Global Cns Stimulants Market

Market Size in USD Billion

CAGR :

%

USD

7.57 Billion

USD

12.06 Billion

2025

2033

USD

7.57 Billion

USD

12.06 Billion

2025

2033

| 2026 –2033 | |

| USD 7.57 Billion | |

| USD 12.06 Billion | |

| % | |

|

Central Nervous System (CNS) Stimulants Market Size

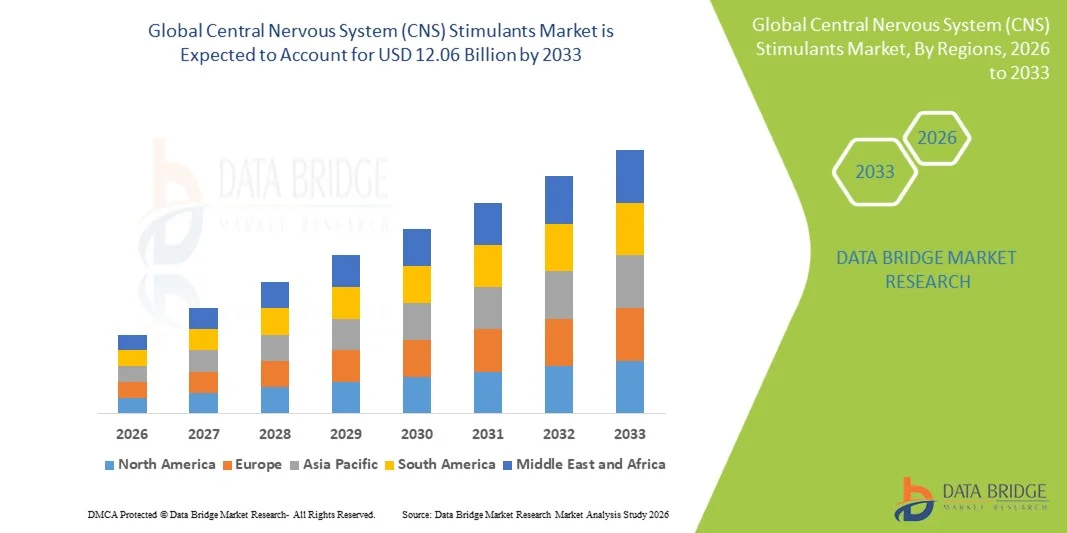

- The global central nervous system (CNS) stimulants market size was valued at USD 7.57 billion in 2025 and is expected to reach USD 12.06 billion by 2033, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological and psychiatric disorders such as attention deficit hyperactivity disorder (ADHD), narcolepsy, and certain cases of depression, leading to higher adoption of central nervous system (CNS) stimulants across various healthcare settings

- Furthermore, rising awareness and diagnosis of cognitive and behavioral disorders, along with growing demand for effective therapies that enhance focus, alertness, and cognitive performance, are establishing CNS stimulants as a key treatment option. These converging factors are accelerating the uptake of Central Nervous System (CNS) Stimulants solutions, thereby significantly boosting the industry's growth

Central Nervous System (CNS) Stimulants Market Analysis

- Central Nervous System (CNS) stimulants, including drugs such as amphetamines and methylphenidate, are widely used in the treatment of conditions like attention deficit hyperactivity disorder (ADHD), narcolepsy, and certain cognitive disorders. These medications play a crucial role in enhancing focus, attention, and wakefulness, making them essential in modern neurological and psychiatric treatment protocols

- The escalating demand for CNS stimulants is primarily fueled by the rising prevalence of ADHD and sleep disorders, increasing awareness and diagnosis rates, and growing acceptance of pharmacological treatments for cognitive and behavioral conditions. In addition, advancements in extended-release formulations and improved patient management strategies are further supporting market growth

- North America dominated the central nervous system (CNS) stimulants market with the largest revenue share of 37.8% in 2025, characterized by high diagnosis rates, advanced healthcare infrastructure, and strong presence of key pharmaceutical companies. The U.S. continues to witness significant growth due to increased prescriptions and widespread adoption of long-acting stimulant medications

- Asia-Pacific is expected to be the fastest growing region in the central nervous system (CNS) stimulants market during the forecast period due to rising awareness of mental health conditions, increasing healthcare expenditure, and a large untreated patient population. Expanding access to psychiatric care in countries such as China and India is further driving regional growth

- The Oral segment dominated the market with a revenue share of 61.4% in 2025, driven by ease of administration and high patient compliance

Report Scope and Central Nervous System (CNS) Stimulants Market Segmentation

|

Attributes |

Central Nervous System (CNS) Stimulants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Central Nervous System (CNS) Stimulants Market Trends

“Rising diagnosis rates and expanding therapeutic applications.”

