Global Clinical Oncology Next Generation Sequencing Market

Market Size in USD Billion

USD

1.04 Billion

USD

3.20 Billion

2025

2033

USD

1.04 Billion

USD

3.20 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.04 Billion | |

| USD 3.20 Billion | |

| % | |

|

Clinical Oncology Next Generation Sequencing Market Overview

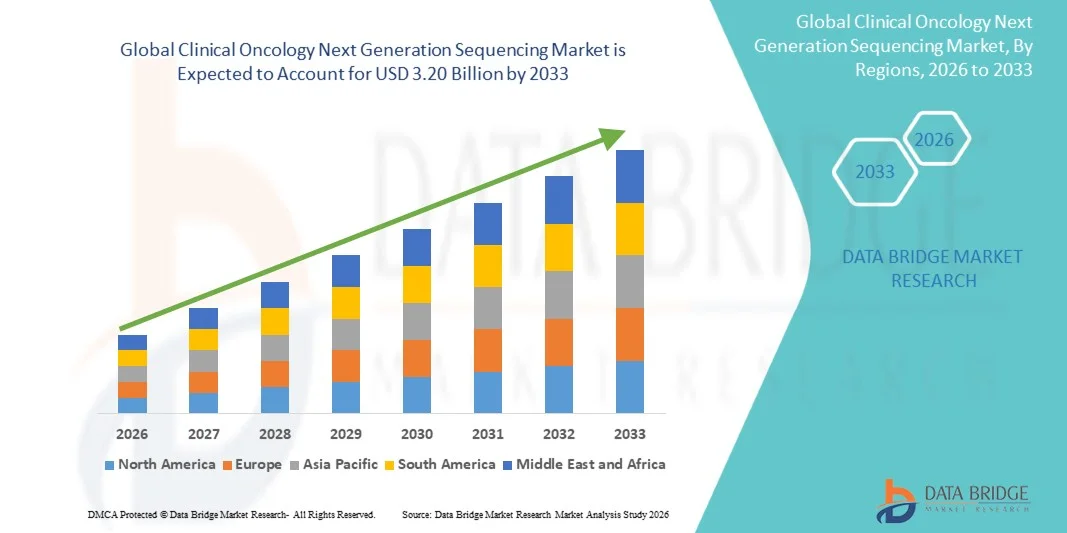

The Clinical Oncology Next Generation Sequencing Market was valued at USD 1.04 billion in 2025 and is projected to reach USD 3.20 billion by 2033, growing at a CAGR of 15.10% from 2026 to 2033. The market is experiencing strong growth driven by the increasing adoption of precision oncology approaches, rapid advancements in next-generation sequencing (NGS) technologies, and the growing demand for personalized cancer diagnostics and treatment strategies. Rising cancer prevalence globally and the need for early, accurate tumor profiling are accelerating the use of NGS-based clinical oncology solutions across healthcare systems.

The increasing integration of genomic sequencing into routine clinical oncology practice, combined with declining sequencing costs and improved bioinformatics capabilities, is enabling widespread adoption of NGS platforms. Hospitals, cancer research institutes, and diagnostic laboratories are increasingly utilizing NGS for tumor mutation profiling, liquid biopsy analysis, and biomarker discovery. In addition, expanding applications in targeted therapy selection, immuno-oncology, and minimal residual disease (MRD) detection are further driving market expansion. Growing government initiatives supporting precision medicine programs and large-scale cancer genomics projects are also contributing to the rapid growth of the Clinical Oncology Next Generation Sequencing Market.

Key Market Trends & Insights

- North America dominated the Clinical Oncology Next Generation Sequencing Market with the largest revenue share of 39.62% in 2025, supported by advanced genomic research infrastructure, strong investments in precision oncology, widespread adoption of next-generation sequencing (NGS) technologies, and the presence of leading biotechnology and pharmaceutical companies.

