Global Business Jet Market

Market Size in USD Billion

CAGR :

%

USD

74.74 Billion

USD

99.19 Billion

2025

2033

USD

74.74 Billion

USD

99.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 74.74 Billion | |

| USD 99.19 Billion | |

| % | |

|

Business Jet Market Overview

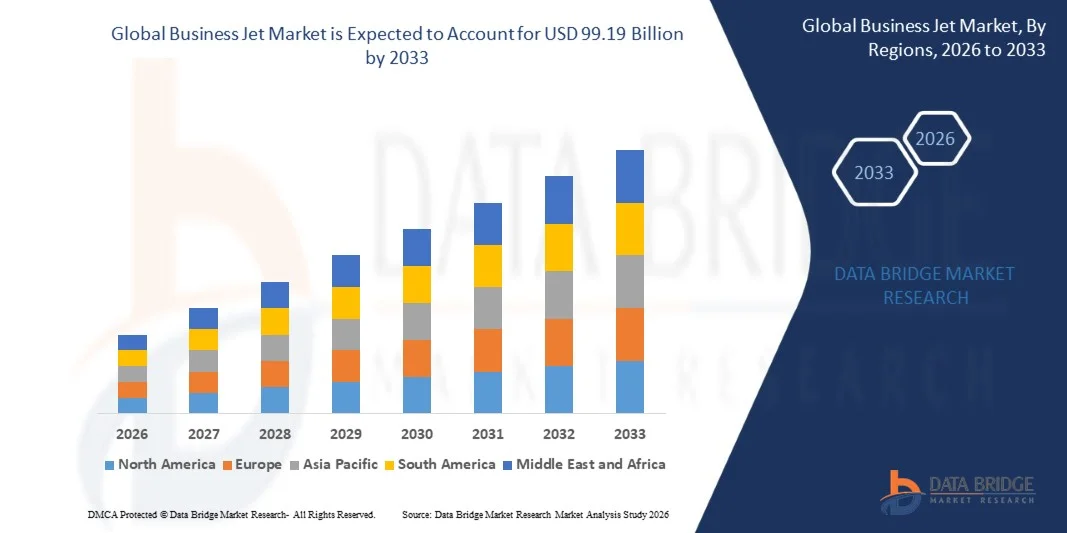

The Business Jet Market was valued at USD 74.74 billion in 2025 and is projected to reach USD 99.19 billion by 2033, growing at a CAGR of 3.60% from 2026 to 2033. The market is witnessing steady expansion driven by rising demand for private air travel, increasing ultra-high-net-worth individual (UHNWI) population, and growing preference for time-efficient and flexible transportation solutions across corporate and personal aviation segments.

The increasing need for reduced travel time, enhanced privacy, and direct connectivity to remote or underserved destinations is significantly boosting business jet adoption among corporate executives, charter operators, and government agencies. In addition, advancements in aircraft range, fuel efficiency, and cabin luxury, along with the integration of next-generation avionics and sustainable aviation fuel (SAF) initiatives, are further supporting market growth across North America, Europe, and emerging Asia-Pacific wealth hubs.

Key Market Trends & Insights

- North America dominated the business jet market with the largest revenue share of approximately 61.3% in 2025, supported by strong corporate aviation demand, extensive airport infrastructure, high aircraft ownership levels, and a well-established business aviation ecosystem.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 5.4% from 2026 to 2033. Growth is driven by rising ultra-high-net-worth population, rapid economic expansion, increasing cross-border business activity, and growing adoption of charter aviation services in countries such as China, India, Singapore, and Indonesia.

- The Mid-Sized segment held the largest market revenue share of approximately 38.6% in 2025 driven by strong demand from corporate travelers seeking balance between range capability, cabin comfort, and operating efficiency. Mid-sized jets are widely used for regional and transcontinental business travel due to their ability to operate efficiently on medium-haul routes while maintaining lower operating costs compared to large jets.

- The Large segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing demand for ultra-long-range intercontinental travel, premium cabin experience, and high-net-worth individual ownership. Growing adoption of aircraft such as Gulfstream and Bombardier Global series for nonstop long-haul routes is further accelerating segment expansion.

