Global Coagulation Reagents Market

Market Size in USD Billion

CAGR :

%

USD

4.00 Billion

USD

9.02 Billion

2025

2033

USD

4.00 Billion

USD

9.02 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.00 Billion | |

| USD 9.02 Billion | |

| % | |

|

Coagulation Reagents Market Overview

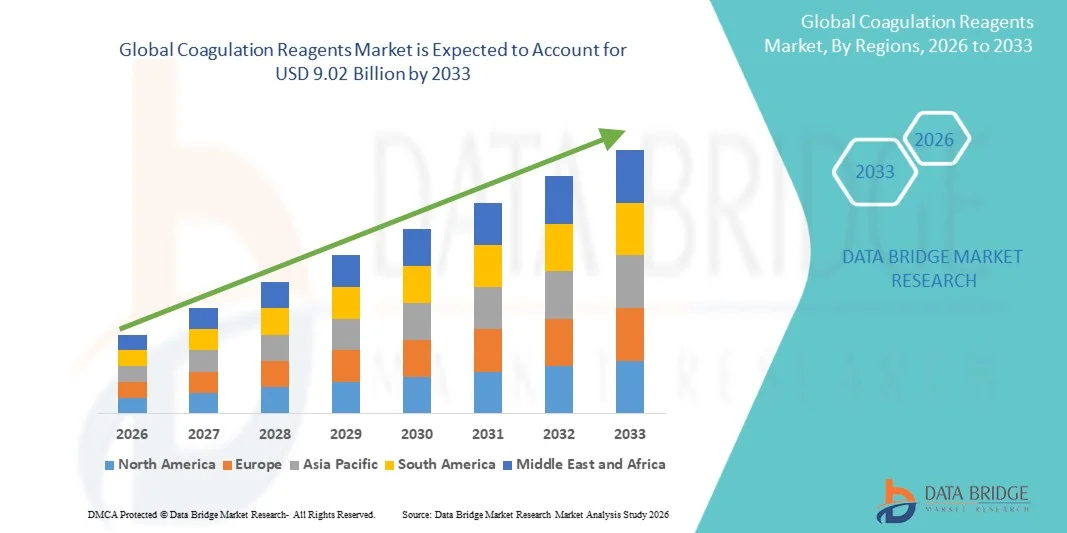

The global Coagulation Reagents market was valued at USD 4.00 billion in 2025 and is projected to reach USD 9.02 billion by 2033, growing at a CAGR of 10.70% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for safe and realistic driver training solutions, rapid advancements in simulation hardware and software, and expanding applications across automotive R&D, defense, and professional motorsport.

The increasing incidence of road accidents globally, combined with stricter government regulations on driver training and road safety, is compelling transportation authorities, driving schools, and military organizations to adopt advanced simulation technologies. Fixed-base and VR/AR-enabled simulators are replacing traditional on-road training in many markets, offering cost-effective, repeatable, and risk-free environments for skill development and autonomous vehicle validation.

Key Market Trends & Insights

- North America dominated the global Coagulation Reagents market with the largest revenue share of 36.18% in 2025, supported by advanced healthcare infrastructure, high adoption of automated coagulation analyzers, and increasing prevalence of cardiovascular and blood clotting disorders across the region.

- The Prothrombin Test segment led the market with a 39.46% share in 2025, driven by its extensive use in monitoring anticoagulant therapy, evaluating bleeding disorders, and routine pre-surgical coagulation assessment.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by rising healthcare expenditure, increasing prevalence of cardiovascular and blood-related disorders, and expanding diagnostic laboratory networks across China, India, and Japan.

- The Optical Technology segment is the fastest-growing technology category, projected to register a CAGR of 7.1%, reflecting growing demand for high-sensitivity, rapid, and automated coagulation testing solutions in clinical laboratories.

- The Hospitals segment dominates the end-use category with a 43.28% revenue share in 2025, led by rising patient admissions, increasing surgical procedures, and growing demand for routine coagulation screening and emergency diagnostic testing.

- Mechanical Technology accounts for 37.84% of the market, preferred by healthcare facilities and diagnostic laboratories for its testing reliability, cost-efficiency, and broad compatibility with coagulation analyzers.