- The Companion Diagnostics segment dominated the market with a share of 48.15% in 2025, driven by strong integration of NGS in targeted therapy development and precision oncology treatment selection.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 11.3% from 2026 to 2033, fueled by expanding cancer diagnostics infrastructure, increasing healthcare investments, rising adoption of precision medicine, and growing genomic research activities across China, India, Japan, and South Korea.

- The NGS Data Analysis workflow segment is the fastest-growing category, projected to register a CAGR of 11.8%, reflecting rising demand for bioinformatics platforms, AI-driven genomic interpretation, and cloud-based sequencing data processing solutions.

- The Companion Diagnostics application segment dominates the market with a 41.27% revenue share in 2025, supported by increasing use of genomic testing for therapy selection, personalized cancer treatment, and targeted drug development.

- The Laboratories segment accounted for the largest end-user share of 46.35% in 2025, driven by high sample processing volumes, advanced sequencing infrastructure, and growing integration of oncology testing services.

- The Whole Exome Sequencing (WES) segment is witnessing strong growth due to its ability to efficiently analyze protein-coding regions of the genome, making it highly suitable for cancer mutation profiling and clinical research applications.

- The Screening application segment is emerging as a key growth area, supported by increasing adoption of early cancer detection programs, expanding population-based genomic screening initiatives, and rising awareness of preventive oncology diagnostics.

Market Size & Forecast

- Global Market Value (2025): USD 1.04 Billion

- Expected Market Value (2033): USD 3.20 Billion

- Forecast CAGR (2026–2033): 15.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Clinical Oncology Next Generation Sequencing Market Segmentation

|

Attributes |

Clinical Oncology Next Generation Sequencing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Illumina Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Precision Oncology and Personalized Cancer Treatment Approaches · Rising Adoption of NGS in Liquid Biopsy and Early Cancer Detection · Growing Integration of AI-Driven Genomic Data Analysis and Cloud-Based NGS Platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Clinical Oncology Next Generation Sequencing Market Trends

Trend: Expanding Adoption of Precision Oncology and Genomic-Driven Cancer Treatment

The global Clinical Oncology Next Generation Sequencing (NGS) market is witnessing strong growth due to the increasing shift toward precision oncology and genomics-based cancer diagnostics. Clinical oncology NGS enables comprehensive tumor profiling, allowing clinicians to identify actionable mutations, guide targeted therapies, and improve treatment outcomes. The rising global cancer burden, increasing availability of companion diagnostics, and expanding use of multi-gene panels in clinical practice are accelerating adoption across hospitals and diagnostic laboratories. In addition, advancements in high-throughput sequencing, single-cell genomics, and AI-assisted variant interpretation are improving diagnostic accuracy and reducing turnaround times for cancer genomic testing.

Clinical Oncology Next Generation Sequencing Market Dynamics

Key Market Driver: Rising Demand for Personalized Cancer Therapy and Biomarker-Guided Treatment

A major driver of the Clinical Oncology NGS market is the increasing demand for personalized cancer therapy based on genomic profiling. According to the World Health Organization, cancer remains one of the leading causes of mortality globally, with millions of new cases diagnosed annually, driving the need for more precise and effective treatment strategies.

Next-generation sequencing plays a critical role in identifying genetic mutations, tumor heterogeneity, and resistance mechanisms, enabling oncologists to select targeted therapies and immunotherapies more effectively. Pharmaceutical companies are increasingly integrating NGS into clinical trials for biomarker discovery and patient stratification. Furthermore, expanding reimbursement coverage for genomic testing in developed regions such as North America and Europe is supporting wider clinical adoption. The growing implementation of companion diagnostics alongside targeted oncology drugs is further strengthening the role of NGS in modern cancer care.

Key Restraint/Challenge: High Cost of Sequencing and Complex Bioinformatics Interpretation

A significant challenge in the global Clinical Oncology NGS market is the high cost associated with sequencing workflows, specialized instruments, reagents, and data analysis infrastructure. Clinical-grade sequencing requires advanced platforms, quality control systems, and skilled bioinformatics expertise to interpret large-scale genomic datasets. The complexity of variant interpretation and lack of standardized analytical frameworks can lead to variability in clinical reporting. In addition, smaller hospitals and laboratories in emerging economies often face financial constraints that limit adoption of advanced NGS technologies. Limited reimbursement policies in certain regions and the need for continuous software and hardware upgrades further increase operational costs, creating barriers to widespread implementation.

