Global Cell Based Assays Market

Market Size in USD Billion

CAGR :

%

USD

24.95 Billion

USD

43.51 Billion

2025

2033

USD

24.95 Billion

USD

43.51 Billion

2025

2033

| 2026 –2033 | |

| USD 24.95 Billion | |

| USD 43.51 Billion | |

| % | |

|

Cell Based Assays Market Size

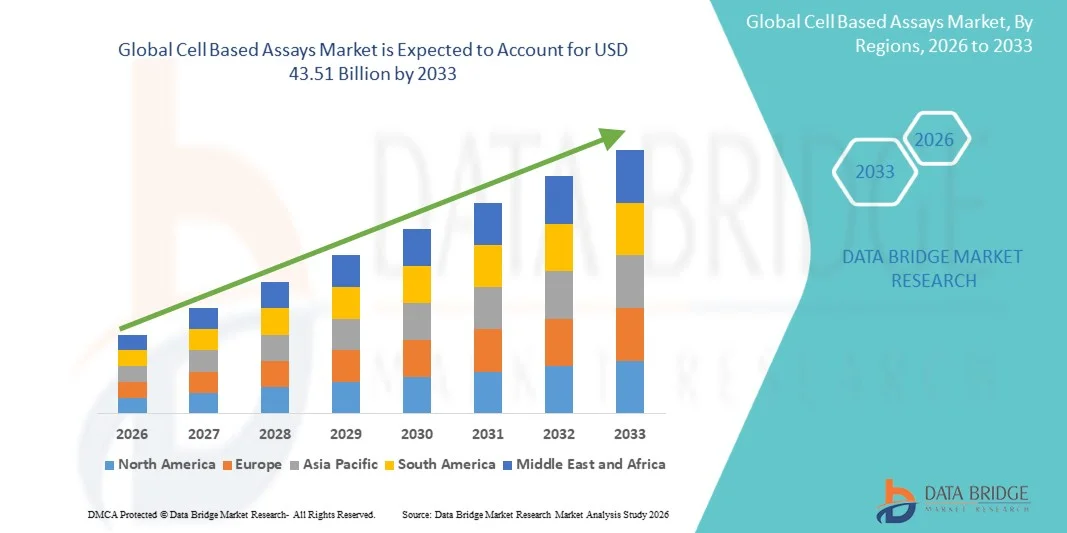

- The global cell-based assays market size was valued at USD 24.95 billion in 2025 and is expected to reach USD 43.51 billion by 2033, at a CAGR of 7.20% during the forecast period

- The market growth is largely fueled by rapid advancements in cell biology research, increasing adoption of high-throughput screening techniques, and the growing demand for reliable, reproducible, and sensitive assay systems in drug discovery and development

- Furthermore, rising investment from pharmaceutical and biotechnology companies, coupled with expanding applications in oncology, immunology, and toxicology studies, is establishing cell-based assays as a critical tool in preclinical and clinical research. These converging factors are accelerating the uptake of cell-based assay solutions, thereby significantly boosting the market’s growth

Cell Based Assays Market Analysis

- Cell-based assays, providing reliable and reproducible in vitro testing platforms, are increasingly vital in modern drug discovery, toxicology testing, and biomedical research due to their ability to mimic physiological conditions and deliver high-throughput, quantitative results

- The escalating demand for cell-based assays is primarily fueled by the growth of pharmaceutical and biotechnology research, increasing preclinical and clinical trial activities, and rising adoption in oncology, immunology, and infectious disease studies

- North America dominated the cell based assays market with the largest revenue share of approximately 41.2% in 2025, driven by the presence of major pharmaceutical and biotechnology companies, advanced research infrastructure, and extensive government and private funding for biomedical research

- Asia-Pacific is expected to be the fastest-growing region in the cell based assays market during the forecast period, with a projected CAGR of 9.6%, supported by increasing investment in R&D, expanding biotech and CRO infrastructure, and a rising number of clinical trials in countries such as China, India, and Japan

- The drug discovery segment dominated the largest market revenue share of 47.8% in 2025, due to extensive use in preclinical screening, lead identification, and toxicity studies

