Global Cancer Treatment Market

Market Size in USD Billion

CAGR :

%

USD

340.93 Billion

USD

850.17 Billion

2025

2033

USD

340.93 Billion

USD

850.17 Billion

2025

2033

| 2026 –2033 | |

| USD 340.93 Billion | |

| USD 850.17 Billion | |

| % | |

|

Cancer Treatment Market Size

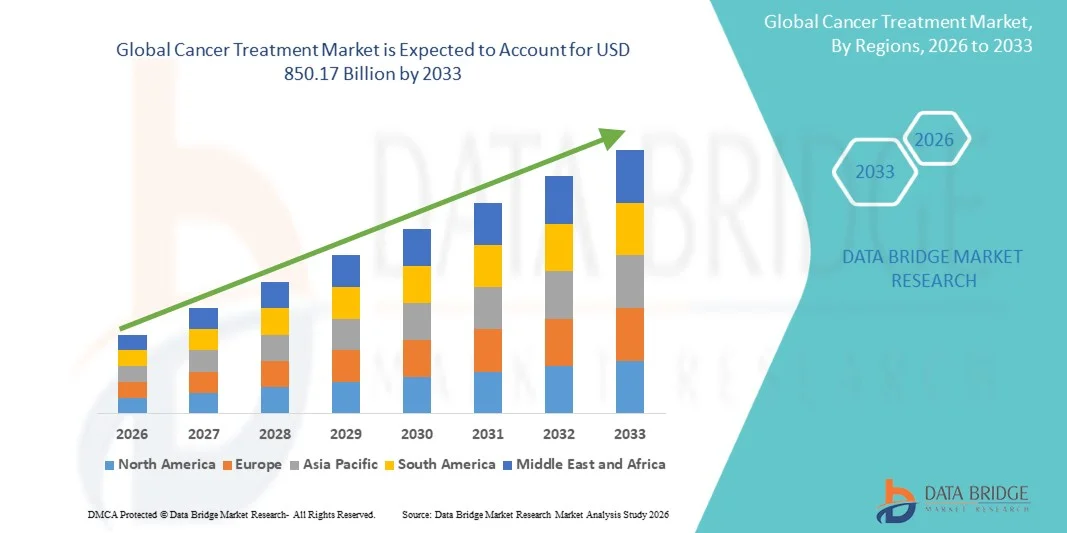

- The global cancer treatment market size was valued at USD 340.93 billion in 2025 and is expected to reach USD 850.17 billion by 2033, at a CAGR of 12.10% during the forecast period

- The market growth is largely fueled by the rising global cancer burden, increasing prevalence of lifestyle-related risk factors, and continuous advancements in oncology therapies such as immunotherapy, targeted therapy, and precision medicine, leading to improved treatment outcomes

- Furthermore, growing investments in oncology research and development, expanding adoption of personalized treatment approaches, and increasing availability of innovative biologics and combination therapies are strengthening clinical adoption across healthcare systems

Cancer Treatment Market Analysis

- Cancer treatment, encompassing a wide range of modalities such as chemotherapy, immunotherapy, targeted therapy, radiation therapy, and surgical oncology, is becoming increasingly critical in modern healthcare systems due to the rising global cancer burden and the growing shift toward precision medicine and personalized treatment approaches aimed at improving patient survival rates and minimizing adverse effects

- The escalating demand for cancer treatment is primarily driven by the increasing incidence of cancer worldwide, aging populations, genetic and lifestyle-related risk factors, and rapid advancements in innovative treatment options such as targeted therapies, immunotherapies, and next-generation biologics

- North America dominated the cancer treatment market with the largest revenue share of 40.8% in 2025, supported by advanced healthcare infrastructure, strong oncology research funding, early adoption of innovative therapies, and the presence of leading pharmaceutical and biotechnology companies, with the U.S. witnessing significant uptake of precision oncology and advanced immuno-oncology drugs