Key Market Opportunity: Integration of Artificial Intelligence and Cloud-Based Genomic Analytics

The integration of artificial intelligence (AI), machine learning, and cloud-based bioinformatics platforms presents a significant opportunity for the Clinical Oncology NGS market. AI-powered tools can rapidly analyze genomic sequences, identify clinically relevant mutations, and assist in predicting therapy response, significantly improving diagnostic efficiency. For instance, leading genomics companies are increasingly adopting cloud-based sequencing platforms to enable real-time collaboration between research institutions, hospitals, and pharmaceutical companies. Multi-omics integration—combining genomics, transcriptomics, and proteomics—is further enhancing cancer biomarker discovery and enabling deeper tumor characterization.

In addition, large-scale national genomic initiatives, such as population-based cancer sequencing programs in North America, Europe, and Asia-Pacific, are expanding the clinical utility of NGS. Increasing investments in precision medicine, rising adoption of liquid biopsy technologies, and growing use of AI-driven diagnostic pipelines are expected to create substantial growth opportunities for the Clinical Oncology NGS market throughout the forecast period.

Clinical Oncology Next Generation Sequencing Market Scope

The Clinical Oncology Next Generation Sequencing market is segmented on the basis of technology, workflow, application, and end user.

- By Technology

On the basis of technology, the Clinical Oncology Next Generation Sequencing Market is segmented into Whole Genome Sequencing, Whole Exome Sequencing, Targeted Sequencing, and Resequencing. The Targeted Sequencing segment dominated the market with a share of 46.82% in 2025, owing to its high accuracy, lower sequencing cost, faster turnaround time, and strong clinical utility in oncology diagnostics. It is widely used for identifying actionable cancer mutations and guiding precision therapy selection in routine clinical workflows. Increasing adoption in companion diagnostics and biomarker-based treatment planning is further strengthening its dominance. Hospitals and diagnostic laboratories prefer targeted panels due to reduced data complexity and faster interpretation. Rising demand for cost-efficient cancer testing in both developed and emerging markets is also supporting segment growth. Additionally, pharmaceutical companies increasingly use targeted sequencing in drug development programs. Strong integration with NGS-based diagnostic kits is enhancing clinical adoption. Expanding oncology testing volumes globally is reinforcing its leading position.

The Whole Genome Sequencing segment is expected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033, driven by increasing demand for comprehensive genomic profiling in complex and rare cancer cases. It enables complete analysis of coding and non-coding regions, improving mutation detection accuracy. Declining sequencing costs and improved bioinformatics infrastructure are accelerating adoption. Growing use in research institutions and cancer genomics projects is supporting expansion. Rising focus on personalized medicine is further driving demand. Integration with AI-based genomic interpretation tools is improving efficiency. Expanding clinical trials involving genomic sequencing is boosting utilization. Government-funded genomic programs are also supporting adoption. Increasing need for deeper tumor profiling is a major growth driver.

- By Workflow

On the basis of workflow, the Clinical Oncology Next Generation Sequencing Market is segmented into NGS Pre-Sequencing, NGS Sequencing, and NGS Data Analysis. The NGS Sequencing segment dominated the market with a share of 42.37% in 2025, due to its central role in generating high-throughput genomic data for oncology applications. It is widely deployed in clinical laboratories and hospitals for tumor profiling and mutation detection. Continuous advancements in sequencing platforms are improving speed and accuracy. High adoption in routine diagnostic workflows supports segment leadership. Strong demand for scalable sequencing systems is reinforcing growth. Increasing integration with automated laboratory systems is improving efficiency. Pharmaceutical companies rely heavily on sequencing outputs for biomarker identification. Rising global cancer burden is driving testing volumes. Expanding infrastructure in molecular diagnostics is further strengthening adoption.