Report Scope and Cell Based Assays Market Segmentation

|

Attributes |

Cell Based Assays Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Thermo Fisher Scientific, Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cell Based Assays Market Trends

“Enhanced Advancements in Cell Based Assays”

- A major trend in the global cell based assays market is the increasing adoption of high-throughput and automated assay platforms that enable faster, more reproducible, and data-rich results

- For instance, Thermo Fisher Scientific launched its Applied Biosystems™ High-Throughput Screening Assay platform in 2024, enabling parallel testing of thousands of samples in drug discovery workflows

- Advanced 3D cell culture models, organ-on-chip systems, and multiplexed assay platforms are increasingly being integrated into preclinical and clinical research workflows to improve accuracy and reduce experimental variability

- North America dominated the market with approximately 42.3% revenue share in 2025, driven by strong R&D investments, early adoption of advanced assay technologies, and the presence of leading biotechnology and pharmaceutical companies such as Thermo Fisher Scientific, PerkinElmer, and BioTek Instruments

- Asia-Pacific is projected to be the fastest-growing region with a CAGR of 10.2% from 2026 to 2033, supported by expanding biotech infrastructure, increasing clinical research activities, and rising healthcare investments in countries like China, Japan, and India

- Europe is witnessing steady growth with a CAGR of 8.5%, primarily due to stringent regulatory requirements, high demand for preclinical testing, and increasing adoption of standardized assay protocols

Cell Based Assays Market Dynamics

Driver

“Growing Demand from Drug Discovery, Clinical Research, and Biotechnology”

- Increasing R&D investment in pharmaceuticals and biotechnology is driving demand for cell-based assays, particularly for oncology, regenerative medicine, and personalized therapies

- For instance, in 2025, Merck KGaA collaborated with the Broad Institute to implement high-content cell-based assays for precision oncology research, enhancing the screening of novel therapeutic compounds

- Global pharmaceutical R&D expenditure exceeded USD 210 billion in 2025, with a significant portion allocated to preclinical studies using advanced assay models

- Collaborations between research institutions and pharmaceutical companies, along with rising clinical trial activities, are accelerating adoption worldwide

- The increasing focus on disease modeling, drug toxicity testing, and mechanism-of-action studies further strengthens the market, particularly in North America, which contributed 42.3% of revenue in 2025, and in Asia-Pacific, expected to reach a CAGR of 10.2%

Restraint/Challenge

“Concerns Regarding Cybersecurity and High Initial Costs”

- The high cost of advanced assay systems and reagents remains a key challenge, limiting adoption in smaller laboratories and developing regions

- For instance, Promega Corporation’s multiplexed assay kits, while highly efficient, cost significantly more than traditional assays, restricting adoption among mid-sized biotech firms in Latin America

- Technical complexity and the need for skilled personnel to execute and interpret experiments restrict market penetration

- Variability in cell lines, culture conditions, and experimental protocols can cause inconsistent results, creating a demand for standardized solutions

- Companies such as Agilent Technologies, Promega Corporation, and BioTek Instruments are addressing these challenges by offering user-friendly kits and standardized protocols, but high premium pricing continues to limit adoption

- Global market expansion is also restrained in Latin America and the Middle East & Africa, where infrastructure and training remain limited, contributing only 5–7% to the total market share in 2025

Cell Based Assays Market Scope

The market is segmented on the basis of type, product and services, technology, application, end user, and distribution channel.

- By Type

On the basis of type, the Cell Based Assays market is segmented into cell viability assay, cytotoxicity assay, cell death assay, cell proliferation assay, and others. The cell viability assay segment dominated the largest market revenue share of 41.8% in 2025, driven by its widespread application in evaluating drug safety and efficacy. The segment is preferred by pharmaceutical and biotechnology companies for preclinical screening due to its reliability and reproducibility. High adoption in contract research organizations (CROs) and academic research institutions enhances market penetration. Advances in assay kits and automation systems support faster throughput and consistent results. The availability of ready-to-use kits, reagents, and standardized protocols promotes adoption across global laboratories. Increasing R&D in oncology, infectious diseases, and regenerative medicine further fuels demand. Integration with high-throughput and high-content screening platforms strengthens its usage. Government initiatives supporting life sciences research increase adoption. Robust analytical tools and software for data interpretation enhance the segment’s utility. The segment benefits from growing pharmaceutical pipelines and regulatory support for innovative therapeutics. Rising awareness of cell-based methodologies in drug discovery accelerates its market dominance.

