Global C3 Glomerulopathy Market

Market Size in USD Billion

CAGR :

%

USD

341.50 Billion

USD

2,872.59 Billion

2025

2033

USD

341.50 Billion

USD

2,872.59 Billion

2025

2033

| 2026 –2033 | |

| USD 341.50 Billion | |

| USD 2,872.59 Billion | |

| % | |

|

C3 Glomerulopathy Market Size

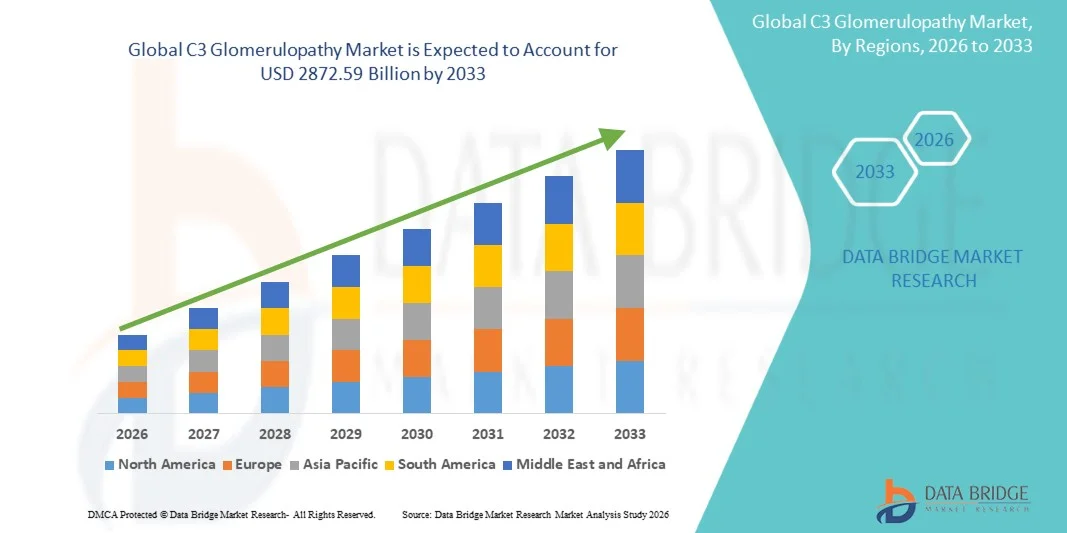

- The global C3 glomerulopathy market size was valued at USD 341.50 billion in 2025and is expected to reach USD 2872.59 billion by 2033, at a CAGR of 30.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of complement-mediated kidney disorders and the rising awareness regarding rare renal diseases, leading to greater demand for advanced targeted therapies and improved diagnostic approaches across healthcare systems

- Furthermore, growing investments in rare disease research, expanding clinical development of complement inhibitors, and rising demand for effective disease-modifying treatments are establishing innovative therapeutics as the preferred approach for managing C3 Glomerulopathy. These converging factors are accelerating the adoption of C3 Glomerulopathy therapies, thereby significantly boosting the market’s growth

C3 Glomerulopathy Market Analysis

- C3 Glomerulopathy is a rare and progressive kidney disorder characterized by abnormal activation of the complement pathway, leading to excessive deposition of complement protein C3 in the glomeruli and resulting in chronic kidney inflammation and impaired renal function

- The rising demand for C3 Glomerulopathy therapies is primarily fueled by increasing awareness of rare kidney diseases, advancements in complement-targeted therapeutics, and growing adoption of precision medicine approaches for nephrology treatment

- North America dominated the C3 glomerulopathy market with the largest revenue share of 41.8% in 2025, characterized by advanced healthcare infrastructure, strong presence of rare disease research programs, and increasing availability of innovative complement inhibitor therapies, with the U.S. experiencing substantial growth in clinical trials and early adoption of targeted biologics for rare renal disorders

- Asia-Pacific is expected to be the fastest growing region in the C3 Glomerulopathy market during the forecast period due to improving healthcare access, increasing awareness regarding rare kidney disorders, and rising investments in nephrology research and specialty care services

