Global Defoamers Market

Market Size in USD Billion

CAGR :

%

USD

6.10 Billion

USD

8.87 Billion

2025

2033

USD

6.10 Billion

USD

8.87 Billion

2025

2033

| 2026 –2033 | |

| USD 6.10 Billion | |

| USD 8.87 Billion | |

| % | |

|

Defoamers Market Size

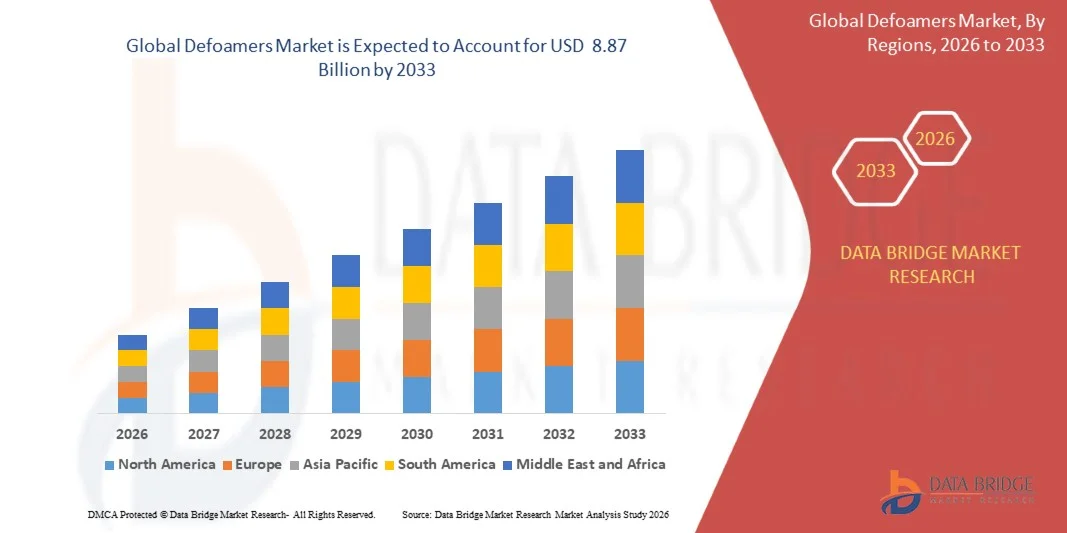

- The global defoamers market size was valued at USD 6.10 billion in 2025 and is expected to reach USD 8.87 billion by 2033, at a CAGR of 4.8% during the forecast period

- The market growth is largely fueled by the increasing use of defoamers across process-intensive industries such as paints & coatings, pulp & paper, water and wastewater treatment, and chemicals, where foam formation significantly impacts production efficiency and product quality

- Furthermore, rising demand for high-performance chemical additives, coupled with strict environmental regulations encouraging low-VOC and water-based formulations, is accelerating the adoption of advanced and sustainable defoaming solutions across industrial applications

Defoamers Market Analysis

- Defoamers are chemical additives designed to prevent or reduce foam formation in industrial processes by destabilizing foam bubbles and improving operational efficiency in liquid-based systems such as coatings, detergents, and wastewater treatment

- The increasing need for process optimization, improved product quality, and regulatory compliance in manufacturing industries is primarily driving the demand for defoamers across diverse end-use sectors

- Asia-Pacific dominated the defoamers market with a share of 38% in 2025, due to strong demand from paints & coatings, water and wastewater treatment, pulp & paper, and chemical processing industries

- North America is expected to be the fastest growing region in the defoamers market during the forecast period due to rising demand from water treatment, paints & coatings, and chemical manufacturing industries

- Silicone defoamers segment dominated the market with a market share of 38.4% in 2025, due to its superior efficiency in foam control across highly demanding industrial processes. These defoamers offer strong surface tension reduction, chemical stability, and compatibility across a wide range of formulations such as paints, coatings, and water treatment systems. Industries prefer silicone-based variants due to their long-lasting performance even under extreme temperature and pH conditions

Report Scope and Defoamers Market Segmentation

|

Attributes |

Defoamers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Defoamers Market Trends

“Increasing Adoption of Bio-Based and Sustainable Defoamer Solutions”

- A significant trend in the defoamers market is the increasing shift toward bio-based and sustainable formulations driven by stringent environmental regulations and growing demand for eco-friendly industrial chemicals. Industries such as paints & coatings, water treatment, and packaging are increasingly adopting low-VOC and biodegradable defoaming agents to align with sustainability targets and regulatory compliance requirements

- For instance, Evonik Industries AG introduced TEGO Foamex 8880, a bio-based defoamer for waterborne inks, reflecting the industry’s transition toward renewable and environmentally safer solutions. Such developments highlight the growing preference for green chemistry-based additives that maintain performance while reducing environmental impact