- Asia-Pacific is expected to be the fastest growing region in the cancer treatment market during the forecast period due to rising healthcare investments, improving access to oncology care, increasing cancer awareness and screening initiatives, and a rapidly expanding patient pool across emerging economies

- Targeted therapy segment dominated the cancer treatment market in 2025 in terms of revenue share of 38.6%, driven by its high efficacy in attacking specific cancer cells while minimizing damage to healthy tissues, increasing adoption of biomarker-driven treatment approaches

Report Scope and Cancer Treatment Market Segmentation

|

Attributes |

Cancer Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cancer Treatment Market Trends

“Rise of Precision Oncology and Immunotherapy Adoption”

- A significant and accelerating trend in the global cancer treatment market is the increasing shift toward precision oncology and immunotherapy-based treatments, which are transforming traditional cancer care by targeting tumor biology more effectively and improving patient outcomes across multiple cancer types

- For instance, therapies such as checkpoint inhibitors including pembrolizumab and nivolumab are widely used across lung, melanoma, and bladder cancers, demonstrating strong clinical success and expanding treatment indications globally

- Advances in biomarker-driven diagnostics and genetic profiling are enabling clinicians to tailor treatments based on individual tumor characteristics, improving response rates and reducing unnecessary toxicity in patients

- The integration of next-generation sequencing (NGS) and companion diagnostics with oncology drugs is facilitating more accurate treatment selection and supporting the development of highly targeted cancer therapies across healthcare systems

- This trend towards more personalized, immune-based, and data-driven treatment approaches is fundamentally reshaping oncology practice, leading companies such as Roche and Merck to expand their immunotherapy pipelines and combination therapy strategies

- The increasing use of AI and digital pathology tools in oncology decision-making is enhancing diagnostic accuracy and supporting faster, more efficient treatment planning in clinical workflows

- The demand for precision oncology and immunotherapy is growing rapidly across both developed and emerging markets, as healthcare providers increasingly prioritize effective, long-term cancer control and improved survival outcomes

Cancer Treatment Market Dynamics

Driver

“Rising Global Cancer Prevalence and Expanding Treatment Innovation”

- The increasing global burden of cancer, coupled with continuous advancements in oncology drug development, is a significant driver for the heightened demand for cancer treatment across hospitals, specialty clinics, and research centers worldwide

- For instance, in March 2025, Pfizer Inc. announced continued expansion of its oncology portfolio with next-generation targeted therapy candidates aimed at improving outcomes in breast and lung cancer patients, strengthening its oncology pipeline

- As cancer incidence rises due to aging populations, environmental exposure, and lifestyle-related risk factors, demand for effective and long-term treatment options such as immunotherapy, targeted therapy, and combination regimens is increasing rapidly

- Furthermore, growing healthcare investments and supportive regulatory approvals for innovative oncology drugs are accelerating the availability of advanced treatment options across both developed and emerging healthcare systems

- The increasing use of combination therapies and personalized medicine approaches is improving treatment efficacy and survival rates, further driving adoption of advanced cancer treatment modalities in clinical practice

- Rising collaborations between pharmaceutical companies and research institutes are accelerating clinical trials and speeding up the development of next-generation oncology therapies

- Expanding government funding and cancer awareness programs are also contributing to earlier diagnosis and higher treatment adoption rates globally

Restraint/Challenge

“High Treatment Costs and Access Inequality Barriers”

- Concerns surrounding the high cost of advanced cancer therapies and unequal access to treatment across different regions pose a significant challenge to broader market penetration and patient affordability

- For instance, many novel immunotherapy and targeted therapy regimens can cost significantly more than traditional chemotherapy, limiting accessibility for patients in low- and middle-income countries

- In addition, reimbursement limitations and varying insurance coverage policies across healthcare systems further restrict patient access to innovative oncology treatments, particularly in emerging economies

- The complexity of cancer drug development, along with stringent regulatory approval processes, also contributes to prolonged timelines and increased commercialization costs for pharmaceutical companies

- While initiatives such as patient assistance programs and biosimilar development are helping to reduce cost burdens, affordability remains a key barrier to widespread adoption of advanced cancer therapies

- Limited oncology infrastructure and shortage of specialized healthcare professionals in developing regions further restrict timely diagnosis and treatment delivery

- Overcoming these challenges through improved pricing strategies, expanded healthcare coverage, and increased production of cost-effective oncology drugs will be vital for sustained market growth

Cancer Treatment Market Scope

The market is segmented on the basis of cancer type, treatment, route of administration, and end user.