- A significant and accelerating trend in the global Central Nervous System (CNS) stimulants market is the increasing diagnosis of neurological and behavioral disorders such as attention-deficit/hyperactivity disorder (ADHD) and narcolepsy, driving the demand for stimulant medications

- For instance, commonly prescribed drugs such as Methylphenidate and Amphetamine are widely used for managing ADHD symptoms, improving attention span, and enhancing cognitive performance in both pediatric and adult populations

- There is a growing trend toward extended-release and long-acting formulations, which improve patient compliance and reduce dosing frequency

- Increasing awareness and reduced stigma around mental health and neurodevelopmental disorders are encouraging more individuals to seek medical treatment

- The expansion of CNS stimulants into off-label and adjunct uses, such as cognitive enhancement and treatment-resistant conditions, is also contributing to market growth

- Pharmaceutical companies are focusing on developing formulations with improved efficacy and lower abuse potential

- The rise of telemedicine and digital health platforms is facilitating easier diagnosis and prescription access, especially in developed regions

- This trend toward broader clinical application, improved formulations, and increased accessibility is significantly shaping the growth of the CNS stimulants market

Central Nervous System (CNS) Stimulants Market Dynamics

Driver

“Increasing Prevalence of ADHD and Narcolepsy”

- The rising global prevalence of ADHD and narcolepsy is a major driver of the CNS stimulants market, as these conditions require long-term pharmacological management

- For instance, the increasing number of ADHD diagnoses among children and adults, particularly in countries such as the United States, has significantly boosted the demand for stimulant medications like methylphenidate and amphetamine-based therapies

- Growing awareness among parents, educators, and healthcare professionals is leading to early diagnosis and timely intervention

- Improvements in diagnostic criteria and screening methods are contributing to higher detection rates of neurodevelopmental disorders

- Expanding healthcare access and insurance coverage for mental health treatments are supporting medication adoption

- Government initiatives and educational programs focused on mental health are further driving treatment uptake

- The increasing focus on improving academic and occupational performance is also contributing to higher prescription rates

- In addition, ongoing research and development efforts aimed at enhancing drug safety and effectiveness are supporting sustained market growth

- The rising demand for personalized treatment approaches is further fueling the growth of the CNS stimulants market globally

Restraint/Challenge

“Risk of Abuse, Dependence, and Regulatory Restrictions”

- One of the major challenges in the CNS stimulants market is the high potential for abuse and dependence associated with these medications

- For instance, drugs such as Amphetamine have a risk of misuse, leading to strict regulatory controls and prescribing limitations in many countries

- Concerns regarding side effects such as insomnia, cardiovascular issues, and appetite suppression can impact patient adherence and treatment continuation

- Stringent regulatory frameworks and classification of many stimulants as controlled substances can limit accessibility and delay treatment initiation

- Social stigma and misconceptions regarding stimulant use, particularly in pediatric populations, may discourage treatment adoption

- The availability of non-stimulant alternatives for ADHD treatment may reduce reliance on stimulant medications in certain cases

- Monitoring requirements and prescription restrictions can increase the burden on healthcare providers and patients

- In addition, pricing pressures and generic competition can impact revenue growth for branded products

- Addressing these challenges through safer formulations, patient education, and balanced regulatory policies will be essential for sustaining long-term market growth

Central Nervous System (CNS) Stimulants Market Scope

The market is segmented on the basis of drugs, indication, route of administration, end-users, and distribution channel.

