Global Catalyst Regeneration Market

Market Size in USD Billion

CAGR :

%

USD

4.90 Billion

USD

9.37 Billion

2025

2033

USD

4.90 Billion

USD

9.37 Billion

2025

2033

| 2026 –2033 | |

| USD 4.90 Billion | |

| USD 9.37 Billion | |

| % | |

|

Catalyst Regeneration Market Size

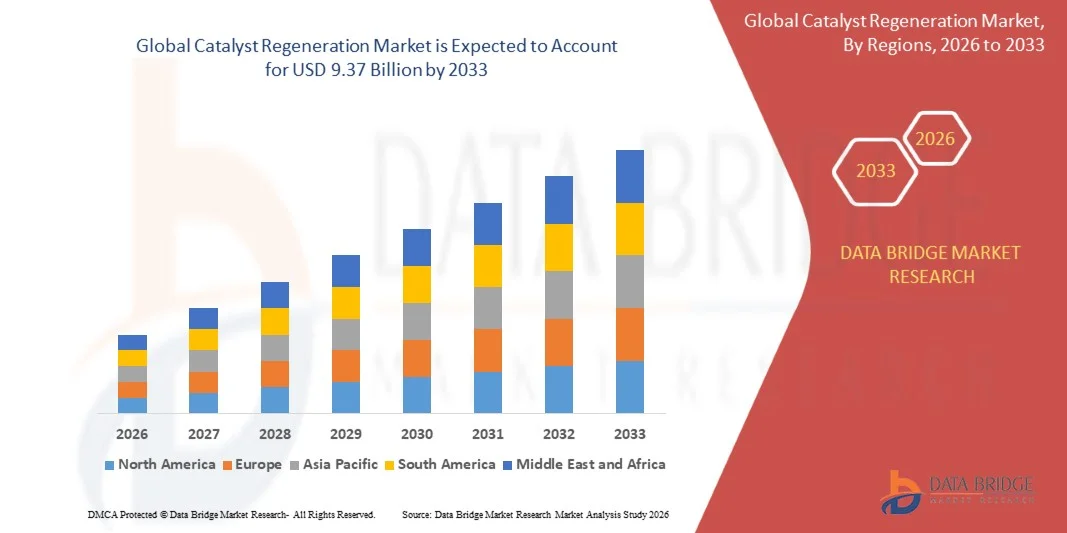

- The global catalyst regeneration market size was valued at USD 4.90 billion in 2025 and is expected to reach USD 9.37 billion by 2033, at a CAGR of 8.45% during the forecast period

- The market growth is largely fueled by the increasing demand for cost optimization and operational efficiency in refining and chemical industries, as catalyst regeneration enables extended catalyst life and reduces the need for frequent replacement, thereby lowering overall production costs

- Furthermore, rising environmental regulations and the need to minimize industrial waste are encouraging industries to adopt regeneration solutions that support sustainable practices and efficient resource utilization, significantly boosting the demand for catalyst regeneration services

Catalyst Regeneration Market Analysis

- Catalyst regeneration involves the restoration of spent catalysts to their original activity and selectivity through processes such as coke removal, metal recovery, and reactivation, making it a critical component in refining, petrochemical, and environmental applications

- The escalating demand for catalyst regeneration is primarily driven by the continuous use of catalysts in hydroprocessing, fluid catalytic cracking, and emission control systems, along with increasing focus on sustainability, cost efficiency, and compliance with stringent environmental standards

- Asia-Pacific dominated the catalyst regeneration market with a share of 42.60% in 2025, due to the strong presence of petroleum refining capacity, rapid industrialization, and increasing demand for efficient catalyst utilization across chemical and energy sectors

- North America is expected to be the fastest growing region in the catalyst regeneration market during the forecast period due to the presence of large-scale refineries, increasing demand for cost-efficient operations, and advancements in regeneration technologies

- Off-site regeneration segment dominated the market with a market share of 73.10% in 2025, due to its ability to provide thorough and standardized regeneration processes under controlled industrial conditions. Refineries and chemical manufacturers often prefer off-site services due to access to advanced technologies, skilled expertise, and compliance with stringent environmental regulations. This method ensures consistent catalyst performance and extended lifecycle, reducing the need for frequent catalyst replacement

Report Scope and Catalyst Regeneration Market Segmentation

|

Attributes |

Catalyst Regeneration Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Catalyst Regeneration Market Trends

