Global Construction Lubricants Market

Market Size in USD Billion

CAGR :

%

USD

10.89 Billion

USD

15.72 Billion

2025

2033

USD

10.89 Billion

USD

15.72 Billion

2025

2033

| 2026 –2033 | |

| USD 10.89 Billion | |

| USD 15.72 Billion | |

| % | |

|

Construction Lubricants Market Size

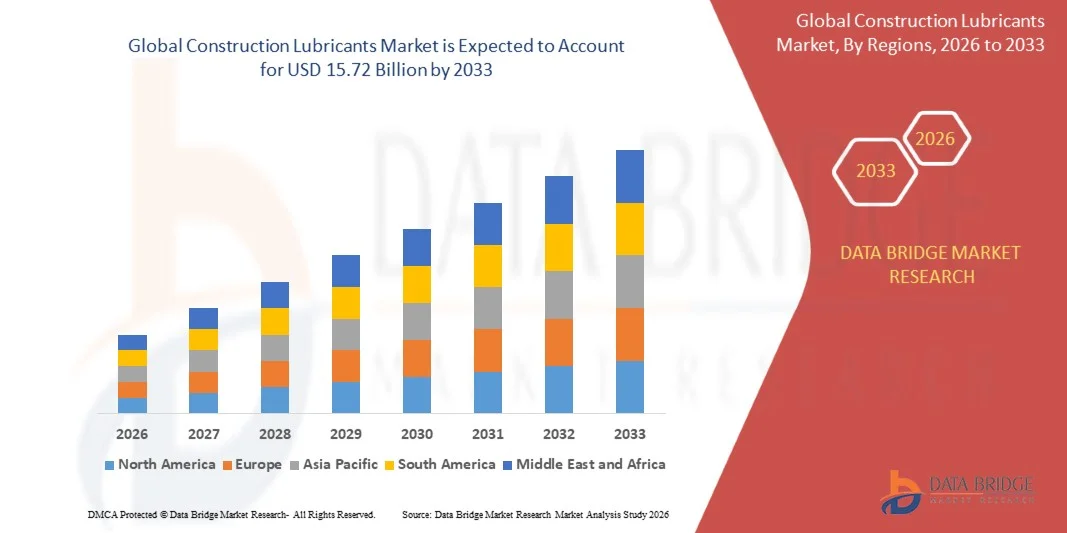

- The global construction lubricants market size was valued at USD 10.89 billion in 2025 and is expected to reach USD 15.72 billion by 2033, at a CAGR of 4.69% during the forecast period

- The market growth is largely fueled by the increasing mechanization in construction activities and rising investments in infrastructure development across emerging and developed economies. The adoption of heavy machinery and advanced construction equipment is driving higher consumption of specialized lubricants, thereby significantly boosting market demand

- Furthermore, growing emphasis on equipment longevity, operational efficiency, and reduced maintenance costs is creating strong demand for high-performance and synthetic lubricants. For instance, companies such as Shell and ExxonMobil are introducing advanced lubricants tailored for heavy-duty machinery, which is accelerating the uptake of premium construction lubricants and driving industry growth

Construction Lubricants Market Analysis

- Construction lubricants are specialized oils, greases, and fluids designed to reduce friction, wear, and operational downtime in construction machinery and equipment. They include hydraulic fluids, engine oils, gear oils, greases, and other products formulated to withstand extreme loads, temperatures, and environmental conditions

- The escalating demand for construction lubricants is primarily fueled by rapid infrastructure expansion, urbanization, and the growing use of technologically advanced construction equipment. In addition, rising environmental regulations and the focus on sustainable, eco-friendly lubricants are encouraging manufacturers to develop high-performance, biodegradable products for construction applications

- Asia-Pacific dominated the construction lubricants market with a share of 47.29% in 2025, due to rapid infrastructure development, increasing construction activities, and strong demand for heavy machinery across emerging economies

- North America is expected to be the fastest growing region in the construction lubricants market during the forecast period due to increasing investments in infrastructure modernization, rising construction activities, and strong demand for advanced construction equipment

- Mineral oil segment dominated the market with a market share of 63% in 2025, due to its cost-effectiveness and widespread availability across construction activities. Contractors and equipment operators prefer mineral oil-based lubricants due to their adequate performance in standard operating conditions and lower upfront costs

Report Scope and Construction Lubricants Market Segmentation

|

Attributes |

Construction Lubricants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Construction Lubricants Market Trends

“Rising Adoption of Synthetic and High-Performance Lubricants”