The NGS Data Analysis segment is expected to grow at the fastest CAGR of 11.2% from 2026 to 2033, driven by rising complexity of genomic datasets generated through sequencing platforms. Increasing demand for AI and machine learning-based interpretation tools is boosting growth. Cloud-based bioinformatics solutions are improving accessibility and scalability. Growing need for real-time clinical decision support is supporting adoption. Expanding precision oncology programs require advanced analytics tools. Rising collaborations between bioinformatics firms and hospitals are accelerating deployment. Increasing use of automated variant interpretation systems is enhancing efficiency. Growth in multi-omics integration is further supporting expansion. Demand for faster and accurate reporting is a key growth driver.

- By Application

On the basis of application, the Clinical Oncology Next Generation Sequencing Market is segmented into Screening, Companion Diagnostics, and Others. The Companion Diagnostics segment dominated the market with a share of 48.15% in 2025, driven by strong integration of NGS in targeted therapy development and precision oncology treatment selection. It plays a critical role in identifying patients eligible for specific cancer therapies. Pharmaceutical companies increasingly depend on companion diagnostics during clinical trials. Regulatory approvals for targeted drugs are boosting demand. High adoption in personalized cancer treatment workflows supports dominance. Strong collaboration between diagnostics firms and pharma companies is accelerating growth. Increasing prevalence of targeted oncology drugs is reinforcing usage. Hospitals widely use companion diagnostics for treatment planning. Expanding biomarker-based drug pipelines is further strengthening adoption.

The Screening segment is expected to grow at the fastest CAGR of 12.0% from 2026 to 2033, driven by rising adoption of early cancer detection programs. Increasing awareness of preventive oncology is boosting demand. Expansion of liquid biopsy-based screening technologies is accelerating growth. Government-led cancer screening initiatives are supporting adoption. Rising focus on non-invasive diagnostic methods is increasing usage. Early detection of cancer significantly improves survival outcomes. Advancements in ultra-sensitive sequencing technologies are enabling better screening accuracy. Growing healthcare investments in preventive diagnostics are expanding reach. Increasing integration of NGS in population health programs is a key driver.

- By End User

On the basis of end user, the Clinical Oncology Next Generation Sequencing Market is segmented into Hospitals, Clinics, Laboratories, and Others. The Hospitals segment dominated the market with a share of 44.69% in 2025, due to strong diagnostic infrastructure and high patient inflow for cancer treatment. Hospitals serve as primary centers for oncology diagnosis and treatment planning. Increasing adoption of precision medicine is driving NGS utilization. Strong availability of molecular diagnostic laboratories within hospitals supports dominance. Integration of NGS in clinical oncology workflows is increasing. Rising cancer burden globally is boosting hospital testing volumes. Strong reimbursement frameworks in developed regions support adoption. Hospitals are increasingly partnering with genomic testing providers. Growing demand for personalized treatment strategies is reinforcing leadership.

The Laboratories segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing outsourcing of genomic testing services. Expansion of specialized molecular diagnostic laboratories is supporting growth. Rising demand for high-throughput sequencing services is accelerating adoption. Cost efficiency of centralized testing models is increasing usage. Growing investment in advanced sequencing infrastructure is boosting capacity. Increasing collaboration with hospitals is expanding service demand. Adoption of automated sequencing workflows is improving efficiency. Rising need for faster turnaround times is supporting growth. Expansion of commercial genomics labs globally is a key driver.

Clinical Oncology Next Generation Sequencing Market Regional Analysis

North America dominated the Clinical Oncology Next Generation Sequencing Market and accounted for the largest revenue share of 39.62% in 2025, supported by advanced genomic research infrastructure, strong investments in precision oncology, widespread adoption of next-generation sequencing (NGS) technologies, and the presence of leading biotechnology and pharmaceutical companies. The region also benefits from robust clinical trial activity, strong reimbursement frameworks for genomic testing, and increasing integration of AI-driven bioinformatics platforms in oncology diagnostics. Continuous advancements in companion diagnostics and personalized cancer therapy development further strengthen North America’s leadership position in the global market.