- The Private segment held the largest market revenue share of approximately 55.2% in 2025 driven by rising ultra-high-net-worth individuals, corporate executives, and family offices preferring full aircraft ownership for flexibility, privacy, and scheduling efficiency.

- The Operators segment is projected to register the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by expansion of charter services, fractional ownership programs, and jet card models, particularly across North America and Europe, improving aircraft utilization rates and reducing ownership burden.

- The OEM segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong aircraft deliveries, increasing fleet modernization, and rising demand for technologically advanced business jets equipped with next-generation avionics and fuel-efficient engines.

- The Aftermarket segment is projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing demand for maintenance, repair, and overhaul (MRO) services, avionics upgrades, and cabin refurbishment activities across aging business jet fleets globally.

- The 3,000 - 5,000 NM segment held the largest market revenue share of approximately 44.7% in 2025 driven by strong demand for transcontinental business travel routes such as North America to Europe and intra-Asia connectivity.

- The > 5,000 NM segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for ultra-long-haul non-stop connectivity, rising intercontinental business activity, and growing adoption of ultra-long-range business jets for corporate and executive travel.

- The Ownership segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong preference among corporations and ultra-high-net-worth individuals for dedicated aircraft availability, operational control, and privacy.

- The On-demand Service segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing popularity of charter services, shared ownership programs, and subscription-based aviation models offering cost-efficient access to private aviation.

- The Aerostructures segment held the largest market revenue share of approximately 34.1% in 2025 driven by increasing production of lightweight composite airframes and high-performance structural components used in modern business jets.

- The Avionics segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by rising integration of advanced flight management systems, AI-based navigation, real-time connectivity solutions, and enhanced safety monitoring technologies across next-generation business aircraft.

Market Size & Forecast

- Global Market Value (2025): USD 74.74 Billion

- Expected Market Value (2033): USD 99.19 Billion

- Forecast CAGR (2026–2033): 3.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Business Jet Market Segmentation

|

Attributes |

Business Jet Key Market Insights |

|

Segments Covered |

· By Aircraft Type: Light, Mid- Sized, Large, and Airliners · By End Use: Private and Operators · By Point of Sale: OEM and Aftermarket · By Range: < 3,000 NM, 3,000 - 5,000 NM, and > 5000 NM · By BusinessModel: On- demand Service, and Ownership · By System: Avionics, Aerostructures, Cabin Interiors, Aircraft Systems, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Textron Inc. (U.S.) |

|

Market Opportunities |

• Expansion Of Sustainable Aviation Fuel Integration In Business Jets |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Business Jet Market Trends

Trend: Rising Demand For Ultra-Long Range, Sustainable, And Digitally Connected Business Jets

Increasing demand for time-efficient private aviation, enhanced cabin comfort, and flexible travel solutions across corporate, government, and high-net-worth individuals is driving innovation in the Business Jet Market. Traditional commercial aviation constraints such as fixed schedules, longer transit times, and limited connectivity to remote destinations are encouraging the shift toward private and fractional jet ownership.

In modern aviation fleets, manufacturers are integrating next-generation avionics and lightweight composite materials, for instance in aircraft such as Gulfstream G700 and Bombardier Global 7500, to improve range efficiency, reduce fuel consumption, and enhance passenger comfort on intercontinental routes exceeding 13,000 km. Cabin digitalization systems, including high-speed satellite connectivity and AI-enabled in-flight management platforms, are also being widely adopted to support seamless communication and productivity during flights.

The rapid expansion of charter aviation and on-demand air mobility platforms is also increasing demand for flexible business jet utilization models capable of reducing ownership costs while maximizing aircraft utilization rates. In addition, sustainability initiatives across aviation are driving increased adoption of Sustainable Aviation Fuel (SAF), with operators in the U.S. and Europe reporting SAF blending trials reaching up to 30–50% in select business aviation routes in 2025. Growing industry validation through fractional ownership and jet card programs is showing improved aircraft utilization efficiency of nearly 20–25% compared to traditional ownership models under high-demand corporate travel conditions

Business Jet Market Dynamics

Key Market Driver: Rising Demand For Time-Efficient Corporate And Private Air Travel Solutions

Corporations and ultra-high-net-worth individuals are increasingly prioritizing speed, flexibility, and privacy in travel, driving strong demand for business jets across North America, Europe, and Asia-Pacific. Business aviation significantly reduces travel time by enabling direct access to over 5,000 airports globally compared to commercial aviation networks, improving productivity and operational efficiency for executives and high-value industries.