- The adoption of sustainable defoamers is also expanding across industrial wastewater treatment facilities where regulatory pressure from organizations such as the U.S. Environmental Protection Agency (EPA) and European Chemicals Agency (ECHA) is encouraging reduced chemical footprint. This is accelerating the replacement of conventional silicone and oil-based products with bio-based alternatives

- The paints & coatings industry is increasingly integrating waterborne and low-emission systems, which require advanced defoaming solutions compatible with eco-friendly formulations. This shift is strengthening demand for sustainable defoamers that ensure foam control without compromising coating quality or process efficiency

- Growing consumer and industrial awareness regarding environmental safety is further supporting the transition toward biodegradable chemical additives across manufacturing sectors. This is encouraging manufacturers to invest in innovation focused on renewable raw materials and sustainable product development

- The overall trend is reinforcing the long-term transformation of the defoamers market toward environmentally responsible chemical solutions that align with global sustainability frameworks and industrial decarbonization goals

Defoamers Market Dynamics

Driver

“Rising Demand from Water and Wastewater Treatment Applications”

- The increasing need for efficient water management systems is a key driver for the defoamers market, as foam formation in aeration tanks, filtration units, and chemical treatment processes can significantly reduce operational efficiency. Defoamers are widely used to improve process stability and ensure smooth operation in municipal and industrial wastewater treatment facilities

- For instance, BASF SE supplies Foamaster and Foamstar defoamers that are extensively used in wastewater treatment applications across multiple regions, supporting efficient foam control in large-scale treatment systems. These solutions help enhance oxygen transfer efficiency and reduce operational disruptions in treatment plants

- Rapid urbanization and industrial expansion are increasing wastewater generation globally, particularly from manufacturing, chemical processing, and food industries. This is creating sustained demand for defoaming agents to maintain compliance with environmental discharge standards and improve treatment efficiency

- Strict regulatory frameworks governing wastewater discharge quality are further driving adoption of advanced foam control solutions in treatment plants. Regulatory bodies are enforcing limits on effluent quality, which requires efficient chemical treatment processes supported by defoamers

- The continuous expansion of wastewater treatment infrastructure globally is reinforcing long-term demand for defoamers, positioning this application segment as a major growth driver for the market

Restraint/Challenge

“Stringent Environmental Regulations Limiting Conventional Chemical Use”

- The defoamers market faces challenges due to increasingly strict environmental regulations restricting the use of certain conventional chemical formulations, particularly those based on non-biodegradable or high-VOC compounds. Compliance requirements are forcing manufacturers to reformulate products, increasing complexity and development costs

- For instance, regulatory frameworks enforced by the European Chemicals Agency (ECHA) under REACH regulations have placed restrictions on specific chemical substances used in industrial additives, impacting traditional defoamer formulations. This has required companies to invest in reformulation and compliance testing

- Manufacturers face higher R&D expenses as they work to develop environmentally compliant alternatives that maintain performance standards while meeting regulatory thresholds. This increases production timelines and slows down product commercialization

- Industries such as coatings, textiles, and chemicals are under pressure to transition toward sustainable production processes, limiting the use of conventional silicone and oil-based defoamers. This creates adjustment challenges for both suppliers and end users

- The ongoing tightening of environmental norms continues to challenge market participants, requiring continuous innovation and adaptation to sustainable chemical solutions while maintaining cost competitiveness and performance efficiency

Defoamers Market Scope

The market is segmented on the basis of product type, medium of dispersion, and application.

• By Product Type

On the basis of product type, the defoamers market is segmented into powder, silicone defoamers, oil defoamers, emulsion defoamers, and polymer defoamers. The silicone defoamers segment dominated the largest market revenue share of 38.4% in 2025, driven by its superior efficiency in foam control across highly demanding industrial processes. These defoamers offer strong surface tension reduction, chemical stability, and compatibility across a wide range of formulations such as paints, coatings, and water treatment systems. Industries prefer silicone-based variants due to their long-lasting performance even under extreme temperature and pH conditions. Their ability to function in both low and high concentration systems further strengthens adoption across large-scale manufacturing environments. The segment continues to lead due to its established usage across mature end-use industries.

The emulsion defoamers segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by increasing demand for water-based formulations across multiple industries. For instance, waterborne coatings manufacturers are increasingly shifting toward emulsion-based defoamers to meet stricter environmental compliance and low-VOC requirements. These defoamers provide easy dispersion in aqueous systems and improve process efficiency in sectors such as textiles, food processing, and wastewater treatment. Their growing preference is also linked to enhanced stability and cost-effective formulation benefits compared to conventional alternatives. Expansion of sustainable chemical processing practices continues to accelerate adoption of emulsion-based solutions across emerging applications.

