Global Chemical Dust Suppressants Market

Market Size in USD Billion

CAGR :

%

USD

1.89 Billion

USD

2.81 Billion

2025

2033

USD

1.89 Billion

USD

2.81 Billion

2025

2033

| 2026 –2033 | |

| USD 1.89 Billion | |

| USD 2.81 Billion | |

| % | |

|

Chemical Dust Suppressants Market Size

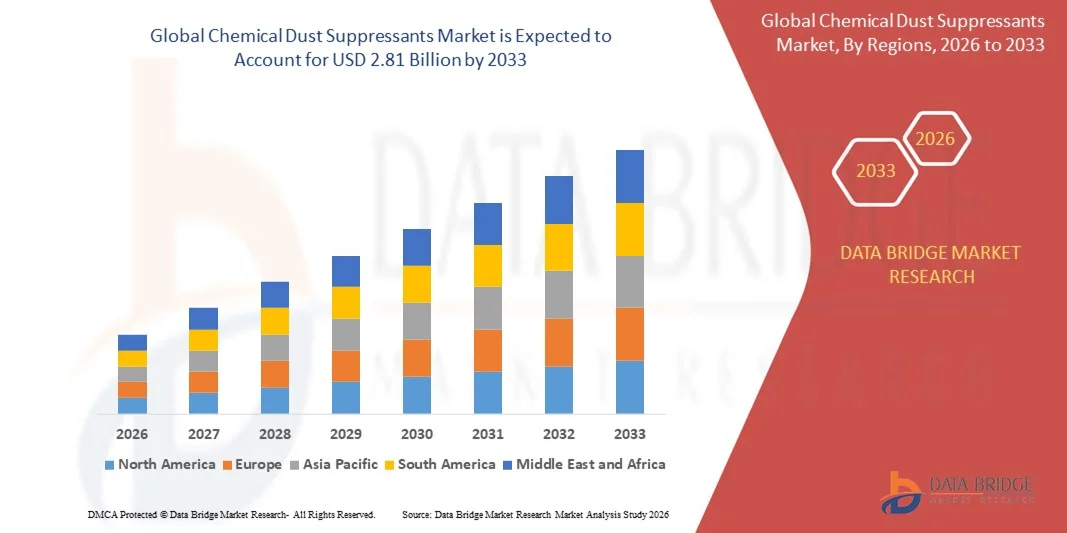

- The global chemical dust suppressants market size was valued at USD 1.89 billion in 2025 and is expected to reach USD 2.81 billion by 2033, at a CAGR of 5.10% during the forecast period

- The market growth is largely driven by increasing regulatory pressure to control airborne particulate emissions across mining, construction, and industrial operations, along with rising awareness of worker health and environmental safety. Expanding infrastructure development, large-scale mining activities, and industrial material handling requirements are intensifying the need for effective dust control solutions, thereby accelerating adoption of chemical dust suppressants

- Furthermore, the growing focus on operational efficiency, reduced water consumption, and long-lasting dust control performance is encouraging end users to shift from conventional methods to advanced chemical formulations. These combined factors are strengthening demand for chemical dust suppressants and supporting sustained market expansion

Chemical Dust Suppressants Market Analysis

- Chemical dust suppressants are specialized formulations applied to control and reduce airborne dust generated during mining, construction, road maintenance, and industrial material handling activities. These products work by binding dust particles or retaining moisture, helping industries comply with environmental regulations while improving workplace safety and visibility

- The rising demand for chemical dust suppressants is primarily fueled by rapid urbanization, expanding mining output, stricter air quality standards, and increasing emphasis on sustainable and efficient dust control practices across industrial sectors

- Asia-Pacific dominated the chemical dust suppressants market with a share of 47.5% in 2025, due to rapid infrastructure development, extensive mining activities, and large-scale construction projects across emerging economies

- North America is expected to be the fastest growing region in the chemical dust suppressants market during the forecast period due to rising mining investments, expanding construction activities, and strict enforcement of environmental and occupational safety regulations

- Wet type dust suppressant segment dominated the market with a market share of 58.5% in 2025, due to its high effectiveness in binding fine dust particles and providing immediate dust control across large operational areas. Wet suppressants are widely preferred in mining and construction sites due to their ease of application through spraying systems and their ability to reduce airborne particulate matter efficiently