- A significant trend in the construction lubricants market is the increasing use of synthetic and high-performance lubricants across heavy machinery and construction equipment, driven by the need to enhance equipment longevity, reduce maintenance frequency, and improve operational efficiency in challenging environments. This trend is elevating the demand for advanced formulations that can withstand extreme temperatures, high loads, and prolonged usage in construction sites

- For instance, Shell and ExxonMobil offer synthetic lubricants and high-performance oils tailored for excavators, loaders, and cranes, helping contractors reduce downtime and extend machinery life under harsh conditions. Such offerings strengthen equipment reliability and ensure continuous operations on large-scale construction projects

- The shift toward mechanized construction is accelerating lubricant consumption, as modern machinery requires specialized oils and greases to maintain optimal performance. This is positioning construction lubricants as essential enablers for productivity gains and operational safety in construction operations

- Equipment manufacturers and contractors are increasingly prioritizing environmentally friendly lubricants that reduce emissions, improve fuel efficiency, and meet regulatory compliance. This trend is driving the development of biodegradable and low-VOC lubricant formulations in the market

- Industries focusing on infrastructure development are expanding their use of multi-functional lubricants that provide anti-wear, anti-oxidation, and corrosion protection properties, ensuring smoother operation of hydraulic systems and engines. This is shaping a stronger preference for performance-enhancing lubricant solutions capable of sustaining demanding industrial conditions

- The market is witnessing robust growth in specialty lubricants for emerging applications such as tunnel boring machines, mining-related construction, and high-capacity cranes. This rising incorporation of high-performance lubricants reinforces the overall transition toward reliable, efficient, and environmentally sustainable machinery operations across global construction projects

Construction Lubricants Market Dynamics

Driver

“Growing Infrastructure Development and Mechanization in Construction”

- The expansion of global infrastructure projects, including highways, railways, and urban development, is driving the demand for construction lubricants that ensure smooth operation and longevity of heavy machinery. Mechanization across construction sites is increasing reliance on advanced lubricants for equipment performance

- For instance, Caterpillar integrates high-performance lubricants in its construction machinery, enabling sustained operation in large-scale infrastructure projects worldwide. This adoption supports continuous productivity and reduces equipment wear under intense operational loads

- Urbanization and rising construction activity in emerging economies are boosting the use of hydraulic oils, engine oils, and greases to maintain equipment efficiency. This is increasing lubricant consumption in both private and government construction initiatives

- The mining and heavy civil engineering sectors require specialized lubricants to handle abrasive and high-load conditions, driving the demand for robust and durable formulations. Construction lubricants are critical in reducing downtime and optimizing machinery lifecycle in these sectors

- The overall increase in mechanization, combined with regulatory emphasis on equipment efficiency and sustainability, continues to accelerate the adoption of advanced construction lubricants across the globe

Restraint/Challenge

“Volatility in Base Oil Prices and Supply Chain Constraints”

- The construction lubricants market faces challenges due to fluctuations in crude oil prices and base oil availability, which directly impact production costs and market pricing. Supply chain disruptions can create shortages of key raw materials and delay lubricant delivery to construction sites

- For instance, BP and TotalEnergies have experienced cost pressures due to global crude oil volatility, influencing the pricing of their construction lubricant products. These fluctuations challenge manufacturers to maintain stable supply and competitive pricing

- The reliance on imported base oils and additives makes manufacturers vulnerable to geopolitical tensions, trade restrictions, and logistical bottlenecks. This affects timely production and distribution of essential lubricant products

- High demand during peak construction periods can strain supply networks, causing shortages or delays for hydraulic, engine, and transmission oils. Maintaining inventory and ensuring consistent availability remain critical challenges for market players

- The market continues to encounter constraints related to balancing high-quality lubricant production with economic feasibility under volatile raw material conditions. These challenges collectively compel manufacturers to optimize sourcing strategies and strengthen supply chain resilience to meet construction industry demands

Construction Lubricants Market Scope

The market is segmented on the basis of base oil, equipment type, product type, and application.

• By Base Oil

On the basis of base oil, the construction lubricants market is segmented into mineral oil and synthetic oil. The mineral oil segment dominated the largest market revenue share of 63% in 2025, driven by its cost-effectiveness and widespread availability across construction activities. Contractors and equipment operators prefer mineral oil-based lubricants due to their adequate performance in standard operating conditions and lower upfront costs. These lubricants are extensively used in developing regions where cost sensitivity remains high and large-scale infrastructure projects demand economical lubrication solutions. The established supply chain and familiarity among end users further strengthen the dominance of mineral oil in the market.