- The Prothrombin segment dominated the market with a share of 39.46% in 2025 due to its extensive use in monitoring anticoagulant therapy, assessing blood clotting disorders, and conducting routine pre-surgical coagulation testing.

Market Size & Forecast

- Global Market Value (2025): USD 4.00 Billion

- Expected Market Value (2033): USD 9.02 Billion

- Forecast CAGR (2026–2033): 10.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Global Coagulation Reagents Market Segmentation

|

Attributes |

Coagulation Reagents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• F. Hoffmann-La Roche Ltd |

|

Market Opportunities |

· Increasing adoption of automated and AI-integrated coagulation analyzers · Rising demand for point-of-care coagulation testing in emergency care · Expanding healthcare infrastructure and growing awareness regarding early diagnosis |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Coagulation Reagents Market Trends

Trend: Rising Adoption of Automated and High-Sensitivity Coagulation Testing

Healthcare providers and diagnostic laboratories are increasingly adopting automated coagulation analyzers and high-sensitivity coagulation reagents to improve testing accuracy, reduce turnaround time, and support high-volume diagnostic workflows. Advanced optical and electrochemical technologies are enabling rapid detection of clotting abnormalities, thrombosis risk, and anticoagulant therapy effectiveness. The growing use of D-Dimer and Prothrombin tests in emergency medicine, cardiovascular care, and post-surgical monitoring is further accelerating demand for reliable reagent solutions. In addition, hospitals are integrating AI-enabled laboratory systems and digital data management platforms to streamline coagulation diagnostics and improve clinical decision-making accuracy.

Global Coagulation Reagents Market Dynamics

Key Market Driver: Increasing Prevalence of Cardiovascular and Blood Clotting Disorders

The growing global burden of cardiovascular diseases, deep vein thrombosis (DVT), pulmonary embolism, hemophilia, and liver disorders is significantly driving demand for coagulation reagents. According to global health statistics, cardiovascular diseases account for millions of deaths annually, increasing the need for routine coagulation monitoring and anticoagulant therapy management. Hospitals and diagnostic laboratories are expanding coagulation testing capabilities to support early diagnosis and treatment monitoring. The rising number of surgical procedures and trauma cases is also increasing the utilization of APTT, fibrinogen, and prothrombin testing across healthcare settings. Furthermore, aging populations in North America, Europe, and parts of Asia-Pacific are contributing to higher incidences of clotting disorders, creating sustained demand for advanced coagulation diagnostic solutions.

Key Restraint/Challenge: High Cost of Automated Coagulation Diagnostic Systems

A major challenge in the global coagulation reagents market is the high cost associated with advanced coagulation analyzers and automated laboratory infrastructure. Modern systems require significant investment in analyzer procurement, reagent calibration, maintenance, software integration, and quality assurance programs. Smaller hospitals, independent laboratories, and healthcare facilities in developing economies often face budget constraints that limit adoption of high-end coagulation testing technologies. In addition, maintaining reagent stability, ensuring cold-chain logistics, and complying with stringent regulatory standards increase operational costs for manufacturers and end users.

The growing implementation of fully automated coagulation laboratories across developed healthcare systems highlights the substantial capital expenditure required for modern diagnostic infrastructure, creating barriers for smaller and resource-constrained healthcare providers.

Key Market Opportunity: Expansion of Point-of-Care and AI-Integrated Coagulation Diagnostics

The increasing adoption of point-of-care coagulation testing presents a significant growth opportunity for market players. Portable and rapid-testing coagulation reagent kits are gaining popularity in emergency departments, ambulatory surgical centers, and home healthcare settings due to their ability to provide immediate results and support faster clinical decisions. AI-integrated coagulation platforms are also emerging as a major innovation area, enabling predictive analytics, automated result interpretation, and workflow optimization in diagnostic laboratories.

In addition, expanding healthcare infrastructure and rising awareness regarding early thrombosis detection in emerging economies such as China, India, Brazil, and Southeast Asian countries are creating strong opportunities for reagent manufacturers. The development of cloud-connected diagnostic systems and next-generation optical testing technologies is further supporting market expansion by improving accessibility, efficiency, and diagnostic precision across decentralized healthcare environments.

Global Coagulation Reagents Market Scope

The Coagulation Reagents market is segmented on the basis of test type, technology, and end use.

