Global Dairy Products Processing Equipment Market

Market Size in USD Billion

CAGR :

%

USD

10.67 Billion

USD

16.75 Billion

2025

2033

USD

10.67 Billion

USD

16.75 Billion

2025

2033

| 2026 –2033 | |

| USD 10.67 Billion | |

| USD 16.75 Billion | |

| % | |

|

Dairy Products Processing Equipment Market Size

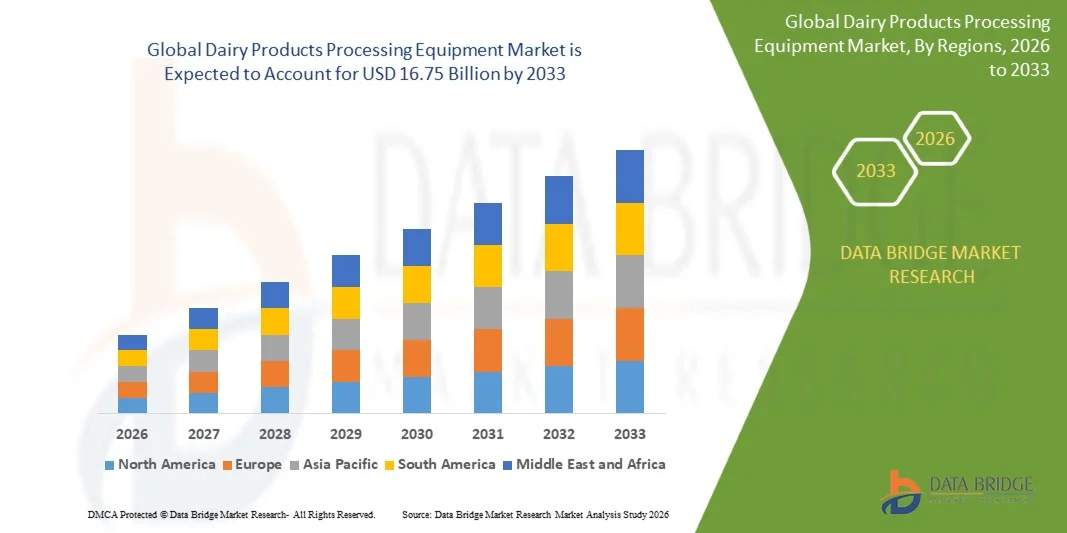

- The global dairy products processing equipment market size was valued at USD 10.67 billion in 2025 and is expected to reach USD 16.75 billion by 2033, at a CAGR of 5.80% during the forecast period

- The market growth is largely fueled by the increasing demand for processed and packaged dairy products, driven by rising population, urbanization, and changing dietary preferences toward milk, cheese, yogurt, and protein-rich dairy foods. The expansion of organized dairy supply chains and growing investment in modern dairy infrastructure are further supporting the adoption of advanced processing equipment across production facilities

- Furthermore, rising focus on food safety regulations, quality standardization, and automation in dairy production is accelerating the deployment of high-efficiency equipment such as pasteurizers, homogenizers, separators, and filtration systems. These converging factors are improving production efficiency, shelf-life, and product consistency, thereby significantly boosting the industry's growth

Dairy Products Processing Equipment Market Analysis

- Dairy products processing equipment includes machinery and systems used for processing raw milk into value-added dairy products such as pasteurized milk, butter, cheese, yogurt, and milk powder. These systems incorporate technologies for heating, cooling, separation, homogenization, drying, and packaging to ensure hygiene, efficiency, and product quality in dairy manufacturing operations

- The escalating demand for dairy processing equipment is primarily fueled by the rapid expansion of industrial dairy processing facilities, increasing automation in food manufacturing, and growing consumption of value-added dairy products supported by urbanization and rising disposable incomes globally

- Asia-Pacific dominated the dairy products processing equipment market with a share of 39.71% in 2025, due to strong dairy consumption, expanding milk production capacity, and rapid modernization of dairy processing infrastructure

- North America is expected to be the fastest growing region in the dairy products processing equipment market during the forecast period due to dairy products processing equipment market, driven by rising demand for processed dairy products and high adoption of automation in food processing plants