Report Scope and Chemical Dust Suppressants Market Segmentation

|

Attributes |

Chemical Dust Suppressants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Chemical Dust Suppressants Market Trends

Shift Toward Eco-Friendly Dust Suppressant Formulations

- A key trend in the chemical dust suppressants market is the increasing shift toward eco-friendly and biodegradable formulations, driven by rising environmental concerns and stricter air quality regulations across mining, construction, and industrial sectors. End users are prioritizing solutions that effectively control dust while minimizing soil contamination, water pollution, and long-term ecological impact

- For instance, Benetech Inc. has expanded the adoption of its biodegradable dust control solutions across mining and bulk material handling operations to help clients meet environmental compliance requirements. Such products support sustainable operations while maintaining high dust suppression efficiency in large-scale industrial environments

- The demand for plant-based, polymer, and non-toxic chemical suppressants is increasing as industries seek alternatives to traditional salt-based products that can cause corrosion and environmental degradation. This transition is encouraging manufacturers to invest in greener chemistry and advanced formulation technologies

- Mining companies are increasingly integrating environmentally responsible dust suppressants into haul road management and material transfer points to reduce particulate emissions without increasing water consumption. This trend aligns with broader sustainability goals adopted by major mining operators worldwide

- Construction and infrastructure projects are also adopting eco-friendly dust suppressants to comply with urban air quality norms and community health standards. The emphasis on sustainable construction practices is strengthening the long-term relevance of environmentally safe dust control chemicals

- Overall, the shift toward eco-friendly formulations is reinforcing innovation in the chemical dust suppressants market and supporting wider acceptance of sustainable dust management solutions across regulated industrial sectors

Chemical Dust Suppressants Market Dynamics

Driver

Stringent Safety Regulations on Dust Emissions

- Stringent occupational safety and environmental regulations governing dust emissions are a major driver of growth in the chemical dust suppressants market. Regulatory bodies are enforcing strict limits on airborne particulate matter to protect worker health and reduce environmental pollution in mining, construction, and industrial operations

- For instance, regulatory standards enforced by organizations such as the U.S. Occupational Safety and Health Administration (OSHA) have compelled mining and construction companies to adopt effective dust control measures. Compliance with these standards has increased reliance on chemical dust suppressants to manage respirable dust levels

- Government agencies across Europe and Asia-Pacific are strengthening air quality regulations, particularly around large infrastructure and mining projects, which is accelerating adoption of chemical dust suppression solutions. These regulations require continuous dust mitigation across operational sites

- Industrial operators are increasingly implementing dust suppression programs to avoid penalties, operational shutdowns, and reputational risks associated with non-compliance. Chemical dust suppressants provide a reliable and scalable solution to meet regulatory thresholds

- Collectively, stringent dust emission regulations are driving sustained investment in chemical dust suppressants and positioning them as essential compliance tools for industrial and infrastructure-heavy sectors

Restraint/Challenge

High Cost of Advanced Suppressants

- The chemical dust suppressants market faces challenges due to the high cost associated with advanced and specialty suppressant formulations, particularly polymer-based and environmentally friendly products. These solutions often require complex formulation processes and higher-grade raw materials, increasing overall cost structures

- For instance, Cypher Environmental offers high-performance polymer dust suppressants designed for long-term road stabilization and dust control, but such products typically involve higher upfront costs compared to conventional water-based methods. This can limit adoption among cost-sensitive operators

- Smaller mining and construction companies often face budget constraints that restrict their ability to invest in premium dust suppression chemicals. As a result, some operators continue to rely on less effective short-term solutions despite regulatory pressure

- The application and maintenance requirements of advanced chemical suppressants may also involve specialized equipment and skilled labor, further increasing operational expenses. These factors can slow adoption in developing regions

- Overall, the high cost of advanced chemical dust suppressants remains a key restraint, particularly in emerging markets, where balancing regulatory compliance with operational affordability continues to be a critical challenge

Chemical Dust Suppressants Market Scope

The market is segmented on the basis of nature, type, and end-use.

