Global Calcimimetics Market

Market Size in USD Million

CAGR :

%

USD

925.62 Million

USD

1,486.46 Million

2025

2033

USD

925.62 Million

USD

1,486.46 Million

2025

2033

| 2026 –2033 | |

| USD 925.62 Million | |

| USD 1,486.46 Million | |

| % | |

|

Calcimimetics Market Size

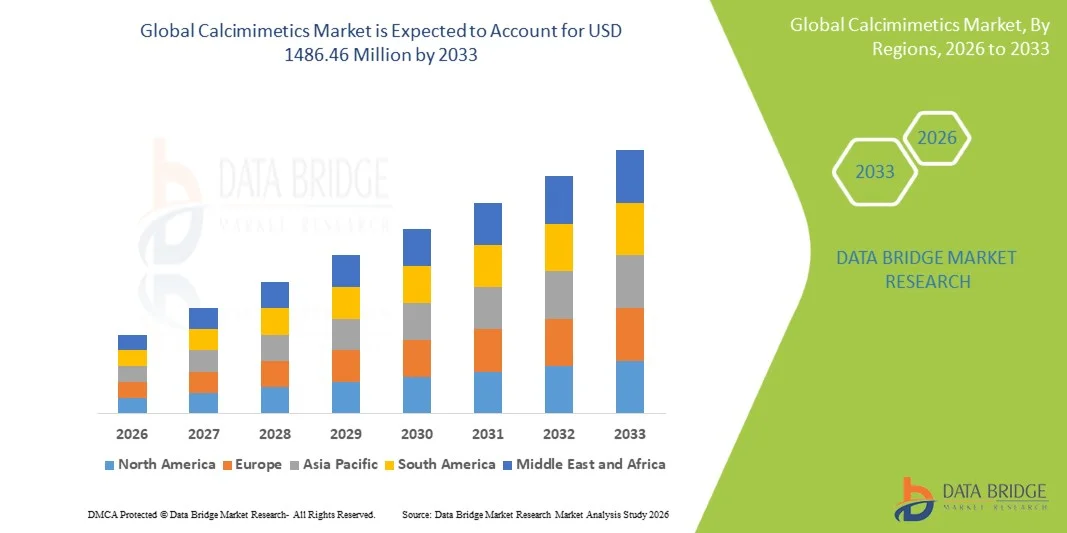

- The global Calcimimetics market size was valued at USD 925.62 Million in 2025 and is expected to reach USD 1486.46 Million by 2033, at a CAGR of 6.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic kidney disease (CKD) and secondary hyperparathyroidism, particularly among patients undergoing dialysis, leading to higher adoption of calcimimetics in both hospital and specialty care settings

- Furthermore, rising demand for effective and targeted therapies to manage calcium and parathyroid hormone levels, along with growing awareness and improved access to advanced renal care treatments, is establishing calcimimetics as a critical therapeutic option. These converging factors are accelerating the uptake of Calcimimetics solutions, thereby significantly boosting the industry's growth

Calcimimetics Market Analysis

- Calcimimetics, a class of drugs used to treat secondary hyperparathyroidism and parathyroid carcinoma by regulating calcium-sensing receptors, are increasingly important in managing mineral imbalance in patients with chronic kidney disease (CKD), particularly those on dialysis. Their clinical effectiveness in controlling parathyroid hormone (PTH) levels makes them a key component in renal care treatment protocols

- The escalating demand for calcimimetics is primarily fueled by the rising prevalence of chronic kidney disease, increasing number of dialysis patients, and growing awareness regarding early management of mineral and bone disorders. In addition, advancements in drug formulations and improved access to nephrology care are further supporting market growth

- North America dominated the calcimimetics market with the largest revenue share of 39.2% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative renal therapies, and strong presence of key pharmaceutical companies. The U.S. continues to witness steady growth due to increasing CKD burden and favorable reimbursement frameworks

- Asia-Pacific is expected to be the fastest growing region in the Calcimimetics market during the forecast period due to rising incidence of kidney disorders, expanding healthcare infrastructure, and increasing healthcare expenditure. Growing awareness and improving access to dialysis and specialty treatments in countries such as China and India are further driving regional growth