- The oral segment held the largest market revenue share of 63.7% in 2025, driven by the convenience and ease of administration associated with oral medications

Report Scope and C3 Glomerulopathy Market Segmentation

|

Attributes |

C3 Glomerulopathy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd. (Switzerland) · Alexion Pharmaceuticals (U.S.) · Apellis Pharmaceuticals (U.S.) · AstraZeneca (U.K.) · Omeros Corporation (U.S.) · ChemoCentryx, Inc. (U.S.) · BioCryst Pharmaceuticals, Inc. (U.S.) · Ionis Pharmaceuticals, Inc. (U.S.) · Regeneron Pharmaceuticals, Inc. (U.S.) · Amgen Inc. (U.S.) · Pfizer Inc. (U.S.) · Sanofi (France) · Bristol Myers Squibb (U.S.) · Takeda Pharmaceutical Company Limited (Japan) · AbbVie Inc. (U.S.) · CSL Limited (Australia) · Travere Therapeutics, Inc. (U.S.) · Aurinia Pharmaceuticals Inc. (Canada) · Visterra, Inc. (U.S.) |

|

Market Opportunities |

· Increasing development of complement-targeted biologics and precision medicines · Rising healthcare investments and improving rare disease diagnostic capabilities in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

C3 Glomerulopathy Market Trends

“Increasing Focus on Complement Pathway-Targeted Therapies and Precision Medicine”

- A major and rapidly evolving trend in the global C3 Glomerulopathy market is the growing emphasis on complement pathway-targeted therapies and precision medicine approaches aimed at addressing the underlying causes of the disease rather than only managing symptoms

- Pharmaceutical and biotechnology companies are increasingly investing in advanced therapies that specifically inhibit components of the complement system, which plays a central role in the progression of C3 Glomerulopathy. Several investigational drugs are being developed to target proteins such as factor B, factor D, and C5, improving disease management outcomes

- For instance, companies such as Novartis, Apellis Pharmaceuticals, and Omeros Corporation are actively advancing complement inhibitor therapies for rare kidney disorders, including C3 Glomerulopathy, through clinical trials and research collaborations

- The growing adoption of precision medicine is also enabling healthcare providers to tailor treatment strategies based on genetic mutations, complement biomarkers, and individual patient profiles. This personalized treatment approach is improving diagnostic accuracy and enhancing therapeutic effectiveness in patients suffering from C3 Glomerulopathy

- Furthermore, advancements in diagnostic technologies such as genetic testing, biomarker identification, and kidney biopsy analysis are supporting early disease detection and better monitoring of treatment responses. These innovations are helping physicians optimize treatment plans and reduce disease progression risks

- This trend toward targeted biologics, personalized therapies, and innovative complement inhibition strategies is transforming the treatment landscape for C3 Glomerulopathy and improving long-term patient outcomes globally

- The demand for advanced therapies and precision-based treatment solutions is increasing significantly across developed and emerging healthcare markets as awareness regarding rare kidney diseases continues to rise

C3 Glomerulopathy Market Dynamics

Driver

“Growing Need Due to Increasing Prevalence of Rare Kidney Disorders and Advancements in Targeted Therapies”

- The increasing prevalence of rare kidney disorders and the rising awareness regarding complement-mediated renal diseases are significant drivers contributing to the growth of the C3 Glomerulopathy market

- For instance, increasing research initiatives and funding support from organizations focused on rare diseases are encouraging the development of novel treatment approaches for C3 Glomerulopathy. In addition, several biotechnology companies are expanding their clinical trial pipelines for complement inhibitor therapies, which is expected to accelerate market growth during the forecast period

- As healthcare providers and researchers gain a deeper understanding of the disease pathology, there is growing demand for innovative therapies capable of slowing disease progression, improving kidney function, and reducing the need for dialysis or kidney transplantation

