Global Container Liner Market

Market Size in USD Billion

CAGR :

%

USD

975.30 Billion

USD

1,519.63 Billion

2025

2033

USD

975.30 Billion

USD

1,519.63 Billion

2025

2033

| 2026 –2033 | |

| USD 975.30 Billion | |

| USD 1,519.63 Billion | |

| % | |

|

Container Liner Market Overview

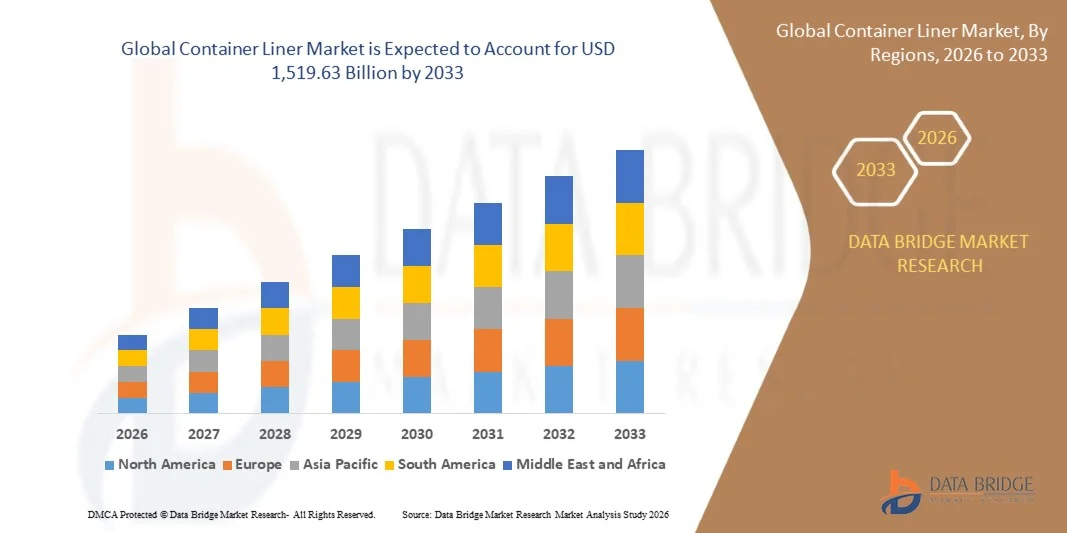

The global container liner market was valued at USD 975.30 billion in 2025 and is projected to reach USD 1,519.63 billion by 2033, growing at a CAGR of 5.70% from 2026 to 2033. The market is witnessing steady expansion driven by rising international trade volumes, increasing containerized cargo transportation, and growing demand for efficient and cost-effective ocean freight services across long-distance trade routes. Container liners play a critical role in global supply chains by enabling standardized shipping of goods across industries such as retail, manufacturing, automotive, and chemicals.

The growing integration of digital freight platforms, automated vessel tracking systems, and optimized route planning is further enhancing operational efficiency and reducing transit costs for shipping operators. In addition, increasing port modernization activities and expansion of major shipping alliances are strengthening global connectivity and capacity utilization. Rising e-commerce cross-border shipments and demand for reliable just-in-time delivery are also accelerating the adoption of container liner services, particularly across high-volume Asia–Europe and Asia–North America trade corridors.

Key Market Trends & Insights

- North America dominated the container liner market with the largest revenue share of approximately 36.7% in 2025, supported by strong import demand for manufactured goods, chemicals, and consumer products, along with well-established port infrastructure across the U.S. and Canada.

- Asia-Pacific container liner market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding manufacturing output, and rising export activity across China, India, Japan, South Korea, and Southeast Asia.

- The Polypropylene segment held the largest market revenue share of approximately 46.2% in 2025, driven by its high tensile strength, chemical resistance, and widespread use in dry bulk cargo transportation across food grains, minerals, and industrial powders. Polypropylene liners are widely preferred due to their cost efficiency, durability, and compatibility with standard shipping containers used in global trade logistics.

- The Polyethylene segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing demand for moisture-resistant and flexible liner solutions in food-grade and pharmaceutical cargo transportation. Rising adoption in humidity-sensitive exports such as sugar, flour, and agricultural commodities is further supporting segment expansion.

- The 40 Foot segment held the largest market revenue share of approximately 58.5% in 2025, driven by its dominance in international freight movement and high-volume bulk cargo shipments across long-haul trade routes. Standardization of 40-foot containers in global shipping networks and their higher payload efficiency make them the preferred choice for exporters and logistics operators.

- The 20 Foot segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing demand for short-haul trade, regional distribution, and port-to-port flexibility in emerging economies. Smaller container formats are increasingly used in congested ports and inland logistics networks where maneuverability and faster turnaround time are critical.