- The Hyperparathyroidism segment dominated the market with a revenue share of 67.1% in 2025, driven by the high prevalence of secondary hyperparathyroidism among patients with chronic kidney disease

Report Scope and Calcimimetics Market Segmentation

|

Attributes |

Calcimimetics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Calcimimetics Market Trends

“Increasing Adoption of Calcimimetics for Chronic Kidney Disease-Related Disorders”

- A significant and accelerating trend in the global calcimimetics market is the increasing adoption of these agents for the management of secondary hyperparathyroidism (SHPT) in patients with chronic kidney disease (CKD), particularly those undergoing dialysis

- For instance, drugs such as Cinacalcet and Etelcalcetide are widely used to regulate parathyroid hormone (PTH) levels, helping reduce complications such as bone disorders and cardiovascular risks in CKD patients

- The shift toward more targeted therapies that act on calcium-sensing receptors is improving treatment outcomes compared to traditional vitamin D analogs

- There is a growing preference for intravenous calcimimetics, particularly in dialysis settings, as they improve patient adherence and allow better clinical monitoring

- In addition, increasing awareness among healthcare providers regarding the importance of managing mineral and bone disorders in CKD patients is supporting market growth

- Pharmaceutical companies are focusing on developing improved formulations with enhanced efficacy and reduced side effects

- The expansion of treatment guidelines recommending calcimimetics for SHPT management is further boosting their adoption in clinical practice

- This trend toward targeted, guideline-driven, and patient-compliant therapies is significantly shaping the growth of the calcimimetics market

Calcimimetics Market Dynamics

Driver

“Rising Prevalence of Chronic Kidney Disease and Secondary Hyperparathyroidism”

- The increasing global prevalence of chronic kidney disease (CKD) is a major driver of the calcimimetics market, as CKD often leads to complications such as secondary hyperparathyroidism requiring long-term treatment

- For instance, the growing number of patients undergoing dialysis worldwide has significantly increased the demand for calcimimetic therapies to control elevated parathyroid hormone levels and associated complications

- Aging populations and rising incidence of diabetes and hypertension are contributing to the increasing burden of CKD globally

- Improved diagnostic capabilities and routine monitoring of kidney function are leading to earlier detection and treatment of CKD-related complications

- Increasing healthcare expenditure and expansion of dialysis centers are supporting greater access to calcimimetic treatments

- Growing awareness regarding CKD complications among patients and healthcare providers is encouraging timely therapeutic intervention

- Government initiatives and healthcare programs aimed at improving kidney disease management are further contributing to market growth

- In addition, ongoing research and development efforts to improve treatment efficacy and safety profiles are supporting sustained market expansion

- The rising focus on improving patient outcomes and reducing hospitalization rates is further driving the demand for calcimimetics globally

Restraint/Challenge

“High Treatment Costs and Risk of Adverse Effects”

- One of the major challenges in the calcimimetics market is the high cost associated with these therapies, particularly for long-term treatment in patients with chronic kidney disease

- For instance, medications such as Cinacalcet can be expensive for patients without adequate insurance coverage, limiting access in low- and middle-income regions

- Adverse effects such as hypocalcemia, nausea, and vomiting can impact patient adherence and require careful monitoring during treatment

- The need for regular laboratory monitoring of calcium and parathyroid hormone levels increases the overall treatment burden

- Limited awareness and access to specialized nephrology care in certain regions can delay diagnosis and treatment initiation

- Availability of alternative therapies, such as vitamin D analogs and phosphate binders, may also limit the adoption of calcimimetics in some cases

- Regulatory challenges and pricing pressures can affect the commercialization of newer calcimimetic drugs

- Patient compliance issues, particularly with oral medications, may impact treatment effectiveness over time

- Addressing these challenges through improved affordability, better patient education, and development of safer therapies will be essential for sustained market growth

Calcimimetics Market Scope

The market is segmented on the basis of drugs, indication, route of administration, end-users, and distribution channel.