The synthetic oil segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its superior performance characteristics and longer service intervals. Synthetic lubricants offer enhanced thermal stability, oxidation resistance, and improved efficiency in extreme operating environments, making them suitable for advanced construction machinery. Increasing adoption of high-performance and technologically advanced equipment drives the demand for synthetic oils. In addition, growing awareness regarding equipment longevity and reduced maintenance costs contributes to the rising shift toward synthetic-based lubricants.

• By Equipment Type

On the basis of equipment type, the construction lubricants market is segmented into earthmoving equipment, material handling equipment, heavy construction vehicles, and others. The earthmoving equipment segment dominated the largest market revenue share in 2025, driven by its extensive usage in large-scale construction and infrastructure development projects. Equipment such as excavators, loaders, and bulldozers require continuous lubrication for efficient operation under heavy loads and harsh environments. The high operational intensity and frequent usage of these machines significantly increase lubricant consumption. Growing investments in road construction, mining, and urban development further reinforce the dominance of this segment.

The material handling equipment segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for efficient logistics and warehouse operations at construction sites. Equipment such as cranes, forklifts, and hoists require specialized lubricants to ensure smooth functioning and safety. The expansion of large-scale construction projects and industrial facilities increases the need for advanced material handling solutions. In addition, automation trends and rising focus on operational efficiency contribute to higher adoption of lubricants in this segment.

• By Product Type

On the basis of product type, the construction lubricants market is segmented into hydraulic fluid, engine oil, gear oil, automatic transmission fluid (ATF), compressor oil, grease, and others. The hydraulic fluid segment dominated the largest market revenue share in 2025, driven by its critical role in operating hydraulic systems across construction equipment. Hydraulic systems are widely used in machinery such as excavators and loaders, requiring consistent lubrication to maintain pressure and efficiency. The continuous demand for smooth operation and reduced wear and tear supports the extensive use of hydraulic fluids. Increasing mechanization in construction activities further drives the dominance of this segment.

The grease segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its ability to provide long-lasting lubrication and protection in high-load applications. Grease is widely used in components exposed to dust, moisture, and extreme conditions, offering superior sealing and resistance properties. The rising need for reducing maintenance frequency and improving equipment durability supports its adoption. In addition, advancements in grease formulations enhance performance, further accelerating its demand in construction operations.

• By Application

On the basis of application, the construction lubricants market is segmented into commercial and personal. The commercial segment dominated the largest market revenue share in 2025, driven by extensive use of construction equipment in infrastructure development, industrial projects, and large-scale commercial construction activities. High equipment utilization rates and continuous operations significantly increase lubricant consumption in this segment. Government investments in infrastructure development and urbanization projects further boost demand for construction lubricants in commercial applications. The presence of large construction firms and contractors also supports segment dominance.

The personal segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing small-scale construction, renovation, and residential development activities. Rising disposable income and growing interest in home improvement projects contribute to higher demand for lubricants used in small machinery and tools. The availability of compact and user-friendly equipment supports lubricant usage among individual users. In addition, the expansion of the DIY construction trend further accelerates growth in this segment.

Construction Lubricants Market Regional Analysis

- Asia-Pacific dominated the construction lubricants market with the largest revenue share of 47.29% in 2025, driven by rapid infrastructure development, increasing construction activities, and strong demand for heavy machinery across emerging economies

- The region’s cost-effective manufacturing environment, rising government investments in transportation and urban development projects, and expanding construction sector are accelerating market growth

- The availability of low-cost labor, favorable government initiatives, and ongoing industrialization across developing countries are contributing to increased consumption of construction lubricants in large-scale projects

China Construction Lubricants Market Insight

China held the largest share in the Asia-Pacific construction lubricants market in 2025, owing to its massive construction industry and continuous investments in infrastructure development. The country’s strong manufacturing base for construction equipment, coupled with government-backed urbanization and smart city initiatives, drives lubricant demand. High usage of heavy machinery across residential, commercial, and industrial projects further strengthens market growth.

India Construction Lubricants Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by expanding infrastructure projects, rising urbanization, and increasing government initiatives such as Smart Cities Mission and Make in India. Growing investments in roads, railways, and housing development significantly increase the demand for construction equipment and lubricants. In addition, the rapid growth of the real estate sector and industrial expansion are supporting market expansion.

Europe Construction Lubricants Market Insight

The Europe construction lubricants market is expanding steadily, supported by strong regulatory standards, demand for high-performance lubricants, and increasing focus on sustainability. The region emphasizes the use of advanced lubricants that enhance equipment efficiency and reduce environmental impact. Rising renovation activities and infrastructure upgrades across developed economies are further contributing to market growth.