The cytotoxicity assay segment is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, driven by increasing demand in drug discovery, safety evaluation, and toxicology studies. The segment benefits from advancements in live-cell imaging, real-time monitoring, and label-free detection technologies. Rising adoption in academic and clinical research institutions supports growth. Expansion of biotechnology and pharmaceutical R&D globally accelerates demand. Integration with automated platforms improves throughput and reduces variability. High sensitivity and specificity of modern cytotoxicity assays enhance utility. Governments and private organizations fund research on novel therapeutics, increasing assay demand. Emerging applications in regenerative medicine and gene therapies contribute to adoption. Rapid urbanization and technological development in Asia-Pacific enhance market expansion. Increasing clinical trial activity and outsourcing to CROs drive segment growth. Innovations in multiplexed assays and miniaturization reduce costs and improve efficiency. Pharmaceutical collaborations and academic partnerships boost global availability and usage.

- By Product and Services

On the basis of product and services, the market is segmented into consumables, services, instruments, and software. The consumables segment held the largest market revenue share of 46.3% in 2025, driven by the recurring demand for reagents, kits, and specialized media. Consumables are critical for consistent assay performance and reproducibility across laboratories. Pharmaceutical and biotech companies prioritize high-quality consumables for drug screening. The segment benefits from the expansion of global research infrastructure and government funding. Increasing use in high-throughput screening supports large-scale adoption. Ready-to-use kits simplify workflows, reducing operational costs. Academic institutions and CROs rely heavily on consumables for routine research activities. Rising pharmaceutical R&D budgets and contract research outsourcing sustain growth. Integration with automated instruments enhances assay efficiency. Consumables support diverse applications in oncology, genetic disorders, and infectious disease research. The segment is favored for its standardized formats and global availability. Growing awareness of assay reproducibility and quality standards reinforces dominance.

The services segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, driven by outsourcing of assay execution, data analysis, and protocol optimization to specialized CROs and service providers. Pharmaceutical and biotechnology companies prefer services to reduce operational costs and accelerate timelines. Access to expert technical support ensures reliable outcomes. Integration with advanced technologies like high-content screening and flow cytometry enhances service offerings. Expansion of clinical trials and drug discovery programs globally boosts demand. Services support validation, customization, and training for laboratory personnel. Growing adoption of contract research for early-stage drug discovery accelerates segment growth. Development of specialized assay platforms and software-driven solutions promotes market penetration. Governments and private investors are funding collaborations for innovative therapeutic research. Emerging markets in Asia-Pacific and Latin America offer new growth opportunities. The rise of personalized medicine necessitates tailored assay services. Service providers leverage technology platforms for scalable and reproducible outputs.

- By Technology

On the basis of technology, the Cell Based Assays market is segmented into flow cytometry, high-throughput screening, high-content screening, and label-free detection. The flow cytometry segment dominated the largest market revenue share of 39.5% in 2025, due to its ability to provide rapid, quantitative, and multiparametric analysis of individual cells. The technology is widely adopted by pharmaceutical companies, CROs, and academic institutes. Flow cytometry is essential for immunophenotyping, drug screening, and apoptosis detection. Advances in automation, multi-laser systems, and software analytics enhance its capabilities. Its compatibility with cell-based assays and high reproducibility support global adoption. Robust data output facilitates decision-making in preclinical research. Integration with high-throughput workflows accelerates drug discovery. Regulatory approvals for automated platforms support adoption. Training programs and technical support by vendors enhance user confidence. The technology is preferred for hematology, oncology, and infectious disease research. Growing demand for personalized medicine and precision therapy reinforces segment growth.

