Global Clad Pipe Market

Market Size in USD Billion

CAGR :

%

USD

4.89 Billion

USD

7.44 Billion

2025

2033

USD

4.89 Billion

USD

7.44 Billion

2025

2033

| 2026 –2033 | |

| USD 4.89 Billion | |

| USD 7.44 Billion | |

| % | |

|

Clad Pipe Market Size

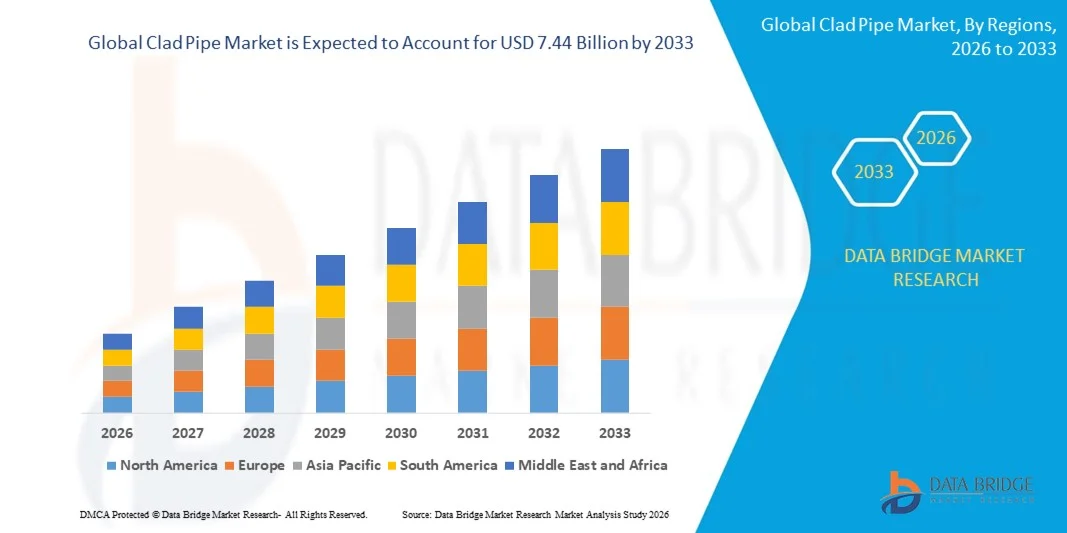

- The global clad pipe market size was valued at USD 4.89 billion in 2025 and is expected to reach USD 7.44 billion by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by increasing industrialization across oil & gas, chemical, and power sectors, leading to higher demand for corrosion-resistant, high-strength, and durable piping solutions for critical infrastructure projects

- Furthermore, growing investments in energy, petrochemical, and water treatment projects are driving the adoption of clad pipes, as industries seek long-term operational reliability and reduced maintenance costs. These converging factors are accelerating the uptake of advanced clad pipe solutions, thereby significantly boosting the industry’s growth

Clad Pipe Market Analysis

- Clad pipes, offering corrosion-resistant and mechanically robust solutions for transporting aggressive fluids and handling high pressures, are becoming essential components in energy, chemical, and industrial applications due to their long service life and structural integrity

- The escalating demand for clad pipes is primarily fueled by the need for safe, high-performance pipelines in offshore and onshore oil & gas, chemical plants, and power generation facilities, alongside increasing regulatory standards for industrial safety and infrastructure reliability

- North America dominated the clad pipe market with a share of over 42% in 2025, due to extensive industrialization, mature oil & gas and chemical sectors, and increasing investments in infrastructure modernization

- Asia-Pacific is expected to be the fastest growing region in the clad pipe market during the forecast period due to rapid industrialization, expanding oil & gas and chemical industries, and rising infrastructure development in countries such as China, Japan, and India

- Metallurgical bonded segment dominated the market with a market share of 46.1% in 2025, due to its superior corrosion resistance and excellent mechanical strength. Industries such as oil & gas and chemical processing prefer metallurgical bonded pipes for transporting aggressive chemicals and high-temperature fluids due to their long service life and minimal maintenance requirements