- By Test Type

On the basis of test type, the global Coagulation Reagents market is segmented into APTT, D-Dimer, Fibrinogen, Prothrombin, and Others. The Prothrombin segment dominated the market with a share of 39.46% in 2025 due to its extensive use in monitoring anticoagulant therapy, assessing blood clotting disorders, and conducting routine pre-surgical coagulation testing. The widespread prevalence of cardiovascular diseases, liver disorders, and thrombotic conditions has significantly increased the demand for prothrombin testing across hospitals and diagnostic laboratories. In addition, the growing aging population, rising number of surgical procedures, and increasing adoption of automated coagulation analyzers are supporting segment growth. Healthcare providers are increasingly utilizing prothrombin reagents for rapid and accurate coagulation assessment in emergency and critical care settings. Furthermore, advancements in optical detection technologies and high-sensitivity reagents are improving test efficiency and clinical reliability, reinforcing the leading position of this segment in the global market.

The D-Dimer segment is expected to witness the fastest CAGR of 7.0% from 2026 to 2033, driven by the increasing incidence of deep vein thrombosis, pulmonary embolism, and cardiovascular complications globally. Growing utilization of D-Dimer testing in emergency departments and intensive care units for rapid thrombosis screening is accelerating segment expansion. In addition, rising awareness regarding early diagnosis of clotting abnormalities, coupled with increasing demand for point-of-care coagulation testing solutions, is supporting market growth. The integration of AI-enabled diagnostic platforms and automated laboratory systems is further improving test turnaround time and accuracy, encouraging broader adoption of D-Dimer reagents across developed and emerging healthcare markets.

- By Technology

On the basis of technology, the global Coagulation Reagents market is segmented into Mechanical, Electrochemical, Optical, and Others. The Mechanical segment dominated the market with a share of 37.84% in 2025 due to its high testing reliability, cost-effectiveness, and widespread adoption across hospitals and diagnostic laboratories. Mechanical coagulation testing technologies are extensively utilized for routine coagulation screening and anticoagulant monitoring because of their operational simplicity and compatibility with a broad range of coagulation analyzers. The increasing number of blood disorder diagnostic procedures, coupled with rising investments in laboratory automation, is supporting the continued demand for mechanical coagulation technologies. In addition, healthcare facilities prefer these systems for their consistent performance, lower maintenance requirements, and suitability for high-volume diagnostic workflows. Strong adoption across medium-sized laboratories and emerging healthcare markets is further reinforcing the dominance of the mechanical technology segment globally.

The Optical segment is projected to register the fastest CAGR of 7.1% from 2026 to 2033, driven by growing demand for high-sensitivity and rapid coagulation testing solutions. Optical technologies provide enhanced accuracy, faster processing speeds, and improved automation capabilities, making them increasingly preferred in advanced diagnostic laboratories and research institutions. Rising adoption of fully automated coagulation analyzers, integration with AI-based diagnostic systems, and increasing demand for precision diagnostics are accelerating the growth of this segment. Furthermore, technological advancements in photometric detection systems and increasing use of optical coagulation testing in critical care and emergency diagnostics are creating strong growth opportunities for manufacturers operating in the global market.

- By End Use

On the basis of end use, the global Coagulation Reagents market is segmented into Hospitals, Research Institutes, Diagnostic Centers, and Others. The Hospitals segment dominated the market with a share of 43.28% in 2025 due to the high volume of coagulation testing procedures conducted for surgical diagnostics, anticoagulant therapy monitoring, trauma care, and cardiovascular disease management. Hospitals remain the primary healthcare facilities for emergency coagulation testing and routine hematology diagnostics because of their advanced laboratory infrastructure and availability of skilled healthcare professionals. Rising patient admissions, increasing prevalence of chronic diseases, and growing number of complex surgical procedures are driving strong demand for coagulation reagents across hospital settings. In addition, hospitals are increasingly investing in automated coagulation analyzers, AI-integrated laboratory systems, and rapid diagnostic technologies to improve testing efficiency and patient outcomes. Expanding healthcare expenditure and modernization of hospital diagnostic infrastructure are further strengthening the dominance of this segment in the global market.