Corporate fleet operators and charter service providers are increasingly expanding aircraft deployment to meet rising cross-border business activity, particularly in financial services, energy, and technology sectors. For instance, major business aviation hubs such as the U.S., U.K., and U.A.E. are witnessing sustained growth in flight hours post-2023 recovery, with North America accounting for more than 60% of global business jet operations in 2025.

Similarly, increasing adoption of fractional ownership models and jet-sharing platforms is enhancing accessibility for mid-tier corporate clients, enabling cost optimization while maintaining premium travel standards. Expansion of airport infrastructure and dedicated FBO (Fixed Base Operator) facilities is further strengthening market penetration in emerging regions.

Key Restraint/Challenge: High Acquisition Costs And Operating Expenses

The business jet market is significantly constrained by high acquisition costs, maintenance expenses, and operational complexities associated with private aircraft ownership and leasing. Aircraft pricing ranges from tens of millions of dollars for light jets to over USD 70–80 million for ultra-long-range jets, limiting adoption to high-net-worth individuals and large corporations.

In addition, rising fuel prices, pilot shortages, and increasing maintenance requirements add substantial operational burdens for operators, reducing overall profitability in charter and fractional ownership segments. Regulatory compliance costs related to aviation safety, emissions standards, and airspace management further increase operational overhead, particularly in Europe and North America where aviation regulations are more stringent.

Furthermore, limited airport infrastructure in developing economies and congestion at major private aviation hubs restrict operational efficiency and aircraft turnaround times, impacting overall market scalability in cost-sensitive regions.

Key Market Opportunity: Expansion Of Sustainable Aviation And Next-Generation Connected Aircraft Systems

The growing focus on sustainability and digital aviation transformation is creating significant opportunities for next-generation business jets equipped with fuel-efficient engines, hybrid-electric propulsion concepts, and advanced avionics systems. Increasing investments in Sustainable Aviation Fuel (SAF) production and distribution infrastructure are enabling operators to reduce carbon emissions while maintaining long-haul operational capabilities.

Manufacturers are increasingly integrating advanced connectivity solutions, predictive maintenance systems, and AI-based flight optimization tools, for instance real-time route optimization technologies that reduce fuel burn by up to 10–15% on long-range business jet missions.

In addition, rising demand in emerging wealth markets across Asia-Pacific, Middle East, and Latin America is expanding opportunities for charter operators and OEMs, supported by growing ultra-high-net-worth populations and increasing cross-border business activity. Development of electric and hybrid business jet prototypes, along with next-generation supersonic business aviation projects, is further expected to redefine long-term market growth trajectories in the global business aviation industry.

Business Jet Market Scope

The market is segmented on the basis of aircraft type, end use, point of sale, range, business model, and system.

- By Aircraft Type

On the basis of aircraft type, the business jet market is segmented into Light, Mid-Sized, Large, and Airliners. The Mid-Sized segment held the largest market revenue share of approximately 38.6% in 2025 driven by strong demand from corporate travelers seeking balance between range capability, cabin comfort, and operating efficiency. Mid-sized jets are widely used for regional and transcontinental business travel due to their ability to operate efficiently on medium-haul routes while maintaining lower operating costs compared to large jets.

The Large segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing demand for ultra-long-range intercontinental travel, premium cabin experience, and high-net-worth individual ownership. Growing adoption of aircraft such as Gulfstream and Bombardier Global series for nonstop long-haul routes is further accelerating segment expansion.

- By End Use

On the basis of end use, the market is segmented into Private and Operators. The Private segment held the largest market revenue share of approximately 55.2% in 2025 driven by rising ultra-high-net-worth individuals, corporate executives, and family offices preferring full aircraft ownership for flexibility, privacy, and scheduling efficiency.