High-content screening is expected to witness the fastest CAGR of 19.1% from 2026 to 2033, driven by rising demand for multiparametric cell analysis, phenotypic screening, and imaging-based drug discovery. Integration with AI and machine learning enables advanced data interpretation. Expansion in pharmaceutical and biotechnology R&D, CRO services, and academic research fuels adoption. Automated workflows and multiplexed assays enhance throughput and efficiency. Governments and private investors support the development of next-generation screening platforms. Emerging applications in gene therapy, regenerative medicine, and oncology increase market potential. Rising adoption in Asia-Pacific due to technological investments supports growth. Customizable assay platforms for diverse applications attract researchers. Software integration improves reproducibility and standardization. Partnerships between instrument manufacturers and service providers enhance adoption. High-content platforms enable real-time monitoring and live-cell imaging. Increasing demand for phenotypic screening in complex disease models accelerates growth.

- By Application

On the basis of application, the market is segmented into drug discovery, basic research, and others. The drug discovery segment dominated the largest market revenue share of 47.8% in 2025, due to extensive use in preclinical screening, lead identification, and toxicity studies. Pharmaceutical companies rely on cell-based assays for efficient evaluation of novel compounds. The segment benefits from the integration of high-throughput and high-content screening technologies. CROs provide outsourced drug discovery services to meet growing R&D demand. Government funding and private investment in drug development support market expansion. Advanced assay kits and automation platforms increase efficiency and reproducibility. Adoption in oncology, infectious disease, and genetic research drives utilization. Integration with computational tools enhances predictive modeling. Pharmaceutical pipelines in North America and Europe sustain dominance. Standardized protocols and regulatory compliance ensure global acceptance. Expansion of biopharma R&D in Asia-Pacific supports growth. Collaboration with academic and research institutions accelerates innovation.

The basic research segment is expected to witness the fastest CAGR of 16.7% from 2026 to 2033, fueled by increasing academic and institutional research activities. Growing interest in cell biology, immunology, and regenerative medicine promotes assay adoption. Emerging markets in Asia-Pacific and Latin America show rapid uptake. Funding by governments and private organizations accelerates experimental studies. Integration with flow cytometry, high-content screening, and imaging platforms enhances research capabilities. Multiparametric and label-free assays enable detailed cellular analysis. Adoption in gene editing, stem cell research, and toxicology studies supports growth. Collaboration with instrument manufacturers and software providers improves assay efficiency. Customizable assay platforms meet diverse research needs. Online training and technical support expand accessibility. Academic consortia and partnerships drive methodological innovations. Increasing publications and scientific validation promote global adoption.

- By End User

On the basis of end user, the market is segmented into pharmaceutical and biotechnology companies, CROs, academic and research institutions, government organizations, and others. The pharmaceutical and biotechnology companies segment dominated the largest market revenue share of 51.2% in 2025, due to high R&D investment, advanced infrastructure, and global operations. Companies leverage cell-based assays for preclinical screening, target validation, and translational research. Strong pipelines in oncology, infectious diseases, and genetic disorders reinforce adoption. Collaborations with CROs and academic institutions support research acceleration. Government grants and incentives further enhance utilization. Integration with automated instruments and software improves productivity. Global regulatory support for assay standardization encourages growth. Demand for reproducible and scalable results ensures segment dominance. Expansion into emerging markets fuels revenue growth. The segment benefits from technical expertise and high-throughput capabilities.