Report Scope and Clad Pipe Market Segmentation

|

Attributes |

Clad Pipe Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Clad Pipe Market Trends

Rising Use of Metallurgical Bonded and Weld Overlay Pipes

- A significant trend in the clad pipe market is the increasing adoption of metallurgical bonded and weld overlay pipes, driven by their superior resistance to corrosion, erosion, and high-temperature environments. This trend is elevating the role of clad pipes as essential solutions for industries requiring durable and high-performance piping systems

- For instance, Vallourec and Tenaris supply a wide range of clad pipes with advanced welding and metallurgical bonding techniques that are widely used in oil & gas, chemical, and power projects. Such pipes enhance operational safety, extend service life, and reduce maintenance requirements in challenging industrial applications

- The oil & gas sector is increasingly relying on clad pipes for onshore and offshore pipelines where conventional materials fail to withstand aggressive corrosive media. This is positioning clad pipes as critical infrastructure components for deepwater and high-pressure environments

- The chemical processing industry is adopting clad pipes to transport highly corrosive chemicals and acids, where resistance to pitting and cracking is vital. The use of these pipes ensures compliance with safety standards and minimizes downtime due to pipe degradation

- Power generation facilities are integrating clad pipes in boilers, heat exchangers, and condensers to manage high-temperature and high-pressure fluids efficiently. This integration supports longer operational cycles and reduces replacement frequency, thereby optimizing overall plant performance

- Industries focusing on water treatment, desalination, and industrial manufacturing are expanding their use of clad pipes to handle abrasive slurries and harsh chemical environments. This rising incorporation reinforces the importance of clad pipes in ensuring process reliability, minimizing leaks, and sustaining industrial productivity

Clad Pipe Market Dynamics

Driver

Expansion of Oil & Gas, Chemical, and Power Sectors

- The rapid expansion of oil & gas, chemical, and power sectors worldwide is driving demand for clad pipes that offer enhanced durability and corrosion resistance. These sectors require piping solutions capable of withstanding aggressive process conditions and ensuring long-term operational stability

- For instance, Baker Hughes provides clad pipes for offshore oil & gas projects that operate under extreme pressure and temperature conditions. These solutions enable energy companies to maintain uninterrupted operations and reduce the risk of failures in critical pipelines

- Increasing investments in new chemical plants and refineries are creating demand for high-quality clad piping systems that can handle corrosive and high-temperature fluids efficiently. This is pushing manufacturers to innovate advanced bonding and overlay techniques to meet stringent industrial standards

- The growth of power generation projects, particularly in regions focusing on thermal and nuclear energy, is fueling the need for pipes that sustain high-pressure and heat-intensive processes. Clad pipes ensure safe transfer of steam and water, protecting equipment and reducing maintenance overheads

- Rising global energy demand and industrial expansion continue to drive the adoption of clad pipes. The need for robust, long-lasting, and maintenance-efficient piping systems is positioning clad pipes as critical enablers of industrial growth

Restraint/Challenge

High Manufacturing and Installation Costs

- The clad pipe market faces challenges due to the high costs associated with manufacturing and installing metallurgical bonded and weld overlay pipes. Specialized processes, advanced materials, and skilled labor requirements contribute to elevated production expenses

- For instance, Tenaris invests heavily in automated welding lines and quality assurance systems to produce clad pipes for high-specification projects. These advanced operations increase capital expenditure and raise the overall cost per unit, limiting broader adoption in cost-sensitive projects

- The complex fabrication techniques required to bond dissimilar metals or apply corrosion-resistant overlays demand precise control and quality inspections. These factors lengthen production timelines and further add to operational costs

- Transportation, handling, and installation of heavy clad pipes in industrial facilities require specialized equipment and trained personnel, which increases project execution costs. These logistical challenges impact smaller-scale projects and regional installations

- Market growth is constrained by the difficulty of scaling high-quality production while maintaining competitive pricing. Manufacturers must balance cost, quality, and performance to meet increasing industrial demand while sustaining profitability

Clad Pipe Market Scope

The market is segmented on the basis of pipe type, grade, outer diameter, and wall thickness.