The Diagnostic Centers segment is anticipated to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by the increasing shift toward specialized and decentralized diagnostic services. Rising demand for rapid and cost-effective coagulation testing, coupled with growing preference for outpatient diagnostic solutions, is accelerating the expansion of diagnostic centers worldwide. These facilities are increasingly adopting automated and point-of-care coagulation testing technologies to improve operational efficiency and reduce turnaround time. In addition, growing awareness regarding preventive healthcare and early disease detection is encouraging patients to undergo routine coagulation screening through independent diagnostic laboratories. Expanding laboratory networks in emerging economies and rising investments in advanced diagnostic technologies are further supporting the rapid growth of the diagnostic centers segment globally.

Global Coagulation Reagents Market Regional Analysis

North America dominated the Coagulation Reagents market and accounted for the largest revenue share of 36.18% in 2025, supported by advanced healthcare infrastructure, high adoption of automated coagulation analyzers, and increasing prevalence of cardiovascular and blood clotting disorders across the region. The region also benefits from strong presence of leading diagnostic companies, rising healthcare expenditure, and growing demand for rapid and accurate coagulation testing solutions across hospitals and diagnostic laboratories. Increasing incidence of thrombosis, hemophilia, liver disorders, and cardiovascular diseases, along with growing utilization of anticoagulant therapies, continues to strengthen North America’s leadership position in the global market.

U.S. Coagulation Reagents Market Insight

The U.S. Coagulation Reagents market is witnessing strong growth due to increasing prevalence of cardiovascular diseases, rising number of surgical procedures, and growing adoption of automated coagulation diagnostic systems. Hospitals and diagnostic laboratories are increasingly utilizing advanced coagulation reagents for thrombosis screening, anticoagulant monitoring, and emergency diagnostics. In addition, strong investments in healthcare technologies, AI-enabled laboratory automation, and point-of-care testing solutions are accelerating market expansion across the country. The presence of major diagnostic manufacturers and rising awareness regarding early disease detection are further supporting market growth in the U.S.

Europe Coagulation Reagents Market Insight

The Europe Coagulation Reagents market remains a major contributor to global revenue, driven by advanced healthcare systems, strong government support for diagnostic testing, and increasing adoption of automated laboratory technologies. Rising prevalence of blood clotting disorders, cardiovascular diseases, and aging population across the region are supporting demand for coagulation testing solutions. Additionally, increasing focus on precision diagnostics, high laboratory testing standards, and growing investments in hematology research are further enhancing the adoption of coagulation reagents throughout Europe.

U.K. Coagulation Reagents Market Insight

The U.K. Coagulation Reagents market is experiencing steady growth, supported by increasing demand for routine coagulation testing, rising cases of thrombotic disorders, and growing healthcare expenditure. Hospitals and diagnostic centers are increasingly adopting high-sensitivity coagulation analyzers and automated testing platforms to improve testing efficiency and patient outcomes. Furthermore, integration of AI-based laboratory systems and digital diagnostic technologies is enhancing clinical accuracy and operational performance, contributing to market expansion across the country.

Germany Coagulation Reagents Market Insight

The Germany Coagulation Reagents market is expanding steadily due to the country’s advanced diagnostic infrastructure, strong pharmaceutical and biotechnology industry presence, and increasing adoption of next-generation coagulation testing technologies. Healthcare providers and research institutions are increasingly utilizing automated coagulation analyzers for rapid and precise diagnostic procedures. Continuous advancements in optical and electrochemical testing technologies, coupled with rising investments in healthcare innovation and laboratory modernization, are further driving market growth in Germany.

Asia-Pacific Coagulation Reagents Market Insight

The Asia-Pacific Coagulation Reagents market is expected to witness rapid growth at a CAGR of 7.4% from 2026 to 2033, driven by rising healthcare expenditure, increasing prevalence of cardiovascular and blood-related disorders, and expanding diagnostic laboratory networks across countries such as China, India, and Japan. Growing awareness regarding early disease diagnosis, improving healthcare infrastructure, and increasing adoption of automated coagulation analyzers are supporting regional market expansion. In addition, rising government initiatives for healthcare modernization and expanding access to diagnostic services are accelerating the adoption of coagulation reagents across hospitals and diagnostic centers in the region.

