Global Can Coatings Market

Market Size in USD Billion

CAGR :

%

USD

3.26 Billion

USD

4.51 Billion

2025

2033

USD

3.26 Billion

USD

4.51 Billion

2025

2033

| 2026 –2033 | |

| USD 3.26 Billion | |

| USD 4.51 Billion | |

| % | |

|

Can Coatings Market Size

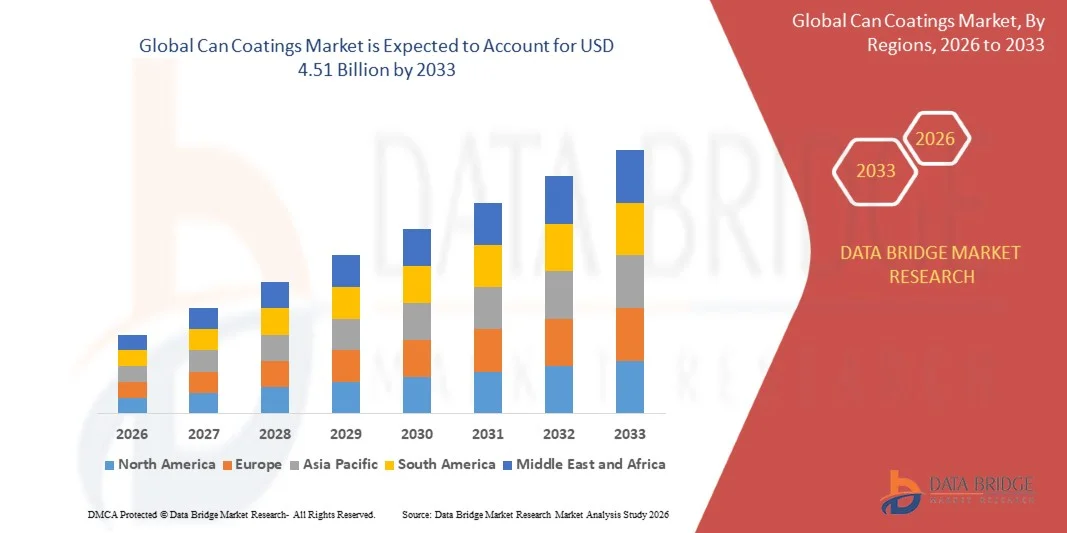

- The global can coatings market size was valued at USD 3.26 billion in 2025 and is expected to reach USD 4.51 billion by 2033, at a CAGR of 4.15% during the forecast period

- The market growth is largely fuelled by the rising demand for packaged and processed food and beverages, increasing awareness of food safety and hygiene, and the need for protective coatings that extend shelf life

- Growing adoption of eco-friendly and sustainable coatings, coupled with technological advancements in coating formulations, is supporting market expansion

Can Coatings Market Analysis

- The global can coatings market is witnessing steady growth, driven by the increasing consumption of ready-to-eat and packaged products, which require high-quality protective coatings to maintain product integrity

- Manufacturers are focusing on innovation and sustainable solutions, including BPA-free and low-VOC coatings, to meet regulatory requirements and changing consumer preferences, while also enhancing durability and corrosion resistance

- North America dominated the can coatings market with the largest revenue share of 38.5% in 2025, driven by the growing demand for packaged food and beverages, as well as stringent regulations on food safety and packaging standards

- Asia-Pacific region is expected to witness the highest growth rate in the global can coatings market, driven by expanding urban populations, increasing disposable incomes, growth of the packaged food and beverage industry, and rising awareness of sustainable and high-performance coating solutions

- The Epoxy segment held the largest market revenue share in 2025, driven by its excellent corrosion resistance, chemical stability, and suitability for both food and beverage packaging. Epoxy coatings are widely adopted due to their ability to extend shelf life and protect the integrity of the contents, making them a preferred choice among manufacturers. The segment is also supported by regulatory approvals for food contact safety, making epoxy-based coatings a reliable solution for global can producers