- By Pipe Type

On the basis of pipe type, the Clad Pipe market is segmented into metallurgical bonded, mechanically lined, and weld overlay. The metallurgical bonded segment dominated the market with the largest revenue share of 46.1% in 2025, driven by its superior corrosion resistance and excellent mechanical strength. Industries such as oil & gas and chemical processing prefer metallurgical bonded pipes for transporting aggressive chemicals and high-temperature fluids due to their long service life and minimal maintenance requirements. The strong market demand is further supported by advancements in bonding technology that enhance the structural integrity and reliability of these pipes. Metallurgical bonded pipes are also compatible with a wide range of industrial standards, making them a preferred choice for critical applications.

The mechanically lined segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing use in water treatment, pulp & paper, and power generation industries. For instance, companies such as Sandvik have developed mechanically lined clad pipes with improved erosion and corrosion resistance, offering cost-effective solutions for large-scale industrial applications. Their modular manufacturing and repair-friendly design make them increasingly popular among end users. The demand is also supported by growing industrial investments in regions with high chemical processing activity.

- By Grade

On the basis of grade, the Clad Pipe market is segmented into 316, 625, 825, and others. The 625 grade segment held the largest market revenue share in 2025 due to its exceptional high-temperature strength and corrosion resistance, particularly in harsh environments such as offshore oil & gas operations. Industries prioritize grade 625 for critical pipelines that handle sour gas, seawater, and highly corrosive chemicals, reducing the risk of failures and operational downtime. The widespread availability of this grade from established suppliers also supports its market dominance. Its compatibility with welding and fabrication processes further enhances its adoption across industrial sectors.

The 825 grade segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its superior resistance to oxidizing acids and enhanced mechanical properties. For instance, Nippon Steel has expanded production of grade 825 clad pipes to cater to increasing demand in the chemical and petrochemical industries. The growth is supported by rising industrialization in Asia-Pacific, where complex chemical processes require high-performance materials. In addition, the ability of grade 825 pipes to withstand extreme operating conditions without compromising safety or efficiency makes them a preferred choice for new installations.

- By Outer Diameter

On the basis of outer diameter, the Clad Pipe market is segmented into 4–12 inch, 12–24 inch, 24–48 inch, 48–60 inch, and 60–120 inch. The 24–48 inch segment dominated the market with the largest revenue share in 2025, driven by its extensive use in mid- to large-scale industrial pipelines and offshore projects. These sizes are preferred for transporting hydrocarbons, chemicals, and high-pressure steam due to their optimal balance between flow capacity and installation feasibility. The widespread adoption is also supported by international standards that favor these diameters for industrial and utility pipelines. The availability of customized sizes within this range further increases its attractiveness to engineers and project planners.

The 48–60 inch segment is projected to witness the fastest growth from 2026 to 2033, fueled by increasing investments in large-scale energy and water infrastructure projects. For instance, Tenaris has supplied 48–60 inch clad pipes for several high-pressure oil pipelines in the U.S. and Middle East, demonstrating strong industrial adoption. The growth is further driven by expanding pipeline networks requiring high-capacity flow systems capable of reducing friction losses and improving operational efficiency.

- By Wall Thickness

On the basis of wall thickness, the Clad Pipe market is segmented into 3–6 mm, 6–18 mm, 18–36 mm, 36–60 mm, and 60–120 mm. The 18–36 mm segment dominated the market with the largest revenue share in 2025, attributed to its wide applicability in chemical, power, and oil & gas industries. This wall thickness provides an ideal balance between pressure tolerance and material cost, enabling long-term reliability under high-stress operating conditions. Industries prefer this thickness for pipelines transporting corrosive fluids, where mechanical strength and durability are critical. The segment’s dominance is supported by consistent demand from mature markets in North America and Europe, where infrastructure standards favor this specification.

The 36–60 mm segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing use in high-pressure and deepwater applications. For instance, Vallourec has supplied 36–60 mm thick clad pipes for offshore oil fields, where high structural integrity is crucial under extreme environmental conditions. The segment’s growth is further supported by rising industrial safety regulations and the need for enhanced corrosion resistance, encouraging the adoption of thicker-walled pipes in new projects.