“Rising Adoption of Sustainable and Circular Catalyst Management Practices”

- A significant trend in the catalyst regeneration market is the increasing shift toward sustainable and circular management of catalysts, driven by the need to reduce industrial waste and optimize resource utilization across refining and chemical industries. This trend is strengthening the role of regeneration as a critical solution for extending catalyst life while minimizing environmental impact

- For instance, BASF SE has been advancing catalyst recycling and regeneration solutions that improve metal recovery and reduce waste generation across chemical processes. Such initiatives are supporting circular economy goals and encouraging wider adoption of regeneration services across industries

- Industries are increasingly focusing on reducing dependence on fresh catalyst production by reusing spent catalysts through advanced regeneration techniques that restore activity and performance. This is improving cost efficiency and aligning with sustainability targets across large-scale industrial operations

- The growing emphasis on emission reduction in sectors such as power generation and refining is driving the use of regenerated catalysts in emission control systems. This trend is enhancing the demand for regeneration services as companies aim to comply with stricter environmental norms

- Technological advancements in regeneration processes are enabling higher recovery rates and improved catalyst performance, making regenerated catalysts more comparable to fresh alternatives. This is increasing confidence among end-users and supporting long-term adoption

- The market is witnessing a transition toward integrated catalyst lifecycle management where regeneration, recycling, and reuse are becoming essential components of industrial strategies. This is reinforcing the importance of sustainable practices and positioning catalyst regeneration as a key enabler of efficient and environmentally responsible operations

Catalyst Regeneration Market Dynamics

Driver

“Increasing Demand for Cost Optimization and Catalyst Lifecycle Extension”

- The increasing need to optimize operational costs in refining and chemical industries is driving the demand for catalyst regeneration, as it allows companies to extend catalyst lifespan and reduce replacement frequency. This approach significantly lowers capital expenditure while maintaining process efficiency across critical applications

- For instance, Honeywell UOP provides catalyst regeneration services that help refiners restore catalyst performance and reduce downtime, improving overall plant productivity. These solutions enable operators to achieve better returns on catalyst investments while maintaining consistent output

- Catalysts used in processes such as hydroprocessing and fluid catalytic cracking require regular maintenance to sustain efficiency, making regeneration a cost-effective alternative to replacement. This is increasing reliance on regeneration services across large-scale industrial facilities

- Industries are focusing on maximizing asset utilization and minimizing operational disruptions, which is encouraging the adoption of on-site and off-site regeneration solutions. This trend is supporting continuous production and improving overall process reliability

- The ongoing need for efficient and economical production processes continues to reinforce this driver, as companies seek to balance performance, cost, and sustainability. This is positioning catalyst regeneration as a vital strategy for long-term operational optimization across industries

Restraint/Challenge

“Stringent Environmental Regulations and Complex Regeneration Processes”

- The catalyst regeneration market faces challenges due to stringent environmental regulations that govern emissions, waste handling, and disposal processes, requiring companies to adopt advanced and compliant regeneration technologies. These regulations increase operational complexity and raise compliance costs for service providers

- For instance, Environmental Protection Agency enforces strict emission and waste management standards that impact catalyst regeneration operations, requiring companies to invest in advanced treatment and monitoring systems. This adds to operational expenses and creates barriers for smaller players in the market

- The regeneration process itself involves complex procedures such as coke removal, metal recovery, and reactivation, which require specialized equipment and technical expertise. These complexities can limit scalability and increase turnaround time for regeneration services

- Handling hazardous materials and ensuring safe processing conditions further adds to the operational burden, requiring strict adherence to safety protocols and environmental guidelines. This increases the overall cost and complexity of regeneration operations

- The combined impact of regulatory pressures and technical complexities continues to restrain market growth, as companies must balance compliance requirements with cost efficiency and operational feasibility. This challenge underscores the need for continuous innovation and process optimization within the catalyst regeneration industry

Catalyst Regeneration Market Scope

The market is segmented on the basis of type, end-user, and application.

• By Type

On the basis of type, the catalyst regeneration market is segmented into off-site regeneration and on-site regeneration. The off-site regeneration segment dominated the largest market revenue share of 73.10% in 2025, driven by its ability to provide thorough and standardized regeneration processes under controlled industrial conditions. Refineries and chemical manufacturers often prefer off-site services due to access to advanced technologies, skilled expertise, and compliance with stringent environmental regulations. This method ensures consistent catalyst performance and extended lifecycle, reducing the need for frequent catalyst replacement. In addition, off-site regeneration allows companies to minimize operational risks and maintain high efficiency across critical processes. The availability of specialized service providers further strengthens the dominance of this segment.