- Processed milk segment dominated the market with a market share of 36.46% in 2025, due to high global consumption and consistent demand from urban populations. Processing equipment used in this segment supports large-scale pasteurization, homogenization, and packaging operations, ensuring product safety and uniformity

Report Scope and Dairy Products Processing Equipment Market Segmentation

|

Attributes |

Dairy Products Processing Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· GEA Group (Germany) · SPX FLOW, Inc (U.S.) · Tetra Laval International S.A. (Switzerland) · Alfa Laval Corporate AB (Sweden) · John Bean Technologies Corporation (JBT) Corporation (U.S.) · IMA Industria Macchine Automatiche SPA (Italy) · IDMC Limited (India) · Feldmeier Equipment, Inc. (U.S.) · Scherjon Dairy Equipment Holland B.V. (Netherlands) · Coperion GmbH (Germany) · Van Den Heuvel Dairy & Food Equipment B.V. (Netherlands) |

|

Market Opportunities |

· Expansion of Dairy Processing Infrastructure in Emerging Economies · Growing Adoption of Energy-Efficient and Sustainable Processing Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Dairy Products Processing Equipment Market Trends

“Increasing Adoption of Automation and Smart Dairy Processing Systems”

- A significant trend in the dairy products processing equipment market is the increasing adoption of automation and smart processing systems, driven by the need for higher production efficiency, consistent product quality, and reduced operational dependency on manual labor across large-scale dairy facilities. This integration is enhancing process control in milk handling, separation, pasteurization, and packaging operations, strengthening overall productivity in dairy manufacturing plants

- For instance, DeLaval’s Milking Automation MA Series introduces automated monitoring and modular upgrade capabilities that improve efficiency in dairy operations, while GEA Group develops advanced separator and processing systems that enhance automation and energy optimization in large dairy plants. Such systems are enabling dairy producers to improve yield consistency and operational reliability across continuous production cycles

- The adoption of automated dairy processing technologies is increasing rapidly as producers aim to reduce human intervention in hygiene-sensitive processes such as milk pasteurization and cheese production. This is positioning automation as a core requirement for modern dairy infrastructure development across both developed and emerging markets

- The integration of digital monitoring systems and real-time process control is improving traceability, quality assurance, and production optimization in dairy processing plants. This is enabling manufacturers to maintain strict hygiene standards while improving operational decision-making and efficiency

- Dairy companies are increasingly investing in advanced processing lines that support continuous production, reduced downtime, and higher output scalability. This is strengthening the shift toward fully integrated and automated dairy production ecosystems

- The market is witnessing strong expansion in smart dairy processing solutions that combine automation, data analytics, and energy-efficient technologies. This growing integration is reshaping traditional dairy manufacturing into a more efficient, technology-driven production environment

Dairy Products Processing Equipment Market Dynamics

Driver

“Rising Demand for Processed and Value-Added Dairy Products”

- The growing consumption of processed and value-added dairy products such as cheese, yogurt, milk powder, and flavored dairy beverages is a key driver of the dairy products processing equipment market, supported by rising urbanization, changing dietary habits, and increasing protein-rich food demand. This is driving large-scale expansion of dairy processing facilities and modernization of production infrastructure globally

- For instance, Nestlé and Amul significantly contribute to the demand for advanced dairy processing equipment through large-scale production of packaged milk, yogurt, and cheese, requiring high-capacity pasteurizers, homogenizers, and filtration systems. These operations depend on efficient processing technologies to maintain consistent product quality and high-volume output

- The increasing preference for packaged and hygienically processed dairy products is encouraging dairy manufacturers to invest in automated and standardized processing equipment. This is improving shelf life, safety, and product consistency across dairy supply chains

- Rising health awareness and demand for protein-rich diets are boosting consumption of dairy-based nutritional products, further increasing reliance on advanced processing technologies. This is strengthening equipment adoption across both liquid and solid dairy segments

- The continuous growth in global dairy consumption patterns is reinforcing long-term investment in processing infrastructure. This sustained demand is strengthening the overall expansion of the dairy products processing equipment market