- Furthermore, advancements in biologics, monoclonal antibodies, and complement pathway inhibitors are significantly improving treatment possibilities for patients with C3 Glomerulopathy. The increasing availability of orphan drug designations and regulatory support for rare disease therapies is also encouraging pharmaceutical companies to invest in this market

- The expansion of specialized nephrology centers, improved access to genetic testing, and increasing adoption of precision medicine approaches are further supporting early diagnosis and effective disease management

- In addition, rising healthcare expenditure, improving awareness among clinicians, and growing patient advocacy initiatives are contributing to increased diagnosis rates and treatment adoption worldwide, thereby driving the overall growth of the C3 Glomerulopathy market

Restraint/Challenge

“High Treatment Costs and Limited Disease Awareness”

- The high cost associated with advanced biologic therapies and complement inhibitor treatments remains a significant challenge restraining the broader growth of the C3 Glomerulopathy market

- Treatments for rare kidney disorders often involve expensive long-term therapies, specialized diagnostic procedures, and continuous monitoring, creating financial burdens for patients and healthcare systems, particularly in low- and middle-income countries

- For instance, complement-targeted therapies and biologic drugs under development for C3 Glomerulopathy may involve substantial treatment costs due to complex manufacturing processes and limited patient populations. These pricing challenges can restrict accessibility for many patients worldwide

- In addition, limited awareness regarding C3 Glomerulopathy among both patients and general healthcare practitioners can lead to delayed diagnosis and underreporting of cases. Since the disease is rare and shares symptoms with other kidney disorders, accurate diagnosis often requires advanced testing and specialist consultation

- The lack of standardized treatment guidelines and limited availability of approved therapies in certain regions also present obstacles to effective disease management. Furthermore, insufficient reimbursement policies for rare disease treatments may discourage patients from pursuing advanced therapeutic options

- Addressing these challenges through increased awareness campaigns, improved reimbursement frameworks, expanded research funding, and the development of cost-effective treatment alternatives will be essential for supporting long-term growth in the global C3 Glomerulopathy market

C3 Glomerulopathy Market Scope

The market is segmented on the basis of treatment, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the C3 Glomerulopathy market is segmented into corticosteroids, ACE inhibitors, immunosuppressive therapy, and others. The corticosteroids segment dominated the largest market revenue share of 41.8% in 2025, driven by its widespread use as a first-line treatment option for controlling inflammation and suppressing immune system activity associated with C3 Glomerulopathy. Healthcare professionals commonly prescribe corticosteroids because they provide rapid therapeutic response in reducing proteinuria and slowing kidney damage progression. Their affordability and widespread availability across hospitals and specialty clinics further support their strong adoption globally. In addition, corticosteroids are frequently used in combination with supportive therapies such as ACE inhibitors, enhancing overall treatment effectiveness. Increasing diagnosis rates of complement-mediated kidney disorders and growing awareness regarding early disease management are also contributing to segment growth. Favorable reimbursement availability for corticosteroid-based therapies in several developed healthcare markets further strengthens demand. Furthermore, physicians continue to rely on corticosteroids due to extensive clinical experience and established treatment guidelines supporting their use in renal inflammatory diseases.

The immunosuppressive therapy segment is anticipated to witness the fastest growth rate with a CAGR of 22.1% from 2026 to 2033, fueled by the increasing focus on targeted treatment approaches and long-term disease management. Immunosuppressive therapies are gaining significant traction among nephrologists due to their ability to regulate abnormal immune responses and reduce complement-mediated kidney injury. Rising clinical research activities for novel biologics and complement inhibitors are accelerating segment expansion globally. These therapies are increasingly prescribed for patients who do not adequately respond to corticosteroid treatment alone. In addition, growing investments in rare kidney disease therapeutics and advancements in precision medicine are supporting broader adoption of immunosuppressive agents. Increasing collaborations between biotechnology companies and research institutions for advanced renal therapies are further driving market growth. The expanding pipeline of innovative immunomodulatory drugs is also expected to create substantial opportunities for this segment during the forecast period.

