Global Commercial Telematics Market

Market Size in USD Billion

CAGR :

%

USD

64.80 Billion

USD

240.29 Billion

2025

2033

USD

64.80 Billion

USD

240.29 Billion

2025

2033

| 2026 –2033 | |

| USD 64.80 Billion | |

| USD 240.29 Billion | |

| % | |

|

Commercial Telematics Market Size

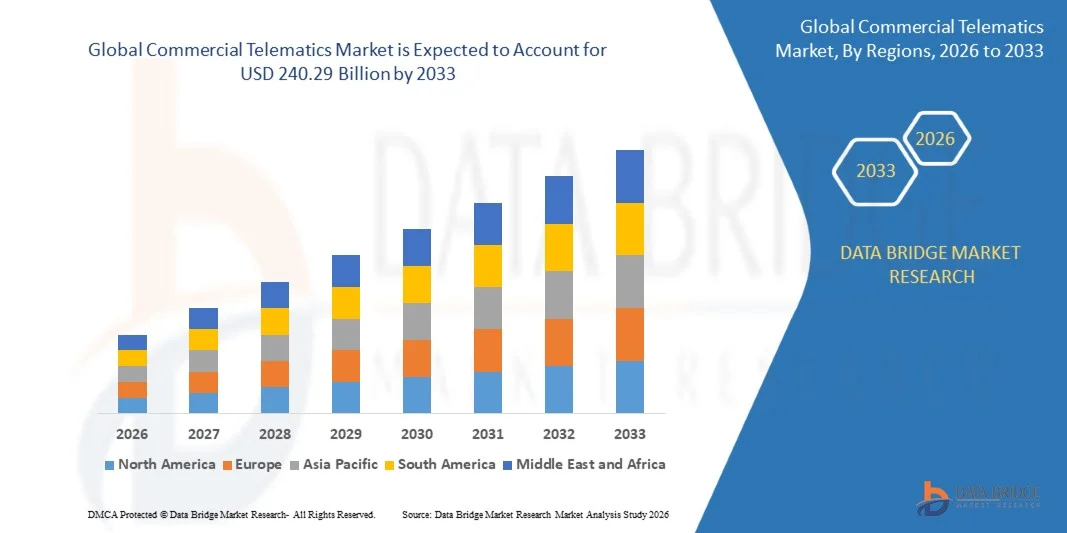

- The global commercial telematics market size was valued at USD 64.80 billion in 2025 and is expected to reach USD 240.29 billion by 2033, at a CAGR of 17.80% during the forecast period

- The market growth is largely fuelled by the increasing adoption of connected vehicles, rising demand for fleet management solutions, and the need for real-time monitoring and optimization of logistics operations

- Growing focus on reducing operational costs, improving fuel efficiency, and enhancing driver safety is further driving the uptake of telematics solutions

Commercial Telematics Market Analysis

- The market is witnessing significant adoption in logistics, transportation, and construction sectors, where fleet efficiency and safety are critical

- Increasing regulatory requirements for vehicle tracking, emission monitoring, and driver behavior management are creating additional demand for telematics solutions

- North America dominated the commercial telematics market with the largest revenue share of 35.42% in 2025, driven by increasing adoption of connected vehicles, fleet management solutions, and regulatory compliance requirements

- Asia-Pacific region is expected to witness the highest growth rate in the global commercial telematics market, driven by rising vehicle sales, growing demand for fleet management solutions, adoption of IoT-enabled monitoring, and increasing investments in connected fleet technologies across emerging economies such as China, India, and Japan

- The OEM segment held the largest market revenue share in 2025, driven by increasing integration of telematics systems in new commercial vehicles for fleet monitoring, fuel optimization, and regulatory compliance. OEM telematics solutions offer seamless integration with vehicle electronics, enhanced data reliability, and long-term technical support, making them a preferred choice for large fleets. Rising emphasis on safety, operational efficiency, and predictive maintenance is further supporting OEM adoption. Fleet operators also benefit from factory-installed solutions that are pre-configured for vehicle-specific parameters

Report Scope and Commercial Telematics Market Segmentation

|

Attributes |

Commercial Telematics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• AirIQ Inc. (U.S.) |

|

Market Opportunities |

• Increasing Adoption Of Electric And Connected Commercial Vehicles |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Commercial Telematics Market Trends

“Rising Adoption of Connected Vehicles and Fleet Management Solutions”

• The growing focus on operational efficiency and real-time monitoring is significantly shaping the commercial telematics market, as fleet operators increasingly adopt solutions that optimize routes, reduce fuel consumption, and improve driver safety. Telematics systems are gaining traction due to their ability to provide data-driven insights, predictive analytics, and regulatory compliance, encouraging adoption across logistics, transportation, and construction sectors