Restraint/Challenge

“High Capital Investment and Maintenance Costs of Advanced Equipment”

- The dairy products processing equipment market faces a major challenge due to the high capital investment required for advanced processing systems, including pasteurizers, separators, homogenizers, and automated production lines, which limits adoption among small and medium-scale dairy producers. These systems also require significant maintenance costs, skilled labor, and regular upgrades to maintain operational efficiency

- For instance, Tetra Pak’s advanced dairy processing lines and Alfa Laval’s high-performance separation systems involve substantial upfront investment and specialized maintenance requirements, making them more accessible to large dairy corporations rather than smaller processors. This creates a barrier for widespread adoption in cost-sensitive markets

- The installation of modern dairy processing equipment requires complex infrastructure, including temperature-controlled environments and integrated cleaning systems, which further increases overall project costs. This adds financial pressure on dairy manufacturers during capacity expansion

- Operational maintenance of high-precision equipment demands trained technical personnel and continuous servicing, increasing long-term operating expenditure. This impacts profitability for mid-sized dairy processors with limited budgets

- The combination of high initial investment and ongoing maintenance expenses continues to restrain rapid adoption of advanced dairy processing technologies. This challenge is particularly significant in developing regions where cost sensitivity remains high

Dairy Products Processing Equipment Market Scope

The market is segmented on the basis of type, application, operation, and distribution channel.

- By Type

On the basis of type, the Dairy Products Processing Equipment market is segmented into pasteurizers, homogenizers, mixers and blenders, separators, evaporators and dryers, membrane filtration equipment, and others. The pasteurizers segment dominated the largest market revenue share in 2025, driven by its critical role in ensuring microbial safety and extending shelf life of milk and dairy products. Dairy processors widely deploy pasteurizers as they are essential for compliance with food safety standards and maintaining consistent product quality across large-scale production facilities. The segment benefits from strong adoption in liquid milk processing plants where continuous thermal treatment is a core requirement. Rising demand for packaged dairy beverages further strengthens its leading position across both developed and emerging dairy industries.

The membrane filtration equipment segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by increasing demand for high-efficiency separation and protein concentration processes. This equipment is gaining traction due to its ability to process dairy products at lower temperatures while preserving nutritional value and improving yield. It is widely used in applications such as whey protein extraction and lactose reduction, which are gaining importance in functional dairy product manufacturing. The growing focus on premium dairy ingredients and value-added products continues to accelerate adoption across modern processing facilities.

- By Application

On the basis of application, the market is segmented into processed milk, fresh dairy products, butter and buttermilk, cheese, milk powder, and protein ingredients. The processed milk segment dominated the largest market revenue share of 36.46% in 2025, driven by high global consumption and consistent demand from urban populations. Processing equipment used in this segment supports large-scale pasteurization, homogenization, and packaging operations, ensuring product safety and uniformity. The segment benefits from strong distribution networks and continuous demand from retail and institutional buyers. Increasing preference for packaged and standardized milk products further reinforces its dominance in the market.

The protein ingredients segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for high-protein nutrition in sports, clinical, and functional food applications. Advanced dairy processing equipment is increasingly used to extract whey and casein proteins with higher purity and efficiency. This growth is supported by the expansion of protein-rich dietary trends and the development of fortified food products. Manufacturers are investing in advanced filtration and separation systems to meet quality requirements and diversify product offerings in this segment.

- By Operation

On the basis of operation, the market is segmented into automatic and semi-automatic systems. The automatic segment dominated the largest market revenue share in 2025, driven by increasing adoption of advanced processing lines in large dairy manufacturing facilities. Automation enhances production efficiency, reduces manual intervention, and ensures consistent product quality across high-volume operations. It also supports integration with digital monitoring systems for real-time process control and hygiene management. Growing demand for standardized and scalable dairy production continues to strengthen the dominance of fully automated systems.