- By Route of Administration

On the basis of route of administration, the C3 Glomerulopathy market is segmented into oral and parenteral. The oral segment held the largest market revenue share of 63.7% in 2025, driven by the convenience and ease of administration associated with oral medications. Patients undergoing long-term treatment for C3 Glomerulopathy often prefer oral therapies because they can be self-administered without requiring frequent hospital visits. The widespread availability of corticosteroids and ACE inhibitors in tablet and capsule formulations significantly contributes to the segment’s dominance. Oral medications also improve patient compliance and reduce healthcare costs associated with inpatient treatment and injectable administration. Physicians commonly prescribe oral drugs for chronic disease management due to flexible dosing and easier treatment monitoring. Increasing patient awareness regarding early disease treatment and the growing prevalence of chronic kidney disorders are further supporting segment growth. In addition, advancements in oral drug formulations and improved therapeutic efficacy continue to strengthen the adoption of oral therapies globally.

The parenteral segment is expected to witness the fastest CAGR of 21.4% from 2026 to 2033, driven by the increasing use of biologics, monoclonal antibodies, and advanced complement inhibitor therapies administered through injections and infusions. Parenteral administration offers rapid therapeutic action and improved bioavailability, making it suitable for severe and progressive disease conditions. Hospitals and specialty clinics are increasingly utilizing injectable therapies for patients requiring intensive renal care and targeted immune modulation. The growing number of clinical trials evaluating innovative biologic drugs for complement-mediated kidney disorders is also accelerating segment growth. In addition, rising investments in specialty pharmaceuticals and personalized treatment approaches are supporting increased demand for parenteral therapies. The expansion of infusion therapy centers and improved healthcare infrastructure in emerging economies are further expected to contribute to the growth of this segment during the forecast period.

- By End-Users

On the basis of end-users, the C3 Glomerulopathy market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment accounted for the largest market revenue share of 46.5% in 2025, driven by the availability of advanced diagnostic technologies, specialized nephrology departments, and comprehensive patient management services. Hospitals remain the primary treatment centers for rare kidney diseases due to their ability to provide multidisciplinary care and access to experienced healthcare professionals. The increasing number of hospital admissions related to chronic kidney disorders and complement-mediated diseases further supports segment dominance. In addition, hospitals are the leading providers of advanced immunosuppressive therapies and biologic treatments that require continuous monitoring and specialized administration. Government investments in healthcare infrastructure and the expansion of renal care facilities are also positively influencing market growth. Furthermore, hospitals frequently participate in clinical research studies and rare disease treatment programs, strengthening their position within the global C3 Glomerulopathy market. The growing availability of advanced laboratory testing and renal biopsy procedures within hospitals also contributes significantly to segment expansion.

The specialty clinics segment is anticipated to witness the fastest CAGR of 20.8% from 2026 to 2033, fueled by the rising demand for personalized nephrology care and specialized treatment solutions for rare renal diseases. Specialty clinics provide focused expertise in kidney disorders, enabling faster diagnosis and customized treatment planning for patients with C3 Glomerulopathy. Increasing patient preference for outpatient treatment settings and shorter waiting times is contributing to segment growth. These clinics also offer improved accessibility to specialized physicians and advanced disease monitoring services. In addition, the growing establishment of private nephrology clinics and independent renal care centers is accelerating market expansion globally. Technological advancements in diagnostic procedures and increasing awareness regarding early disease detection are further supporting demand for specialty clinic services. The ability of specialty clinics to deliver cost-effective and patient-centric treatment solutions is expected to strengthen their market presence during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the C3 Glomerulopathy market is segmented into hospital pharmacy, retail pharmacy, online pharmacies, and others. The hospital pharmacy segment held the largest market revenue share of 48.1% in 2025, driven by the high volume of prescriptions generated within hospital settings and the increasing use of specialty medications for rare kidney disorders. Hospital pharmacies play a critical role in dispensing immunosuppressive therapies, biologics, and injectable medications that require controlled handling and professional supervision. The presence of trained pharmacists and integrated patient management systems further supports segment dominance. In addition, hospital pharmacies ensure timely availability of advanced therapies for inpatients and critically ill individuals undergoing intensive renal treatment. Rising healthcare expenditure on chronic kidney disease management and increasing hospitalization rates are also contributing to segment growth. Collaborations between pharmaceutical companies and hospital networks for specialty drug distribution further strengthen the position of hospital pharmacies in the market. Furthermore, the availability of reimbursement support and access to high-cost biologic therapies continue to drive demand within this segment.