• By Medium of Dispersion

On the basis of medium of dispersion, the market is segmented into aqueous systems and non-aqueous or solvent systems. The aqueous systems segment held the largest market revenue share in 2025, driven by the widespread shift toward water-based formulations in industrial and consumer applications. These systems are extensively used in paints, coatings, detergents, and wastewater treatment processes where foam generation is a critical operational challenge. Strong regulatory push toward low-emission and environmentally safer formulations has further strengthened the dominance of aqueous-based defoamers. Their compatibility with a broad range of end-use industries enhances adoption across both developed and developing regions. The segment remains the primary choice due to its sustainability advantages and operational versatility.

The non-aqueous or solvent-based segment is expected to witness the fastest growth from 2026 to 2033, supported by demand from specialized industrial applications requiring high-performance chemical stability. For instance, solvent-based systems are increasingly used in petrochemical processing and heavy-duty industrial coatings where water-based alternatives are less effective. These defoamers provide superior performance in harsh chemical environments and high-temperature operations. Rising demand from niche manufacturing sectors and advanced chemical processing facilities is contributing to accelerated adoption. The segment continues to expand as industries seek tailored solutions for complex non-aqueous production environments.

• By Application

On the basis of application, the defoamers market is segmented into chemical formulation, textiles, construction materials, paints & coatings, pulp & paper, food processing, pharmaceuticals, household & personal care, and water and wastewater treatment. The paints & coatings segment dominated the largest market revenue share in 2025, driven by extensive use of defoamers in improving product quality, surface finish, and manufacturing efficiency. Foam formation during mixing and application processes creates defects, making defoamers essential for achieving smooth and uniform coatings. Strong demand from construction and automotive industries further supports segment leadership. Rapid industrialization and infrastructure development continue to sustain high consumption of coating materials globally. The segment remains central due to its broad industrial integration and consistent demand growth.

The water and wastewater treatment segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing global focus on clean water management and environmental sustainability. For instance, municipal and industrial wastewater treatment facilities are increasingly adopting advanced defoaming solutions to improve aeration efficiency and process stability. Rising water scarcity concerns and stricter discharge regulations are encouraging wider deployment of chemical treatment technologies. Defoamers play a critical role in reducing operational inefficiencies caused by excessive foam in treatment systems. Expanding investments in water infrastructure projects continue to accelerate demand for high-performance defoaming agents across regions.

Defoamers Market Regional Analysis

- Asia-Pacific dominated the defoamers market with the largest revenue share of 38% in 2025, driven by strong demand from paints & coatings, water and wastewater treatment, pulp & paper, and chemical processing industries

- The region benefits from large-scale industrial manufacturing base, rapid expansion of construction activities, and high consumption of process chemicals across multiple end-use sectors

- Strong industrialization, increasing investments in infrastructure development, and growing adoption of cost-efficient chemical additives are accelerating market expansion

China Defoamers Market Insight

China held the largest share in the Asia-Pacific defoamers market in 2025, supported by its extensive chemical manufacturing ecosystem and large-scale industrial production. Strong demand from paints & coatings, pulp & paper, and wastewater treatment industries is reinforcing market growth. The country’s well-established supply chain for specialty chemicals enables efficient production and distribution of defoaming agents. In addition, continuous expansion of manufacturing facilities and strict process efficiency requirements are strengthening China’s leadership in the regional market.

India Defoamers Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rapid expansion in construction, textiles, and water treatment industries. Government-led infrastructure development projects are increasing the use of paints, coatings, and construction materials requiring defoamers. Growing industrialization and rising adoption of chemical formulations in manufacturing processes are further supporting demand. In addition, increasing investments in wastewater treatment infrastructure are accelerating long-term market growth across the country.

Europe Defoamers Market Insight

The Europe defoamers market is expanding steadily, supported by strong demand from paints & coatings, pulp & paper, pharmaceuticals, and food processing industries. The region emphasizes high-performance and environmentally compliant chemical additives, driving adoption of advanced defoaming solutions. Strict environmental regulations are encouraging the use of low-VOC and sustainable formulations across industrial applications. In addition, technological advancements in chemical processing are supporting broader application of defoamers in specialized industries.

Germany Defoamers Market Insight

Germany accounted for the largest share in the Europe defoamers market in 2025, driven by its strong industrial manufacturing base and advanced chemical industry. High demand from automotive coatings, industrial processing, and machinery manufacturing is supporting market growth. The country’s focus on process efficiency and high-quality output is increasing adoption of advanced defoaming agents. In addition, strong R&D capabilities and established chemical production infrastructure are reinforcing Germany’s leadership in the regional market.