- By Nature

On the basis of nature, the chemical dust suppressants market is segmented into dry type dust suppressant and wet type dust suppressant. The wet type dust suppressant segment dominated the largest market revenue share of 58.5% in 2025, driven by its high effectiveness in binding fine dust particles and providing immediate dust control across large operational areas. Wet suppressants are widely preferred in mining and construction sites due to their ease of application through spraying systems and their ability to reduce airborne particulate matter efficiently. Their compatibility with water-based operations and lower risk of re-suspension further supports their strong adoption. In addition, regulatory emphasis on workplace safety and air quality control has reinforced demand for wet-type solutions in heavy-duty applications.

The dry type dust suppressant segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by rising adoption in regions facing water scarcity and strict water usage regulations. Dry suppressants offer longer-lasting dust control and reduced maintenance requirements compared to conventional wet methods. Their suitability for remote mining locations and unpaved roads, where water availability is limited, is driving increased interest. Advancements in formulation technology are also improving their efficiency and environmental compatibility, accelerating market growth.

- By Type

On the basis of type, the chemical dust suppressants market is segmented into polymer emulsions, hygroscopic salts, and others. The polymer emulsions segment accounted for the largest market revenue share in 2025, owing to their strong binding properties and ability to form durable crusts on dust-prone surfaces. These suppressants are extensively used in mining haul roads and construction sites due to their long service life and resistance to traffic and weather conditions. Their effectiveness in reducing particulate emissions over extended periods makes them a cost-efficient solution for large-scale industrial operations. Growing investments in infrastructure development have further strengthened demand for polymer-based dust suppressants.

The hygroscopic salts segment is expected to register the fastest growth during the forecast period, driven by their ability to attract and retain moisture from the air, ensuring continuous dust suppression. These salts are widely adopted for unpaved roads and material handling areas due to their relatively low cost and ease of application. Increasing use in developing economies, where cost sensitivity is high, supports segment growth. Improvements in product formulations to reduce corrosion and environmental impact are also enhancing their acceptance across multiple end-use industries.

- By End-Use

On the basis of end-use, the chemical dust suppressants market is segmented into mining, construction, chemical & pharmaceuticals, metal extraction, industrial materials, rock production, and others. The mining segment dominated the market revenue share in 2025, driven by the extensive need to control dust emissions from drilling, blasting, and haul road activities. Strict occupational health and environmental regulations have compelled mining operators to adopt advanced dust suppression solutions. The large scale of mining operations and continuous exposure to dust make chemical suppressants essential for operational safety and regulatory compliance. Sustained global demand for minerals and metals continues to support strong consumption in this segment.

The construction segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by rapid urbanization and expanding infrastructure projects worldwide. Construction activities generate significant dust during earthmoving, demolition, and material handling processes, increasing the need for effective suppression solutions. Growing enforcement of air quality standards in urban areas is accelerating adoption. The flexibility of chemical dust suppressants across different construction environments further contributes to their rising use in this end-use segment.

Chemical Dust Suppressants Market Regional Analysis

- Asia-Pacific dominated the chemical dust suppressants market with the largest revenue share of 47.5% in 2025, driven by rapid infrastructure development, extensive mining activities, and large-scale construction projects across emerging economies

- High demand for dust control solutions in mining haul roads, construction sites, and industrial material handling, along with cost-effective production and availability of raw materials, is accelerating regional market growth

- Stringent environmental regulations related to air quality, rising awareness of worker safety, and increasing government investments in transportation and urban infrastructure are supporting sustained consumption of chemical dust suppressants

China Chemical Dust Suppressants Market Insight

China held the largest share in the Asia-Pacific chemical dust suppressants market in 2025, supported by its dominant mining sector, large construction industry, and extensive industrial manufacturing base. Strong government enforcement of dust emission norms, particularly in mining and urban construction zones, is driving adoption. Continuous infrastructure expansion and large-scale road and rail projects further reinforce market demand.

India Chemical Dust Suppressants Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rapid urbanization, increasing mining output, and accelerating infrastructure development under national programs. Growing regulatory focus on particulate matter control and occupational safety is encouraging the use of chemical dust suppressants. Expansion of road construction, stone quarrying, and industrial materials handling is contributing to strong market momentum.