The online pharmacies segment is expected to witness the fastest CAGR of 23.3% from 2026 to 2033, driven by the rapid adoption of digital healthcare platforms and increasing consumer preference for convenient medicine purchasing options. Online pharmacies offer benefits such as home delivery, discounted pricing, and easy accessibility to long-term medications for chronic disease management. Rising internet penetration and smartphone usage are significantly contributing to the expansion of digital pharmaceutical services worldwide. Patients increasingly prefer online channels for repeat prescription purchases due to convenience and time-saving advantages. In addition, supportive government initiatives promoting telemedicine and e-pharmacy services are accelerating market growth. The expansion of secure digital payment systems and improved logistics infrastructure are also supporting broader adoption of online pharmacy platforms. Growing awareness regarding home-based healthcare solutions and increasing demand for contactless medicine delivery are expected to further drive the growth of this segment during the forecast period.

C3 Glomerulopathy Market Regional Analysis

- North America dominated the C3 Glomerulopathy market with the largest revenue share of 41.8% in 2025, characterized by advanced healthcare infrastructure, a strong presence of rare disease research programs, and increasing availability of innovative complement inhibitor therapies. The region is witnessing substantial growth in clinical trials and early adoption of targeted biologics for rare renal disorders, particularly across specialized nephrology centers and academic institutions

- The growing focus on precision medicine, rising diagnosis rates of rare kidney diseases, and favorable reimbursement frameworks are further supporting market expansion across North America. In addition, increasing collaborations between biotechnology companies and research organizations are accelerating the development of novel therapies for C3 Glomerulopathy

- The widespread presence of specialized healthcare facilities, strong awareness among healthcare professionals, and improved access to advanced diagnostic technologies continue to strengthen the region’s position as a leading market for C3 Glomerulopathy treatment and management

U.S. C3 Glomerulopathy Market Insight

The U.S. C3 glomerulopathy market captured the largest revenue share in 2025 within North America, driven by the increasing prevalence of rare kidney disorders and the strong presence of clinical research initiatives focused on complement-mediated diseases. The country is experiencing rapid adoption of targeted biologic therapies and complement inhibitors, supported by extensive investments in rare disease drug development. Furthermore, favorable regulatory support, rising awareness regarding early diagnosis, and the growing number of specialized nephrology treatment centers are contributing significantly to market growth in the U.S.

Europe C3 Glomerulopathy Market Insight

The Europe C3 glomerulopathy market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness regarding rare renal diseases and the growing availability of advanced therapeutic options. The region benefits from strong healthcare systems, supportive government initiatives for orphan diseases, and rising investments in nephrology research. In addition, the presence of leading pharmaceutical companies and academic collaborations is supporting the development and commercialization of innovative treatment approaches for C3 Glomerulopathy.

U.K. C3 Glomerulopathy Market Insight

The U.K. C3 glomerulopathy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by growing awareness regarding complement-mediated kidney disorders and increasing access to specialized renal care services. The country’s strong clinical research ecosystem, expanding adoption of biologic therapies, and supportive healthcare reimbursement policies are further fueling market growth. In addition, the increasing focus on early disease detection and personalized treatment approaches is expected to accelerate the adoption of advanced therapies across the U.K. market.

Germany C3 Glomerulopathy Market Insight

The Germany C3 glomerulopathy market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and rising investments in rare disease research. Germany’s strong emphasis on medical innovation and precision medicine is encouraging the adoption of targeted therapies for complement-related kidney disorders. Furthermore, increasing collaborations between research institutes, pharmaceutical companies, and nephrology centers are supporting the development of effective treatment solutions and improving patient access to specialized care.

