significant shift toward sustainable automotive manufacturing. The agreement focuses on using hydrogen-based steel production instead of conventional fossil fuel-based processes, reducing carbon emissions across structural vehicle components. This initiative aligns with the supplier’s goal of cutting its carbon footprint by 30% by 2030 while meeting increasing demand from European OEMs for green supply chains. The development strengthens the adoption of low-emission materials in BIW production and accelerates sustainability transformation in the automotive industry

- In August 2024, Toyota Motor Corporation announced the installation of a large-scale gigacasting machine at its Aichi Prefecture facility in Japan, designed to revolutionize Body in White manufacturing. The equipment enables production of large aluminum structural sections as single units, replacing multiple stamped parts and significantly simplifying vehicle assembly. This innovation is expected to reduce production complexity, lower costs, and improve structural rigidity for next-generation electric vehicles, including the Lexus LF-ZC. The development reflects a major shift toward integrated manufacturing processes that enhance efficiency and support EV platform optimization

- In April 2024, ArcelorMittal expanded its Multi Part Integration steel solution into the Japanese market through a licensing agreement with G-Tekt Corporation, strengthening advanced Body in White manufacturing capabilities. The collaboration enables the use of partial ablation and laser welding technologies combined with hot stamping to produce large integrated BIW modules. This approach reduces the number of individual components, lowers overall vehicle weight, and decreases assembly costs, particularly for electric vehicles. The development supports improved crash performance, enhanced structural efficiency, and reduced carbon emissions in automotive production

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.