• By Drugs

On the basis of drugs, the Central Nervous System (CNS) Stimulants market is segmented into Phendimetrazine, Phentermine, Methamphetamine, Dextroamphetamine, and Others. The Dextroamphetamine segment dominated the market with the largest revenue share of 36.8% in 2025, driven by its widespread use in the treatment of attention deficit hyperactivity disorder (ADHD) and narcolepsy. Its strong efficacy in improving focus, attention span, and cognitive function supports high prescription rates. Physicians prefer dextroamphetamine due to its well-established clinical profile and predictable outcomes. Increasing prevalence of ADHD across both pediatric and adult populations significantly contributes to demand. Availability of extended-release formulations enhances patient adherence and convenience. Strong adoption in developed healthcare systems further supports its dominance. Pharmaceutical companies continue to innovate formulations for improved safety and reduced side effects. Growing awareness regarding mental health disorders boosts diagnosis and treatment rates. Overall, dextroamphetamine remains the dominant drug segment.

The Phentermine segment is expected to witness the fastest CAGR of 15.5% from 2026 to 2033, driven by increasing demand for weight management therapies amid rising global obesity rates. Phentermine is widely used as an appetite suppressant, supporting short-term obesity treatment. Growing awareness regarding lifestyle-related disorders and weight management fuels adoption. Increasing physician prescriptions for obesity-related conditions support growth. Availability of combination therapies enhances treatment effectiveness. Rising healthcare expenditure and focus on preventive care further accelerate demand. Expanding use in outpatient and specialty clinics supports accessibility. Pharmaceutical advancements in safer formulations improve patient compliance. Overall, phentermine is the fastest-growing drug segment.

• By Indication

On the basis of indication, the market is segmented into Major Depressive Disorder, Anxiety Disorders, Attention Deficit Hyperactivity Disorder, and Others. The Attention Deficit Hyperactivity Disorder (ADHD) segment dominated the market with a revenue share of 48.9% in 2025, driven by the increasing prevalence of ADHD globally, particularly among children and adolescents. CNS stimulants are the first-line treatment for ADHD due to their effectiveness in improving concentration and reducing hyperactivity. Growing awareness among parents and educators supports early diagnosis and treatment. Strong clinical guidelines recommend stimulant medications for ADHD management. Increasing adoption of extended-release formulations enhances adherence. Government initiatives supporting mental health awareness contribute to market growth. Rising demand for long-term therapy ensures sustained usage. Hospitals and specialty clinics play a key role in treatment delivery. Overall, ADHD remains the dominant indication segment.

The Major Depressive Disorder segment is expected to witness the fastest CAGR of 16.1% from 2026 to 2033, driven by rising global burden of depression and increasing acceptance of pharmacological treatments. CNS stimulants are increasingly explored as adjunct therapies in treatment-resistant depression. Growing awareness regarding mental health conditions supports diagnosis and treatment. Increasing stress levels and lifestyle changes contribute to higher prevalence. Expansion of mental health services enhances accessibility. Pharmaceutical research focusing on novel therapeutic applications supports growth. Rising demand for effective and rapid-acting treatments further accelerates adoption. Overall, major depressive disorder is the fastest-growing indication segment.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Injectable, and Others. The Oral segment dominated the market with a revenue share of 61.4% in 2025, driven by ease of administration and high patient compliance. Oral CNS stimulants are widely prescribed due to their convenience and effectiveness. Availability of tablets and extended-release capsules supports flexible dosing regimens. Patients prefer oral medications for long-term treatment adherence. Strong distribution through retail pharmacies enhances accessibility. Physicians commonly prescribe oral drugs for ADHD and depression management. Cost-effectiveness of oral formulations supports widespread adoption. Increasing prevalence of neurological and psychiatric conditions further drives demand. Overall, oral administration remains the dominant segment.

The Injectable segment is expected to witness the fastest CAGR of 14.8% from 2026 to 2033, driven by increasing use in specialized clinical settings and emergency treatments. Injectable CNS stimulants provide rapid onset of action and improved bioavailability. Hospitals prefer injectable formulations for acute care scenarios. Growing demand for controlled and monitored drug delivery supports adoption. Technological advancements in drug delivery systems enhance safety and efficacy. Expansion of hospital infrastructure further supports growth. Rising focus on advanced treatment options accelerates demand. Overall, injectable administration is the fastest-growing segment.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated the market with a revenue share of 47.6% in 2025, driven by high patient inflow for diagnosis and treatment of neurological and psychiatric disorders. Hospitals provide comprehensive care including diagnosis, prescription, and monitoring of CNS stimulant therapies. Availability of specialized healthcare professionals supports effective treatment. Hospitals are key centers for managing severe and complex cases. Strong infrastructure and reimbursement systems enhance accessibility. Increasing hospitalization rates for mental health conditions support demand. Hospitals also play a role in clinical trials and research activities. Overall, hospitals remain the dominant end-user segment.