Clad Pipe Market Regional Analysis

- North America dominated the clad pipe market with the largest revenue share of over 42% in 2025, driven by extensive industrialization, mature oil & gas and chemical sectors, and increasing investments in infrastructure modernization

- Consumers and industries in the region highly value the reliability, corrosion resistance, and long-term durability offered by clad pipes for critical applications such as offshore pipelines, power plants, and chemical processing units

- This widespread adoption is further supported by stringent safety standards, technological advancements in bonding and overlay techniques, and strong demand from industrial maintenance and retrofit projects, establishing clad pipes as a preferred solution in the region

U.S. Clad Pipe Market Insight

The U.S. clad pipe market captured the largest revenue share in North America in 2025, fueled by the demand for high-performance pipelines in the oil & gas, chemical, and energy sectors. The adoption of metallurgical bonded and weld overlay pipes is increasing due to their resistance to corrosion, high-pressure tolerance, and ability to transport aggressive fluids safely. Government regulations and industrial standards promoting long-term infrastructure reliability further boost market growth. In addition, investments in pipeline expansions, refinery upgrades, and petrochemical facilities are driving the preference for advanced clad pipe solutions.

Europe Clad Pipe Market Insight

The Europe clad pipe market is projected to expand at a substantial CAGR during the forecast period, primarily driven by rising industrialization, strict environmental and safety regulations, and the need for corrosion-resistant and high-strength piping solutions. Countries such as Germany, France, and Italy are witnessing increased adoption of clad pipes in chemical processing, power generation, and offshore applications. European industries prioritize durability and long service life, encouraging the use of metallurgical bonded and weld overlay pipes. The integration of clad pipes into both new installations and retrofitting projects further supports growth across the region.

U.K. Clad Pipe Market Insight

The U.K. clad pipe market is expected to grow at a noteworthy CAGR during the forecast period, driven by demand in oil & gas, power plants, and chemical industries. Industrial operators in the region are increasingly prioritizing corrosion resistance, high-pressure handling, and reduced maintenance costs, making clad pipes an attractive solution. The U.K.’s industrial modernization initiatives and growing infrastructure projects continue to stimulate demand for high-performance piping solutions such as weld overlay and mechanically lined pipes.

Germany Clad Pipe Market Insight

The Germany clad pipe market is anticipated to expand at a considerable CAGR, fueled by increasing industrial automation, energy sector growth, and stringent safety and quality standards. German industries prefer metallurgical bonded and weld overlay pipes for chemical, power, and petrochemical applications requiring high reliability. The emphasis on long-term durability, operational efficiency, and eco-friendly materials supports the adoption of clad pipes in both manufacturing and construction sectors.

Asia-Pacific Clad Pipe Market Insight

The Asia-Pacific clad pipe market is poised to grow at the fastest CAGR during 2026–2033, driven by rapid industrialization, expanding oil & gas and chemical industries, and rising infrastructure development in countries such as China, Japan, and India. The region’s focus on smart manufacturing, energy efficiency, and industrial modernization is encouraging the adoption of clad pipes. Furthermore, APAC’s emergence as a manufacturing hub for clad pipe components and systems is increasing affordability and accessibility, enabling widespread usage across residential, commercial, and industrial sectors.

Japan Clad Pipe Market Insight

The Japan clad pipe market is gaining momentum due to the country’s advanced manufacturing sector, emphasis on high-quality materials, and energy infrastructure upgrades. The Japanese market emphasizes corrosion resistance, operational safety, and long service life, driving the adoption of metallurgical bonded and mechanically lined pipes. Industrial modernization and integration of high-performance piping solutions in power plants and chemical facilities are fueling growth.

China Clad Pipe Market Insight

The China clad pipe market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, industrial expansion, and growing demand in oil & gas, chemical, and power generation sectors. The country is witnessing high adoption of metallurgical bonded and weld overlay pipes due to their durability, cost-effectiveness, and compatibility with large-scale industrial projects. Government initiatives supporting infrastructure development and industrial safety, along with strong domestic manufacturers, are key factors propelling the market in China.