The on-site regeneration segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for minimizing downtime and operational disruptions. Industries are adopting on-site solutions to regenerate catalysts directly within their facilities, reducing transportation costs and turnaround time. This approach enhances operational flexibility and allows continuous production without significant interruptions. Technological advancements have improved the efficiency and safety of on-site regeneration processes, making them more viable for large-scale applications. Growing emphasis on cost optimization and real-time maintenance is accelerating adoption across refineries and chemical plants.

• By End-User

On the basis of end-user, the catalyst regeneration market is segmented into petroleum refining, chemical synthesis, environmental, and polymer. The petroleum refining segment dominated the largest market revenue share in 2025, driven by the extensive use of catalysts in refining processes such as hydrocracking and fluid catalytic cracking. Refineries require regular catalyst regeneration to maintain operational efficiency and meet fuel quality standards. Increasing global demand for refined petroleum products continues to support consistent utilization of catalyst regeneration services. Stringent environmental regulations further necessitate efficient catalyst performance, reinforcing demand in this segment. The scale of refinery operations and continuous processing requirements significantly contribute to its market leadership.

The chemical synthesis segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for specialty chemicals and increased production activities worldwide. Chemical manufacturers rely on catalysts to optimize reaction efficiency and product yield, making regeneration essential for cost control. Expansion of chemical industries in emerging economies is driving higher adoption of regeneration services. In addition, advancements in catalyst technologies are encouraging more frequent regeneration to maintain process efficiency. The need for sustainable and resource-efficient production practices further accelerates growth in this segment.

• By Application

On the basis of application, the catalyst regeneration market is segmented into coal power plant, cement plant, steel plant, and others. The coal power plant segment dominated the largest market revenue share in 2025, driven by the widespread use of catalysts in emission control systems such as selective catalytic reduction. Power plants require regular regeneration to ensure effective reduction of nitrogen oxide emissions and compliance with environmental standards. Increasing regulatory pressure on emissions has reinforced the need for efficient catalyst performance in thermal power generation. The large installed base of coal-fired plants globally further supports sustained demand for regeneration services. Continuous operation and high catalyst usage make this segment a key contributor to market revenue.

The cement plant segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising infrastructure development and increased cement production globally. Cement manufacturing processes involve emission control systems that depend on catalyst efficiency, driving the need for regeneration. Growing environmental concerns and stricter emission norms are encouraging adoption of catalyst regeneration in cement plants. Technological improvements are enabling more efficient regeneration processes tailored to cement industry requirements. Expansion of construction activities, particularly in developing regions, is further accelerating demand in this segment.

Catalyst Regeneration Market Regional Analysis

- Asia-Pacific dominated the catalyst regeneration market with the largest revenue share of 42.60% in 2025, driven by the strong presence of petroleum refining capacity, rapid industrialization, and increasing demand for efficient catalyst utilization across chemical and energy sectors

- The region’s expanding refining infrastructure, cost-efficient service capabilities, and rising investments in chemical manufacturing are accelerating the adoption of catalyst regeneration services

- Growing environmental regulations, availability of skilled workforce, and increasing focus on operational efficiency across developing economies are contributing to higher demand for regeneration solutions

China Catalyst Regeneration Market Insight

China held the largest share in the Asia-Pacific catalyst regeneration market in 2025, owing to its extensive refining capacity and dominance in chemical manufacturing. The country’s strong industrial ecosystem, continuous expansion of petrochemical complexes, and government support for sustainable industrial practices are major growth drivers. Increasing focus on emission reduction and cost optimization is further driving the demand for catalyst regeneration services across industries.

India Catalyst Regeneration Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by expanding refinery capacity, rising chemical production, and increasing focus on reducing operational costs. Government initiatives supporting domestic manufacturing and industrial expansion are strengthening demand for regeneration services. In addition, growing emphasis on environmental compliance and efficient catalyst usage is contributing to significant market growth.

Europe Catalyst Regeneration Market Insight

The Europe catalyst regeneration market is expanding steadily, supported by strict environmental regulations, strong presence of advanced refining technologies, and increasing focus on sustainability. Industries in the region emphasize reducing waste and improving catalyst lifecycle efficiency, driving demand for regeneration services. Continuous investments in cleaner production technologies are further supporting market expansion.