• Increasing awareness around fleet safety, cost reduction, and sustainability has accelerated the demand for commercial telematics in trucking, delivery, and public transportation. Companies are actively seeking solutions that enhance operational visibility, prevent accidents, and improve fuel efficiency, prompting collaborations between telematics providers and fleet operators to integrate advanced features

• Technological trends, including AI-driven analytics, IoT-enabled monitoring, and cloud-based telematics platforms, are influencing purchasing decisions. Manufacturers and service providers are emphasizing data accuracy, system integration, and scalable solutions, which help differentiate offerings in a competitive market

• For instance, in 2024, Geotab in Canada and Verizon Connect in the U.S. expanded their telematics service portfolios with AI-powered fleet management solutions for commercial vehicles. These launches responded to rising operator demand for efficiency, safety, and regulatory compliance, with distribution across enterprise, logistics, and public transport sectors

• While adoption of commercial telematics is growing, sustained market expansion depends on continuous innovation, cost-effective solutions, and interoperability across vehicle types. Providers are also focusing on improving predictive analytics, cloud infrastructure, and cybersecurity to drive broader adoption

Commercial Telematics Market Dynamics

Driver

“Growing Demand for Fleet Efficiency, Safety, and Connected Vehicle Solutions”

• Rising operational and regulatory requirements are a major driver for the commercial telematics market. Fleet operators are increasingly implementing telematics to monitor vehicle location, optimize routes, reduce fuel consumption, and ensure driver safety

• Expanding applications in logistics, transportation, and public service fleets are influencing market growth. Telematics help improve operational efficiency, reduce downtime, and ensure compliance with local and international regulations, enabling operators to meet performance and safety expectations

• Providers are actively promoting telematics solutions through product innovation, AI-based analytics, and cloud integration. Growing awareness of cost savings, environmental benefits, and fleet optimization is encouraging partnerships between software providers and fleet operators to improve solution performance and scalability

• For instance, in 2023, Trimble in the U.S. and TomTom Telematics in the Netherlands reported increased adoption of connected fleet management solutions across commercial trucking and delivery services. The expansion followed rising demand for route optimization, fuel management, and real-time monitoring, helping operators achieve cost efficiency and compliance

• Although rising demand supports growth, wider adoption depends on cost optimization, cybersecurity, and standardization across vehicle types. Investment in cloud platforms, AI capabilities, and robust data integration will be critical for meeting global demand and maintaining a competitive edge

Restraint/Challenge

“High Implementation Cost and Integration Complexity”

• The relatively high cost of telematics hardware, software, and subscription services remains a key challenge, limiting adoption among small and mid-sized fleet operators. Initial investment and ongoing maintenance expenses contribute to adoption barriers

• Integration complexity with existing fleet systems, vehicles, and enterprise IT infrastructure restricts deployment in some organizations. Variability in vehicle types and telematics protocols can further affect seamless adoption and data accuracy

• Connectivity and cybersecurity concerns also impact market growth, as telematics systems require reliable internet connections and protection against data breaches. Providers must invest in secure networks, regular updates, and compliance with regional data regulations

• For instance, in 2024, fleet operators in India and Brazil reported slower uptake of telematics solutions due to high costs, integration challenges, and limited technical expertise. Smaller operators struggled with system compatibility and training requirements, affecting overall market penetration

• Overcoming these challenges will require cost-effective solutions, simplified integration, and robust customer support. Collaboration with vehicle manufacturers, fleet operators, and software providers, along with flexible pricing and subscription models, can unlock the long-term growth potential of the global commercial telematics market

Commercial Telematics Market Scope

The market is segmented on the basis of type, platform, application, and end user.

• By Type

On the basis of type, the commercial telematics market is segmented into OEM and Aftermarket. The OEM segment held the largest market revenue share in 2025, driven by increasing integration of telematics systems in new commercial vehicles for fleet monitoring, fuel optimization, and regulatory compliance. OEM telematics solutions offer seamless integration with vehicle electronics, enhanced data reliability, and long-term technical support, making them a preferred choice for large fleets. Rising emphasis on safety, operational efficiency, and predictive maintenance is further supporting OEM adoption. Fleet operators also benefit from factory-installed solutions that are pre-configured for vehicle-specific parameters.

The Aftermarket segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising retrofitting of existing vehicles with telematics devices to improve fleet efficiency, safety, and monitoring capabilities. Aftermarket solutions are particularly attractive to small and medium-sized enterprises due to their lower cost, flexible deployment, and compatibility with multiple vehicle types. Increasing availability of plug-and-play devices, subscription-based models, and mobile integration is further fueling adoption. Growing awareness among fleet operators about ROI and operational savings is also contributing to Aftermarket market growth.