The Operators segment is projected to register the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by expansion of charter services, fractional ownership programs, and jet card models, particularly across North America and Europe, improving aircraft utilization rates and reducing ownership burden.

- By Point of Sale

On the basis of point of sale, the market is segmented into OEM and Aftermarket. The OEM segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong aircraft deliveries, increasing fleet modernization, and rising demand for technologically advanced business jets equipped with next-generation avionics and fuel-efficient engines.

The Aftermarket segment is projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing demand for maintenance, repair, and overhaul (MRO) services, avionics upgrades, and cabin refurbishment activities across aging business jet fleets globally.

- By Range

On the basis of range, the market is segmented into < 3,000 NM, 3,000 - 5,000 NM, and > 5,000 NM. The 3,000 - 5,000 NM segment held the largest market revenue share of approximately 44.7% in 2025 driven by strong demand for transcontinental business travel routes such as North America to Europe and intra-Asia connectivity.

The > 5,000 NM segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for ultra-long-haul non-stop connectivity, rising intercontinental business activity, and growing adoption of ultra-long-range business jets for corporate and executive travel.

- By Business Model

On the basis of business model, the market is segmented into On-demand Service and Ownership. The Ownership segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong preference among corporations and ultra-high-net-worth individuals for dedicated aircraft availability, operational control, and privacy.

The On-demand Service segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing popularity of charter services, shared ownership programs, and subscription-based aviation models offering cost-efficient access to private aviation.

- By System

On the basis of system, the market is segmented into Avionics, Aerostructures, Cabin Interiors, Aircraft Systems, and Others. The Aerostructures segment held the largest market revenue share of approximately 34.1% in 2025 driven by increasing production of lightweight composite airframes and high-performance structural components used in modern business jets.

The Avionics segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by rising integration of advanced flight management systems, AI-based navigation, real-time connectivity solutions, and enhanced safety monitoring technologies across next-generation business aircraft.

Business Jet Market Regional Analysis

North America Business Jet Market Insight

North America dominated the business jet market with the largest revenue share of approximately 61.3% in 2025, supported by strong demand for corporate aviation, high concentration of ultra-high-net-worth individuals, and well-developed airport infrastructure including FBO networks and private aviation terminals. The region benefits from extensive business activity across financial services, technology, and energy sectors, where time-efficient travel solutions are critical. High aircraft ownership rates, strong charter ecosystems, and advanced maintenance and support services further strengthen market leadership in the region.

U.S. Business Jet Market Insight

The U.S. business jet market captured the largest revenue share in North America in 2025, driven by strong corporate travel demand, expanding private aviation networks, and increasing adoption of fractional ownership and jet card programs. The country hosts one of the world’s largest business jet fleets, supported by established OEM presence and major operators such as NetJets and Flexjet. Rising demand for long-range and ultra-long-range jets for domestic and transatlantic travel, along with increasing integration of advanced avionics and cabin connectivity systems, is further accelerating market expansion.

Europe Business Jet Market Insight

The Europe business jet market is expected to witness steady growth from 2026 to 2033, primarily driven by increasing demand for efficient cross-border travel within major business hubs such as the U.K., Germany, France, and Switzerland. Strict commercial airline schedules and growing emphasis on productivity and time optimization are encouraging adoption of private aviation. The region is also witnessing rising demand for charter services and fractional ownership models, particularly among corporate executives and high-net-worth individuals seeking flexible travel solutions.

U.K. Business Jet Market Insight

The U.K. business jet market is expected to witness strong growth from 2026 to 2033, driven by high concentration of financial services firms, increasing demand for private charter services, and rising preference for flexible and secure travel solutions. London remains one of the most active business aviation hubs in Europe, supported by airports such as Farnborough and Luton dedicated to private aviation operations. Growing concerns around travel efficiency and security are further supporting adoption of business jets among corporate users and high-net-worth individuals.