Germany Catalyst Regeneration Market Insight

Germany’s catalyst regeneration market is driven by its well-established chemical industry, advanced manufacturing capabilities, and strong focus on sustainable industrial practices. The country benefits from high adoption of efficient process technologies and robust R&D infrastructure. Demand is supported by the need to optimize catalyst performance and comply with stringent environmental standards.

U.K. Catalyst Regeneration Market Insight

The U.K. market is supported by increasing investments in chemical processing industries and a growing focus on reducing industrial emissions. Strong regulatory frameworks and emphasis on sustainability are encouraging the adoption of catalyst regeneration services. The country’s focus on innovation and efficient resource utilization is further contributing to market growth.

North America Catalyst Regeneration Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by the presence of large-scale refineries, increasing demand for cost-efficient operations, and advancements in regeneration technologies. Rising environmental awareness and strict emission norms are encouraging industries to adopt regeneration solutions. In addition, ongoing modernization of refining infrastructure is supporting market expansion.

U.S. Catalyst Regeneration Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its extensive refining network, strong technological capabilities, and high adoption of advanced catalyst management practices. The country’s focus on operational efficiency, regulatory compliance, and sustainability is driving consistent demand for regeneration services. Presence of major industry players and continuous investments in process optimization further strengthen its market position.

Catalyst Regeneration Market Share

The catalyst regeneration industry is primarily led by well-established companies, including:

- Al Bilad Catalyst Company (Saudi Arabia)

- Coalogix Inc. (U.S.)

- Cormetech Inc. (U.S.)

- EBINGER Katalysatorservice GmbH & Co. KG (Germany)

- Eco-Rigen S.r.l. (Italy)

- EURECAT INDIA Catalyst Services Pvt Ltd (India)

- Haldor Topsoe A/S (Denmark)

- NIPPON KETJEN Co. Ltd. (Japan)

- Porocel (U.S.)

- STEAG ENERGY SERVICES (Germany)

- Advanced Catalyst System LLC (U.S.)

- Albemarle Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- Johnson Matthey (U.K.)

- BASF SE (Germany)

Latest Developments in Global Catalyst Regeneration Market

- In May 2025, Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business for USD 2.4 billion, significantly strengthening its integrated capabilities across catalyst manufacturing, regeneration, and metals recovery. This strategic consolidation is enabling the company to offer a unified platform that improves catalyst lifecycle efficiency and streamlines operations for refiners and petrochemical producers. The move is also enhancing scalability and technological depth, allowing end-users to reduce downtime, optimize catalyst performance, and achieve better cost control, thereby accelerating the adoption of regeneration services across the market

- In April 2025, Clariant launched the StyroMax UL-100 catalyst, achieving benchmark styrene yields at a reduced steam-to-oil ratio of 0.76 wt. This advancement is significantly lowering energy consumption in styrene monomer production, addressing one of the key cost and sustainability challenges in the industry. As producers increasingly focus on energy efficiency and emission reduction, such high-performance catalysts are driving the need for specialized regeneration services to maintain optimal performance over extended operational cycles

- In February 2025, Albemarle Corporation expanded its catalyst regeneration service capabilities with advanced reactivation technologies designed to restore catalyst activity in hydroprocessing applications. This development is enabling refineries to extend catalyst lifespan and reduce the frequency of costly replacements, improving overall operational efficiency. The increased reliability and effectiveness of regeneration solutions are encouraging broader adoption among refiners aiming to maximize returns on catalyst investments while maintaining consistent processing output

- In January 2025, BASF introduced enhanced catalyst recycling and regeneration solutions focused on improving metal recovery rates and minimizing industrial waste. This initiative is supporting the transition toward circular economy practices by enabling the reuse of valuable metals and reducing dependency on raw material extraction. As environmental regulations become more stringent, such sustainable regeneration solutions are gaining traction, driving demand across chemical and refining industries seeking compliance and cost efficiency

- In 2023, Honeywell UOP strengthened its position as a global leader in refining and petrochemical technologies through its robust catalyst division offering both manufacturing and regeneration services. Its integrated approach allows refiners to seamlessly manage catalyst performance throughout its lifecycle, ensuring higher process efficiency and reduced operational disruptions. The company’s continued investment in innovation and service capabilities is reinforcing its influence in the catalyst regeneration market while supporting long-term industry growth

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Catalyst Regeneration Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Catalyst Regeneration Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Catalyst Regeneration Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.