U.K. Defoamers Market Insight

The U.K. market is supported by strong demand from pharmaceuticals, food processing, and water treatment industries. Increasing focus on sustainable manufacturing practices is driving adoption of efficient defoaming solutions across production processes. The country’s well-developed industrial and chemical sectors are supporting steady market growth. In addition, rising investments in environmental management and wastewater treatment infrastructure are further contributing to market expansion.

North America Defoamers Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand from water treatment, paints & coatings, and chemical manufacturing industries. Strong focus on process optimization and regulatory compliance is increasing the use of high-performance defoamers. Technological advancements in specialty chemicals are further expanding application areas across industries. In addition, growing investments in industrial modernization and sustainable manufacturing are accelerating regional market growth.

U.S. Defoamers Market Insight

The U.S. accounted for the largest share in the North America defoamers market in 2025, supported by strong demand from water and wastewater treatment, chemicals, and paints & coatings industries. The country benefits from advanced chemical manufacturing capabilities and strong industrial infrastructure. High adoption of process optimization solutions across large-scale industries is reinforcing market growth. In addition, continuous innovation in specialty chemical formulations is strengthening the U.S. leadership position in the regional market.

Defoamers Market Share

The defoamers industry is primarily led by well-established companies, including:

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Altana (Germany)

- Dow (U.S.)

- ALLNEX NETHERLANDS B.V. (Netherlands)

- Arkema (France)

- Momentive (U.S.)

- MÜNZING Corporation (Germany)

- ELEMENTS PLC (U.K.)

- Ashland. (U.S.)

- Clariant (Switzerland)

- SAN NOPCO LIMITED (South Korea)

Latest Developments in Global Defoamers Market

- In May 2025, Clariant expanded its production portfolio for sustainable defoamers in Europe, focusing on bio-based and low-VOC formulations for coatings and industrial applications. This expansion strengthens Clariant’s position in the sustainable defoamers market by increasing production capacity for eco-friendly and low-emission solutions across Europe. The move is driven by rising regulatory pressure on VOC reduction and growing demand for green chemistry in coatings, construction materials, and industrial processing. By enhancing availability of bio-based defoamers, the company supports manufacturers transitioning toward sustainable formulations while improving compliance with environmental standards. This also improves supply reliability and accelerates adoption of high-performance sustainable defoaming agents in regulated industries

- In April 2025, PennWhite India (PWI) Private Limited announced plans to establish a foam control chemistry manufacturing plant in Chennai, India. This initiative strengthens domestic production of defoaming agents in India by reducing import dependence and improving supply chain efficiency. The new manufacturing facility under the FoamDoctor brand is expected to support rising demand from wastewater treatment, chemicals, textiles, and industrial processing sectors. It enables faster product availability and cost-effective distribution for local industries, improving overall market responsiveness. The development also reflects India’s growing role as a manufacturing hub for specialty chemicals driven by expanding industrial demand

- In November 2024, Evonik Coating Additives launched TEGO Foamex 16 and TEGO Foamex 11 for waterborne architectural coatings. These product launches enhance Evonik’s defoamer portfolio by offering improved foam control solutions for low, medium, and high PVC coating systems. Designed for waterborne formulations, they support sustainability goals by enabling efficient performance with reduced environmental impact. Their introduction strengthens application efficiency in architectural coatings where foam stability directly affects surface quality and finish consistency. This development supports increasing adoption of advanced defoamers aligned with regulatory and performance requirements in the coatings industry

- In November 2023, BASF expanded defoamer production capacity at its Dilovasi plant in Türkiye. This capacity expansion enhances BASF’s ability to meet rising demand for Foamaster and Foamstar products across South-East Europe, the Middle East, and Africa. It improves regional supply availability and ensures faster delivery of defoaming solutions to key industries such as paints & coatings, chemicals, and industrial processing. The development supports growing industrial activity and increasing need for efficient foam control in large-scale manufacturing. It also strengthens BASF’s production capabilities and market presence across high-demand regions

- In October 2023, Evonik launched TEGO Foamex 8880, a bio-based defoamer for waterborne inks. This launch strengthens sustainable innovation in the defoamers market by introducing a bio-based solution for foam control in printing ink applications. The hybrid technology combining bio-based polymer and polyether siloxane improves foam prevention efficiency while allowing flexible integration during ink manufacturing and application stages. It enhances process stability and print quality while supporting environmental sustainability goals in the packaging and printing industry. This development contributes to the growing shift toward eco-friendly defoaming solutions in waterborne systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Defoamers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Defoamers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Defoamers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.