Europe Chemical Dust Suppressants Market Insight

The Europe chemical dust suppressants market is growing steadily, supported by strict environmental regulations, strong emphasis on workplace safety, and widespread adoption of sustainable dust control practices. Demand is driven by construction, metal extraction, and industrial material processing activities. The region’s focus on eco-friendly and biodegradable suppressant formulations is shaping product adoption trends.

Germany Chemical Dust Suppressants Market Insight

Germany’s market growth is driven by its advanced construction sector, strong industrial base, and stringent air quality regulations. The country emphasizes compliance with environmental standards, leading to consistent demand for high-performance dust suppressants. Adoption is particularly strong in industrial materials handling, metal extraction, and large-scale infrastructure maintenance projects.

U.K. Chemical Dust Suppressants Market Insight

The U.K. market is supported by infrastructure refurbishment activities, growing construction output, and increasing regulatory scrutiny on dust emissions at work sites. Rising focus on urban air quality management and worker health is strengthening demand. Use of chemical dust suppressants is expanding across construction, demolition, and road maintenance applications.

North America Chemical Dust Suppressants Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising mining investments, expanding construction activities, and strict enforcement of environmental and occupational safety regulations. Increased adoption of advanced dust control solutions in haul roads and industrial sites is boosting demand. Focus on operational efficiency and regulatory compliance continues to support market expansion.

U.S. Chemical Dust Suppressants Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its extensive mining operations, large construction sector, and well-established industrial materials industry. Strong regulatory frameworks governing particulate emissions and worker safety are key demand drivers. Ongoing investments in infrastructure development and industrial modernization further strengthen the U.S. market position.

Chemical Dust Suppressants Market Share

The chemical dust suppressants industry is primarily led by well-established companies, including:

- BASF SE (Germany)

- Quaker Houghton (U.S.)

- Benetech Inc. (U.S.)

- Alumichem A/S (Denmark)

- Cypher Environmental (Canada)

- FUCHS (Germany)

- Hexion Inc. (U.S.)

- Dow (U.S.)

- Camfil (Sweden)

- Tecpro Systems Ltd. (India)

- Ecolab Inc. (U.S.)

- Cargill, Incorporated (U.S.)

- Chemtex Speciality Limited (India)

- Dust Solutions, Inc. (U.S.)

- Donaldson Company, Inc. (U.S.)

- I-CAT Environmental Solutions (U.K.)

- ADW (U.S.)

- CHEMIKA (Switzerland)

- Rare Track Speciality Product LLP (India)

- Celanese Corporation (U.S.)

- Accéntuate Ltd (U.K.)

Latest Developments in Global Chemical Dust Suppressants Market

- In September 2024, Donaldson Company expanded its manufacturing facility in Johor, Malaysia, strengthening its production capacity for industrial dust control and suppression solutions. This expansion supports rising demand from mining and construction sectors in Asia-Pacific and enhances Donaldson’s ability to serve large-scale industrial clients, reinforcing competitive intensity in the chemical dust suppressants and control market

- In July 2024, Spraying Systems Co. entered into a partnership with Rio Tinto to develop customized, water-efficient dust suppression solutions for iron ore mining operations in Western Australia. This collaboration addresses critical challenges related to water scarcity and regulatory compliance, setting a benchmark for sustainable dust suppression practices in large mining operations and influencing broader market adoption of advanced spray-based chemical suppressants

- In May 2024, Camfil AB introduced its CamCarb XG activated carbon filtration system aimed at enhancing dust and contaminant control in chemical processing environments. The launch expands Camfil’s portfolio beyond conventional dust capture by integrating particulate and chemical control, supporting demand for high-performance suppression solutions in regulated industrial settings and specialty manufacturing

- In March 2024, Nederman Holding AB completed the acquisition of Dust Solutions Inc., expanding its footprint in the North American dust suppression market. This acquisition strengthens Nederman’s mobile and site-based dust control offerings for construction and demolition activities, increasing consolidation in the market and improving access to integrated chemical dust suppressant solutions

- In January 2024, Quaker Chemical Corporation launched its DUSTLOCK polymer-based dust suppressant designed specifically for coal mining applications. The product introduction addresses the need for longer-lasting suppression with reduced water usage, supporting efficiency improvements in mining operations and driving innovation toward high-performance, polymer-based chemical dust suppressants

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Chemical Dust Suppressants Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Chemical Dust Suppressants Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Chemical Dust Suppressants Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.