The CROs segment is expected to witness the fastest CAGR of 17.4% from 2026 to 2033, driven by increasing outsourcing of preclinical and translational research activities. CROs provide specialized expertise, advanced instruments, and global reach to pharmaceutical clients. Growing adoption of contract research for efficiency and cost reduction supports expansion. Integration with flow cytometry, high-content, and high-throughput platforms enhances service offerings. Increasing clinical research activities, particularly in Asia-Pacific, drive growth. CROs benefit from collaborations with academic and government institutions. Demand for customized assay services for complex disease models accelerates adoption. Use of AI and automation improves efficiency and reliability. Government policies supporting R&D outsourcing facilitate market penetration. Strategic partnerships and licensing agreements expand global reach. High demand in oncology, infectious diseases, and gene therapy research sustains growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct and indirect. The direct segment dominated the largest market revenue share of 55.1% in 2025, driven by strong relationships between assay manufacturers and end users. Direct sales facilitate customization, technical support, and timely delivery. Pharmaceutical and biotech companies prefer direct engagement for complex assay solutions. Contract research organizations also benefit from direct vendor interactions for technical guidance. Integration with service and instrument sales ensures comprehensive solutions. Global coverage by leading manufacturers supports market reach. Training and after-sales support enhance customer loyalty. Government and institutional procurement favors direct channels. Direct sales enable faster adoption of new technologies and assay innovations. Increasing complexity of assays necessitates direct engagement. Global expansion of manufacturers reinforces segment dominance.

The indirect segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2033, driven by growing use of distributors, resellers, and e-commerce platforms. Indirect channels expand accessibility to smaller laboratories and emerging markets. Distributors provide local support, inventory management, and technical assistance. Increasing penetration in Asia-Pacific and Latin America promotes adoption. Online marketplaces facilitate efficient procurement and cost-effectiveness. Academic institutions and small biotech firms increasingly rely on indirect channels. Integration of instruments, consumables, and software in bundled offerings enhances attractiveness. Indirect channels enable rapid expansion into new geographies. Partnerships between manufacturers and distributors improve reach. Growth of cloud-based ordering and digital platforms accelerates adoption. Indirect sales provide flexibility and reduce logistical challenges.

Cell Based Assays Market Regional Analysis

- North America dominated the cell based assays market with the largest revenue share of approximately 41.2% in 2025

- Driven by the presence of major pharmaceutical and biotechnology companies, advanced research infrastructure, and extensive government and private funding for biomedical research

- Key players such as Thermo Fisher Scientific, Bio-Rad Laboratories, and PerkinElmer are leading the adoption of innovative assay platforms, high-throughput screening systems, and automation solutions

U.S. Cell Based Assays Market Insight

The U.S. cell based assays market captured the largest revenue share of 82% in 2025 within North America. The market growth is fueled by increasing investments in drug discovery, biologics research, and personalized medicine. Leading companies such as Thermo Fisher Scientific, PerkinElmer, and Agilent Technologies have launched high-content and automated assay platforms, enabling faster and more accurate research outcomes. The growing integration of AI-driven data analysis and cloud-based laboratory information management systems (LIMS) is further enhancing efficiency in preclinical and clinical research.

Europe Cell Based Assays Market Insight

The Europe cell based assays market is projected to expand at a substantial CAGR of around 7.8% during the forecast period, primarily driven by increasing regulatory requirements, rising adoption of 3D cell culture models, and strong pharmaceutical and biotech R&D activity. Companies such as Merck KGaA, Lonza Group, and BioTek Instruments are providing advanced assay kits and automated solutions to meet the needs of both research institutions and contract research organizations (CROs).

U.K. Cell Based Assays Market Insight

The U.K. cell based assays market is expected to grow at a noteworthy CAGR of 8.2%, supported by rising home-grown biotech research, government funding initiatives, and increasing use of cell-based assays in drug toxicity and efficacy studies. Leading players like PerkinElmer and Bio-Rad Laboratories are expanding their offerings with multiplexed assays and high-throughput platforms to cater to this growing demand.

Germany Cell Based Assays Market Insight

Germany cell based assays market is anticipated to expand at a CAGR of approximately 7.5%, driven by its focus on innovation, digitalization of laboratories, and adoption of automated and standardized assay platforms. Companies such as Agilent Technologies and Thermo Fisher Scientific are introducing advanced solutions for reproducible and scalable cell-based assays, meeting both academic and industrial research demands.

Asia-Pacific Cell Based Assays Market Insight

The Asia-Pacific cell based assays market is expected to be the fastest-growing region, with a projected CAGR of 9.6% from 2026 to 2033. Growth is supported by increasing investment in R&D, expanding biotech and CRO infrastructure, and a rising number of clinical trials in China, India, and Japan. The presence of domestic companies such as Sino Biological and WuXi AppTec, combined with government initiatives promoting biotechnology and healthcare research, is accelerating market adoption.