Report Scope and Can Coatings Market Segmentation

|

Attributes |

Can Coatings Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Akzo Nobel N.V. (Netherlands) |

|

Market Opportunities |

• Rising Demand For Eco-Friendly And BPA-Free Can Coatings |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Can Coatings Market Trends

“Rising Demand For Protective And Sustainable Coatings”

• Growing consumer preference for packaged and processed food and beverages is significantly shaping the global can coatings market, as manufacturers increasingly seek coatings that enhance product shelf life, safety, and quality. Protective coatings are gaining traction due to their ability to prevent corrosion, contamination, and chemical interaction between the container and contents, strengthening adoption across beverage, food, and industrial applications

• Increasing awareness around food safety, hygiene, and environmental sustainability has accelerated the demand for eco-friendly can coatings, including BPA-free and low-VOC formulations. Manufacturers are actively prioritizing sustainable sourcing and production processes, prompting collaborations between coating suppliers and can manufacturers to improve performance and comply with regulations

• Sustainability and regulatory compliance trends are influencing procurement and manufacturing decisions, with companies emphasizing transparent supply chains, certifications, and eco-friendly production methods. These factors are helping brands differentiate products in a competitive market while reinforcing consumer trust

• For instance, in 2024, Sherwin-Williams in the U.S. and AkzoNobel in the Netherlands launched new BPA-free and low-VOC can coatings for beverage and food cans. These initiatives were introduced to meet rising consumer preference for safe and sustainable packaging, with distribution across retail, industrial, and export channels. The products were also promoted as environmentally responsible choices, enhancing brand credibility and market penetration

• While demand for advanced and eco-friendly can coatings is increasing, sustained market growth depends on continuous R&D, cost-effective production, and maintaining functional performance. Manufacturers are also focusing on improving scalability, regulatory compliance, and innovative formulations that balance safety, sustainability, and durability for broader adoption

Can Coatings Market Dynamics

Driver

“Rising Adoption Of Eco-Friendly And Protective Can Coatings”

• Growing demand for safe, sustainable, and high-performance can coatings is a key driver for the global market. Manufacturers are replacing conventional coatings with BPA-free and low-VOC alternatives to meet regulatory requirements, enhance product appeal, and comply with environmental standards. This trend also encourages research into novel coating formulations to improve corrosion resistance and chemical stability

• Expanding applications in beverage, food, and industrial packaging are further influencing market growth. Can coatings help protect contents, maintain quality, and extend shelf life, enabling manufacturers to meet consumer expectations for safe and high-quality packaged products

• Coating manufacturers and food & beverage companies are actively promoting advanced can coating solutions through innovation, marketing, and certifications. These efforts are supported by the growing global emphasis on sustainability, safety, and regulatory compliance, and they also encourage partnerships to improve performance and reduce environmental impact

• For instance, in 2023, PPG Industries in the U.S. and Jotun in Norway reported increased adoption of eco-friendly can coatings in food and beverage packaging. This expansion followed rising demand for BPA-free, low-VOC, and recyclable packaging solutions, driving repeat orders and product differentiation. Both companies also highlighted sustainability and certification compliance in marketing campaigns to build trust and strengthen brand loyalty

• Although eco-friendly and protective coatings support growth, wider adoption depends on cost optimization, raw material availability, and scalable production processes. Investment in R&D, supply chain efficiency, and advanced coating technologies will be critical for meeting global demand and maintaining a competitive advantage

Restraint/Challenge

“High Cost And Stringent Regulatory Compliance”

• The higher cost of eco-friendly and protective can coatings compared to conventional alternatives remains a key challenge, limiting adoption among price-sensitive manufacturers. Elevated raw material costs and complex production processes contribute to higher pricing, which can affect market penetration in cost-driven regions

• Regulatory requirements and compliance standards for food-contact coatings add complexity, particularly in emerging markets. Manufacturers must adhere to stringent safety, environmental, and quality standards, which can increase operational costs and slow market adoption

• Supply chain and logistical challenges also impact market growth, as high-quality coatings require certified raw materials, proper handling, and specialized storage. Any disruption in supply or inconsistency in product quality can affect production schedules and market availability

• For instance, in 2024, distributors in Southeast Asia supplying beverage and food can manufacturers reported slower uptake due to higher prices of BPA-free coatings and complex regulatory requirements. This limited adoption in cost-sensitive markets, prompting some manufacturers to delay switching from conventional coatings

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and collaboration with regulatory bodies. Developing competitively priced, safe, and sustainable coating formulations, while ensuring compliance and promoting functional benefits, will be essential for long-term market growth

Can Coatings Market Scope

The can coatings market is segmented on the basis of type and application.