- By Cancer Type

On the basis of cancer type, the market is segmented into breast cancer, colorectal cancer with liver metastases, lung carcinoma, prostate cancer, ovarian cancer, head-and-neck cancer, pancreatic cancer, glioblastoma, renal cell carcinoma, anaplastic thyroid carcinoma, sarcoma, and others. The lung carcinoma segment dominated the market with the largest revenue share of 19.4% in 2025, driven by its high global incidence, strong association with smoking and environmental pollution, and the widespread adoption of advanced therapies such as immunotherapy and targeted therapy. Lung cancer also benefits from significant clinical research activity and early adoption of precision medicine approaches, making it a major focus area for pharmaceutical innovation. In addition, increasing screening programs and improved diagnostic imaging are supporting earlier detection and higher treatment uptake.

The pancreatic cancer segment is expected to witness the fastest growth rate of 18.6% from 2026 to 2033, driven by rising disease awareness, increasing unmet clinical needs, and advancements in targeted and combination therapies. Pancreatic cancer has historically shown poor prognosis, encouraging strong R&D focus on novel treatment approaches such as immunotherapy combinations and precision oncology. For instance, new biomarker-based clinical trials are improving patient stratification and treatment effectiveness. The growing use of genetic testing is also enabling earlier identification of high-risk patients. Pharmaceutical companies are increasingly investing in breakthrough therapies to address the limited survival outcomes. In addition, expanding oncology research funding is accelerating innovation in this segment globally.

- By Treatment

On the basis of treatment, the market is segmented into medication, targeted therapies, radiotherapy, surgery, and others. The targeted therapies segment dominated the market with the largest revenue share of 38.6% in 2025, driven by its ability to selectively attack cancer cells while minimizing damage to healthy tissues, resulting in improved efficacy and reduced side effects compared to traditional chemotherapy. Targeted therapies are widely used across multiple cancer types including breast, lung, and colorectal cancers, significantly improving survival outcomes. The increasing adoption of biomarker-based diagnostics has further strengthened the use of these therapies in personalized treatment planning.

The immunotherapy and advanced medication segment (under others/biologics category) is expected to witness the fastest growth rate of 20.3% from 2026 to 2033, driven by rapid advancements in immune checkpoint inhibitors and CAR-T cell therapies. Immunotherapy is transforming cancer treatment by harnessing the body’s immune system to fight tumor cells more effectively. For instance, checkpoint inhibitors have shown significant success in melanoma and lung cancer treatment. Increasing clinical trials and regulatory approvals are expanding treatment indications across multiple cancer types. The growing shift toward personalized medicine is further accelerating adoption. In addition, combination regimens involving immunotherapy are showing superior clinical outcomes, driving strong future growth potential.

- By Route of Administration

On the basis of route of administration, the market is segmented into injectable, oral, and others. The injectable segment dominated the market with the largest revenue share of 72.8% in 2025, driven by the widespread use of intravenous chemotherapy, monoclonal antibodies, and immunotherapy drugs that require controlled administration in clinical settings. Injectable therapies ensure faster bioavailability and precise dosing, making them the preferred choice in hospital-based cancer treatment. Many advanced biologics and targeted therapies are also primarily developed in injectable forms due to their complex molecular structures.