Germany Construction Lubricants Market Insight

Germany’s construction lubricants market is driven by its advanced engineering capabilities, strong presence of construction equipment manufacturers, and emphasis on high-quality industrial operations. The country’s focus on precision, efficiency, and sustainability supports the adoption of high-performance lubricants. Increasing investments in infrastructure modernization and industrial construction further boost demand.

U.K. Construction Lubricants Market Insight

The U.K. market is supported by ongoing infrastructure development, renovation of aging structures, and rising adoption of advanced construction technologies. The demand for efficient and environmentally compliant lubricants is increasing due to strict regulatory frameworks. Growth in commercial construction and public infrastructure projects continues to support lubricant consumption.

North America Construction Lubricants Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing investments in infrastructure modernization, rising construction activities, and strong demand for advanced construction equipment. Technological advancements and the adoption of high-performance lubricants are enhancing operational efficiency. In addition, the focus on reducing maintenance costs and improving equipment lifespan supports market expansion.

U.S. Construction Lubricants Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its well-established construction sector, significant infrastructure investments, and strong presence of equipment manufacturers. The country’s focus on innovation, efficiency, and sustainability drives the adoption of advanced lubricant solutions. Increasing residential and commercial construction activities further strengthen market growth in the region.

Construction Lubricants Market Share

The construction lubricants industry is primarily led by well-established companies, including:

- Royal Dutch Shell (Netherlands)

- ExxonMobil (U.S.)

- BP (U.K.)

- Chevron Corporation (U.S.)

- TotalEnergies SE (France)

- Sinopec (China)

- Indian Oil Corporation (India)

- PetroChina Company Limited (China)

- Lukoil (Russia)

- Phillips 66 Company (U.S.)

- Bel-Ray Company LLC (U.S.)

- Morris Lubricants (U.K.)

- Penrite Oil (Australia)

- Valvoline (U.S.)

- Liqui Moly GmbH (Germany)

- ENI S.p.A. (Italy)

- Addinol Lube Oil GmbH (Germany)

- Lubrication Engineers, Inc. (U.S.)

- FUCHS Petrolub SE (Germany)

- Lubricating Specialties Company (U.S.)

- Southern Lubrication (Pvt) Ltd. (Pakistan)

- Schaeffer Manufacturing Co. (U.S.)

- AFRILUBE (South Africa)

- Leahy-Wolf (U.S.)

- QALCO (U.S.)

Latest Developments in Global Construction Lubricants Market

- In September 2025, ExxonMobil announced a partnership with a leading construction equipment manufacturer to co-develop advanced lubricant formulations for high-performance machinery. This collaboration is expected to strengthen ExxonMobil’s position in the construction lubricants market by delivering products specifically optimized for equipment performance and durability. By integrating lubricant design with machinery requirements, the company can enhance customer satisfaction, reduce maintenance needs, and create a competitive advantage through tailored, high-performance solutions

- In August 2025, Shell launched a new line of biodegradable lubricants designed for construction machinery. This initiative reinforces Shell’s leadership in sustainable solutions and addresses the increasing demand for environmentally friendly lubricants in the construction sector. By offering eco-conscious products without compromising performance, Shell is poised to capture market share among construction firms prioritizing sustainability, while simultaneously enhancing its brand reputation and aligning with global green construction trends

- In May 2023, BIGBEN introduced ScaffOil, a high-performance and eco-friendly lubricant tailored for scaffolding and general construction applications. Its superior penetrating ability and weather resistance provide enhanced durability and operational efficiency for construction operations. This launch represents a strategic advancement in construction lubricants, positioning BIGBEN as a provider of specialized products that meet evolving sector demands for long-lasting and environmentally responsible solutions

- In June 2022, Volvo Construction Equipment launched Volvo Hydraulic Oil 98611 HO103, a lubricant extending drain intervals in crawler excavators to 3,000 hours. The product improves equipment longevity, optimizes fuel efficiency, and reduces oil consumption, while offering multiple viscosity options. Its introduction is considered a technological milestone, strengthening Volvo’s presence in the construction lubricants market by enhancing operational efficiency and aligning with environmental performance expectations

- In March 2022, BPCL launched four new MAK lubrication products aimed at improving performance, dependability, and durability for construction equipment. These offerings are expected to bolster BPCL’s market position by meeting the growing demand for reliable and high-performance lubricants, thereby enabling customers to maintain equipment efficiency and extend service intervals in challenging construction environments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Construction Lubricants Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Construction Lubricants Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Construction Lubricants Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.