• By Type

On the basis of type, the can coatings market is segmented into Epoxy, Acrylic, Polyester, Oleoresins, Vinyl, Alkyd, and Polyolefin. The Epoxy segment held the largest market revenue share in 2025, driven by its excellent corrosion resistance, chemical stability, and suitability for both food and beverage packaging. Epoxy coatings are widely adopted due to their ability to extend shelf life and protect the integrity of the contents, making them a preferred choice among manufacturers. The segment is also supported by regulatory approvals for food contact safety, making epoxy-based coatings a reliable solution for global can producers.

The Acrylic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior flexibility, clarity, and ease of application. Acrylic-based can coatings are particularly popular for decorative and protective purposes, offering compatibility with sustainable and BPA-free formulations, which are increasingly demanded by environmentally conscious consumers. The lightweight and cost-effective nature of acrylic coatings, combined with strong adhesion and resistance to wear, is encouraging adoption across beverage, aerosol, and general line cans.

• By Application

On the basis of application, the can coatings market is segmented into Food Cans, Beverage Cans, General Line Cans, and Aerosol Cans. The Beverage Cans segment held the largest market share in 2025, attributed to the rapid growth of the soft drinks and energy drinks industries, which require durable and safe coatings to preserve product quality. Beverage can coatings ensure resistance to corrosion, maintain taste integrity, and provide compatibility with printing and labeling, which enhances brand appeal.

The Food Cans segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing demand for packaged foods and the rising adoption of eco-friendly, BPA-free coatings. Food can coatings provide essential protection against contamination, corrosion, and metal interaction, ensuring food safety and compliance with regulatory standards. The growth is further supported by the rising trend of ready-to-eat meals, canned fruits, and vegetables, which are driving higher coating demand globally.

Can Coatings Market Regional Analysis

• North America dominated the can coatings market with the largest revenue share of 38.5% in 2025, driven by the growing demand for packaged food and beverages, as well as stringent regulations on food safety and packaging standards

• Manufacturers in the region are increasingly prioritizing high-performance coatings that ensure product safety, corrosion resistance, and extended shelf life, which is boosting the adoption of advanced can coatings

• This widespread adoption is further supported by high production capacities, advanced manufacturing infrastructure, and a strong preference for sustainable and eco-friendly packaging solutions, establishing can coatings as a critical component for the packaging industry

U.S. Can Coatings Market Insight

The U.S. can coatings market captured the largest revenue share in 2025 within North America, fueled by the rising demand for canned food and beverage products and strict regulatory requirements for packaging safety. The market is benefiting from the adoption of advanced epoxy, acrylic, and polyester coatings that enhance durability, chemical resistance, and shelf life. In addition, growing investments in sustainable and recyclable packaging materials are further propelling the market’s expansion. Manufacturers are also focusing on innovations to meet consumer preferences for safe, high-quality, and environmentally responsible packaging.

Europe Can Coatings Market Insight

The Europe can coatings market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent EU regulations on food contact materials and environmental compliance. Increasing awareness about sustainable packaging and rising demand for high-performance coatings across the food and beverage sector are supporting market adoption. Countries such as Germany, France, and the U.K. are witnessing strong growth due to increased urbanization, packaging innovations, and a preference for eco-friendly solutions.

U.K. Can Coatings Market Insight

The U.K. can coatings market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for safe and sustainable packaging in both food and beverage sectors. Manufacturers are focusing on innovative coating technologies that improve shelf life, corrosion resistance, and chemical protection. The growing e-commerce sector and retail demand for premium canned products are also contributing to market expansion. In addition, the adoption of environmentally friendly and recyclable coatings aligns with regulatory initiatives and consumer preferences.