The oral segment is expected to witness the fastest growth rate of 17.9% from 2026 to 2033, driven by increasing patient preference for convenient, non-invasive treatment options that can be administered at home. Oral chemotherapy and targeted therapy drugs are gaining popularity due to improved adherence and reduced hospital dependency. For instance, oral kinase inhibitors are widely used in chronic cancer management such as breast and renal cancers. The expansion of home-based cancer care models is further supporting growth. Pharmaceutical companies are increasingly focusing on developing oral formulations of advanced oncology drugs. In addition, improved drug stability and absorption technologies are enhancing the effectiveness of oral cancer treatments.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share of 64.5% in 2025, driven by the availability of advanced oncology infrastructure, multidisciplinary treatment capabilities, and access to a wide range of cancer therapies including chemotherapy, radiotherapy, and surgical oncology. Hospitals serve as the primary point of care for complex and late-stage cancer cases requiring integrated treatment approaches. The presence of specialized oncology departments and skilled healthcare professionals further strengthens hospital dominance.

The specialty clinics segment is expected to witness the fastest growth rate of 19.2% from 2026 to 2033, driven by increasing demand for personalized oncology care and outpatient treatment services. Specialty clinics offer focused cancer care with shorter waiting times and more individualized treatment plans. For instance, oncology clinics specializing in breast or hematologic cancers are expanding rapidly in urban regions. The rising adoption of ambulatory care and day-care chemotherapy services is further supporting growth. Patients are increasingly preferring specialty centers for follow-up treatments and second opinions. In addition, advancements in targeted therapies and oral medications are enabling more outpatient-based cancer care delivery models.

Cancer Treatment Market Regional Analysis

- North America dominated the cancer treatment market with the largest revenue share of 40.8% in 2025, supported by advanced healthcare infrastructure, strong oncology research funding, early adoption of innovative therapies, and the presence of leading pharmaceutical and biotechnology companies

- Patients and healthcare providers in the region highly value access to cutting-edge treatment modalities, precision oncology approaches, and comprehensive cancer care supported by well-established hospital networks and specialized oncology centers

- This widespread adoption is further supported by high healthcare expenditure, strong presence of leading pharmaceutical and biotechnology companies, and continuous investment in oncology research and clinical trials, establishing North America as a global hub for advanced cancer treatment solutions

The U.S. Cancer Treatment Market

The U.S. cancer treatment market captured the largest share within North America in 2025, driven by strong adoption of cutting-edge oncology therapies, advanced hospital infrastructure, and high investment in cancer research and development. Patients in the country benefit from early access to innovative treatments such as CAR-T therapies, immune checkpoint inhibitors, and precision medicine-based approaches. The strong presence of global pharmaceutical leaders and biotech startups further accelerates drug innovation and clinical trial activity. In addition, widespread health insurance coverage and increasing focus on personalized medicine are significantly boosting treatment adoption across cancer care centers.

Europe Cancer Treatment Market

The Europe cancer treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by rising cancer incidence, well-established public healthcare systems, and increasing focus on early diagnosis and structured screening programs. The region benefits from strong oncology infrastructure and widespread adoption of advanced therapies including targeted therapy, radiotherapy, and immunotherapy across hospitals and specialty centers. Favorable reimbursement frameworks and regulatory support for innovative oncology drugs are also encouraging faster adoption of new treatment options, strengthening the overall market growth in Europe.

U.K. Cancer Treatment Market

The U.K. cancer treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing cancer awareness, strong public healthcare delivery through the NHS, and rising demand for advanced oncology treatments. Growing concerns about cancer mortality are driving early screening initiatives and encouraging adoption of precision medicine-based approaches across healthcare facilities. In addition, the country’s strong clinical research ecosystem and participation in global oncology trials are improving patient access to innovative cancer therapies and strengthening treatment outcomes.

Germany Cancer Treatment Market

The Germany cancer treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by high healthcare spending, advanced hospital infrastructure, and strong emphasis on research-driven oncology care. The country’s focus on personalized medicine, biomarker-based therapies, and technologically advanced treatment methods is improving diagnostic accuracy and treatment effectiveness. Increasing integration of digital health solutions and strong collaboration between academic institutions and pharmaceutical companies are further accelerating oncology innovation and market expansion in Germany.