U.S. Clinical Oncology Next Generation Sequencing Market Insight

The U.S. clinical oncology next generation sequencing market is witnessing strong growth due to rapid expansion of precision medicine programs, increasing adoption of tumor profiling in routine oncology practice, and rising investments in cancer genomics research. Leading biotechnology firms, academic medical centers, and pharmaceutical companies are actively integrating NGS into drug development pipelines and clinical trials for biomarker identification and patient stratification. In addition, strong federal and private funding support for cancer research, along with growing availability of FDA-approved companion diagnostics, is accelerating clinical adoption across hospitals and specialized cancer centers.

Europe Clinical Oncology Next Generation Sequencing Market Insight

The Europe clinical oncology next generation sequencing market remains a key contributor to global revenue, driven by strong public healthcare systems, expanding national cancer genome initiatives, and increasing adoption of precision oncology frameworks. Countries such as Germany, the U.K., and France are investing heavily in genomic medicine programs and centralized cancer screening initiatives. The region is also witnessing rising collaboration between academic institutions and biotechnology companies for biomarker discovery and translational oncology research. Increasing integration of NGS into routine clinical diagnostics is further supporting market expansion across Europe.

U.K. Clinical Oncology Next Generation Sequencing Market Insight

The U.K. clinical oncology next generation sequencing market is experiencing steady growth, supported by initiatives such as national cancer sequencing programs and increasing adoption of genomic testing within the National Health Service (NHS). The country’s strong research ecosystem, combined with rising investment in precision oncology and liquid biopsy technologies, is enabling early cancer detection and improved treatment selection. Furthermore, collaborations between academic research institutions and pharmaceutical companies are accelerating innovation in cancer genomics and personalized therapy development.

Germany Clinical Oncology Next Generation Sequencing Market Insight

The Germany clinical oncology next generation Sequencing market is expanding steadily due to strong biomedical research infrastructure, high healthcare spending, and increasing integration of genomic diagnostics into oncology care pathways. German research institutes and hospitals are actively adopting NGS for cancer subtype classification, therapy selection, and resistance mutation detection. In addition, growing participation in European genomic research networks and increasing investment in digital health infrastructure are further supporting market growth.

Asia-Pacific Clinical Oncology Next Generation Sequencing Market Insight

The Asia-Pacific clinical oncology next generation sequencing market is expected to be the fastest-growing region, with a CAGR of 11.3% from 2026 to 2033, driven by expanding healthcare infrastructure, rising cancer incidence, and increasing adoption of precision medicine approaches. Governments across China, India, Japan, and South Korea are investing heavily in genomic medicine initiatives and national cancer research programs. Growing availability of cost-effective sequencing platforms and expanding clinical laboratory networks are further accelerating adoption across the region.

Japan Clinical Oncology Next Generation Sequencing Market Insight

The Japan clinical oncology next generation Sequencing market is witnessing consistent growth due to strong government support for cancer genomics, advanced healthcare infrastructure, and increasing adoption of personalized oncology treatments. Japanese research institutions are actively involved in large-scale genomic sequencing projects focused on cancer mutation profiling and biomarker discovery. In addition, integration of AI-based diagnostic tools and expansion of precision medicine programs are strengthening clinical adoption of NGS technologies.

China Clinical Oncology Next Generation Sequencing Market Insight

The China clinical oncology next generation Sequencing market is growing rapidly, supported by rising cancer burden, expanding genomic research capabilities, and strong government investment in precision medicine initiatives. Increasing establishment of large-scale sequencing centers, growing biotechnology industry, and expanding use of NGS in hospital-based oncology diagnostics are driving market growth. In addition, collaborations between domestic and international genomics companies are accelerating technology transfer and improving accessibility of advanced cancer sequencing solutions across China.

Clinical Oncology Next Generation Sequencing Market Share

The Clinical Oncology Next Generation Sequencing industry is primarily led by well-established companies, including:

- Moog Inc. (U.S.)