Germany Can Coatings Market Insight

The Germany can coatings market is expected to witness the fastest growth rate from 2026 to 2033, fueled by advanced manufacturing infrastructure, technological innovation, and strict adherence to EU food safety standards. The increasing production of canned food and beverages, combined with sustainability initiatives, is driving the adoption of high-performance coatings. The integration of eco-friendly solutions, such as water-based and low-VOC coatings, is also gaining traction, reflecting Germany’s focus on environmental responsibility and regulatory compliance.

Asia-Pacific Can Coatings Market Insight

The Asia-Pacific can coatings market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and a booming packaged food and beverage industry in countries such as China, India, and Japan. The region is also experiencing growing investments in modern coating technologies and eco-friendly solutions to meet international quality standards. Furthermore, as APAC emerges as a manufacturing hub for coated cans, affordability and accessibility of high-quality can coatings are improving across the region.

Japan Can Coatings Market Insight

The Japan can coatings market is expected to witness the fastest growth rate from 2026 to 2033 due to increasing demand for safe, high-quality packaging and premium canned products. The adoption of advanced coating technologies that enhance corrosion resistance, shelf life, and chemical protection is driving market expansion. In addition, the country’s focus on sustainability and compliance with environmental regulations is encouraging manufacturers to develop eco-friendly coating solutions.

China Can Coatings Market Insight

The China can coatings market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrialization, a growing middle class, and high consumption of canned food and beverages. The push toward smart manufacturing and eco-friendly, high-performance coatings is significantly supporting market growth. Strong domestic production capabilities and investment in coating innovations are further driving adoption, making China one of the most important markets for can coatings in the region.

Can Coatings Market Share

The Can Coatings industry is primarily led by well-established companies, including:

• Akzo Nobel N.V. (Netherlands)

• PPG Industries, Inc. (U.S.)

• The Sherwin-Williams Company (U.S.)

• RPM International Inc. (U.S.)

• Axalta Coating Systems (U.S.)

• AZTRON TECHNOLOGIES, LLC (U.S.)

• BALL CORPORATION (U.S.)

• A.W. Chesterton Company (U.S.)

• KC Jones Plating Company (U.S.)

• OM Sangyo Co., Ltd. (Japan)

• Poeton (U.S.)

• Endura Coatings (U.K.)

• Twin City Plating (U.S.)

• Nickel Composite Coatings, Inc. (U.S.)

• SURTECKARIYA Co., Ltd. (Japan)

• Sharretts Plating Company (U.S.)

• Integer Holdings Corporation (U.S.)

• Interplate LTD (U.K.)

• Composite Coatings, Inc. (U.S.)

• Hunger International GmbH (Germany)

Latest Developments in Global Can Coatings Market

- In September 2025, AkzoNobel (Netherlands) entered a strategic partnership with a leading beverage manufacturer to develop customized can coatings that extend product shelf life and reduce environmental impact. The collaboration leverages advanced coating technologies to enhance durability, improve resistance to corrosion, and minimize chemical emissions. This initiative strengthens AkzoNobel’s innovation portfolio, reinforces its sustainability commitments, and positions the company competitively in the global can coatings market, particularly in regions with stringent environmental regulations

- In August 2025, PPG Industries (U.S.) launched a new line of water-based can coatings focused on reducing volatile organic compounds (VOCs). The coatings are designed to meet sustainability standards, enhance food safety, and improve shelf life of packaged products. By introducing eco-friendly solutions, PPG aims to capture environmentally conscious customers, comply with global regulations, and increase its market share across North America, Europe, and Asia-Pacific

- In July 2025, BASF (Germany) expanded its production capacity for can coatings in Asia to meet growing demand in the region. The expansion allows faster supply to beverage and food manufacturers, improves operational efficiency, and supports the company’s regional growth strategy. This move positions BASF to capture emerging market opportunities, strengthen relationships with local clients, and address increasing consumer preference for sustainable and high-performance coatings

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Can Coatings Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Can Coatings Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Can Coatings Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.