The semi-automatic segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by its affordability and flexibility for small and medium-scale dairy processors. These systems allow partial automation while maintaining manual control over key processing stages, making them suitable for regional dairy plants. Increasing demand from developing dairy markets supports the adoption of cost-effective processing solutions. The segment benefits from gradual upgrades in traditional dairy units transitioning toward improved efficiency without full automation investment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hypermarkets, food specialty stores, convenience stores, and others. The hypermarkets segment dominated the largest market revenue share in 2025, driven by strong procurement of dairy products for mass retail distribution and private label offerings. These channels rely heavily on efficient processing equipment to ensure large-scale supply consistency and product standardization. Their extensive customer reach and high turnover rates support continuous demand for processed dairy goods. Expansion of organized retail networks further strengthens the dominance of this segment in the dairy processing ecosystem.

The food specialty stores segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by increasing demand for premium, organic, and artisanal dairy products. These outlets focus on differentiated product offerings that require advanced processing techniques for quality enhancement and flavor preservation. Growing consumer preference for niche dairy categories such as gourmet cheese and high-protein dairy snacks is driving equipment innovation. The segment is expanding as manufacturers target specialized retail channels to capture higher-margin opportunities.

Dairy Products Processing Equipment Market Regional Analysis

- Asia-Pacific dominated the dairy products processing equipment market with the largest revenue share of 39.71% in 2025, driven by strong dairy consumption, expanding milk production capacity, and rapid modernization of dairy processing infrastructure

- The region benefits from large-scale milk procurement systems, cost-efficient production facilities, and increasing adoption of automated dairy processing technologies across commercial dairies

- Rapid urbanization, rising demand for packaged dairy products, and growing investments in cold chain and processing facilities are accelerating market expansion

China Dairy Products Processing Equipment Market Insight

China held the largest share in the Asia-Pacific dairy products processing equipment market in 2025, supported by its extensive dairy processing industry and strong demand for liquid milk, yogurt, cheese, and milk powder products. The country has a well-developed food processing infrastructure enabling large-scale deployment of pasteurizers, separators, homogenizers, and membrane filtration systems in industrial dairy plants. Strong consumption growth in urban areas and expansion of leading dairy brands are further strengthening equipment demand. In addition, continuous automation upgrades and strict food safety regulations are driving modernization of dairy processing facilities.

India Dairy Products Processing Equipment Market Insight

India is witnessing the fastest growth in the Asia-Pacific dairy products processing equipment market, driven by rising milk production, increasing organized dairy processing, and growing demand for packaged and value-added dairy products. Expansion of dairy cooperatives and private sector investments is boosting adoption of processing equipment such as pasteurizers, mixers, and homogenizers. Government initiatives supporting dairy infrastructure development, cold chain expansion, and food processing modernization are further strengthening market growth. In addition, increasing consumption of milk, cheese, and yogurt is accelerating investment in advanced dairy processing technologies.

Europe Dairy Products Processing Equipment Market Insight

Europe is expanding steadily in the dairy products processing equipment market, supported by strong demand for cheese, yogurt, butter, and specialty dairy products. The region emphasizes advanced processing technologies, high hygiene standards, and energy-efficient dairy equipment systems across production facilities. Strict food safety regulations and sustainability mandates are encouraging adoption of automated and high-efficiency processing solutions. In addition, continuous innovation in dairy formulation and processing techniques is enhancing equipment modernization across the regional dairy industry.

Germany Dairy Products Processing Equipment Market Insight

Germany accounted for the largest share in the Europe dairy products processing equipment market in 2025, driven by its strong dairy manufacturing base and advanced food engineering capabilities. The country has extensive use of high-performance pasteurizers, separators, evaporators, and homogenizers in large-scale dairy production facilities. Strong R&D capabilities and advanced industrial automation support continuous innovation in dairy processing systems. In addition, export-oriented dairy production and the presence of leading equipment manufacturers are reinforcing Germany’s leadership in the regional market.

U.K. Dairy Products Processing Equipment Market Insight

The U.K. dairy products processing equipment market is supported by strong demand from packaged dairy, specialty cheese, and functional dairy product segments. Increasing focus on automation, efficiency, and product quality is driving adoption of modern dairy processing equipment across production facilities. The country’s strong food manufacturing and retail ecosystem supports consistent demand for advanced processing systems. In addition, sustainability initiatives and investment in energy-efficient dairy production are further strengthening market growth.

