Global Cardiovascular Disease Drug Market

Market Size in USD Billion

USD

189.27 Billion

USD

280.06 Billion

2025

2033

USD

189.27 Billion

USD

280.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 189.27 Billion | |

| USD 280.06 Billion | |

| % | |

|

Cardiovascular Disease Drug Market Overview

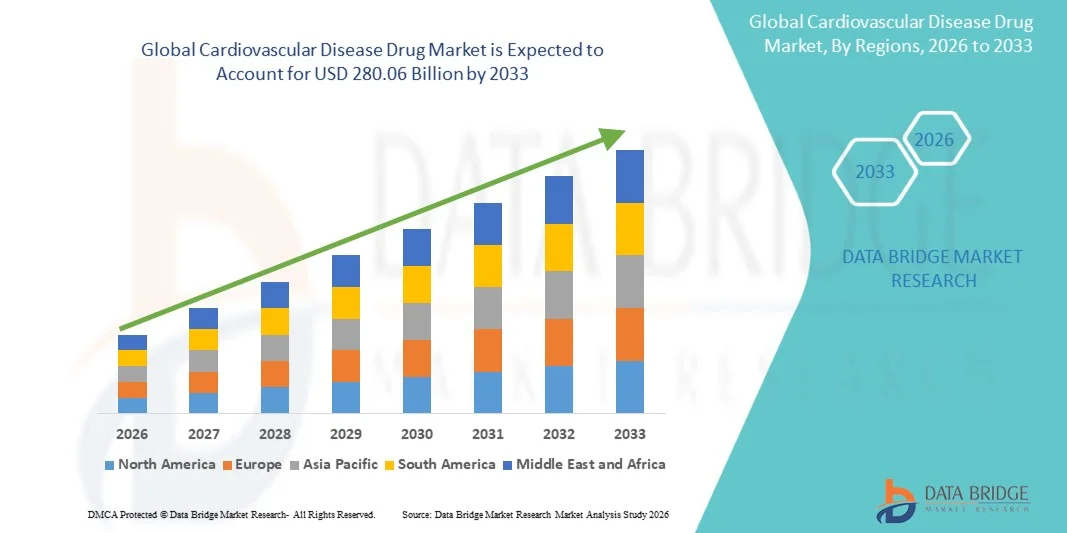

The Cardiovascular Disease Drug Market was valued at USD 189.27 billion in 2025 and is projected to reach USD 280.06 billion by 2033, growing at a CAGR of 5.02% from 2026 to 2033. The market is witnessing steady expansion driven by the rising global burden of cardiovascular disorders, increasing prevalence of hypertension, coronary artery disease, and stroke, along with growing geriatric population and lifestyle-related risk factors such as obesity, diabetes, and sedentary habits.

The growing demand for effective long-term disease management, combined with continuous innovation in anticoagulants, antihypertensives, lipid-lowering agents, and novel biologics, is significantly strengthening market growth. In addition, improved diagnostic rates, expanded healthcare access in emerging economies, and increasing adoption of combination therapies are encouraging widespread use of cardiovascular drugs. Strong pharmaceutical R&D pipelines and rising focus on preventive care and personalized medicine are further accelerating market expansion globally.

Key Market Trends & Insights

- North America dominated the Cardiovascular Disease Drug Market with the largest revenue share of 38.62% in 2025, supported by high disease prevalence, strong reimbursement systems, and advanced pharmaceutical R&D infrastructure.

- The Antihypertensive Drugs segment led the market with a 34.15% share in 2025, driven by the rising global burden of hypertension, which remains the primary risk factor for most cardiovascular diseases.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by increasing geriatric population, rapid urbanization, and expanding access to healthcare and generic medicines in China and India.

- Anticoagulants are the fastest-growing drug class, projected to register a CAGR of 7.3%, reflecting the surge in prevalence of atrial fibrillation, stroke risk, and thromboembolic disorders.

- The Coronary Artery Disease segment dominated the indication category with a 36.48% revenue share in 2025, led by its high global prevalence and strong association with lifestyle-related risk factors such as smoking, diabetes, and unhealthy diets

- Oral accounted for 72.6% of the market, preferred by its ease of administration, high patient compliance, and widespread use in chronic disease management.