Asia-Pacific Cancer Treatment Market

The Asia-Pacific cancer treatment market is poised to grow at the fastest CAGR of 15.8% during the forecast period of 2026 to 2033, driven by rapidly increasing cancer prevalence, improving healthcare infrastructure, and expanding access to advanced oncology therapies. Government initiatives focused on cancer screening, early diagnosis, and healthcare modernization are significantly enhancing treatment adoption across emerging economies. Rising investments from global pharmaceutical companies and increasing affordability of cancer drugs are further strengthening the region’s growth potential.

Japan Cancer Treatment Market

The Japan cancer treatment market is gaining momentum due to its advanced healthcare system, strong technological capabilities, and high adoption of precision oncology and immunotherapy-based treatments. The country’s well-established cancer screening programs enable early detection, improving treatment success rates across major cancer types. In addition, the integration of robotics, AI-assisted diagnostics, and advanced surgical technologies is enhancing treatment precision and clinical outcomes, making Japan a key innovation-driven oncology market.

India Cancer Treatment Market

The India cancer treatment market accounted for the largest market share in Asia-Pacific in 2025, driven by a rapidly growing patient population, increasing cancer awareness, and expanding access to affordable oncology treatments. Strong growth in healthcare infrastructure, rising investments in specialized cancer hospitals, and government-led initiatives for early detection are improving treatment accessibility across urban and semi-urban regions. The availability of cost-effective generic oncology drugs and the expansion of private healthcare providers are further supporting strong market growth in India.

Cancer Treatment Market Share

The Cancer Treatment industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- AstraZeneca PLC (U.K.)

- Sanofi (France)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Merck KGaA (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Ipsen S.A. (France)

- Servier Laboratories (France)

- Pfizer Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Amgen Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Gilead Sciences, Inc. (U.S.)

What are the Recent Developments in Global Cancer Treatment Market?

- In November 2025, the U.S. FDA approved multiple new oncology therapies including sevabertinib for HER2-mutated non-small cell lung cancer and ziftomenib for relapsed/refractory acute myeloid leukemia, marking significant progress in precision oncology. These approvals expanded treatment options for genetically defined cancers and reinforced the shift toward biomarker-driven therapy selection. The approvals also included novel kinase inhibitors and combination regimens targeting hard-to-treat malignancies

- In November 2025, the FDA approved tarlatamab-dlle (Imdelltra) for extensive-stage small cell lung cancer after platinum-based chemotherapy. This bispecific T-cell engager represents a breakthrough in targeting DLL3-positive cancer cells, offering a new treatment option for highly aggressive and previously hard-to-treat cancers. The approval demonstrates rapid progress in precision immunotherapy and next-generation biologics

- In June 2025, the FDA expanded approval for Keytruda (pembrolizumab) as a perioperative treatment for PD-L1-positive resectable head and neck cancer, based on Phase III KEYNOTE-689 trial results. The study demonstrated a 30% reduction in event-free survival risk, establishing a new treatment paradigm in head and neck oncology. This development highlights increasing use of immunotherapy in combination with surgery and radiotherapy

- In April 2025, the U.S. FDA approved perioperative pembrolizumab (Keytruda) for resectable, locally advanced head and neck squamous cell carcinoma, marking a major shift in integrating immunotherapy into early-stage cancer treatment. The therapy is administered before and after surgery in combination with standard treatments, significantly reducing recurrence risk and improving event-free survival outcomes

- In February 2024, the U.S. FDA approved AMTAGVI (lifileucel), the first tumor-infiltrating lymphocyte (TIL) cell therapy for the treatment of advanced melanoma. This marked a major milestone as it became the first approved individualized cell therapy for a solid tumor cancer, expanding the role of adoptive cell therapy beyond hematologic malignancies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.