• By Drugs

On the basis of drugs, the Calcimimetics market is segmented into Cinacalcet, Etelcalcetide, and Others. The Cinacalcet segment dominated the market with the largest revenue share of 62.4% in 2025, driven by its widespread use as an oral calcimimetic agent for managing secondary hyperparathyroidism in patients with chronic kidney disease. Its strong clinical efficacy in reducing parathyroid hormone (PTH) levels supports its extensive adoption. Cinacalcet is widely prescribed due to ease of oral administration and well-established safety profile. The availability of generic versions significantly improves affordability and access across both developed and emerging markets. Hospitals and dialysis centers frequently use cinacalcet as part of routine treatment protocols. Increasing prevalence of chronic kidney disease (CKD) further drives demand. Strong physician familiarity and long-term clinical data reinforce its position. Favorable reimbursement policies in several regions enhance accessibility. Overall, cinacalcet remains the dominant drug segment.

The Etelcalcetide segment is expected to witness the fastest CAGR of 15.8% from 2026 to 2033, driven by increasing adoption of intravenous therapies in dialysis settings. Etelcalcetide offers improved patient compliance as it is administered during hemodialysis sessions, eliminating the need for daily oral dosing. Growing preference for hospital-administered therapies enhances treatment adherence. Its higher efficacy in reducing PTH levels compared to traditional therapies supports rapid adoption. Increasing number of dialysis patients globally contributes to demand growth. Healthcare providers favor etelcalcetide for patients with poor adherence to oral medications. Technological advancements in dialysis care further support its integration. Expanding healthcare infrastructure in emerging markets accelerates uptake. Overall, etelcalcetide is the fastest-growing drug segment.

• By Indication

On the basis of indication, the market is segmented into Hyperparathyroidism, Hypercalcemia, and Others. The Hyperparathyroidism segment dominated the market with a revenue share of 67.1% in 2025, driven by the high prevalence of secondary hyperparathyroidism among patients with chronic kidney disease. Calcimimetics are primarily indicated for managing this condition, making it the largest segment. Increasing incidence of CKD due to diabetes and hypertension significantly contributes to demand. Hospitals and dialysis centers are major users of calcimimetics for managing PTH levels. Early diagnosis and routine monitoring further support treatment adoption. Strong clinical guidelines recommend calcimimetics for hyperparathyroidism management. Growing awareness among healthcare professionals enhances prescription rates. Availability of effective oral and injectable therapies supports market growth. Overall, hyperparathyroidism remains the dominant indication segment.

The Hypercalcemia segment is expected to witness the fastest CAGR of 14.9% from 2026 to 2033, driven by increasing cases of malignancy-associated hypercalcemia and primary hyperparathyroidism. Rising cancer prevalence contributes to higher incidence of hypercalcemia. Calcimimetics are increasingly used to control elevated calcium levels in patients. Growing awareness and improved diagnostic capabilities support early treatment. Hospitals are expanding treatment protocols for managing electrolyte imbalances. Increasing adoption of advanced therapies enhances patient outcomes. Pharmaceutical innovations in drug formulations support growth. Expanding healthcare access in emerging markets further accelerates demand. Overall, hypercalcemia is the fastest-growing indication segment.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Injectable, and Others. The Oral segment dominated the market with a revenue share of 59.3% in 2025, driven by ease of administration and high patient compliance. Oral calcimimetics such as cinacalcet are widely prescribed for long-term management of hyperparathyroidism. Patients prefer oral medications due to convenience and non-invasive nature. Availability of generic oral drugs enhances affordability and accessibility. Hospitals and outpatient settings frequently prescribe oral therapies. Strong distribution through retail pharmacies supports widespread adoption. Pharmaceutical companies continue to improve oral formulations for better efficacy. Increasing prevalence of CKD supports sustained demand. Overall, oral administration remains the dominant segment.

The Injectable segment is expected to witness the fastest CAGR of 16.2% from 2026 to 2033, driven by increasing use of intravenous therapies in dialysis centers. Injectable calcimimetics provide consistent drug delivery and improved bioavailability. Healthcare providers prefer injectable options for patients undergoing regular dialysis. Growing demand for hospital-administered therapies enhances adoption. Technological advancements in drug delivery systems support safety and effectiveness. Rising patient population requiring dialysis further drives growth. Expansion of specialized dialysis centers boosts demand. Overall, injectable administration is the fastest-growing segment.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Centres, and Others. The Hospitals segment dominated the market with a revenue share of 53.6% in 2025, driven by high patient inflow for chronic kidney disease and related complications. Hospitals serve as primary centers for diagnosis and treatment of hyperparathyroidism and hypercalcemia. Availability of dialysis units and skilled healthcare professionals supports effective therapy administration. Hospitals are key users of both oral and injectable calcimimetics. Strong infrastructure and reimbursement systems enhance patient access. Increasing number of CKD patients admitted to hospitals supports demand. Collaboration with pharmaceutical companies enables adoption of advanced therapies. Overall, hospitals remain the dominant end-user segment.