- The Heart Failure segment is the fastest-growing indication category, with a CAGR of 7.1%, driven by rising aging population and increasing incidence of chronic cardiovascular complications.

Market Size & Forecast

- Global Market Value (2025): USD 189.27 Billion

- Expected Market Value (2033): USD 280.06 Billion

- Forecast CAGR (2026–2033): 5.02%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Cardiovascular Disease Drug Market Segmentation

|

Attributes |

Cardiovascular Disease Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Novartis AG (Switzerland) · Bayer AG (Germany) · Bristol-Myers Squibb Company (U.S.) · AstraZeneca (U.K.) · Sanofi (France) · Merck & Co., Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Eli Lilly and Company (U.S.) · Boehringer Ingelheim International GmbH (Germany) · Amgen Inc. (U.S.) · AbbVie Inc. (U.S.) · Daiichi Sankyo Company, Limited (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Novo Nordisk A/S (Denmark) · GSK plc (U.K.) · Servier Laboratories (France) · Teva Pharmaceutical Industries Ltd. (Israel) · Recordati S.p.A. (Italy) · Otsuka Pharmaceutical Co., Ltd. (Japan) |

|

Market Opportunities |

· Rapid expansion of novel oral anticoagulants (NOACs) and next-generation anti-thrombotic therapies · Increasing adoption of fixed-dose combination cardiovascular drugs (polypills) · Growing investment in personalized and precision cardiology therapies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cardiovascular Disease Drug Market Trends

Trend: Growth in Novel Oral Therapies & Combination Cardiovascular Treatments

Pharmaceutical companies are increasingly focusing on novel oral therapies and fixed-dose combination drugs to improve long-term adherence in cardiovascular disease management, particularly for hypertension, dyslipidemia, and heart failure. The shift toward single-pill regimens is reducing pill burden and improving patient compliance across aging populations. Integration of advanced drug formulations and extended-release mechanisms is enhancing therapeutic effectiveness and minimizing side effects, while precision medicine approaches are enabling more targeted treatment strategies based on patient risk profiles. For instance, NOAC-based combination therapies are being widely adopted in stroke prevention and atrial fibrillation management, demonstrating improved safety outcomes and simplified dosing regimens.

Cardiovascular Disease Drug Market Dynamics

Key Market Driver: Rising Prevalence of Lifestyle-Induced Cardiovascular Disorders

The increasing global burden of cardiovascular diseases driven by sedentary lifestyles, unhealthy dietary patterns, obesity, diabetes, and hypertension is significantly boosting demand for effective therapeutic drugs. Growing geriatric populations and improved diagnostic rates are further expanding the treated patient pool, leading to sustained prescription growth across both developed and emerging economies. Healthcare systems are increasingly prioritizing early intervention and chronic disease management, driving continuous consumption of antihypertensive, lipid-lowering, and anticoagulant drugs. For instance, widespread adoption of statin therapy in high-risk populations has significantly increased in both preventive and long-term cardiovascular care settings.

Key Restraint/Challenge: High Cost of Novel Cardiovascular Drug Development and Therapy

A major restraint in the cardiovascular disease drug market is the high cost associated with R&D, clinical trials, and commercialization of innovative therapies, particularly biologics and next-generation anticoagulants. Strict regulatory approval processes, patent expirations, and pricing pressures from healthcare payers further limit profitability and market accessibility in cost-sensitive regions. In addition, the long development timelines and risk of late-stage trial failures create financial uncertainty for pharmaceutical companies. For instance, the development of advanced PCSK9 inhibitors has demonstrated strong efficacy but remains limited in uptake due to high treatment costs and reimbursement constraints in several emerging markets.

Key Market Opportunity: Expansion of Precision Medicine and Biomarker-Guided Cardiovascular Therapies

The integration of precision medicine and biomarker-based drug development presents a major opportunity in the cardiovascular disease drug market, enabling more targeted and effective treatment approaches for high-risk patients. Advances in genomics, proteomics, and digital health monitoring are supporting the development of personalized therapy regimens that improve outcomes and reduce adverse effects. Pharmaceutical companies are increasingly investing in companion diagnostics and AI-driven drug discovery platforms to enhance treatment specificity and clinical success rates. For instance, biomarker-guided use of anticoagulants in atrial fibrillation patients is improving stroke prevention strategies while minimizing bleeding risks in personalized treatment pathways.