• By Platform

On the basis of platform, the market is segmented into Embedded Systems, Tethered Systems, and Smartphone Integration Systems. Embedded Systems held the largest market share in 2025, supported by their reliability, direct integration with vehicle electronics, and ability to provide real-time insights on driver behavior, vehicle performance, and fuel usage. These systems are favored for large-scale fleet operations due to minimal maintenance requirements and continuous data collection. The rising adoption of connected vehicle infrastructure and cloud-based analytics is further enhancing the appeal of embedded platforms. Fleet operators benefit from high accuracy and seamless integration with existing enterprise systems.

The Smartphone Integration Systems segment is expected to grow at the fastest rate from 2026 to 2033, driven by the increasing use of mobile applications for fleet monitoring, alerts, and analytics. These systems allow managers to track vehicle location, monitor driver behavior, and receive real-time notifications from anywhere, improving decision-making efficiency. The rise of BYOD (Bring Your Own Device) policies and mobile-first telematics solutions is accelerating adoption. Smartphone platforms also enable cost-effective deployment for small and medium fleets, encouraging rapid market expansion.

• By Application

On the basis of application, the market is segmented into Insurance Telematics, Fleet / Asset Management, Satellite Navigation, Infotainment, Remote Alarm and Monitoring, and Telehealth Solutions. Fleet / Asset Management accounted for the largest revenue share in 2025 due to the growing demand for route optimization, fuel efficiency, and operational productivity across logistics, transportation, and construction sectors. Companies are investing in telematics to reduce downtime, enhance asset utilization, and improve compliance with safety regulations. Predictive analytics and reporting features also strengthen fleet management capabilities, supporting industry-wide adoption. Increasing focus on sustainability and cost reduction is further boosting demand for these solutions.

Insurance Telematics is expected to witness the fastest growth from 2026 to 2033, driven by the adoption of usage-based insurance (UBI) models, driver behavior monitoring, and risk assessment programs. Insurers and fleet operators are increasingly using telematics to tailor insurance premiums, incentivize safe driving, and minimize claim costs. The rising availability of connected vehicle data and AI-enabled risk analytics is enhancing the effectiveness of insurance telematics. Growing awareness among businesses and drivers about financial and safety benefits is further driving segment expansion.

• By End User

On the basis of end user, the market is segmented into Healthcare, Construction, Transportation and Logistics, and Government and Utilities. Transportation and Logistics held the largest market share in 2025, fueled by the growing need for real-time tracking, route optimization, and compliance with regional and international regulations. Fleet operators are increasingly using telematics to improve delivery efficiency, reduce operational costs, and monitor driver performance. Integration with GPS, predictive maintenance, and cloud platforms further enhances operational insights and decision-making. The rise of e-commerce and last-mile delivery services is also driving adoption in this sector.

The Healthcare segment is expected to witness the fastest growth from 2026 to 2033, driven by the adoption of telematics-enabled solutions for emergency vehicles, patient transport, and remote monitoring of medical fleets. Telehealth services integrated with vehicle telematics improve response times, operational efficiency, and patient safety. Increasing government initiatives and private investments to digitize healthcare transport and mobile medical units are supporting growth. Advanced analytics, predictive routing, and mobile connectivity further enhance fleet management in the healthcare sector.

Commercial Telematics Market Regional Analysis

• North America dominated the commercial telematics market with the largest revenue share of 35.42% in 2025, driven by increasing adoption of connected vehicles, fleet management solutions, and regulatory compliance requirements

• Fleet operators in the region highly value real-time tracking, predictive analytics, and seamless integration with enterprise systems, which improve operational efficiency, reduce fuel costs, and enhance driver safety

• This widespread adoption is further supported by high fleet density, advanced telecommunications infrastructure, and rising awareness of telematics benefits, establishing telematics solutions as a critical tool for transportation, logistics, and construction sectors

U.S. Commercial Telematics Market Insight

The U.S. commercial telematics market captured the largest revenue share in 2025 within North America, fueled by rapid deployment of connected fleet solutions and the growing trend of data-driven fleet optimization. Operators are increasingly prioritizing predictive maintenance, driver behavior monitoring, and fuel efficiency. The rising use of AI-enabled analytics, cloud-based platforms, and mobile monitoring applications further drives market growth. Moreover, regulatory mandates on fleet safety, emissions tracking, and telematics adoption are significantly contributing to the market’s expansion.

Europe Commercial Telematics Market Insight

The Europe commercial telematics market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent transportation regulations, sustainability initiatives, and the rising need for operational efficiency. Increasing urbanization and congestion management are fostering the adoption of fleet telematics solutions. European operators are also leveraging telematics to reduce emissions, optimize routes, and enhance vehicle utilization. The region is witnessing significant uptake across logistics, construction, and public service fleets.