The Homecare segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2033, driven by increasing preference for long-term treatment in home settings. Patients with stable conditions prefer home-based therapy for convenience and comfort. Availability of oral medications supports self-administration. Telemedicine and remote consultations enhance accessibility. Growing awareness regarding mental health management boosts adoption. Cost-effectiveness compared to hospital care supports growth. Increasing acceptance of community-based care models further drives demand. Overall, homecare is the fastest-growing end-user segment.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Retail Pharmacy segment dominated the market with a revenue share of 46.3% in 2025, driven by widespread availability of CNS stimulant medications and easy accessibility. Retail pharmacies serve as primary distribution points for prescription drugs. Strong presence across urban and rural regions ensures broad reach. Availability of generic medications improves affordability. Pharmacists play a key role in ensuring patient adherence. Increasing prescription volumes for ADHD and depression support demand. Established supply chains ensure consistent availability. Overall, retail pharmacy dominates the distribution channel segment.

The Online Pharmacy segment is expected to witness the fastest CAGR of 17.6% from 2026 to 2033, driven by increasing digital healthcare adoption and consumer preference for convenience. Online platforms offer home delivery and competitive pricing. Rising internet penetration supports rapid growth. Integration with telemedicine enhances prescription access. Patients prefer discreet purchasing for mental health medications. Expanding logistics infrastructure ensures timely delivery. Regulatory support for e-pharmacies boosts trust. Overall, online pharmacy is the fastest-growing distribution channel segment.

Central Nervous System (CNS) Stimulants Market Regional Analysis

- North America dominated the central nervous system (CNS) stimulants market with the largest revenue share of 37.8% in 2025, characterized by high diagnosis rates, advanced healthcare infrastructure, and strong presence of key pharmaceutical companies. The region continues to witness strong demand due to increasing prescriptions and widespread adoption of long-acting stimulant medications

- Consumers in the region benefit from strong awareness of ADHD and narcolepsy, well-established diagnostic frameworks, and broad access to mental healthcare services, which significantly supports treatment adoption

- This widespread adoption is further supported by robust insurance coverage, increasing mental health screening in educational institutions, and the availability of both branded and generic CNS stimulant therapies, establishing North America as the leading regional market

U.S. Central Nervous System (CNS) Stimulants Market Insight

The U.S. central nervous system (CNS) stimulants market captured the largest revenue share in 2025 within North America, driven by high prescription rates and strong clinical awareness of ADHD and related disorders. Patients increasingly rely on pharmacological treatment as a first-line therapy for symptom management. For instance, medications such as Methylphenidate are widely prescribed across pediatric, adolescent, and adult populations in the country. The market is further supported by strong healthcare infrastructure, widespread insurance coverage, and increasing acceptance of long-acting stimulant formulations that improve patient compliance. In addition, ongoing R&D by pharmaceutical companies is improving safety profiles and reducing abuse potential, supporting sustained market growth.

Europe Central Nervous System (CNS) Stimulants Market Insight

The Europe central nervous system (CNS) stimulants market is projected to expand at a substantial CAGR throughout the forecast period, driven by rising awareness of mental health disorders and increasing diagnosis of ADHD across both children and adults. The region benefits from strong regulatory frameworks and structured healthcare systems that support early diagnosis and treatment initiation. Growing urbanization and improved access to psychiatric care are also contributing to higher treatment adoption rates across major European countries.

U.K. Central Nervous System (CNS) Stimulants Market Insight

The U.K. central nervous system (CNS) stimulants market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing ADHD diagnosis rates and growing demand for pharmacological treatment options. Rising awareness among healthcare professionals and patients is encouraging early screening and intervention. In addition, strong public healthcare access through the NHS is improving availability of CNS stimulant medications across the country.