Cardiovascular Disease Drug Market Scope

The cardiovascular disease drug market is segmented on the basis of drug class, indication, route of administration, and distribution channel.

- By Drug Class

On the basis of drug class, the Cardiovascular Disease Drug Market is segmented into antihypertensive drugs, anticoagulants, antiplatelet drugs, lipid-lowering agents, beta blockers, calcium channel blockers, ACE inhibitors, angiotensin II receptor blockers, vasodilators, and others. The Antihypertensive Drugs segment dominated the market with a 34.15% share in 2025, owing to the rising global burden of hypertension, which remains the primary risk factor for most cardiovascular diseases. These drugs are widely prescribed across both primary care and specialty settings due to their effectiveness in long-term blood pressure control. Increasing geriatric population and lifestyle-related risk factors such as obesity and stress are further strengthening demand. Strong clinical guidelines recommending early intervention and continuous therapy also support consistent usage. In addition, high availability of generic antihypertensive medicines enhances accessibility across emerging economies.

The Anticoagulants segment is expected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by the increasing prevalence of atrial fibrillation, stroke risk, and thromboembolic disorders. Rising adoption of novel oral anticoagulants (NOACs) over traditional therapies is significantly improving patient compliance and safety outcomes. These drugs require less monitoring and offer predictable pharmacological effects, making them highly preferred in modern clinical practice. Expanding use in post-surgical and long-term cardiovascular risk management is further accelerating growth. Growing awareness regarding stroke prevention is also supporting wider adoption. Continuous innovation in safer and more effective anticoagulant therapies is strengthening this segment’s expansion.

- By Indication

On the basis of indication, the Cardiovascular Disease Drug Market is segmented into hypertension, coronary artery disease, arrhythmia, heart failure, dyslipidemia, stroke, and others. The Coronary Artery Disease segment dominated the market with a 36.48% revenue share in 2025, driven by its high global prevalence and strong association with lifestyle-related risk factors such as smoking, diabetes, and unhealthy diets. Patients require long-term pharmacological management, including statins, antiplatelets, and beta blockers, which significantly increases drug consumption. Improved diagnostic capabilities and early screening programs are further expanding the treated patient base. Hospitals and specialty clinics play a key role in continuous treatment adherence. Increasing cardiovascular mortality rates globally also contribute to sustained demand for CAD therapies.

The Heart Failure segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by rising aging population and increasing incidence of chronic cardiovascular complications. Advances in SGLT2 inhibitors and ARNI-based therapies are transforming treatment outcomes and expanding therapeutic options. Growing hospital admissions related to heart failure are increasing drug utilization significantly. Improved awareness and early diagnosis are enabling timely intervention and long-term management. Pharmaceutical companies are heavily investing in innovative heart failure drugs with better survival benefits. Expanding clinical guidelines supporting combination therapies are further accelerating segment growth.

- By Route of Administration

On the basis of route of administration, the Cardiovascular Disease Drug Market is segmented into oral, injectable, and others. The Oral segment dominated the market with a 72.6% share in 2025, owing to its ease of administration, high patient compliance, and widespread use in chronic disease management. Most cardiovascular drugs such as statins, antihypertensives, and beta blockers are orally administered for long-term therapy. Oral formulations are preferred in outpatient and homecare settings due to convenience and cost-effectiveness. Availability of extended-release and once-daily formulations further improves adherence. Strong penetration of generic oral drugs also supports market dominance. Continuous innovation in oral drug delivery systems enhances therapeutic efficiency.

The Injectable segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing use of biologics and advanced lipid-lowering therapies. Injectable drugs are gaining traction in acute care settings such as hospitals and emergency cardiovascular interventions. High efficacy and rapid action make them suitable for critical conditions such as acute heart failure and severe hypercholesterolemia. Development of long-acting injectable therapies is improving patient convenience. Rising adoption of PCSK9 inhibitors is significantly contributing to segment expansion. Increasing focus on advanced biologic cardiovascular therapies is further supporting growth.