U.K. Commercial Telematics Market Insight

The U.K. commercial telematics market is expected to witness strong growth from 2026 to 2033, driven by the increasing need for fleet optimization, driver safety, and operational cost reduction. Adoption is also encouraged by government incentives for connected vehicle technologies and stringent regulatory frameworks for transport operations. Integration with cloud analytics, smartphone applications, and IoT-enabled monitoring is enhancing the efficiency and scalability of telematics solutions in both private and public fleets.

Germany Commercial Telematics Market Insight

The Germany commercial telematics market is expected to witness rapid growth from 2026 to 2033, fueled by advanced digital infrastructure, high fleet density, and a focus on sustainable logistics. Operators are adopting telematics solutions to monitor emissions, reduce fuel consumption, and improve fleet performance. The integration of telematics with predictive maintenance, route optimization, and AI analytics is becoming increasingly prevalent, aligning with local priorities for efficiency, safety, and environmental compliance.

Asia-Pacific Commercial Telematics Market Insight

The Asia-Pacific commercial telematics market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising vehicle sales, increasing e-commerce and logistics activities, and growing adoption of fleet management technologies in countries such as China, India, and Japan. Government initiatives promoting smart transportation and digital fleet solutions are further supporting market expansion. The region’s emergence as a manufacturing hub for telematics hardware and software is improving affordability and accessibility for small and medium fleet operator.

Japan Commercial Telematics Market Insight

The Japan commercial telematics market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced technological ecosystem, high fleet density, and demand for operational efficiency. Adoption is driven by the increasing integration of AI-based analytics, IoT monitoring, and mobile fleet management platforms. Telematics solutions are increasingly used for predictive maintenance, driver safety, and fuel optimization. The rising need for connected emergency and healthcare transport vehicles also supports market expansion.

China Commercial Telematics Market Insight

The China commercial telematics market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, high logistics demand, and rising investment in connected fleet infrastructure. Telematics adoption is increasing across transportation, delivery, and construction fleets to improve route efficiency, reduce operational costs, and monitor driver behavior. The push toward smart cities, coupled with strong domestic telematics providers and affordable solutions, is driving widespread market growth across the country.

Commercial Telematics Market Share

The Commercial Telematics industry is primarily led by well-established companies, including:

• AirIQ Inc. (U.S.)

• Bridgestone Corporation (Japan)

• Geotab Inc. (Canada)

• Omnitracs (U.S.)

• General Motors (U.S.)

• Masternaut Limited (U.K.)

• Mix Telematics International (South Africa)

• Octo Group S.p.A (Italy)

• Trimble Inc. (U.S.)

• Verizon (U.S.)

• Zonar Systems (U.S.)

• PTC (U.S.)

• TomTom International BV (Netherlands)

• Daimler AG (Germany)

• SenSight Technologies Pvt. Ltd (India)

• TELTONIKA (Lithuania)

• AB Volvo (Sweden)

• Ryder System, Inc. (U.S.)

• GPS Insight (U.S.)

Latest Developments in Global Commercial Telematics Market

- In February 2024, Geotab and Daimler Truck North America (DTNA) collaborated to integrate Freightliner truck data with Geotab’s MyGeotab platform. This development enables fleet operators to access unified real-time data without additional hardware, improving operational decision-making, safety, and sustainability. The solution is expected to enhance efficiency across commercial fleets and strengthen the adoption of integrated telematics in North America

- In February 2024, Phillips Connect and Noregon partnered to integrate Connect1 trailer data into TripVision Remote Diagnostics. The collaboration provides detailed insights into trailer health and brake performance, helping fleets optimize maintenance schedules and reduce downtime. This integration supports improved operational efficiency, cost savings, and wider adoption of connected diagnostics in commercial fleets

- In September 2023, Airbiquity partnered with Tessolve to integrate OTAmatic and LOGmatic with Tessolve’s TERA devices. The initiative enables secure software updates and flexible data logging for connected vehicles while streamlining OEM development and deployment. The collaboration strengthens telematics functionality, enhances data management, and accelerates the adoption of connected vehicle solutions

- In August 2022, MiX Telematics partnered with Hino Trucks’ Edge platform to provide data services to MiX customers operating Hino trucks in North America. The development allows fleet operators to monitor maintenance, safety, efficiency, and compliance in real time without aftermarket hardware. This collaboration improves fleet performance and supports broader adoption of OEM-integrated telematics solution

- In January 2022, Qualcomm Technologies, Inc. and Renault Group expanded their collaboration to equip upcoming vehicles with Snapdragon Digital Chassis platforms. The initiative delivers connected, intelligent, and scalable automotive telematics solutions, enhancing digital cockpits, driver assistance, and in-vehicle connectivity. This development drives innovation in vehicle telematics, promotes safer operations, and strengthens market growth for connected automotive solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.