Japan Cell Based Assays Market Insight

Japan’s cell based assays market growth is propelled by high-tech research facilities, increasing focus on regenerative medicine, and a rising number of smart laboratories. Companies such as Takara Bio and Sysmex Corporation are developing automated and high-content assay systems to support both academic and pharmaceutical research.

China Cell Based Assays Market Insight

China cell based assays market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, expanding clinical research, and growing adoption of high-throughput and automated assay platforms. Domestic players like WuXi AppTec and Sino Biological, alongside multinational companies, are increasing availability and affordability of cell-based assay solutions, contributing significantly to market expansion.

Cell Based Assays Market Share

The Cell Based Assays industry is primarily led by well-established companies, including:

• Thermo Fisher Scientific, Inc. (U.S.)

• Merck KGaA (Germany)

• PerkinElmer, Inc. (U.S.)

• BD (U.S.)

• Bio-Rad Laboratories, Inc. (U.S.)

• Agilent Technologies, Inc. (U.S.)

• Promega Corporation (U.S.)

• Lonza Group AG (Switzerland)

• GE Healthcare Life Sciences (U.K.)

• Horizon Discovery Group plc (U.K.)

• Takara Bio Inc. (Japan)

• Danaher Corporation (U.S.)

• Charles River Laboratories International, Inc. (U.S.)

• Sartorius AG (Germany)

• BD Biosciences (U.S.)

Latest Developments in Global Cell Based Assays Market

- In October 2023, Danaher Corporation announced a partnership with 10x Genomics to advance automation solutions for single‑cell assay workflows, strengthening capabilities in cell‑based assays and improving efficiency and precision in complex single‑cell research applications

- In May 2023, Axxam and Promega Corporation formalized an agreement to offer early‑stage drug discovery services that include customized luminescence‑based and cell‑based assays compatible with miniaturized high‑throughput screening formats, enhancing screening capacities for novel drug targets

- In April 2024, Becton Dickinson and Company launched the BD FACSDiscover S8 Cell Sorters, a new cell sorting solution that enhances researchers’ ability to conduct precise cell biology, immunology, and oncology cell‑based assays with improved resolution and performance

- In October 2024, PerkinElmer collaborated with academic institutions to co‑develop AI‑enabled assay kits tailored to neurodegenerative disease modeling using iPSC‑derived neuronal cells in high‑throughput screening formats, expanding applications for cell‑based assay platforms

- In December 2024, Bio‑Techne announced the expansion of its product portfolio with validated cell‑based assays targeting cytokine signaling and checkpoint inhibitor research, providing enhanced tools for immunotherapy development and signaling studies

- In January 2025, Eurofins DiscoverX launched a next‑generation GPCR screening solution that integrates advanced cell‑based assays with novel reporter constructs to improve receptor profiling accuracy across multiple therapeutic classes, supporting drug discovery across immunology and oncology

- In February 2025, Thermo Fisher Scientific announced an expansion of its cell‑based assay service offerings by introducing advanced 3D culture models and multiplex readout technologies designed to support complex drug efficacy testing and high‑content cellular profiling

- In March 2025, Sartorius introduced an upgraded Incucyte platform featuring enhanced image analytics and AI‑based analysis capabilities to accelerate high‑content screening for immuno‑oncology, regenerative medicine, and other cell‑based assays

- In July 2025, INDIGO Biosciences announced the expansion of its alternative species line with the launch of multiple luciferase‑based reporter assays for dog, rat, and pig receptors, enabling species‑specific translational screening and comparative pharmacology in drug development

- In June 2025, Agilent’s xCELLigence RTCA platform was leveraged to support potency assay development for a newly approved CAR‑T therapy, using real‑time, label‑free monitoring of cell behavior to validate therapeutic activity in clinical research settings and demonstrating advanced application of cell‑based assays in cutting‑edge therapies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.