- By Distribution Channel

On the basis of distribution channel, the Cardiovascular Disease Drug Market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The Hospital Pharmacies segment dominated the market with a 52.11% share in 2025, driven by high patient inflow in acute cardiovascular cases and strong prescription rates from hospital-based specialists. Hospitals serve as the primary point of care for critical conditions such as myocardial infarction and heart failure. Strong availability of emergency and chronic cardiovascular medications supports continuous demand. Integration with inpatient treatment systems ensures consistent drug dispensing. Government healthcare systems and insurance coverage further strengthen hospital-based distribution. Increasing hospitalization rates for cardiovascular conditions also reinforce segment leadership.

The Online Pharmacies segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by rising digital healthcare adoption and increasing preference for home delivery of medicines. Patients with chronic cardiovascular conditions are increasingly opting for convenient refill options. Growing penetration of e-commerce healthcare platforms is improving drug accessibility in urban and semi-urban regions. Digital prescriptions and telemedicine integration are further accelerating adoption. Competitive pricing and discounts are also encouraging usage of online channels. Expanding digital infrastructure in emerging economies is supporting rapid segment growth.

Cardiovascular Disease Drug Market Regional Analysis

North America dominated the Cardiovascular Disease Drug Market with the largest revenue share of 38.62% in 2025, supported by high disease prevalence, strong reimbursement systems, and advanced pharmaceutical R&D infrastructure. The region also benefits from robust pharmaceutical R&D activities, early adoption of novel drug classes such as NOACs and PCSK9 inhibitors, and favorable reimbursement frameworks. Increasing focus on preventive cardiology, widespread statin usage, and strong presence of leading pharmaceutical companies continues to strengthen North America’s leadership position in the global market.

U.S. Cardiovascular Disease Drug Market Insight

The U.S. cardiovascular disease drug market is witnessing strong growth due to high prevalence of cardiovascular disorders, strong healthcare infrastructure, and extensive adoption of advanced therapeutic drugs. The country’s mature pharmaceutical ecosystem, along with increasing use of novel anticoagulants, statins, and biologics, is driving demand across hospitals, specialty clinics, and retail pharmacies. In addition, growing emphasis on preventive cardiology, early diagnosis, and personalized medicine is accelerating drug adoption across high-risk patient populations, supported by strong insurance coverage and advanced clinical care systems.

Europe Cardiovascular Disease Drug Market Insight

The Europe cardiovascular disease drug market remains a major contributor to global revenue, driven by strong government healthcare systems, high disease awareness, and widespread access to essential cardiovascular therapies. The region benefits from robust clinical research activity, increasing adoption of combination therapies, and strong focus on early disease management and preventive care. Growing elderly population, structured reimbursement frameworks, and standardized treatment guidelines continue to enhance cardiovascular drug utilization across major European economies, ensuring consistent market demand.

U.K. Cardiovascular Disease Drug Market Insight

The U.K. cardiovascular disease drug market is experiencing steady growth, supported by rising burden of heart disease, strong NHS-driven treatment access, and increasing adoption of preventive therapies. Expanding use of statins, antihypertensives, and anticoagulants is contributing to market growth across both primary and secondary care settings. Furthermore, integration of clinical guidelines, national screening programs, and data-driven treatment approaches is improving patient outcomes, while increasing focus on early intervention is supporting long-term drug consumption.

Germany Cardiovascular Disease Drug Market Insight

The Germany cardiovascular disease drug market is expanding steadily due to strong pharmaceutical manufacturing capabilities, advanced clinical research infrastructure, and high demand for innovative therapies. Cardiovascular drugs are widely used in hospitals and outpatient care for managing chronic conditions such as hypertension, coronary artery disease, and heart failure. Continuous adoption of advanced lipid-lowering agents, combination therapies, and structured healthcare reimbursement systems is further strengthening treatment accessibility and supporting consistent market growth.