Clad Pipe Market Share

The clad pipe industry is primarily led by well-established companies, including:

- Japan Steel Works, LTD. (Japan)

- NobelClad (U.S.)

- FTV Proclad International Ltd (U.K.)

- Inox Tech (India)

- Tenaris (Luxembourg)

- Eisenbau Krämer GmbH (Germany)

- EEW GROUP (Germany)

- IODS Pipeclad (U.S.)

- H. Butting GmbH & Co. KG (Germany)

- Cladtek Holdings Pte Ltd. (Singapore)

- Gieminox Tectubi Raccordi (Italy)

- Canadoil Forge Ltd. (Canada)

- Jiuli Group Co., Ltd. (China)

- Precision Castparts Corp. (U.S.)

- Guangzhou Pearl River Petroleum Steel Pipe Co., Ltd (China)

Latest Developments in Global Clad Pipe Market

- In November 2025, BUTTING Group expanded its global footprint by establishing a new North American headquarters and its first U.S. clad pipe production facility in Loxley, Alabama, aimed at improving supply responsiveness and reducing lead times for energy, chemical, and industrial sectors. This strategic move allows the company to deliver high-performance clad pipes locally, meeting the growing demand for corrosion-resistant and durable solutions. The facility enhances operational efficiency for industries relying on long-life pipelines, such as oil & gas and chemical processing. By localizing production, BUTTING can also better customize products to regional standards and industrial requirements. This expansion strengthens the company’s competitive position in North America and reinforces its global growth strategy

- In May 2025, NobelClad launched next-generation explosion-bonded clad plates tailored for subsea pipeline applications, offering superior corrosion resistance and extended service life under harsh deepwater conditions. These plates provide operators with safer, more reliable pipelines capable of withstanding high pressures, aggressive chemicals, and saline environments. The innovation supports the expansion of offshore oil & gas and subsea energy infrastructure. With enhanced bonding technology, these clad plates reduce the risk of operational failures and maintenance downtime. The launch reflects a market trend towards high-performance, long-lasting materials that optimize safety, efficiency, and cost-effectiveness in challenging industrial applications

- In March 2025, JSW Steel upgraded its clad pipe manufacturing capabilities to enhance bonding strength, production efficiency, and overall quality for high-demand energy infrastructure projects, enabling the production of mechanically robust and reliable pipes for critical applications. These improvements meet the rigorous standards of offshore oil & gas, chemical, and power sectors where corrosion resistance and high-pressure handling are vital. The manufacturing upgrade also increases output and reduces production lead times, improving market responsiveness. By strengthening the mechanical integrity of clad pipes, JSW supports longer service life, reduced operational risks, and higher adoption in large-scale projects. This initiative positions the company as a key provider of advanced piping solutions in the global market

- In February 2025, BUTTING Group introduced enhanced mechanically lined clad pipes designed specifically for chemical plants handling corrosive media under elevated pressure conditions, ensuring greater resistance to chemical attack and improved operational reliability. These pipes enable continuous industrial operations with minimal maintenance and reduced downtime. By addressing high-pressure and aggressive chemical conditions, the innovation meets the exacting demands of modern chemical and petrochemical facilities. The mechanically lined pipes are expected to see rapid adoption due to their cost-efficiency and long service life. This development reinforces BUTTING’s role as a provider of specialized, high-performance piping solutions for challenging industrial environments

- In January 2025, JSW Steel implemented strategic upgrades to its clad pipe manufacturing processes focused on improving bonding strength, production efficiency, and product quality for high-demand energy infrastructure projects, allowing the company to deliver highly durable, reliable piping solutions. The upgrades meet the increasing industrial demand for corrosion-resistant and high-strength materials in offshore and onshore oil & gas pipelines, as well as chemical and power plant applications. Enhanced production capabilities also enable JSW to meet tighter delivery schedules while maintaining strict quality standards. This initiative supports extended service life, reduces failure risks, and provides clients with operational efficiency benefits. The upgrade further strengthens JSW’s competitive edge in the global clad pipe market and expands its market share in critical industrial sectors

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Clad Pipe Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Clad Pipe Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Clad Pipe Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.