Asia-Pacific C3 Glomerulopathy Market Insight

The Asia-Pacific C3 glomerulopathy market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033 due to improving healthcare access, increasing awareness regarding rare kidney disorders, and rising investments in nephrology research and specialty care services. Rapidly developing healthcare infrastructure across countries such as China, Japan, and India is facilitating better diagnosis and treatment of C3 Glomerulopathy. In addition, government initiatives promoting rare disease management, coupled with increasing healthcare expenditure and growing adoption of advanced biologic therapies, are contributing significantly to regional market growth.

Japan C3 Glomerulopathy Market Insight

The Japan C3 glomerulopathy market is gaining momentum due to the country’s technologically advanced healthcare system, growing focus on rare disease diagnosis, and rising demand for precision medicine. Japan’s strong clinical research capabilities and increasing adoption of innovative biologic therapies are supporting market expansion. Moreover, the country’s aging population and rising incidence of chronic kidney diseases are expected to further increase the demand for effective treatment solutions for C3 Glomerulopathy.

China C3 Glomerulopathy Market Insight

The China C3 glomerulopathy market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, growing awareness regarding rare diseases, and increasing investments in biotechnology research. China is witnessing significant improvements in diagnostic capabilities and access to specialized nephrology care services, supporting the early detection and treatment of C3 Glomerulopathy. In addition, strong government support for healthcare innovation and the increasing presence of domestic and international pharmaceutical companies are accelerating market growth in the country.

C3 Glomerulopathy Market Share

The C3 Glomerulopathy industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd. (Switzerland)

- Alexion Pharmaceuticals (U.S.)

- Apellis Pharmaceuticals (U.S.)

- AstraZeneca (U.K.)

- Omeros Corporation (U.S.)

- ChemoCentryx, Inc. (U.S.)

- BioCryst Pharmaceuticals, Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Amgen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Bristol Myers Squibb (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- AbbVie Inc. (U.S.)

- CSL Limited (Australia)

- Travere Therapeutics, Inc. (U.S.)

- Aurinia Pharmaceuticals Inc. (Canada)

- Visterra, Inc. (U.S.)

Latest Developments in Global C3 Glomerulopathy Market

- In March 2025, Novartis announced that the U.S. Food and Drug Administration (FDA) approved Fabhalta (iptacopan) for the treatment of adults with C3 Glomerulopathy (C3G) to reduce proteinuria, making it the first and only FDA-approved therapy specifically indicated for C3G. The approval was supported by positive Phase III APPEAR-C3G trial results demonstrating sustained reduction in proteinuria and stabilization of kidney function

- In February 2025, Novartis announced that the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency adopted a positive opinion recommending approval of Fabhalta (iptacopan) for adults with C3 Glomerulopathy. The recommendation marked a significant regulatory milestone for the first oral Factor B inhibitor targeting the alternative complement pathway in C3G

- In February 2025, Apellis Pharmaceuticals and Sobi announced that the European Medicines Agency validated the indication extension application for Aspaveli (pegcetacoplan) for the treatment of C3 Glomerulopathy (C3G) and primary immune complex membranoproliferative glomerulonephritis (IC-MPGN). The filing was supported by data from the Phase III VALIANT study evaluating complement C3 inhibition in rare kidney diseases

- In July 2025, Apellis Pharmaceuticals announced that the FDA approved EMPAVELI (pegcetacoplan) for patients aged 12 years and older with C3 Glomerulopathy (C3G) or primary IC-MPGN to reduce proteinuria. The approval was based on Phase III VALIANT trial results showing significant proteinuria reduction, stabilization of kidney function, and substantial clearance of C3 deposits

- In March 2025, the FDA officially confirmed the approval of Fabhalta (iptacopan) as the first treatment for adults with C3 Glomerulopathy, highlighting that the therapy received Priority Review, Breakthrough Therapy, and Orphan Drug designations due to the significant unmet medical need associated with this ultra-rare kidney disease

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.