Germany Central Nervous System (CNS) Stimulants Market Insight

The Germany central nervous system (CNS) stimulants market is expected to expand at a considerable CAGR during the forecast period, driven by increasing awareness of neurodevelopmental disorders and strong demand for structured treatment pathways. Germany’s advanced healthcare infrastructure and focus on precision medicine are supporting consistent diagnosis and treatment of ADHD. The market is also benefiting from a preference for regulated, high-quality pharmaceutical products and increasing use of long-acting stimulant formulations.

Asia-Pacific Central Nervous System (CNS) Stimulants Market Insight

The Asia-Pacific central nervous system (CNS) stimulants market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising awareness of mental health conditions, increasing healthcare expenditure, and a large untreated patient population. Countries such as China, India, and Japan are witnessing improved diagnosis rates due to expanding psychiatric healthcare access. Government initiatives focused on mental health awareness and integration of psychiatric services into primary healthcare systems are further supporting market growth. In addition, increasing affordability of generic stimulant medications is improving access across a broader population base.

Japan Central Nervous System (CNS) Stimulants Market Insight

The Japan central nervous system (CNS) stimulants market is gaining momentum due to increasing awareness of ADHD and related disorders, along with a strong focus on healthcare innovation. The country’s aging population and demand for simplified treatment options are supporting the adoption of CNS stimulant therapies. Improved access to psychiatric care and growing integration of digital healthcare services are further contributing to market expansion.

China Central Nervous System (CNS) Stimulants Market Insight

The China central nervous system (CNS) stimulants market accounted for the largest market revenue share in Asia Pacific in 2025, driven by rapid urbanization, expanding healthcare access, and rising awareness of mental health conditions. Increasing diagnosis rates of ADHD, particularly among children and adolescents, are supporting demand for stimulant medications. The presence of strong domestic pharmaceutical manufacturing capabilities and availability of affordable generic drugs are key factors driving market growth.

Central Nervous System (CNS) Stimulants Market Share

The Central Nervous System (CNS) Stimulants industry is primarily led by well-established companies, including:

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Lupin Limited (India)

- Cipla Ltd. (India)

- Aurobindo Pharma Ltd. (India)

- Zydus Lifesciences Ltd. (India)

- Intas Pharmaceuticals Ltd. (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Torrent Pharmaceuticals Ltd. (India)

- Takeda Pharmaceutical Company Limited (Japan)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Johnson & Johnson (U.S.)

- Amneal Pharmaceuticals (U.S.)

- Mallinckrodt Pharmaceuticals (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Sandoz Group AG (Switzerland)

- Viatris Inc. (U.S.)

Latest Developments in Global Central Nervous System (CNS) Stimulants Market

- In March 2021, the U.S. Food and Drug Administration (FDA) approved Azstarys (serdexmethylphenidate and dexmethylphenidate) for the treatment of attention-deficit/hyperactivity disorder (ADHD) in patients aged six years and older, introducing a novel prodrug formulation designed to provide both immediate and extended symptom control

- In April 2021, the U.S. FDA approved Qelbree (viloxazine extended-release capsules) developed by Supernus Pharmaceuticals for the treatment of ADHD in pediatric patients, marking the first new non-stimulant ADHD therapy approved in years and expanding treatment options alongside traditional CNS stimulants

- In May 2022, the U.S. FDA expanded approval of Qelbree (viloxazine ER) to include adults with ADHD, representing the first non-stimulant ADHD drug approved for adults in over two decades and influencing prescribing dynamics in the broader CNS stimulant treatment landscape

- In June 2025, the U.S. Food and Drug Administration (FDA) announced class-wide labeling revisions for extended-release stimulant medications used to treat ADHD, requiring updated warnings about increased risk of weight loss and adverse reactions in children under six years, reflecting heightened regulatory scrutiny of stimulant safety

- In November 2025, Otsuka Pharmaceutical submitted a New Drug Application (NDA) to the U.S. FDA for centanafadine, a novel triple reuptake inhibitor targeting norepinephrine, dopamine, and serotonin for ADHD treatment, representing a potential next-generation CNS stimulant/adjacent therapy under regulatory review

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.