- The End Fill segment held the largest market revenue share of approximately 42.7% in 2025, driven by its ease of installation, compatibility with standard container designs, and efficient discharge mechanism for bulk materials such as grains, resins, and minerals.

- The Wide Access segment is projected to register the fastest growth at a CAGR of 10.3% from 2026 to 2033, driven by rising demand for faster loading and unloading operations in high-volume logistics hubs. Increasing adoption in chemical and food ingredient transportation, where contamination control and operational efficiency are critical, is further accelerating segment growth.

- The Agriculture segment held the largest market revenue share of approximately 31.4% in 2025, driven by large-scale global trade of grains, cereals, and bulk agricultural commodities such as wheat, corn, and rice. Expanding international food trade and increasing demand for cost-efficient bulk transport solutions are further strengthening segment dominance.

- The Pharmaceuticals segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by rising global demand for temperature-sensitive and contamination-free transportation of active pharmaceutical ingredients and bulk drug intermediates. Increasing regulatory compliance requirements and expansion of pharmaceutical exports from Asia-Pacific economies are further supporting segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 975.30 Billion

- Expected Market Value (2033): USD 1,519.63 Billion

- Forecast CAGR (2026–2033): 5.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Container Liner Market Segmentation

|

Attributes |

Container Liner Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Greif (U.S.) |

|

Market Opportunities |

• Expansion Of Digital Freight Platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Container Liner Market Trends

Trend: Expansion Of Digital Freight Optimization And Decarbonized Shipping Networks

Increasing demand for efficient, cost-effective, and sustainable maritime logistics solutions is reshaping global container liner operations across major trade routes such as Asia–Europe and Asia–North America. Container shipping companies are increasingly adopting AI-based route optimization, real-time vessel tracking, and predictive demand planning systems to reduce fuel consumption, improve vessel utilization, and enhance schedule reliability.

In modern container liner operations, shipping giants are integrating digital twin technologies and automated port coordination systems, For instance to optimize berth allocation and reduce container dwell time, improving turnaround efficiency and lowering congestion at major ports such as Singapore and Rotterdam. In addition, carriers are increasingly deploying slow steaming strategies and LNG-powered vessels to comply with IMO 2023 carbon intensity regulations, reducing greenhouse gas emissions per voyage while maintaining cost competitiveness.

The rapid expansion of e-commerce cross-border trade and just-in-time manufacturing supply chains is also increasing demand for high-frequency liner services with enhanced reliability and transit visibility. In addition, global alliances such as 2M, Ocean Alliance, and THE Alliance continue to restructure service networks to improve capacity sharing and reduce operational redundancies. Fleet modernization programs launched in 2024–2025, including deployment of ultra-large container vessels exceeding 24,000 TEU capacity, are further improving economies of scale and reducing per-unit shipping costs in high-volume trade corridors.

Global Container Liner Market Dynamics

Key Market Driver: Rising Global Trade Volumes And Supply Chain Reconfiguration

The expansion of global trade, particularly in manufactured goods, electronics, automotive components, and consumer products, is a major driver of container liner demand. Increasing industrial output in Asia-Pacific economies, especially China, India, Vietnam, and South Korea, is supporting strong export flows, while reshoring and nearshoring trends in North America and Europe are reshaping shipping routes and increasing demand for flexible liner capacity.

Container shipping remains the backbone of global trade, accounting for nearly 80% of non-bulk goods transportation by volume. For instance, the Asia–Europe route continues to handle some of the highest container traffic globally, with millions of TEUs transported annually through major hubs such as Shanghai, Singapore, Rotterdam, and Hamburg. Shipping alliances such as 2M and THE Alliance are optimizing vessel deployment and schedule reliability to manage fluctuating demand patterns and port congestion challenges.

In addition, e-commerce expansion and just-in-time manufacturing models are increasing demand for frequent, smaller shipment cycles, pushing liner operators to enhance fleet agility and expand feeder network connectivity across secondary ports and emerging trade hubs.

Key Market Restraint/Challenge: Freight Rate Volatility And High Operational Costs

The container liner industry faces persistent challenges from freight rate volatility, driven by geopolitical tensions, fluctuating fuel prices, and global supply-demand imbalances. Spot freight rates experienced extreme fluctuations during 2021–2023 supply chain disruptions, followed by significant corrections as fleet capacity normalized and demand softened in certain trade lanes.

In addition, high capital expenditure associated with ultra-large vessel deployment, port infrastructure limitations, and increasing compliance costs for decarbonization regulations such as IMO 2023 emission targets are creating financial pressure on operators. Bunker fuel costs remain a major operational burden, accounting for a significant portion of voyage expenses, particularly for long-haul routes.