Japan Coagulation Reagents Market Insight

The Japan Coagulation Reagents market is witnessing consistent growth due to rising aging population, increasing incidence of cardiovascular disorders, and strong adoption of advanced diagnostic technologies. Hospitals, research institutes, and diagnostic laboratories are increasingly utilizing high-precision coagulation testing systems for disease diagnosis and anticoagulant monitoring. Moreover, growing investments in laboratory automation, AI-integrated healthcare systems, and precision medicine are further contributing to market growth in Japan.

China Coagulation Reagents Market Insight

The China Coagulation Reagents market is growing rapidly, driven by expanding healthcare infrastructure, rising prevalence of chronic diseases, and increasing government focus on improving diagnostic capabilities. Growing adoption of automated coagulation analyzers and rapid diagnostic technologies across hospitals and diagnostic laboratories is significantly boosting market demand. In addition, rising healthcare spending, increasing awareness regarding preventive healthcare, and rapid expansion of laboratory networks are positioning China as one of the fastest-growing markets for coagulation reagents globally.

Global Coagulation Reagents Market Share

The Coagulation Reagents industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd

- Siemens Healthineers AG

- Abbott Laboratories

- Danaher Corporation

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

- Werfen S.A.

- Bio-Rad Laboratories Inc.

- Horiba Ltd.

- Diagnostica Stago S.A.S.

- Sekisui Medical Co. Ltd.

- Trinity Biotech plc

- Becton, Dickinson and Company

- NIHON KOHDEN CORPORATION

- Meril Life Sciences Pvt. Ltd.

- Maccura Biotechnology Co., Ltd.

- Instrumentation Laboratory Company

- Grifols S.A.

- Helena Laboratories Corporation

- BioMedica Diagnostics Inc.

- Randox Laboratories Ltd.

- Tulip Diagnostics Pvt. Ltd.

- Erba Mannheim

- HemoSonics LLC

- Beijing Succeeder Technology Inc.

Latest Developments in Global Coagulation Reagents Market

- In June 2025, Sysmex Corporation received U.S. FDA clearance for its CN-6000 automated blood coagulation analyzer along with reagent products for five common hemostasis tests, including PT/INR, APTT, fibrinogen, antithrombin, and D-dimer. The approval strengthened Sysmex’s position in automated coagulation diagnostics and expanded access to high-throughput testing solutions for hospitals and laboratories

- In February 2024, F. Hoffmann-La Roche Ltd announced the launch of three new coagulation tests for oral Factor Xa inhibitors, including apixaban, edoxaban, and rivaroxaban, designed to support clinical decision-making in patients receiving direct oral anticoagulant therapies. The new assays utilize Roche’s reagent cassette technology to improve workflow automation, reagent preparation efficiency, and testing accuracy on cobas analyzers, strengthening the company’s hemostasis diagnostics portfolio

- In April 2024, Sysmex Corporation and Siemens Healthineers AG began independently distributing their combined portfolio of hemostasis testing solutions across the U.S. and Europe. The development expanded access to advanced coagulation analyzers and reagent systems, enabling laboratories to improve automation, testing throughput, and diagnostic efficiency in coagulation testing workflows

- In December 2024, Werfen S.A. expanded its Hemostasis and Acute Care Diagnostics Technology Center in Bedford through a new 105,000-square-foot facility backed by a USD 50 million investment. The expansion was aimed at strengthening innovation capabilities, accelerating development of advanced coagulation reagents and analyzer technologies, and enhancing manufacturing and R&D operations in hemostasis diagnostics

- In July 2022, HORIBA Medical enhanced its fully automated Yumizen G800 hemostasis analyzer with a new Tube Filling Level Check functionality. The upgrade was designed to reduce pre-analytical testing errors and improve reliability in coagulation diagnostics, supporting laboratories in achieving more accurate and efficient coagulation testing workflows

- In August 2021, Siemens Healthineers AG launched the Sysmex CN-3000 and CN-6000 Hemostasis Systems for mid- and high-volume coagulation testing laboratories. The fully automated systems were developed to improve testing productivity, workflow standardization, and clinical efficiency for routine and specialized coagulation diagnostics

- In February 2021, Siemens Healthineers AG and Sysmex Corporation renewed and extended their long-standing global partnership for hemostasis products, including distribution and service agreements for Sysmex CN-Series automated blood coagulation analyzers. The collaboration reinforced both companies’ positions in the global coagulation diagnostics and reagent market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.