Asia-Pacific Cardiovascular Disease Drug Market Insight

The Asia-Pacific cardiovascular disease drug market is expected to witness rapid growth, driven by increasing geriatric population, rising prevalence of lifestyle-related diseases, and expanding healthcare access across emerging economies. Growing awareness regarding early diagnosis and long-term disease management, along with increasing availability of affordable generic drugs, is supporting regional market expansion. In addition, rising healthcare investments, expansion of insurance coverage, and pharmaceutical manufacturing growth are accelerating drug adoption across both urban and semi-urban populations.

Japan Cardiovascular Disease Drug Market Insight

The Japan cardiovascular disease drug market is witnessing consistent growth due to aging population, advanced healthcare system, and strong focus on chronic disease management. Widespread adoption of antihypertensive and lipid-lowering therapies is driving steady demand across hospitals and outpatient care facilities. Moreover, increasing use of innovative drug formulations, improved adherence strategies, and precision medicine approaches is further enhancing treatment outcomes and strengthening long-term cardiovascular care management.

China Cardiovascular Disease Drug Market Insight

The China cardiovascular disease drug market is growing rapidly, driven by rising prevalence of hypertension, coronary artery disease, and diabetes, along with expanding healthcare infrastructure. Increasing government focus on chronic disease management, improved access to essential medicines, and large-scale public health initiatives are significantly boosting drug consumption. In addition, rapid expansion of domestic pharmaceutical production, growing hospital networks, and increasing adoption of modern cardiovascular therapies are positioning China as one of the fastest-growing markets globally.

Cardiovascular Disease Drug Market Share

The cardiovascular disease drug industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Amgen Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Novo Nordisk A/S (Denmark)

- GSK plc (U.K.)

- Servier Laboratories (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Recordati S.p.A. (Italy)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

Latest Developments in Cardiovascular Disease Drug Market

- In May 2023, the U.S. FDA approved Inpefa (sotagliflozin) developed by Lexicon Pharmaceuticals and Bayer for reducing the risk of cardiovascular death, heart failure hospitalization, and urgent care visits in adults with heart failure or type 2 diabetes with cardiovascular risk. This approval strengthened the role of dual SGLT1/2 inhibition in cardiovascular protection, particularly for high-risk patients. The drug adds another important option in the growing SGLT inhibitor class, which is increasingly used in cardiometabolic disease management. FDA Inpefa Approval

- In March 2023, results from the CLEAR Outcomes trial demonstrated that bempedoic acid (Nexletol/Nexlizet) significantly reduced major adverse cardiovascular events in statin-intolerant patients, providing strong evidence for its role in LDL cholesterol management. The study highlighted its effectiveness in lowering cardiovascular risk without the muscle-related side effects often associated with statins, making it an important alternative therapy. These findings have supported broader clinical acceptance of non-statin lipid-lowering strategies in cardiovascular disease prevention

- In August 2022, the U.S. FDA approved Jardiance (empagliflozin) from Boehringer Ingelheim and Eli Lilly for heart failure with preserved ejection fraction (HFpEF). This expanded indication significantly broadened its use beyond diabetes and reduced ejection fraction heart failure, making it a key therapy in cardiovascular care. Clinical studies demonstrated reduced hospitalization risk and improved quality of life in patients with HFpEF, addressing a previously underserved patient population with limited treatment options. FDA Jardiance Heart Failure Approval

- In December 2021, the U.S. FDA approved Leqvio (inclisiran) by Novartis, the first small-interfering RNA (siRNA) therapy for LDL cholesterol reduction. The therapy offers a twice-yearly dosing regimen, significantly improving patient adherence compared to daily statins, especially in long-term cardiovascular risk management. It targets PCSK9 production in the liver, leading to sustained LDL cholesterol lowering and providing an important option for patients with atherosclerotic cardiovascular disease or familial hypercholesterolemia. FDA Leqvio Approval

- In January 2021, the U.S. FDA approved Verquvo (vericiguat) developed by Bayer and Merck for the treatment of patients with symptomatic chronic heart failure with reduced ejection fraction. This approval was based on clinical evidence showing its ability to reduce the risk of cardiovascular death and heart failure hospitalization in high-risk patients already receiving standard therapy. The drug introduced a new therapeutic mechanism targeting the nitric oxide–soluble guanylate cyclase pathway, strengthening treatment options for advanced heart failure management. FDA Verquvo Approval

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.