For instance, container shipping companies operating Panamax and post-Panamax vessels often face cost inefficiencies on underutilized routes, where lower load factors reduce profitability and increase per-container transportation costs. Limited port readiness in developing regions further restricts seamless adoption of mega-vessels, creating bottlenecks in global logistics networks.

Key Market Opportunity: Digitalization, Green Shipping, And Integrated Logistics Expansion

The container liner market is experiencing strong growth opportunities through digital transformation, sustainable shipping initiatives, and vertical integration into end-to-end logistics services. Shipping companies are increasingly investing in smart container technologies, blockchain-based documentation systems, and AI-enabled route optimization tools to improve transparency, reduce delays, and enhance supply chain resilience.

Liner operators are also expanding into logistics and freight forwarding services to capture higher value across the supply chain. For instance, carriers are developing integrated door-to-door solutions that combine ocean freight with inland transportation, warehousing, and last-mile delivery services, improving customer retention and revenue diversification.

In addition, the transition toward green shipping fuels and carbon-neutral operations is creating new investment opportunities in alternative fuel infrastructure and energy-efficient vessel design. Pilot projects involving methanol-powered container ships in Europe and Asia during 2025 are demonstrating significant reductions in greenhouse gas emissions, supporting long-term sustainability targets and regulatory compliance across global shipping networks.

Global Container Liner Market Scope

The market is segmented on the basis of material type, capacity, product type, and end-user application.

• By Material Type

On the basis of material type, the container liner market is segmented into Polypropylene, Polyvinyl Chloride (PVC), Polyethylene, Metalized Films, and Others. The Polypropylene segment held the largest market revenue share of approximately 46.2% in 2025, driven by its high tensile strength, chemical resistance, and widespread use in dry bulk cargo transportation across food grains, minerals, and industrial powders. Polypropylene liners are widely preferred due to their cost efficiency, durability, and compatibility with standard shipping containers used in global trade logistics.

The Polyethylene segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing demand for moisture-resistant and flexible liner solutions in food-grade and pharmaceutical cargo transportation. Rising adoption in humidity-sensitive exports such as sugar, flour, and agricultural commodities is further supporting segment expansion.

• By Capacity

On the basis of capacity, the container liner market is segmented into 20 Foot, 30 Foot, and 40 Foot containers. The 40 Foot segment held the largest market revenue share of approximately 58.5% in 2025, driven by its dominance in international freight movement and high-volume bulk cargo shipments across long-haul trade routes. Standardization of 40-foot containers in global shipping networks and their higher payload efficiency make them the preferred choice for exporters and logistics operators.

The 20 Foot segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing demand for short-haul trade, regional distribution, and port-to-port flexibility in emerging economies. Smaller container formats are increasingly used in congested ports and inland logistics networks where maneuverability and faster turnaround time are critical.

• By Product Type

On the basis of product type, the container liner market is segmented into End Fill, Open Top, Top Fill, and Wide Access liners. The End Fill segment held the largest market revenue share of approximately 42.7% in 2025, driven by its ease of installation, compatibility with standard container designs, and efficient discharge mechanism for bulk materials such as grains, resins, and minerals.

The Wide Access segment is projected to register the fastest growth at a CAGR of 10.3% from 2026 to 2033, driven by rising demand for faster loading and unloading operations in high-volume logistics hubs. Increasing adoption in chemical and food ingredient transportation, where contamination control and operational efficiency are critical, is further accelerating segment growth.

• By End-User

On the basis of end-user, the container liner market is segmented into Agriculture, Chemical, Building and Construction, Mining, Food and Beverages, and Pharmaceuticals. The Agriculture segment held the largest market revenue share of approximately 31.4% in 2025, driven by large-scale global trade of grains, cereals, and bulk agricultural commodities such as wheat, corn, and rice. Expanding international food trade and increasing demand for cost-efficient bulk transport solutions are further strengthening segment dominance.

The Pharmaceuticals segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by rising global demand for temperature-sensitive and contamination-free transportation of active pharmaceutical ingredients and bulk drug intermediates. Increasing regulatory compliance requirements and expansion of pharmaceutical exports from Asia-Pacific economies are further supporting segment growth.

Global Container Liner Market Regional Analysis

North America Container Liner Market Insight

North America dominated the container liner market with the largest revenue share of approximately 36.7% in 2025, supported by strong import demand for manufactured goods, chemicals, and consumer products, along with well-established port infrastructure across the U.S. and Canada. The region benefits from high containerized trade volumes through major ports such as Los Angeles, Long Beach, New York–New Jersey, and Vancouver. Increasing reliance on efficient maritime logistics, coupled with supply chain diversification away from single-source regions, is further strengthening container liner demand. In addition, growing adoption of digital freight platforms and integrated logistics solutions is improving vessel utilization and operational efficiency across transpacific trade routes.