Germany Business Jet Market Insight

The Germany business jet market is expected to witness steady growth from 2026 to 2033, supported by strong industrial and manufacturing base, increasing demand for executive travel, and emphasis on efficient cross-border connectivity within Europe. Germany’s focus on sustainability and advanced aviation technologies is encouraging adoption of newer, fuel-efficient aircraft models. Business aviation is increasingly used by automotive, engineering, and technology companies for rapid access to global markets and production sites.

Asia-Pacific Business Jet Market Insight

The Asia-Pacific business jet market is expected to witness the fastest growth rate from 2026 to 2033, supported by rising ultra-high-net-worth population, rapid economic expansion, and increasing cross-border business activity in countries such as China, India, Singapore, and Indonesia. Growing adoption of charter services and shared ownership models is improving accessibility to private aviation. The region is also benefiting from expanding airport infrastructure and increasing availability of business aviation services, supporting strong market penetration.

Japan Business Jet Market Insight

The Japan business jet market is expected to witness steady growth from 2026 to 2033 due to high technological advancement, strong corporate culture, and demand for efficient domestic and international travel solutions. Limited geographical size combined with high business intensity is encouraging use of business jets for time-sensitive executive travel. Increasing integration of advanced avionics, connectivity systems, and rising interest in charter-based aviation services are further supporting market development.

China Business Jet Market Insight

The China business jet market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid economic growth, expanding high-net-worth population, and increasing demand for premium corporate travel solutions. The development of private aviation infrastructure, including dedicated terminals and expanding FBO services, is strengthening market penetration. Rising adoption of business jets for corporate expansion, government use, and luxury travel, along with growing availability of domestically operated aircraft, is further driving market growth in the country.

Business Jet Market Share

The Business Jet industry is primarily led by well-established companies, including:

• Textron Inc. (U.S.)

• Embraer (Brazil)

• Gulfstream Aerospace Corporation (U.S.)

• Pilatus Aircraft (Switzerland)

• Boeing (U.S.)

• Airbus S.A.S. (France)

• Bombardier (Canada)

• Dassault Aviation (France)

• Honda Aircraft Company (U.S.)

• Volocopter GmbH (Germany)

• Zunum Aero (U.S.)

• Joby Aviation (U.S.)

• Karem Aircraft (U.S.)

• Samad Aerospace Ltd. (U.K.)

• AirCharter International (U.K.)

• VistaJet (Malta)

• Qatar Airways (Qatar)

• NetJets IP, LLC (U.S.)

Latest Developments in Business Jet Market

- In October 2025, Honda Aircraft Company initiated production of its first test unit of the HondaJet 2600 concept, beginning with wing-structure assembly in North Carolina, which is expected to advance next-generation light jet development and strengthen its position in the ultra-efficient business aviation segment, thereby enhancing competition in the long-range light jet market

- In May 2025, Bombardier completed the maiden flight of its first production Global 8000 business jet from Toronto Pearson International Airport, validating key systems under production conditions, which is expected to improve ultra-long-range performance capabilities and reinforce Bombardier’s competitiveness in the premium large-cabin jet segment

- In February 2025, Embraer Executive Jets signed a major purchase agreement with Flexjet for 182 aircraft, including Praetor 500, Praetor 600, and Phenom 300E models, along with an expanded services and support package, which is expected to significantly expand Flexjet’s fleet and strengthen Embraer’s global market share in the fractional ownership and executive jet segment

- In December 2024, Airbus Corporate Jets partnered with AMAC Aerospace in Basel to join the ACJ Services Centre Network, enabling enhanced maintenance, engineering, VIP cabin refurbishment, and upgrade services, which is expected to improve lifecycle support efficiency and strengthen Airbus’s aftermarket service ecosystem in the business aviation market

- In October 2024, Textron Aviation introduced next-generation Cessna Citation light jets including the M2 Gen3, CJ3 Gen3, and CJ4 Gen3, integrating advanced avionics such as Garmin Emergency Autoland, which is expected to improve pilot safety, operational efficiency, and strengthen Textron’s leadership in the light business jet category

- In March 2024, Gulfstream Aerospace Corporation received FAA certification for the G700 and commenced customer deliveries, marking entry into the ultra-long-range category, which is expected to expand high-end aircraft offerings and intensify competition in the long-range business jet market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.