- Dallara (Italy)

- Exail (France)

- IPG Automotive GmbH (Germany)

- aiMotive (Hungary)

- VI‑grade GmbH (Germany)

- Cruden B.V. (Netherlands)

- Dynisma Ltd. (UK)

- Applied Intuition Inc. (U.S.)

- rFpro (rFpro Limited) (England)

- Siemens AG (Germany)

- Dassault Systèmes SE (France)

- MTS Systems Corporation (U.S.)

- CAE Inc. (Canada)

- NVIDIA Corporation (U.S.)

- AB Dynamics PLC (U.K.)

- Forum8 (Japan)

- Mitsubishi Precision Co., Ltd. (Japan)

- FAAC Incorporated (U.S.)

- DriveSafety (U.S.)

- Simtec Simulation Technology GmbH (Germany)

- MB Dynamics Inc. (U.S.)

- Sanlab Simulation (India)

- SimCraft (U.S.)

- CXC Simulations (U.S.)

- XPI Simulation (United Kingdom)

- Tecknotrove Simulator Systems Pvt. Ltd. (India)

- Zhejiang Kechi Intelligent Technology Co., Ltd. (China)

- Shenzhen Zhongzhi Simulation (China)

- Hindustan Simulators (India)

- DriveSimSolutions (U.S.)

- Teksim Technologies (India)

- iMVR Inc. (U.S.)

- SimXperience (U.S.)

Latest Developments in Clinical Oncology Next Generation Sequencing Market

- In September 2025, Moog Inc. has unveiled its latest motion systems all electric E60 Series and the electro pneumatic P60 Series, setting a new benchmark for simulation across aviation, land, and maritime training with support for up to 14,000 kg loads and high fidelity motion for Level D flight simulators and other professional uses. The upgraded platforms deliver enhanced reliability, compact design and sustained operational uptime, reflecting modernized electronics and sustainable operation. These new systems strengthen Moog’s market leadership in simulation motion technology by boosting performance, energy efficiency, and usability

- In January 2025, Exail Technologies has acquired Leukos, a French photonics specialist known for pulsed micro lasers, supercontinuum laser sources, ultrafast lasers, and simulation-enabled optical systems, strengthening its technological and industrial capabilities in advanced laser and simulation technologies. The deal integrates Leukos’s expertise with Exail’s photonics, optical, and simulation platforms, broadening product offerings for applications in biophotonics, microelectronics, and high-fidelity training simulations. This strategic acquisition accelerates Exail’s innovation in high-tech technologies, creating synergies that expand its reach in scientific, industrial, and simulation applications while reinforcing its position as a leading advanced-technology provider

- In November 2025, IPG Automotive launched CarMaker 15.0, the latest version of its driving simulation software used for virtual vehicle development. The new release improves simulation accuracy by integrating virtual electronic control units (vECUs), allowing engineers to test software and vehicle systems at earlier development stages. It also includes enhanced sensor models and improved endurance testing capabilities for ADAS and autonomous vehicles. This development strengthens IPG Automotive’s position in the driving simulator market, as CarMaker enables automotive manufacturers to perform complex vehicle tests in a virtual driving environment instead of physical road testing.

- In November 2024, IPG Automotive released CarMaker 14.0, introducing new simulation capabilities including advanced sensor models and more realistic virtual environments. The update allows developers to simulate complex traffic scenarios involving pedestrians, vehicles, and different weather conditions. These features help automotive companies test ADAS and autonomous driving systems more efficiently in driving simulators, reducing development time and cost. The upgrade also expanded simulation capabilities for heavy-duty vehicles using the TruckMaker platform.

- In June 2023, IPG Automotive participated in the UNICARagil research project, collaborating with universities and industry partners to develop automated vehicle architectures. The company contributed its CarMaker driving simulation platform to support simulation and validation of automated driving systems in Software-in-the-Loop (SIL) and Hardware-in-the-Loop (HIL) environments. This collaboration demonstrates the application of Clinical Oncology Next Generation Sequencing in research and development of autonomous mobility solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.