U.S. Container Liner Market Insight

The U.S. container liner market captured the largest revenue share in 2025 within North America, driven by high import dependency on Asia-Pacific manufacturing hubs and strong consumption of electronics, automotive parts, and retail goods. The expansion of e-commerce and omnichannel retail networks is significantly increasing containerized shipment volumes through major gateways such as the Ports of Los Angeles, Long Beach, and Savannah. In addition, strategic investments in port modernization, automation, and inland intermodal connectivity are enhancing cargo handling efficiency. The growing presence of major liner operators such as Hapag-Lloyd and CMA CGM in U.S. trade lanes is further supporting market expansion through improved service reliability and capacity deployment.

Europe Container Liner Market Insight

The Europe container liner market is expected to witness steady growth from 2026 to 2033, driven by stringent environmental regulations, expansion of green shipping initiatives, and strong intra-regional trade. Increasing focus on decarbonization under IMO emission frameworks and EU climate targets is accelerating the adoption of low-emission vessels and alternative fuels such as LNG and green methanol. Major European ports such as Rotterdam, Hamburg, and Antwerp are enhancing infrastructure to support larger vessels and digitalized cargo handling systems. Rising demand for resilient supply chains and nearshoring of manufacturing activities is also contributing to stable container liner demand across the region.

U.K. Container Liner Market Insight

The U.K. container liner market is expected to witness steady growth from 2026 to 2033, supported by strong import demand for consumer goods, machinery, and automotive components. Post-Brexit trade realignment has increased the importance of efficient maritime connectivity with Europe, North America, and Asia. The expansion of major ports such as Felixstowe, Southampton, and London Gateway is enhancing container handling capacity and reducing congestion. In addition, increasing adoption of digital shipping documentation and automated port operations is improving turnaround times and operational efficiency across U.K. trade routes.

Germany Container Liner Market Insight

The Germany container liner market is expected to witness stable growth from 2026 to 2033, driven by the country’s strong industrial base, export-oriented economy, and high dependence on maritime logistics. Germany serves as a key gateway for European trade through major ports such as Hamburg and Bremerhaven. Growing exports of automotive components, machinery, and chemicals are sustaining container shipping demand. In addition, investments in smart port infrastructure and sustainable shipping practices are supporting the transition toward low-emission maritime logistics aligned with national and EU climate objectives.

Asia-Pacific Container Liner Market Insight

The Asia-Pacific container liner market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding manufacturing output, and rising export activity across China, India, Japan, South Korea, and Southeast Asia. The region accounts for the majority of global container throughput, with major ports such as Shanghai, Singapore, Ningbo-Zhoushan, and Shenzhen handling significant trade volumes. Increasing participation in global value chains, coupled with growing intra-Asia trade, is further driving container liner demand. In addition, strong presence of leading carriers such as COSCO Shipping Lines and Evergreen Marine Corporation is enhancing capacity expansion and route optimization across key shipping lanes.

Japan Container Liner Market Insight

The Japan container liner market is expected to witness steady growth from 2026 to 2033, driven by strong export demand for automobiles, electronics, and industrial machinery. Japan’s highly developed port infrastructure and strategic location in Asia-Pacific trade routes support efficient container movement through ports such as Yokohama, Nagoya, and Kobe. Increasing adoption of digital logistics systems and automated port operations is improving supply chain efficiency. In addition, Japan’s focus on carbon reduction in maritime transport is encouraging the use of energy-efficient vessels and alternative fuels in container shipping operations.

China Container Liner Market Insight

The China container liner market accounted for the largest market revenue share in Asia-Pacific in 2025, supported by its position as the world’s largest manufacturing hub and exporter of goods. Massive container throughput is handled through major ports such as Shanghai, Ningbo-Zhoushan, Shenzhen, and Guangzhou. Rapid growth in e-commerce exports, industrial production, and global trade integration continues to drive container shipping demand. Strong domestic carriers such as COSCO Shipping Holdings are further strengthening market capacity and global connectivity through fleet expansion and international route development.

Global Container Liner Market Share

The Container Liner industry is primarily led by well-established companies, including:

• Greif (U.S.)

• Thrace Group (Greece)

• Bemis Manufacturing Company (U.S.)

• LC Packaging (Netherlands)

• Berry Global Inc. (U.S.)

• UNITED BAGS, INC. (U.S.)

• DISPLAY PACK (U.S.)

• CDF Corporation (U.S.)

• Bulk Corp International (India)

• Emmbi, Inc. (India)

• Nier Systems Inc. (U.S.)

• Rishi FIBC Solutions PVT. Ltd. (India)

• Ven Pack (India)

• Umasree Texplast Pvt. Ltd. (India)

• Shree Tirupati Balajee FIBC Ltd (India)

• Jet Tech Pvt Ltd (India)

• Signode (U.S.)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Container Liner Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Container Liner Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Container Liner Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.