North America Dairy Products Processing Equipment Market Insight

North America is projected to grow at a strong CAGR from 2026 to 2033 in the dairy products processing equipment market, driven by rising demand for processed dairy products and high adoption of automation in food processing plants. Strong presence of large-scale dairy processors and advanced manufacturing infrastructure is supporting equipment demand across the region. Continuous technological innovation in processing efficiency, hygiene control, and energy optimization is further expanding market growth. In addition, increasing investments in dairy plant modernization and expansion of value-added dairy production are accelerating regional development.

U.S. Dairy Products Processing Equipment Market Insight

The U.S. accounted for the largest share in the North America dairy products processing equipment market in 2025, supported by strong demand from processed milk, cheese, yogurt, and protein-rich dairy products. The country benefits from highly advanced dairy processing infrastructure and strong adoption of automated, high-capacity processing equipment systems. Leading dairy companies are continuously investing in plant upgrades and advanced processing technologies to improve efficiency, product quality, and output consistency. In addition, strict food safety regulations and rising demand for functional dairy products are reinforcing the U.S. leadership position in the regional market.

Dairy Products Processing Equipment Market Share

The dairy products processing equipment industry is primarily led by well-established companies, including:

- GEA Group (Germany)

- SPX FLOW, Inc (U.S.)

- Tetra Laval International S.A. (Switzerland)

- Alfa Laval Corporate AB (Sweden)

- John Bean Technologies Corporation (JBT) Corporation (U.S.)

- IMA Industria Macchine Automatiche SPA (Italy)

- IDMC Limited (India)

- Feldmeier Equipment, Inc. (U.S.)

- Scherjon Dairy Equipment Holland B.V. (Netherlands)

- Coperion GmbH (Germany)

- Van Den Heuvel Dairy & Food Equipment B.V. (Netherlands)

Latest Developments in Global Dairy Products Processing Equipment Market

- In February 2025, Agathangelou introduced a fully automatic halloumi and grilled cheese production line, marking a significant shift toward advanced automation in dairy processing operations. This development is expected to enhance production efficiency, reduce reliance on manual labor, and improve product consistency in traditional cheese manufacturing. The system’s ability to reduce labor costs by up to 70% and increase yield by 2–3% highlights its strong impact on operational productivity and quality standardization within the dairy products processing equipment market

- In January 2025, DeLaval launched the Milking Automation MA Series, including MA100, MA200, and MA500 models, designed to improve automation in milking processes through real-time monitoring and modular system upgrades. This innovation is strengthening automation trends in the dairy equipment market by enabling higher efficiency, better herd management, and scalable adoption in conventional milking parlours. The integration of data-driven insights is further enhancing operational decision-making and supporting precision dairy farming practices

- In March 2024, GEA presented advanced separator technologies at Anuga FoodTec 2024, focusing on improving energy efficiency and operational performance in dairy processing systems. This innovation addresses key industry challenges such as rising energy costs and labor shortages by optimizing water and energy consumption in separation processes. It is expected to strengthen sustainability-driven demand for high-efficiency dairy processing equipment and support cost reduction across large-scale dairy operations

- In February 2024, Feldmeier Equipment Inc. announced an investment of over USD 20 million to expand its Shell Rock, Iowa facility with 130,000 square feet of advanced stainless steel manufacturing space. This expansion is expected to enhance production capacity for dairy processing equipment components, improve supply chain efficiency, and meet rising demand for hygienic stainless steel systems. It also reinforces the company’s position in supporting large-scale dairy infrastructure development in North America

- In January 2024, SPX FLOW, Inc. introduced the Seamless Infusion Vessel under its APV brand, designed to improve efficiency and hygiene in ingredient infusion processes for the food, beverage, and dairy industries. This innovation enhances sanitary processing standards by minimizing contamination risks through a crevice-free design and simplifying cleaning operations. It is expected to drive greater adoption of hygienic and efficient processing systems across dairy manufacturing facilities globally

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Dairy Products Processing Equipment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Dairy Products Processing Equipment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Dairy Products Processing Equipment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.