The Homecare segment is expected to witness the fastest CAGR of 15.5% from 2026 to 2033, driven by increasing preference for managing chronic conditions outside hospital settings. Patients prefer oral therapies that can be self-administered at home. Growing awareness about chronic disease management supports homecare adoption. Telehealth and remote monitoring improve treatment adherence. Cost-effectiveness compared to hospital visits encourages patients to opt for homecare. Rising elderly population further supports demand. Healthcare systems promote home-based care to reduce hospital burden. Overall, homecare is the fastest-growing end-user segment.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Hospital Pharmacy segment dominated the market with a revenue share of 48.9% in 2025, driven by high prescription volumes in hospitals and dialysis centers. Hospital pharmacies ensure immediate availability of calcimimetic drugs for inpatient and outpatient care. Strong integration with hospital treatment protocols supports efficient drug dispensing. Bulk procurement systems improve cost efficiency. Physicians prefer hospital pharmacies for controlled and monitored distribution. Increasing hospitalization rates for CKD patients support demand. Hospital pharmacies also handle specialized storage requirements. Overall, hospital pharmacy remains the dominant distribution channel.

The Online Pharmacy segment is expected to witness the fastest CAGR of 17.2% from 2026 to 2033, driven by rising digitalization of healthcare and increasing patient preference for convenient drug purchasing. Online platforms offer home delivery and competitive pricing. Growing internet penetration supports rapid adoption. Integration with telemedicine enhances prescription access. Patients with chronic conditions prefer recurring online purchases. Expanding logistics infrastructure ensures timely delivery. Regulatory support for e-pharmacies boosts market confidence. Overall, online pharmacy is the fastest-growing distribution channel segment.

Calcimimetics Market Regional Analysis

- North America dominated the calcimimetics market with the largest revenue share of 39.2% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative renal therapies, and strong presence of key pharmaceutical companies

- The region benefits from widespread use of calcimimetic agents for managing secondary hyperparathyroidism in chronic kidney disease patients. For instance, therapies such as Cinacalcet and Etelcalcetide are extensively prescribed across the United States and Canada, improving disease management outcomes

- This dominance is further supported by increasing CKD burden, favorable reimbursement frameworks, high healthcare expenditure, and strong clinical awareness, establishing calcimimetics as a key component in renal care management

U.S. Calcimimetics Market Insight

The U.S. calcimimetics market captured the largest revenue share of 81% in 2025 within North America, driven by increasing prevalence of chronic kidney disease and strong adoption of advanced treatment options. Healthcare providers are increasingly focusing on managing complications such as secondary hyperparathyroidism in dialysis patients, leading to sustained demand for calcimimetic therapies. In addition, favorable reimbursement policies and widespread availability of both oral and intravenous formulations are supporting treatment adoption. Moreover, the presence of leading pharmaceutical companies, continuous clinical research, and well-established dialysis infrastructure are significantly contributing to the growth of the calcimimetics market in the United States.

Europe Calcimimetics Market Insight

The Europe calcimimetics market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of chronic kidney disease and strong public healthcare systems. The region is witnessing rising adoption of cost-effective treatment approaches. For instance, countries such as Germany and France are promoting the use of calcimimetic therapies alongside dialysis treatment to improve patient outcomes. In addition, supportive reimbursement frameworks, growing awareness among healthcare professionals, and expanding access to nephrology care are contributing to steady market growth across Europe.

U.K. Calcimimetics Market Insight

The U.K. calcimimetics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing burden of kidney disorders and rising demand for effective long-term treatment solutions. Public healthcare initiatives and structured renal care programs are encouraging early diagnosis and management of CKD-related complications. Furthermore, improved access to medications through national healthcare systems is supporting market expansion. The growing focus on improving patient outcomes and reducing hospitalization rates is further contributing to the growth of the calcimimetics market in the U.K.

Germany Calcimimetics Market Insight

The Germany calcimimetics market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong emphasis on renal disease management. Germany is witnessing increased adoption of both oral and intravenous calcimimetic therapies. For instance, the use of Cinacalcet in CKD patients undergoing dialysis is improving disease control and treatment outcomes. In addition, strong regulatory frameworks, increasing healthcare expenditure, and growing awareness of kidney-related complications are supporting market growth in the country.

Asia-Pacific Calcimimetics Market Insight

The Asia-Pacific calcimimetics market is expected to be the fastest growing region during the forecast period due to rising incidence of kidney disorders, expanding healthcare infrastructure, and increasing healthcare expenditure. The region is witnessing a growing patient population requiring renal care. For instance, countries such as China and India are expanding access to dialysis centers and specialty treatments, increasing the adoption of calcimimetic therapies. Furthermore, improving healthcare access, rising awareness, and growing investments in pharmaceutical manufacturing are significantly contributing to regional market growth.

Japan Calcimimetics Market Insight

The Japan calcimimetics market is gaining momentum due to increasing prevalence of chronic kidney disease and a rapidly aging population. The country is characterized by high adoption of advanced renal therapies. For instance, intravenous calcimimetic treatments are increasingly used in dialysis settings to improve patient adherence and clinical outcomes. In addition, strong healthcare infrastructure and emphasis on improving quality of life are driving demand for calcimimetics in Japan.

China Calcimimetics Market Insight

The China calcimimetics market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to its large patient population, increasing healthcare investments, and expanding access to renal care services. The country is witnessing significant growth in the treatment of CKD-related complications. For instance, increased availability of affordable calcimimetic drugs is improving treatment accessibility across both urban and rural areas. Government initiatives, improving healthcare infrastructure, and growing focus on chronic disease management are further propelling the growth of the calcimimetics market in China.

Calcimimetics Market Share

The Calcimimetics industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- KAI Pharmaceuticals (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

- Takeda Pharmaceutical Company (Japan)

- Novartis AG (Switzerland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Dr. Reddy’s Laboratories (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Cipla Ltd. (India)

- Aurobindo Pharma Ltd. (India)

- Zydus Lifesciences Ltd. (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Viatris Inc. (U.S.)

- Apotex Inc. (Canada)

- Sandoz International GmbH (Switzerland)

- Intas Pharmaceuticals Ltd. (India)

Latest Developments in Global Calcimimetics Market

- In February 2021, the U.S. Food and Drug Administration (FDA) approved Parsabiv (etelcalcetide) label updates by Amgen Inc., reinforcing its use for the treatment of secondary hyperparathyroidism in adult patients with chronic kidney disease (CKD) on hemodialysis and providing updated clinical safety and efficacy information

- In August 2021, Amneal Pharmaceuticals, Inc. received FDA approval for its generic version of cinacalcet tablets, expanding access to calcimimetic therapy for patients with secondary hyperparathyroidism and parathyroid carcinoma

- In March 2022, the European Medicines Agency (EMA) endorsed continued clinical use and safety monitoring updates for cinacalcet-based therapies, supporting their role in managing calcium and parathyroid hormone levels in CKD patients across Europe

- In September 2022, Zydus Lifesciences Ltd. received approval from the U.S. FDA to market Cinacalcet Tablets (generic Sensipar) in multiple strengths, strengthening competition and affordability in the global calcimimetics market

- In July 2023, Cipla Limited launched generic cinacalcet tablets in select international markets, improving patient access to cost-effective calcimimetic treatment options for hyperparathyroidism

- In April 2024, clinical studies published in nephrology journals highlighted the expanded use of calcimimetics such as etelcalcetide and cinacalcet in improving biochemical control of secondary hyperparathyroidism, supporting their continued integration into CKD treatment protocols

- In May 2025, ongoing clinical research and treatment guidelines continued to recommend calcimimetic therapies as a key component in managing mineral and bone disorders in CKD patients, reinforcing their sustained clinical importance and global demand

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.